|

시장보고서

상품코드

1851759

연속 혈당 모니터링(CGM) : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Continuous Glucose Monitoring (CGM) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

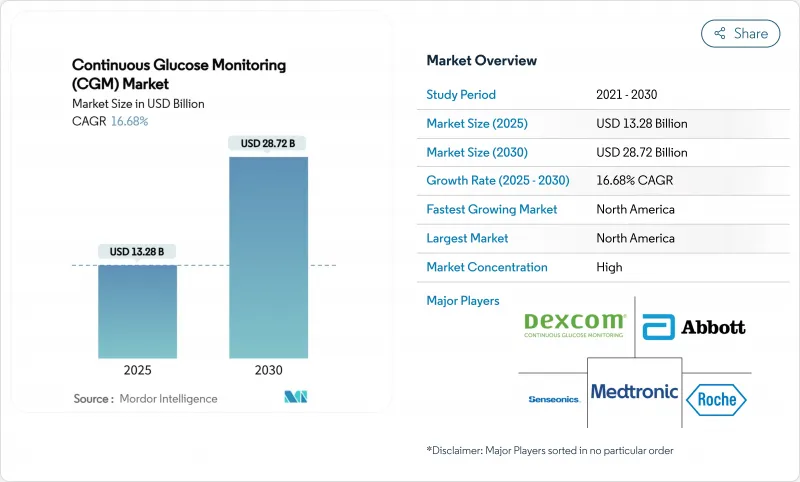

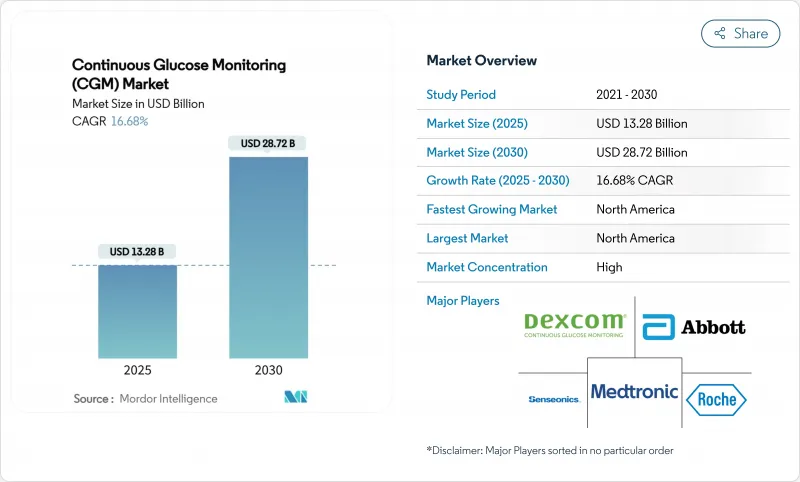

연속 혈당 모니터링(CGM) 시장 규모는 2025년에 132억 7,519만 달러로 평가되었고 2030년에는 287억 1,526만 달러에 이를 것으로 예측되며, CAGR은 16.68%를 나타낼 전망입니다.

센서 소형화, 지원적 보험급여, 소비자 웰니스와 의료적 필요성의 융합이 견고한 성장의 원동력입니다. 북미가 매출 창출을 주도하지만, 스마트폰 보급률과 당뇨병 유병률이 수렴하면서 아시아태평양 지역이 가장 빠른 시장 확대를 기록 중입니다. 지속적인 기기-소프트웨어 융합은 반복적 수익원을 창출하여 기존 업체들이 하드웨어와 분석 구독 서비스를 묶어 판매하도록 유도합니다. 한편, 이식형 및 비침습형 프로토타입은 연속 혈당 모니터링 시장이 예방 및 웰니스 중심의 활용 사례로 확대될 것이라는 기대를 부추긴다.

세계의 연속 혈당 모니터링(CGM) 시장 동향 및 인사이트

당뇨병의 유병률 상승과 조기 진단

발병률 가속화는 구조적 수요를 뒷받침합니다. 2형 당뇨병이 전체 사례의 96%를 차지하며 아시아태평양 지역에서 발병 연령이 낮아지는 추세이기 때문입니다. 현재 해당 지역의 발병 연령 중앙값은 45세 미만으로, 수십 년에 걸친 모니터링 기간을 창출하고 있습니다(IDF). 인공지능 기반 선진화된 검진 기술은 위험군을 조기에 식별하여 예방적 센서 사용을 촉진합니다. 메디케어의 2024년 정책은 저혈당 발작이 있는 제2형 당뇨병 환자의 접근성을 확대하여 즉시 보험 가입자 기반을 증가시켰습니다. 이미 연평균 18.41% 성장 중인 소아 시장도 보호자들이 학교 및 스포츠 환경에서의 안전망으로 지속적인 추적을 인식함에 따라 이 흐름을 타고 있습니다.

원격 모니터링 및 원격 의료 통합의 급속한 보급

실시간 데이터 스트림은 추가 인력 없이 더 많은 환자를 관리할 수 있게 하며, 미국 CPT 코드 보상 제도는 원격 환자 모니터링 키트를 도입한 의료 제공자에게 혜택을 부여합니다. 미국 및 유럽 전역의 농촌 지역 환자들은 장거리 이동 없이도 전문의의 관리를 받게 되어 치료 순응도와 혈당 조절이 개선됩니다. 스마트폰 전용 앱은 별도 수신기 비용을 절감하여 젊은 기술 친화적 사용자들의 진입 장벽을 낮춥니다.

지불자와 환자에게 부담되는 높은 기기 및 소모품 비용

10-14일마다 교체가 필요한 센서는 미국 메디케어 수혜자에게 공동부담금 적용 후 월 100-200달러의 비용이 발생하여 고정 소득에 부담을 줍니다. 저소득 및 중간 소득 국가에서는 보조금 미적용 소매 가격이 평균 월급을 초과합니다. 구독 모델이 진입 비용을 낮추지만 여전히 많은 이들에게는 접근이 어렵습니다. 혁신적인 사용량 기반 또는 성과 기반 계약이 재정적 장벽을 완화할 수 있으나, 광범위한 도입은 아직 초기 단계입니다.

부문 분석

센서는 2024년 매출의 84.89%를 차지하며 17.84%의 연평균 성장률(CAGR)을 기록, 필수적인 생리적 접점으로서의 역할을 입증했습니다. 지속적인 소재 혁신으로 주류 일회용 제품의 착용 기간이 10일에서 14일로 연장되었으며, 이식형 제품은 연간 교체 주기를 약속합니다. 수명 연장은 직접적으로 평생 소유 비용을 낮추어, 센서 기반 연속 혈당 모니터링 시장 규모가 매출 성장의 주된 동력이 되었습니다. 반면, 블루투스 저에너지 모듈과 휴대폰 직접 연결 아키텍처가 해당 계층을 상품화함에 따라 송신기 하드웨어는 6.19%의 연평균 성장률만을 기록했습니다. 플랫폼 공급업체들은 이제 송신기 기능을 센서 하우징이나 스마트폰 앱에 통합하여 단위 마진을 압박하지만, 간소화된 설정으로 소비자를 사로잡고 있습니다.

2세대 센서 화학 기술은 효소 안정화와 폴리머 막을 활용해 드리프트를 억제함으로써, 보다 공격적인 인슐린 투여 알고리즘과 자동 인슐린 전달 시스템 통합을 가능케 합니다. 글루코트랙(Glucotrack)과 센소닉스(Senseonics)의 이식형 솔루션은 저프로파일·유지보수 부담이 적은 기기로의 전환을 보여줌으로써, 기존에 서비스가 부족했던 직업 및 운동 분야 시장을 개척할 수 있습니다. 센서가 반이식형 자산으로 진화함에 따라, 소프트웨어 분석 및 클라우드 구독 서비스가 점유율을 확대하며 가치 창출의 중심이 하드웨어에서 종단적 데이터 서비스로 전환되고 있습니다.

지역 분석

북미는 확고한 보험 체계와 높은 기기 활용도를 바탕으로 2024년 51.01%의 점유율을 유지했습니다. 해당 지역은 2030년까지 연평균 18.24%의 성장률로 73억 달러의 증분 매출을 추가할 것으로 전망됩니다. 메디케어의 2024년 4월 정책은 저혈당 증상이 확인된 제2형 당뇨병 환자의 적용 대상 확대를 통해 잠재적 성인 환자 집단을 개방하고 지속적인 단위 성장을 보장했습니다. 캐나다의 단일 지불자 시스템은 전국적으로 처방 목록을 통일하여 주간 격차를 완화하는 반면, 멕시코의 사회보장 개혁은 도시 중심지에서 기기 환급 범위를 확대하고 있습니다.

아시아태평양 지역은 현재 18.18%의 점유율을 기록하며 16.08%라는 가장 가파른 연평균 성장률을 보이고 있습니다. 중국 국가급 약품 목록은 2025년부터 센서 포함 시범 운영을 시작했으며, 국내 제조사들은 2선 도시 수요 충족을 위해 생산 규모를 확대 중입니다. 인도의 높은 스마트폰 보급률과 종량제 보험 앱은 가정의 진입 장벽을 낮춥니다. 일본과 한국은 소비자 가전 대기업들이 다목적 웨어러블에 혈당 모듈을 내장함에 따라 높은 1인당 보급률을 유지하며, 이 추세는 동남아시아 전역으로 확산될 전망입니다.

유럽은 보편적 의료 보장 및 통합 조달 체계에 힘입어 중간 단일자리 수 성장률을 기록 중입니다. 독일은 제1형 당뇨병 환자의 표준 치료법으로 CGM을 적극 권장하며, 영국 국민건강보험(NHS) 장기 계획은 공장 보정 모델로의 하드웨어 업그레이드 비용을 지원합니다. 동유럽 시장은 미개척 영역으로 부상 중이며, 체코와 폴란드는 2025년 EU 구조 기금을 활용한 시범 자금 지원 프로그램을 도입해 당뇨병 치료 현대화를 추진 중입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 당뇨병 유병률의 상승 및 조기 진단

- 원격 모니터링과 원격 의료 통합의 급속한 보급

- 센서 소형화와 정밀도의 비약적 향상

- OECD 및 중국에서의 유리한 보험급여 확대

- 진단된 당뇨병을 넘어선 소비자 웰니스 시장 확대

- 저소득 및 중간소득 국가 진입 장벽을 낮추는 구독형 가격 정책

- 시장 성장 억제요인

- 지불자와 환자에게 부담되는 높은 기기 및 소모품 비용

- 교정/데이터 과부하로 인한 사용성 문제

- 혈당 측정 빈도 감소시키는 GLP-1 체중 감량제

- 사이버 보안 및 데이터 프라이버시 취약성

- 공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 유병률 지표

- 1형 당뇨병 인구

- 2형 당뇨병 인구

제5장 시장 규모와 성장 예측

- 컴포넌트별

- 센서

- 송신기

- 수신기

- 최종 사용자별

- 병원/클리닉

- 홈/개인

- 인구 통계별

- 성인용

- 소아용

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 일본

- 한국

- 중국

- 인도

- 호주

- 베트남

- 말레이시아

- 인도네시아

- 필리핀

- 태국

- 기타 아시아태평양

- 중동 및 아프리카

- 사우디아라비아

- 이란

- 이집트

- 오만

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Abbott Laboratories

- Medtronic plc

- Dexcom Inc.

- Senseonics Holdings Inc.

- F. Hoffmann-La Roche Ltd

- A. Menarini Diagnostics Srl

- i-SENS, Inc.

- Medtrum Technologies Inc.

- Nemaura Medical Inc.

- Zhejiang POCTech Co.,Ltd.

- MicroTech Medical

제7장 시장 기회와 장래의 전망

HBR 25.11.17The continuous glucose monitoring market size stands at USD 13,275.19 million in 2025 and is set to reach USD 28,715.26 million by 2030, advancing at a 16.68% CAGR.

Robust growth stems from sensor miniaturization, supportive reimbursement, and the blending of consumer wellness with medical necessity. North America leads revenue generation, but Asia Pacific records the fastest uptake as smartphone penetration and diabetes prevalence converge. Ongoing device-software convergence creates recurring revenue streams that entice incumbents to bundle hardware with analytics subscriptions. Meanwhile, implantable and non-invasive prototypes foster expectations that the continuous glucose monitoring market will broaden into preventive and wellness-oriented use cases.

Global Continuous Glucose Monitoring (CGM) Market Trends and Insights

Rising Prevalence of Diabetes and Earlier Diagnosis

Accelerating incidence underpins structural demand because type 2 accounts for 96% of cases and is trending younger in Asia Pacific, where the median onset now falls below 45 years, creating decades-long monitoring horizons, IDF. Enhanced screening powered by artificial intelligence identifies at-risk cohorts earlier, prompting preventive sensor use. Medicare's 2024 policy opened access for type 2 patients with hypoglycemic episodes, instantly raising the insured base. Pediatric adoption, already growing at 18.41% CAGR, rides this wave as caregivers view continuous tracking as a safety net for school and sports environments.

Rapid Uptake of Remote Monitoring and Tele-Health Integration

Real-time data streams allow clinicians to manage more people without extra staff, and U.S. CPT-code reimbursements reward providers who deploy remote patient-monitoring kits. Rural patients in the United States and across Europe gain specialist oversight without long drives, improving adherence and glycemic control. Smartphone-native apps cut dedicated receiver costs, lifting barriers for younger, tech-savvy users.

High Device and Consumable Costs for Payers and Patients

Sensors that require replacement every 10-14 days cost USD 100-200 per month for U.S. Medicare beneficiaries after coinsurance, straining fixed incomes. In low- and middle-income countries, unsubsidized retail prices exceed average monthly wages. Although subscription models lower entry costs, they remain out of reach for many. Innovative pay-per-use or outcomes-based contracts could mitigate financial hurdles, yet broad implementation is still nascent.

Other drivers and restraints analyzed in the detailed report include:

- Sensor Miniaturization and Accuracy Breakthroughs

- Favorable Reimbursement Expansion in OECD & China

- GLP-1 Weight-Loss Drugs Reducing Glucose Testing Frequency

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Sensors delivered 84.89% revenue in 2024, underpinning a 17.84% CAGR that reflects their role as the indispensable physiological touchpoint. Continuous material innovation increased wear life from 10 to 14 days on mainstream disposables, while implantable variants promise annual exchange intervals. Extended longevity directly lowers lifetime ownership costs, making the continuous glucose monitoring market size for sensors the primary engine of topline expansion. Transmitter hardware, by contrast, booked just a 6.19% CAGR as Bluetooth Low Energy modules and direct-to-phone architecture commoditize that layer. Platform vendors now bundle transmitter functions into sensor housings or smartphone apps, pressuring unit margins but captivating consumers through simplified setups.

Second-generation sensor chemistry leverages enzyme stabilization and polymer membranes to curtail drift, enabling more aggressive insulin dosing algorithms and automated insulin delivery integration. Implantable solutions from Glucotrack and Senseonics highlight a migration toward low-profile, maintenance-light devices that could open occupational and athletic niches previously underserved. As sensors evolve into semi-implantable assets, software analytics and cloud subscriptions accrue increasing wallet share, pivoting value creation away from hardware toward longitudinal data services.

The Continuous Glucose Monitoring (CGM) Market Report is Segmented by Component (Sensors, Transmitters, Receivers), End User (Hospitals/Clinics, Home/Personal), Demography (Adult, Paediatric), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 51.01% share in 2024, supported by entrenched insurance frameworks and high device literacy. The region is forecast to add USD 7.3 billion in incremental sales at an 18.24% CAGR to 2030. Medicare's April 2024 policy expanded eligibility to type 2 diabetics with documented hypoglycemia, unlocking a latent adult cohort and ensuring sustained unit growth. Canada's single-payer system aligns formularies nationally, smoothing provincial disparities, while Mexico's social-security reforms broaden device reimbursement in urban centers.

Asia Pacific, now at 18.18% share, records the steepest CAGR of 16.08%. China's National Reimbursement Drug List began piloting sensor inclusion in 2025, and domestic manufacturers are scaling to meet tier-2 city demand. India's high smartphone penetration, coupled with pay-as-you-go insurance apps, lowers household entry barriers. Japan and South Korea maintain high per-capita uptake because consumer-electronics majors embed glucose modules into multipurpose wearables, a trend likely to ripple across Southeast Asia.

Europe offers mid-single-digit growth underpinned by universal coverage and coordinated procurement. Germany champions CGM as the standard of care for type 1 patients, while the United Kingdom's NHS Long-Term Plan subsidizes hardware upgrades to factory-calibrated models. Eastern European markets emerge as white space; Czechia and Poland introduced pilot funding in 2025, leveraging EU structural funds to modernize diabetes care.

- Abbott Laboratories

- Medtronic

- Dexcom

- Senseonics

- Roche

- A. Menarini Diagnostics S.r.l.

- I-Sens

- Medtrum Technologies Inc.

- Nemaura Medical Inc.

- Zhejiang POCTech Co.,Ltd.

- MicroTech Medical

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of Diabetes and Earlier Diagnosis

- 4.2.2 Rapid Uptake of Remote Monitoring and Tele-Health Integration

- 4.2.3 Sensor Miniaturization and Accuracy Breakthroughs

- 4.2.4 Favorable Reimbursement Expansion in OECD & China

- 4.2.5 Consumer-Wellness Expansion Beyond Diagnosed Diabetes

- 4.2.6 Subscription Pricing Lowering LMIC Entry Barriers

- 4.3 Market Restraints

- 4.3.1 High Device and Consumable Costs for Payers And Patients

- 4.3.2 Calibration / Data-Overload Usability Concerns

- 4.3.3 GLP-1 Weight-Loss Drugs Reducing Glucose Testing Frequency

- 4.3.4 Cyber-Security and Data-Privacy Vulnerabilities

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Disease-Prevalence Indicators

- 4.8.1 Type-1 Diabetes Population

- 4.8.2 Type-2 Diabetes Population

5 Market Size & Growth Forecasts (Value)

- 5.1 By Component

- 5.1.1 Sensors

- 5.1.2 Transmitters

- 5.1.3 Receivers

- 5.2 By End User

- 5.2.1 Hospitals / Clinics

- 5.2.2 Home / Personal

- 5.3 By Demography

- 5.3.1 Adult

- 5.3.2 Paediatric

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 Japan

- 5.4.3.2 South Korea

- 5.4.3.3 China

- 5.4.3.4 India

- 5.4.3.5 Australia

- 5.4.3.6 Vietnam

- 5.4.3.7 Malaysia

- 5.4.3.8 Indonesia

- 5.4.3.9 Philippines

- 5.4.3.10 Thailand

- 5.4.3.11 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 Saudi Arabia

- 5.4.4.2 Iran

- 5.4.4.3 Egypt

- 5.4.4.4 Oman

- 5.4.4.5 South Africa

- 5.4.4.6 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 Medtronic plc

- 6.3.3 Dexcom Inc.

- 6.3.4 Senseonics Holdings Inc.

- 6.3.5 F. Hoffmann-La Roche Ltd

- 6.3.6 A. Menarini Diagnostics S.r.l.

- 6.3.7 i-SENS, Inc.

- 6.3.8 Medtrum Technologies Inc.

- 6.3.9 Nemaura Medical Inc.

- 6.3.10 Zhejiang POCTech Co.,Ltd.

- 6.3.11 MicroTech Medical

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment