|

시장보고서

상품코드

1851366

독일의 플라스틱 포장 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Germany Plastic Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

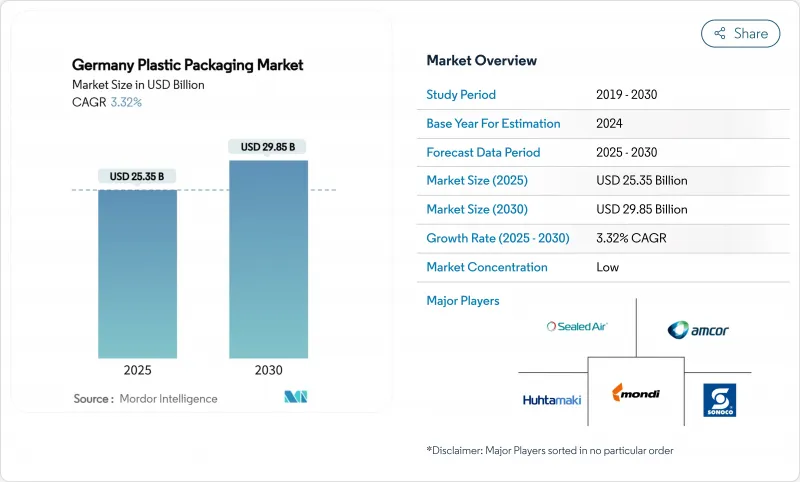

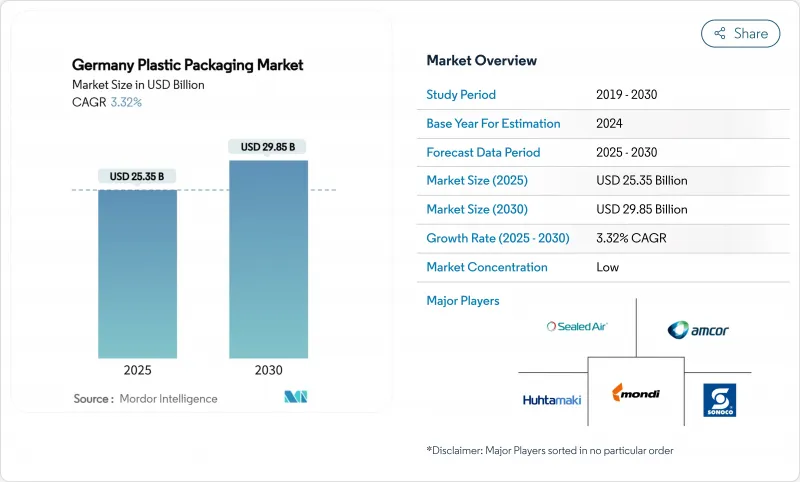

독일의 플라스틱 포장 시장 규모는 2025년에 253억 5,000만 달러로 추정되고, 2030년에는 298억 5,000만 달러에 이를 전망이며, CAGR 3.32%로 안정적으로 추이할 전망입니다.

이 확대는 에너지 비용 상승과 엄격한 규제 요건을 흡수하면서도 순환 경제 설계 원칙으로의 전환이 진행되고 있음을 반영합니다. 식품 포장은 2024년 매출액의 39.32%를 차지했으며, 여전히 양적인 축으로 되어 있지만, 화장품 및 퍼스널케어는 2030년까지 CAGR 5.58%로 페이스세터가 되고 있습니다. 플렉서블 포맷은 전자상거래, 경량 물류, 단일 소재의 채용이 진행됨에 따라 리드를 굳힙니다. 견고한 솔루션에서 PET는 독일의 예금제도와 높은 재활용률로 혜택을 누릴 수 있는 반면, 폴리프로필렌 컴파운드는 자동차 경량화 프로그램에서 견인력을 늘리고 있습니다. 2024년 국내 컨버터의 매출은 4.3% 감소하는 것으로, 독일의 플라스틱 포장 시장은 높은 회수율, 급속한 재료 혁신, 깊은 산업 통합으로 계속 탄력성을 보이고 있습니다.

독일의 플라스틱 포장 시장 동향 및 인사이트

생산자 책임 확대가 재활용 가능한 단일 소재 수요 촉진

독일의 포장 방법은 재활용 가능성에 대한 규제를 강화하고 브랜드 소유자는 복잡한 라미네이트 구조에서 단일 중합체 구조로의 전환을 촉진하고 있습니다. 중앙 포장 등록 기관(ZSVR)은 2024년 최저 기준 업데이트를 발표하고 다층 팩에 높은 컴플라이언스 요금을 부과함으로써 폴리에틸렌과 폴리프로필렌의 단일 소재 배리어 솔루션에 투자를 유도하고 있습니다. 몬디와 프레스냅의 재활용 가능한 단일 소재 반려동물 사료 파우치는 규제 압력이 대규모 상업 전개에 어떻게 반영되는지를 보여줍니다. 또한 이 접근법은 조달팀이 소매업체의 지속가능성 스코어카드에서 높은 점수를 얻고 규정 준수를 시장 차별화 요인으로 바꾸는 데 도움이 됩니다.

독일의 전자상거래 붐이 경량 플렉서블 소포 우편 촉진

온라인 소매는 취급량이 변동하는 가운데 계속 성장하고 있으며, 소포 사업자는 포장 중량을 줄일 필요가 있습니다. DS 스미스는 2024년 독일 패션 물류에서 7억 9,100만 장의 플라스틱 운송 백을 사용했으며, 2030년까지 수요는 42% 증가할 것으로 예측했습니다. 플렉서블 메일러는 치수 중량 수수료와 이산화탄소 배출량을 줄이고 의류 및 소형 전자 기기의 기본 옵션입니다. 아마존이 자사의 풀필먼트 업무에서 플라스틱을 단계적으로 폐지한다고 선언함으로써 타사 판매업자도 추종하게 되어, 재활용 가능한 단일 소재로의 시프트가 가속화합니다.

독일의 플라스틱 세금 0.80 유로/kg안이 버진 수지 가격 급등 초래

2025년 1월에 시행된 단일 사용 플라스틱 기금법은 재활용되지 않은 플라스틱 포장재 1kg당 EUR 0.80을 과세합니다. 연방환경청은 연간 징수액을 14억 유로 가까이로 추정하고 있으며, 버진 폴리머를 사용하는 컨버터에게는 직접적인 타격이 됩니다(umweltbundesamt.de). 2022년 이후 산업용 전기 요금의 265% 인상과 함께 일부 중견 압출업체는 확장 계획을 일시중지하고 있습니다.

부문 분석

폴리에틸렌은 비용 효율성, 씰 무결성, 성숙한 재활용 흐름에 힘입어 2024년 플렉서블 제품 매출의 44.54% 점유율을 유지했습니다. 2025년 폴리에틸렌 형식 시장 규모는 113억 달러로 컨버터가 EVOH가 없는 산소 장벽이 있는 모노머티리얼 파우치를 전개함에 따라 상승을 계속하고 있습니다. 재활용 가능한 폴리올레핀 기반 종이 터치 라미네이트와 같은 신흥 필름은 CAGR 6.87%로 확대되어 이는 생산자 책임 수수료의 리베이트를 해제하는 경량이고 높은 장벽 구조의 연구개발 투자가 지속되고 있음을 보여줍니다.

다른 경질 수지도 마찬가지입니다. PET는 보증금 수익 제도로 리지드 수익의 33.36%를 차지하고 있지만, 폴리프로필렌은 2030년까지 연평균 복합 성장률(CAGR) 5.76%로 다른 리지드 기재를 상회할 전망입니다. 폴리프로필렌의 치수 안정성과 내열성은 반찬 트레이 및 EV 배터리 케이싱에 적합하며 소비자 및 산업용 모두에서 수요가 강화되었습니다. 반대로 PVC와 폴리스티렌은 재활용 관련 정책의 역풍을 겪으며 계속 견인력을 잃고 있습니다.

플렉서블 솔루션은 2024년 매출의 54.1%를 차지했으며, 독일 플라스틱 포장 시장의 주요 제품으로서의 역할을 입증했습니다. 스탠드업 파우치, 프레지핑 백, Form Fill Seal 웹은 리지드 탭에 비해 최대 70%의 재료 절약을 실현하여 환경 대책 요금을 지불하는 브랜드 소유자에게 결정적인 이점이 됩니다. 이 부문은 2030년까지 CAGR 4.61%로 성장할 전망이며, 리지드 포맷을 능가하고 있습니다. 이는 유연한 라인이 낮은 자본이어서 전환 속도가 빠르기 때문에 컨버터가 전자상거래와 관련된 변동 런 사이즈를 흡수하는 데 도움이 되기 때문입니다.

견고한 용기는 치수 안정성이 필요한 탄산 음료, 화장품 용기, 의약품 용도에 여전히 필수적입니다. PET 병은 93%의 인수율과 높은 광학 투명도를 달성하여 식품용 rPET 루프의 오염을 방지합니다. 반면 SCHOTT Pharma의 판지 기반 주사기 지갑은 병원의 폐기물 분류 프로토콜에 맞추어 고가치 의료기기에서도 섬유 슬래시 및 플라스틱 하이브리드를 테스트하고 있음을 입증합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 확대 생산자 책임(VerpackG) 의무화가 재활용 가능한 단일 소재 수요 견인

- 독일의 전자상거래 붐이 경량 플렉서블 소포 우편 촉진

- 금속에서 경질 플라스틱으로 시프트하는 독일의 자동차 및 산업 분야의 경량화

- 재사용 가능 PET 리필 할당이 rPET 프리폼과 병의 사용 가속

- 편리한 식사 문화가 전자레인지 대응 플라스틱 트레이 촉진

- 콜드체인 생물 제제의 파이프라인이 의료용 플라스틱 바이알과 블리스터 수요 확대

- 시장 성장 억제요인

- 독일의 플라스틱세 0.80유로/kg안이 버진 수지 가격 촉진

- 소매 주도의 섬유 시프트(알디, 레베, 리들) 플라스틱 선반 점유율 축소

- 독일의 높은 전기세가 컨버터의 변환 마진 인상

- 한정된 식품용 rPCR 공급이 재생 이용 목표의 달성 방해

- 공급망 분석

- 규제 전망

- 기술의 전망

- 무역 시나리오(관련 HS 코드 아래)

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 재활용 및 지속가능성의 전망

제5장 시장 규모 및 성장 예측

- 소재 유형별

- 경질 플라스틱

- 폴리에틸렌

- 폴리프로필렌(PP)

- 폴리에틸렌테레프탈레이트(PET)

- 폴리염화비닐(PVC)

- 폴리스티렌(PS) 및 발포 폴리스티렌(EPS)

- 기타 경질 플라스틱

- 플렉서블 플라스틱

- 폴리에틸렌

- 2축 연신 폴리프로필렌(BOPP)

- 캐스트 폴리프로필렌(CPP)

- 폴리염화비닐(PVC)

- 에틸렌비닐알코올(EVOH)

- 기타 플렉서블 플라스틱

- 경질 플라스틱

- 패키징 유형별

- 경질 플라스틱 포장

- 병 및 단지

- 트레이 및 클램쉘

- 팔레트 및 나무 프레임

- 기타 경질 플라스틱 포장

- 연질 플라스틱 포장

- 파우치

- 가방

- 필름 및 랩

- 기타 연질 플라스틱 포장

- 경질 플라스틱 포장

- 최종 이용 산업별

- 식품

- 과자류 및 스낵 과자

- 빵 및 시리얼

- 신선한 식품

- 유제품

- 기타 식품

- 음료

- 병 워터

- 주스 및 넥터

- 우유 음료

- 탄산 음료

- 기타 음료

- 의약품

- 화장품 및 퍼스널케어

- 공업용

- 반려동물 사료 및 동물 관리

- 기타 최종 이용 산업

- 식품

- 유통 채널별

- 직접 판매 채널

- 간접 판매 채널

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Amcor plc

- Constantia Flexibles Group

- Alpla Werke Alwin Lehner GmbH

- Sudpack Verpackungen GmbH & Co. KG

- Gerresheimer AG

- Klockner Pentaplast GmbH

- Paccor Packaging GmbH

- Mondi Group(Germany)

- Huhtamaki Oyj(Germany)

- Schur Flexibles Holding GmbH

- Bischof Klein SE & Co. KG

- Greiner Packaging GmbH

- Sealed Air Corporation

- Sonoco Products Company

- Coveris Holding SA

- Wipak Walsrode GmbH & Co. KG

- Tetra Laval Group

- Silgan Holdings Inc.

- Plastipak Holdings Inc.

제7장 시장 기회 및 향후 전망

AJY 25.11.21The Germany plastic packaging market size stood at USD 25.35 billion in 2025 and is on course to reach USD 29.85 billion by 2030, advancing at a steady 3.32% CAGR.

The expansion reflects the sector's ongoing transition toward circular-economy design principles while absorbing higher energy costs and stringent regulatory demands. Food packaging remains the anchor for volume, accounting for 39.32% of 2024 revenues, yet cosmetics and personal care is the pace-setter with a 5.58% CAGR through 2030. Flexible formats consolidate their lead as e-commerce, lightweight logistics and mono-material adoption intensify. In rigid solutions, PET benefits from Germany's deposit system and high recycling rates, whereas polypropylene compounds gain traction in automotive light-weighting programs. Despite a 4.3% decline in domestic converter turnover during 2024, the Germany plastic packaging market continues to demonstrate resilience through high collection rates, rapid material innovation and deep industrial integration.

Germany Plastic Packaging Market Trends and Insights

Extended Producer Responsibility mandates driving recyclable mono-material demand

Germany's Packaging Act tightens recyclability rules, prompting brand owners to shift from complex laminates toward single-polymer structures. The Central Agency Packaging Register (ZSVR) released updated minimum standards in 2024 that attach higher compliance fees to multi-layer packs, channeling investment into mono-material polyethylene and polypropylene barrier solutions. Mondi and Fressnapf's recyclable mono-material pet-food pouch exemplifies how regulatory pressure is translating into large-scale commercial roll-outs. The approach also helps procurement teams score higher on retailer sustainability scorecards, turning compliance into a market differentiator.

E-commerce boom in Germany fueling lightweight flexible parcel mailers

Online retail keeps growing even as volumes fluctuate, pushing parcel operators to trim packing weight. DS Smith estimates 791 million plastic shipping bags were deployed in German fashion logistics during 2024 with unit demand projected to rise 42% to 2030. Flexible mailers reduce dimensional weight fees and carbon emissions, making them the default choice for apparel and small electronics. Amazon's pledge to phase out plastics in its own fulfillment operations pressures third-party sellers to follow, accelerating the shift toward mono-material recyclables.

Proposed EUR 0.80/kg German plastics tax inflating virgin resin prices

The Single-Use Plastics Fund Act that entered force in January 2025 levies EUR 0.80 on every kilogram of non-recycled plastic packaging. The Federal Environment Agency estimates annual collections near EUR 1.4 billion, a direct hit on converters working with virgin polymer streams umweltbundesamt.de. The measure sharpens the financial case for recycled content but also squeezes margins where food-grade rPET or rPP supply remains tight. Coupled with a 265% spike in industrial electricity tariffs since 2022, several mid-sized extruders have paused expansion plans.

Other drivers and restraints analyzed in the detailed report include:

- Automotive & industrial lightweighting shifting from metal to rigid plastics

- Mehrweg PET refill quotas accelerating rPET preform and bottle usage

- Retailer-led fiber shift shrinking plastic shelf share

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polyethylene retained 44.54% share of flexible revenues in 2024, underpinned by cost efficiency, high seal integrity and mature recycling streams. The Germany plastic packaging market size for polyethylene formats stood at USD 11.3 billion in 2025 and continues to edge upward as converters roll out mono-material pouches with EVOH-free oxygen barriers. Emerging films such as recyclable polyolefin-based paper-touch laminates are expanding at 6.87% CAGR, indicating sustained R&D investment in lightweight, high-barrier structures that unlock producer responsibility fee rebates.

Other rigid resins tell a similar story. PET captured 33.36% share of rigid revenues thanks to the deposit-return system, while polypropylene outpaces other rigid substrates with a 5.76% CAGR through 2030. Polypropylene's dimensional stability and heat resistance suit it for ready-meal trays and EV battery casings, reinforcing its demand in both consumer and industrial verticals. Conversely PVC and polystyrene continue to lose traction under recycling-related policy headwinds.

Flexible solutions held 54.1% share of 2024 revenues, validating their role as the workhorse of the Germany plastic packaging market. Stand-up pouches, pre-zipped bags and form-fill-seal webs deliver material savings of up to 70% compared with rigid tubs, a decisive advantage for brand owners paying modulated eco-fees. The segment's 4.61% CAGR through 2030 eclipses rigid formats because flexible lines require lower capital and operate at faster change-over speeds, helping converters absorb fluctuating run sizes linked to e-commerce.

Rigid containers remain indispensable for carbonated beverages, cosmetics jars and pharma applications requiring dimensional stability. PET bottles achieve 93% take-back and high optical clarity, preventing contamination of food-grade rPET loops. Meanwhile, SCHOTT Pharma's cardboard-based syringe wallet demonstrates how even high-value medical devices are testing fiber-slash-plastic hybrids to align with hospital waste-segregation protocols.

The Germany Plastic Packaging Market Report is Segmented by Material Type (Rigid Plastic, Flexible Plastic), Packaging Type (Rigid: Bottles and Jars, Trays and Clamshells, Other Rigid; Flexible: Pouches, Bags and Sacks, Films and Wraps, Other Flexible), End-Use Industry (Food, Beverage, Pharmaceutical, and More), and Distribution Channels (Direct Sales, Indirect Sales). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Amcor plc

- Constantia Flexibles Group

- Alpla Werke Alwin Lehner GmbH

- Sudpack Verpackungen GmbH & Co. KG

- Gerresheimer AG

- Klockner Pentaplast GmbH

- Paccor Packaging GmbH

- Mondi Group (Germany)

- Huhtamaki Oyj (Germany)

- Schur Flexibles Holding GmbH

- Bischof + Klein SE & Co. KG

- Greiner Packaging GmbH

- Sealed Air Corporation

- Sonoco Products Company

- Coveris Holding SA

- Wipak Walsrode GmbH & Co. KG

- Tetra Laval Group

- Silgan Holdings Inc.

- Plastipak Holdings Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Extended Producer Responsibility (VerpackG) Mandates Driving Recyclable Mono-Material Demand

- 4.2.2 E-commerce Boom in Germany Fueling Lightweight Flexible Parcel Mailers

- 4.2.3 Lightweighting in German Automotive and Industrial Sectors Shifting from Metal to Rigid Plastics

- 4.2.4 Mehrweg PET Refill Quotas Accelerating rPET Preform and Bottle Usage

- 4.2.5 Convenience-Ready Meal Culture Boosting Microwave-Suitable Plastic Trays

- 4.2.6 Cold-Chain Biologics Pipeline Expanding Demand for Medical-Grade Plastic Vials and Blisters

- 4.3 Market Restraints

- 4.3.1 Proposed € 0.80/kg German Plastics Tax Inflating Virgin Resin Prices

- 4.3.2 Retailer Led Fiber Shift (Aldi, REWE, Lidl) Shrinking Plastic Shelf Share

- 4.3.3 High German Electricity Costs Raising Conversion Margins for Converters

- 4.3.4 Limited Food-Grade rPCR Supply Curtailing Recycled Content Targets

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Trade Scenario (Under Relevant HS Code)

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Recycling and Sustainability Landscape

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Rigid Plastic

- 5.1.1.1 Polyethylene (PE)

- 5.1.1.2 Polypropylene (PP)

- 5.1.1.3 Polyethylene Terephthalate (PET)

- 5.1.1.4 Polyvinyl Chloride (PVC)

- 5.1.1.5 Polystyrene (PS) and Expanded Polystyrene (EPS)

- 5.1.1.6 Other Rigid Plastic

- 5.1.2 Flexible Plastic

- 5.1.2.1 Polyethylene (PE)

- 5.1.2.2 Biaxially Oriented Polypropylene (BOPP)

- 5.1.2.3 Cast Polypropylene (CPP)

- 5.1.2.4 Polyvinyl Chloride (PVC)

- 5.1.2.5 Ethylene-Vinyl Alcohol (EVOH)

- 5.1.2.6 Other Flexible Plastic

- 5.1.1 Rigid Plastic

- 5.2 By Packaging Type

- 5.2.1 Rigid Plastic Packaging

- 5.2.1.1 Bottles and Jars

- 5.2.1.2 Trays and Clamshells

- 5.2.1.3 Pallets and Crates

- 5.2.1.4 Other Rigid Plastic Packaging

- 5.2.2 Flexible Plastic Packaging

- 5.2.2.1 Pouches

- 5.2.2.2 Bags and Sacks

- 5.2.2.3 Films and Wraps

- 5.2.2.4 Other Flexible Plastic Packaging

- 5.2.1 Rigid Plastic Packaging

- 5.3 By End-use Industry

- 5.3.1 Food

- 5.3.1.1 Confectionery and Snacks

- 5.3.1.2 Breads and Cereals

- 5.3.1.3 Fresh Produce

- 5.3.1.4 Dairy based products

- 5.3.1.5 Other Food Products

- 5.3.2 Beverage

- 5.3.2.1 Bottled Water

- 5.3.2.2 Juices and Nectars

- 5.3.2.3 Dairy Based Beverages

- 5.3.2.4 Carbonated Soft Drinks

- 5.3.2.5 Other Beverages

- 5.3.3 Pharmaceutical

- 5.3.4 Cosmetics and Personal Care

- 5.3.5 Industrial

- 5.3.6 Pet Food and Animal Care

- 5.3.7 Other End-use Industry

- 5.3.1 Food

- 5.4 By Distribution Channels

- 5.4.1 Direct Sales Channels

- 5.4.2 Indirect Sales Channels

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Amcor plc

- 6.4.2 Constantia Flexibles Group

- 6.4.3 Alpla Werke Alwin Lehner GmbH

- 6.4.4 Sudpack Verpackungen GmbH & Co. KG

- 6.4.5 Gerresheimer AG

- 6.4.6 Klockner Pentaplast GmbH

- 6.4.7 Paccor Packaging GmbH

- 6.4.8 Mondi Group (Germany)

- 6.4.9 Huhtamaki Oyj (Germany)

- 6.4.10 Schur Flexibles Holding GmbH

- 6.4.11 Bischof + Klein SE & Co. KG

- 6.4.12 Greiner Packaging GmbH

- 6.4.13 Sealed Air Corporation

- 6.4.14 Sonoco Products Company

- 6.4.15 Coveris Holding SA

- 6.4.16 Wipak Walsrode GmbH & Co. KG

- 6.4.17 Tetra Laval Group

- 6.4.18 Silgan Holdings Inc.

- 6.4.19 Plastipak Holdings Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment