|

시장보고서

상품코드

1851995

자동차용 반도체 시장: 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Automotive Semiconductor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

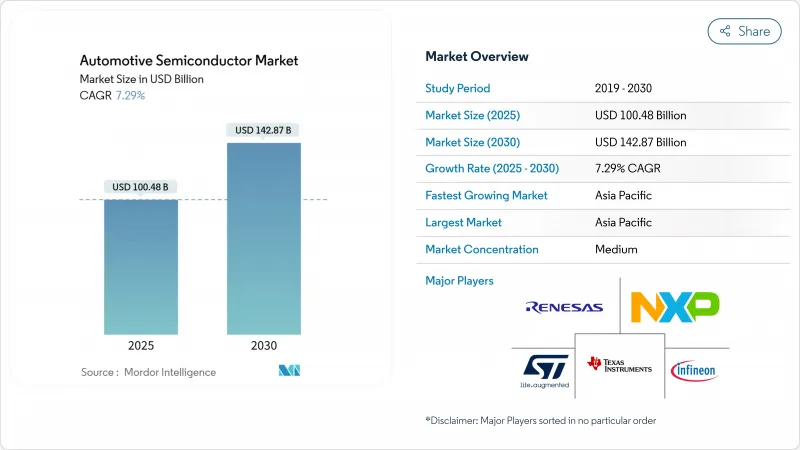

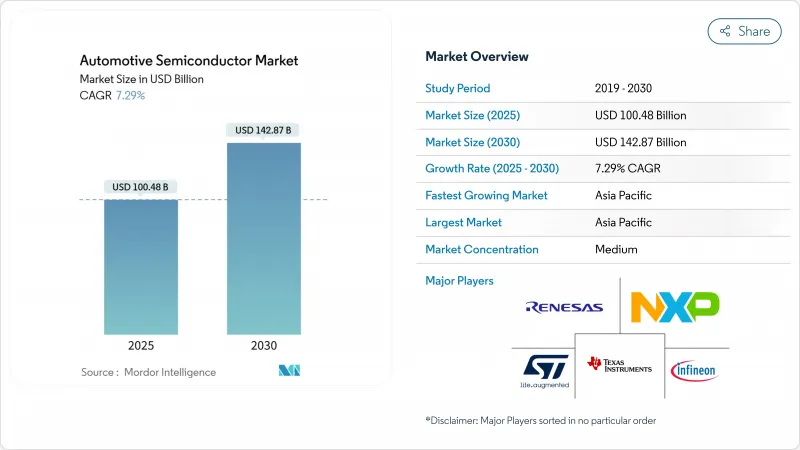

자동차용 반도체 시장 규모는 2025년에 1,004억 8,000만 달러로 추정되고, CAGR 7.29%로 확대될 전망이며, 2030년에는 1,428억 7,000만 달러에 달할 것으로 예측됩니다.

전동화의 의무화, 선진 운전 지원 기능의 급속한 채용, 소프트웨어로 정의된 자동차에 대한 축족은 모든 차량 클래스에서 실리콘의 함량을 높여줍니다. 자동차 제조업체는 장기적인 주조 능력 확보를 경쟁하고 있으며, 존 아키텍처의 보급으로 고성능 프로세서, 메모리, 파워 디바이스에 투자가 집중되고 있습니다. 멀티소싱 전략과 결합된 공급망 탄력성 프로그램은 조달을 재구성하고 있으며, 와이드 밴드갭 디바이스와 통합 파워 모듈은 성숙한 노드 구성 요소가 정상화되어도 가격 결정력을 유지할 수 있는 새로운 디자인 인 기회를 열고 있습니다.

세계의 자동차용 반도체 시장 동향 및 인사이트

전동화로 자동차당 반도체 컨텐츠 증가

배터리 전동 플랫폼에는 내연 모델에 없는 파워 일렉트로닉스, 배터리 관리 IC 및 열 관리 컨트롤러가 추가됩니다. 400V에서 800V 전기 시스템으로의 전환에는 낮은 스위칭 손실로 더 높은 전압을 유지하는 실리콘 카바이드(SiC) MOSFET이 필요합니다. 인피니언 트렌치 기반 SiC 슈퍼 접합 디바이스는 40% 낮은 저항과 25% 높은 전류 성능을 제공하여 트랙션 인버터의 소형화 및 충전 시간 단축을 가능하게 합니다. NXP의 초광대역 무선 배터리 관리 시스템은 무거운 케이블 배선을 제거하고 차량 무게를 줄이고 에너지 밀도가 높은 팩을 위한 공간을 확보합니다. 고전압 아키텍처에는 향상된 절연, 게이트 드라이버 및 고정밀 전류 센서도 필요합니다. 이러한 요인을 종합하면 EV 1대당 반도체 비용이 기존 자동차의 몇 배나 상승합니다.

고급 안전 및 쾌적 시스템에 대한 수요 증가

레벨 2 운전 지원 패키지는 레이더, LiDAR, 고해상도 카메라와 같은 멀티모달 센서 제품군을 통합하여 시간당 테라바이트 데이터를 생성합니다. 실시간 센서 퓨전 워크로드에는 애플리케이션별 프로세서와 임베디드 신경망 가속기가 필요합니다. NXP의 28nm RFCMOS 레이더 원칩 제품군은 360도 커버리지와 통합 AI 객체 분류를 제공하여 부품 비용을 줄이고 시스템 아키텍처를 간소화합니다. ams 오스람의 8채널 펄스 레이저와 같은 보완적인 광학 기술 혁신은 1,000W의 피크 광 출력을 제공하여 고속도로의 자동 조종 기능을 위한 LiDAR 범위를 확장합니다. ISO 26262에 따른 규제 요건은 중복 계산 경로와 안전 진단의 채택을 강화하고 실리콘 지출을 더욱 증가시킵니다.

지속적인 공급망 제약 및 칩 부족

자동차용 리드 타임은 특히 성숙한 노드 마이크로컨트롤러, 센서, 아날로그 컴포넌트의 경우 가전 제품의 표준보다 깁니다. 차량 탑재 등급의 특수 패키징 능력은 동아시아에 집중되어 단일 장애 지점을 창출하고 있습니다. 지리적 위험에 대처하기 위해 GlobalFoundries와 NXP는 22FDX 생산을 드레스덴과 뉴욕으로 나누어 협력 관계를 확대하고 자동차 제조업체에게 1 등급 인증을 충족하는 듀얼 소스 공급 경로를 제공했습니다.

부문 분석

집적회로는 2024년 자동차용 반도체 시장 규모의 866억 달러를 차지하였고, 2030년까지 CAGR 8.5%로 성장이 예측되고 있습니다. 게이트웨이, 차체 및 파워트레인의 각 영역이 더 높은 클럭 속도와 메모리 풋 프린트의 확장으로 이동함에 따라 마이크로컨트롤러가 선두를 달리고 있습니다. Infineon은 AURIX 제품군을 RISC-V 아키텍처로 확장함으로써 마이크로 컴퓨터 시장의 자동차용 반도체 시장에서 28.5%의 점유율을 얻었으며 이 부문의 혁신이 가속화되었습니다. 아날로그 IC는 시스템 온 칩 통합으로 이전 노드 디바이스에 가격 압력이 가해지는 것, 전원 관리, 센서 인터페이스, 전압 레귤레이션에서 매우 중요한 역할을 유지하고 있습니다.

이산 소자, 광전자, 센서 및 MEMS 카테고리가 나머지를 차지합니다. 이산 IGBT와 MOSFET은 트랙션 인버터와 릴레이 대체 스위치를 지원하지만, 여러 다이를 단일 기판에 집적한 파워 모듈 설계가 점점 늘어나고 있습니다. 옵토일렉트로닉스는 적응형 LED 조명과 신흥 LiDAR 유닛으로 혜택을 누리며 MEMS 가속도계, 자이로스코프 및 압력 센서는 ADAS와 편안한 기능으로 널리 사용됩니다. Zonal 아키텍처는 이전의 독립형 컴포넌트를 더 가치있는 IC에 번들로 제공하여 집적 회로가 더 넓은 자동차용 반도체 시장을 계속 능가하는 이유를 설명합니다.

지역 분석

아시아태평양은 2024년 자동차용 반도체 출하량의 71.5%를 차지하였고, 2030년까지 연평균 복합 성장률(CAGR) 7.8%로 성장할 것으로 예측됩니다. 중국의 신에너지차 보급률은 2024년 39%를 넘어 베이징의 100% 조달 목표를 쫓기 위해 같은 해 300개 이상의 국내 칩 설계 회사가 설립되었습니다. 상하이에 본사를 둔 Horizon Robotics는 주요 설계 승리를 확보, 현지 ADAS 프로세서 수량의 33.97% 점유율을 주장했지만 주조 SMIC는 2026년 생산으로 10% 차재 매출 목표를 설정했습니다. 인도는 76,000 달러 crore의 India Semiconductor Mission 아래 반도체 에코시스템을 확대하고 있습니다. 승인된 제안은 총 210억 달러로 Tata Electronics, Himax, PSMC 간의 디스플레이 및 초저전력 AI 파트너십을 포함합니다.

북미는 390억 달러의 CHIPS 및 과학법 우대 조치와 TSMC의 66억 달러의 애리조나 확장과 같은 중요한 프로젝트에 밀려 2위를 차지했습니다. 테슬라는 삼성과 165억 달러, 8년간의 웨이퍼 공급 계약을 맺고 텍사스에서 제조되는 자율주행용 실리콘의 첨단 노드 능력을 확보했습니다. 캐나다 반도체 협의회(Semiconductor Council)는 전기 이동성의 밸류체인에 대한 정책 조정을 추진하기 위해 인피니언을 회원들에게 추가했습니다.

유럽은 430억 유로(486억 달러)의 EU 칩스법에 의해 전략적 자율성을 추구해 2030년까지 세계 생산의 20%를 획득하는 것을 목표로 하고 있습니다. ST 마이크로 일렉트로닉스는 이탈리아 카타니아에서 통합 SiC 공장에 착공했으며, 드레스덴 컨소시엄은 새로운 로직 시설을 위해 50억 유로(57억 달러)의 국가 보조를 확보했습니다. 스텔란티스와 같은 자동차 제조업체는 인피니언과 전력 변환 시스템을 공동 개발하여 SiC MOSFET 공급에 대한 우선 액세스를 보장합니다. 중동 및 아프리카, 남미는 아직 발전도상이지만, 2자리수의 EV 보급률을 나타내고 있어, 현지 공급망이 성숙하면, 장래의 성장 노드가 됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 신흥국의 자동차 생산 증가

- 고급 안전 및 쾌적 시스템에 대한 수요 증가

- 전동화에 의해 1대당의 반도체 탑재량 증가

- 존 E/E 아키텍처와 Software-Defined Vehicle이 하이엔드 프로세서 촉진

- 자동차 등급의 주조 능력에 대한 정부 보조금

- EV 파워트레인에서 SiC와 GaN 파워 디바이스의 채용

- 시장 성장 억제요인

- 고기능차의 고비용

- 공급망의 지속적인 제약 및 칩 부족

- 와이드 밴드갭 기판(SiC/GaN)의 희소성 및 비용

- 긴 자동차 품질 평가 사이클이 시장 투입까지의 시간 지연 초래

- 업계 밸류체인 분석

- 규제 상황

- 기술의 전망

- 자율주행차에서 RF 디바이스 수요

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 진입업자의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 투자 분석

- 거시 경제 동향의 영향

제5장 시장 규모 및 성장 예측

- 디바이스 유형별(디바이스 유형의 출하수는 보완적인 것)

- 이산 반도체

- 다이오드

- 트랜지스터

- 파워 트랜지스터

- 정류기 및 사이리스터

- 기타 이산 소자

- 옵토일렉트로닉스

- LED

- 레이저 다이오드

- 이미지 센서

- 옵토커플러

- 기타 디바이스 유형

- 센서 및 MEMS

- 압력

- 자기장

- 액추에이터

- 가속도 및 요율

- 온도 및 기타

- 집적회로

- 집적회로 유형별

- 아날로그

- 마이크로

- 마이크로프로세서(MPU)

- 마이크로컨트롤러(MCU)

- 디지털 신호 프로세서

- 로직

- 메모리

- 기술 노드별(출하수 해당 없음)

- 3nm 미만

- 3nm

- 5nm

- 7nm

- 16nm

- 28nm

- 28nm초

- 이산 반도체

- 비즈니스 모델별

- IDM

- 디자인 및 패브리스 벤더

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 한국

- 인도

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 이집트

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- NXP Semiconductors NV

- Infineon Technologies AG

- Renesas Electronics Corporation

- STMicroelectronics NV

- Texas Instruments Inc.

- Toshiba Electronic Devices & Storage Corp.

- Micron Technology Inc.

- onsemi

- Analog Devices Inc.

- Robert Bosch GmbH(Semiconductor Division)

- ROHM Co., Ltd.

- NVIDIA Corporation

- Qualcomm Technologies Inc.

- Intel Corporation(Mobileye)

- Samsung Electronics Co., Ltd.(System LSI)

- MediaTek Inc.

- BYD Semiconductor Co. Ltd.

- Semtech Corporation

- Diodes Incorporated

- Microchip Technology Inc.

- Melexis NV

- Elmos Semiconductor SE

- Allegro Microsystems, Inc.

- Skyworks Solutions, Inc.

- Ambarella Inc.

- Wolfspeed Inc.

제7장 시장 기회 및 향후 전망

AJY 25.11.26The automotive semiconductor market size reached USD 100.48 billion in 2025 and is forecast to expand at a 7.29% CAGR, lifting the market value to USD 142.87 billion in 2030.

Mounting electrification mandates, rapid adoption of advanced driver-assistance features, and the pivot toward software-defined vehicles are pushing silicon content higher across every vehicle class. Automakers are racing to secure long-term foundry capacity, and the spread of zonal architectures is concentrating spend on high-performance processors, memory, and power devices. Supply-chain resiliency programs combined with multi-sourcing strategies are reshaping procurement, while wide-bandgap devices and integrated power modules open fresh design-in opportunities that sustain pricing power even as mature-node components normalize.

Global Automotive Semiconductor Market Trends and Insights

Electrification Boosting Semiconductor Content Per Vehicle

Battery-electric platforms add power electronics, battery-management ICs, and thermal-management controllers absent in internal-combustion models. The transition from 400 V to 800 V electrical systems demands silicon-carbide (SiC) MOSFETs that sustain higher voltages with lower switching losses. Infineon's trench-based SiC super-junction devices deliver 40% lower resistance and 25% higher current capability, enabling smaller traction inverters and faster charging times. NXP's ultra-wideband wireless battery-management system removes heavy cabling, trims vehicle weight, and frees space for higher energy-density packs. Higher-voltage architectures also need reinforced isolation, gate drivers, and precision current sensors that command premium average selling prices. Collectively, these factors lift semiconductor dollar content per EV to multiples of conventional vehicles.

Rising Demand for Advanced Safety and Comfort Systems

Level 2+ driver-assistance packages integrate multi-modal sensor suites-radar, LiDAR, and high-resolution cameras-producing terabytes of data per hour. Real-time sensor-fusion workloads require application-specific processors and embedded neural-network accelerators. NXP's 28 nm RFCMOS radar one-chip family now offers 360-degree coverage and built-in AI object classification, cutting bill-of-materials and simplifying system architecture. Complementary optical innovations, such as ams OSRAM's eight-channel pulsed lasers, deliver 1,000 W peak optical power, extending LiDAR range for highway autopilot features. Regulatory demands under ISO 26262 reinforce the adoption of redundant compute paths and safety diagnostics, further elevating silicon spend.

Persistent Supply-Chain Constraints and Chip Shortages

Automotive lead times remain longer than consumer electronics norms, especially for mature-node microcontrollers, sensors, and analog components. Specialized automotive-grade packaging capacity is heavily concentrated in East Asia, creating single points of failure. To address geographic risk, GlobalFoundries and NXP broadened their collaboration on 22FDX production split between Dresden and New York, giving automakers a dual-sourced pathway that meets Grade 1 qualification.Automakers are now embedding foundry capacity clauses into long-term supply agreements to shield vehicle launches from component shortages.

Other drivers and restraints analyzed in the detailed report include:

- Zonal E/E Architectures and Software-Defined Vehicles Spur High-End Processors

- SiC and GaN Power Devices Adoption in EV Powertrains

- Scarcity and Cost of Wide-Bandgap Substrates (SiC/GaN)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Integrated circuits represented USD 86.6 billion of the automotive semiconductor market size in 2024 and are forecast to post an 8.5% CAGR through 2030. Microcontrollers lead the pack as gateway, body, and powertrain domains migrate to higher clock speeds and expanded memory footprints. Infineon captured 28.5% share of the automotive semiconductor market within microcontrollers by expanding its AURIX family to a RISC-V architecture, reinforcing the segment's technological churn. Analog ICs retain a pivotal role in power management, sensor interfacing, and voltage regulation, although system-on-chip consolidation exerts price pressure on older node devices.

Discrete devices, optoelectronics, and sensor/MEMS categories account for the balance. Discrete IGBTs and MOSFETs underpin traction inverters and relay-replacement switches, but design-ins increasingly favor integrated power modules that collapse multiple dies into a single substrate. Optoelectronics benefit from adaptive LED lighting and emerging LiDAR units, while MEMS accelerometers, gyros, and pressure sensors proliferate across ADAS and comfort features. Zonal architectures bundle former standalone components into higher-value ICs, explaining why integrated circuits continue to outpace the wider automotive semiconductor market.

Automotive Semiconductor Market Report is Segmented by Device Type (Discrete Semiconductors [Diodes, and More], Optoelectronics [Laser Diodes, and More], Sensors and MEMS [Pressure, Actuators, and More], and Integrated Circuits), Business Model (IDM, and Design/ Fabless Vendor), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific commanded 71.5% of automotive semiconductor shipments in 2024 and is expected to grow at a 7.8% CAGR to 2030. China's new-energy vehicle penetration surpassed 39% in 2024, and more than 300 domestic chip design firms were established that year to chase Beijing's 100% sourcing target. Shanghai-based Horizon Robotics secured major design wins, claiming 33.97% share of local ADAS processor volume, while foundry SMIC set a 10% automotive revenue goal for 2026 production. India is scaling its semiconductor ecosystem under the USD 76,000 crore India Semiconductor Mission; approved proposals total USD 21 billion, including display and ultralow-power AI partnerships between Tata Electronics, Himax, and PSMC.

North America ranks second, buoyed by the USD 39 billion CHIPS and Science Act incentives and marquee projects such as TSMC's USD 6.6 billion Arizona expansion. Tesla inked a USD 16.5 billion, eight-year wafer-supply pact with Samsung, locking in advanced-node capacity for autonomous-driving silicon manufactured in Texas. Canada's Semiconductor Council added Infineon as a member to drive policy alignment on electric-mobility value chains.

Europe pursues strategic autonomy via the EUR 43 billion (USD 48.6 billion) EU Chips Act, aiming to capture 20% global output by 2030. STMicroelectronics broke ground on an integrated SiC fab in Catania, Italy, while a Dresden consortium secured EUR 5 billion (USD 5.7 billion) in state aid for a new logic facility. Automakers such as Stellantis co-develop power-conversion systems with Infineon, ensuring preferential access to SiC MOSFET supply. The Middle East, Africa, and South America remain nascent but exhibit double-digit EV adoption trajectories, positioning them as future growth nodes once local supply chains mature.

- NXP Semiconductors N.V.

- Infineon Technologies AG

- Renesas Electronics Corporation

- STMicroelectronics N.V.

- Texas Instruments Inc.

- Toshiba Electronic Devices & Storage Corp.

- Micron Technology Inc.

- onsemi

- Analog Devices Inc.

- Robert Bosch GmbH (Semiconductor Division)

- ROHM Co., Ltd.

- NVIDIA Corporation

- Qualcomm Technologies Inc.

- Intel Corporation (Mobileye)

- Samsung Electronics Co., Ltd. (System LSI)

- MediaTek Inc.

- BYD Semiconductor Co. Ltd.

- Semtech Corporation

- Diodes Incorporated

- Microchip Technology Inc.

- Melexis NV

- Elmos Semiconductor SE

- Allegro Microsystems, Inc.

- Skyworks Solutions, Inc.

- Ambarella Inc.

- Wolfspeed Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing vehicle production in emerging economies

- 4.2.2 Rising demand for advanced safety and comfort systems

- 4.2.3 Electrification boosting semiconductor content per vehicle

- 4.2.4 Zonal E/E architectures and software-defined vehicles spur high-end processors

- 4.2.5 Government subsidies for auto-grade foundry capacity

- 4.2.6 SiC and GaN power devices adoption in EV powertrains

- 4.3 Market Restraints

- 4.3.1 High cost of advanced-feature vehicles

- 4.3.2 Persistent supply-chain constraints and chip shortages

- 4.3.3 Scarcity and cost of wide-bandgap substrates (SiC/GaN)

- 4.3.4 Lengthy automotive qualification cycles slow time-to-market

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 RF Device Demand in Autonomous Vehicles

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Investment Analysis

- 4.10 Impact of Macroeconomic Trends

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Device Type (Shipment Volume for Device Type is Complementary)

- 5.1.1 Discrete Semiconductors

- 5.1.1.1 Diodes

- 5.1.1.2 Transistors

- 5.1.1.3 Power Transistors

- 5.1.1.4 Rectifier and Thyristor

- 5.1.1.5 Other Discrete Devices

- 5.1.2 Optoelectronics

- 5.1.2.1 Light-Emitting Diodes (LEDs)

- 5.1.2.2 Laser Diodes

- 5.1.2.3 Image Sensors

- 5.1.2.4 Optocouplers

- 5.1.2.5 Other Device Types

- 5.1.3 Sensors and MEMS

- 5.1.3.1 Pressure

- 5.1.3.2 Magnetic Field

- 5.1.3.3 Actuators

- 5.1.3.4 Acceleration and Yaw Rate

- 5.1.3.5 Temperature and Others

- 5.1.4 Integrated Circuits

- 5.1.4.1 By Integrated Circuit Type

- 5.1.4.1.1 Analog

- 5.1.4.1.2 Micro

- 5.1.4.1.2.1 Microprocessors (MPU)

- 5.1.4.1.2.2 Microcontrollers (MCU)

- 5.1.4.1.2.3 Digital Signal Processors

- 5.1.4.1.3 Logic

- 5.1.4.1.4 Memory

- 5.1.4.2 By Technology Node (Shipment Volume Not Applicable)

- 5.1.4.2.1 < 3nm

- 5.1.4.2.2 3nm

- 5.1.4.2.3 5nm

- 5.1.4.2.4 7nm

- 5.1.4.2.5 16nm

- 5.1.4.2.6 28nm

- 5.1.4.2.7 > 28nm

- 5.1.1 Discrete Semiconductors

- 5.2 By Business Model

- 5.2.1 IDM

- 5.2.2 Design/ Fabless Vendor

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 South America

- 5.3.2.1 Brazil

- 5.3.2.2 Argentina

- 5.3.2.3 Rest of South America

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Rest of Europe

- 5.3.4 Asia-Pacific

- 5.3.4.1 China

- 5.3.4.2 Japan

- 5.3.4.3 South Korea

- 5.3.4.4 India

- 5.3.4.5 Rest of Asia-Pacific

- 5.3.5 Middle East and Africa

- 5.3.5.1 Middle East

- 5.3.5.1.1 Saudi Arabia

- 5.3.5.1.2 United Arab Emirates

- 5.3.5.1.3 Turkey

- 5.3.5.1.4 Rest of Middle East

- 5.3.5.2 Africa

- 5.3.5.2.1 South Africa

- 5.3.5.2.2 Nigeria

- 5.3.5.2.3 Egypt

- 5.3.5.2.4 Rest of Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 NXP Semiconductors N.V.

- 6.4.2 Infineon Technologies AG

- 6.4.3 Renesas Electronics Corporation

- 6.4.4 STMicroelectronics N.V.

- 6.4.5 Texas Instruments Inc.

- 6.4.6 Toshiba Electronic Devices & Storage Corp.

- 6.4.7 Micron Technology Inc.

- 6.4.8 onsemi

- 6.4.9 Analog Devices Inc.

- 6.4.10 Robert Bosch GmbH (Semiconductor Division)

- 6.4.11 ROHM Co., Ltd.

- 6.4.12 NVIDIA Corporation

- 6.4.13 Qualcomm Technologies Inc.

- 6.4.14 Intel Corporation (Mobileye)

- 6.4.15 Samsung Electronics Co., Ltd. (System LSI)

- 6.4.16 MediaTek Inc.

- 6.4.17 BYD Semiconductor Co. Ltd.

- 6.4.18 Semtech Corporation

- 6.4.19 Diodes Incorporated

- 6.4.20 Microchip Technology Inc.

- 6.4.21 Melexis NV

- 6.4.22 Elmos Semiconductor SE

- 6.4.23 Allegro Microsystems, Inc.

- 6.4.24 Skyworks Solutions, Inc.

- 6.4.25 Ambarella Inc.

- 6.4.26 Wolfspeed Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment