|

시장보고서

상품코드

1852177

복합재료 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Composite Material - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

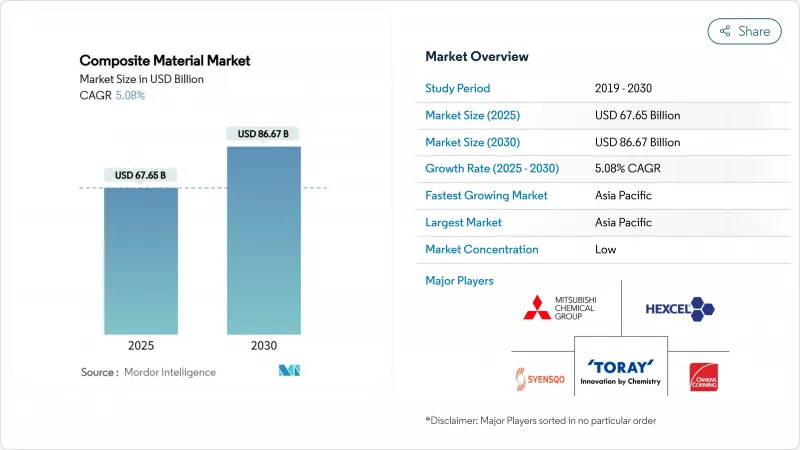

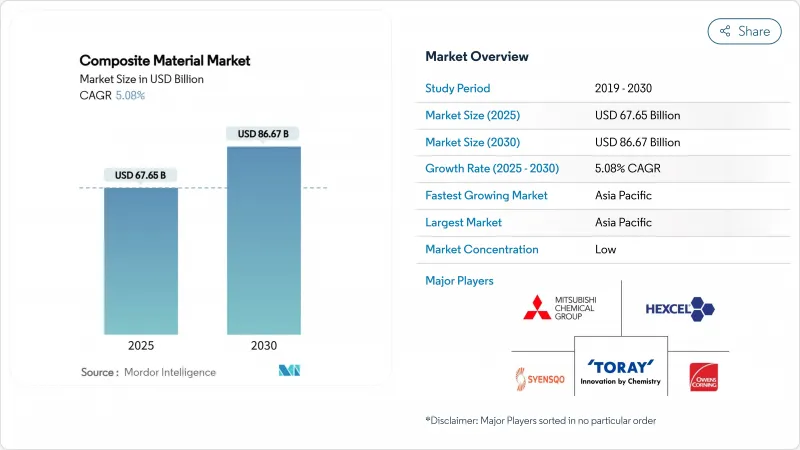

복합재료 시장 규모는 2025년에 676억 5,000만 달러로 평가되었고, 예측기간(2025-2030년)의 CAGR은 5.08%를 나타낼 것으로 예측되며, 2030년에 866억 7,000만 달러에 달할 전망입니다.

운송, 에너지, 인프라 및 전자 분야에서 경량 고성능 소재에 대한 강력한 수요가 적용 분야를 확대하고 있는 반면, 지속적인 공정 자동화는 사이클 시간과 결함을 줄이고 있습니다. 2024년 글로벌 매출의 45.12%를 차지한 아시아태평양 지역은 풍력 터빈 확장, 전기화 프로그램 및 대규모 인프라 프로젝트가 지역 소비를 가속화함에 따라 여전히 물량 성장의 중심지입니다. 세라믹 매트릭스 기술의 급속한 발전, 금속을 폴리머 매트릭스 등급으로 꾸준히 대체하는 추세, 특수 보강재 공급 기반 개선은 신규 진입자의 진입 장벽을 강화하고 있습니다. 그러나 재활용 한계는 장기적인 순환성 목표를 계속해서 흐리게 하며, 수명 종료 솔루션이 설치 속도를 따라가지 못할 경우 채택을 저해할 수 있습니다.

세계의 복합재료 시장 동향 및 인사이트

전동화가 주도하는 E-모빌리티의 탄소섬유 수요

전기자동차는 약 450파운드의 플라스틱 및 폴리머 복합재료를 통합합니다. 이는 내연 기관 플랫폼에 비해 18% 증가한 수치로, 공차 중량이 10% 감소할 때마다 일반적으로 주행 거리가 6-8% 늘어나는 특성이 있기 때문입니다. 배터리 케이스는 대표적 적용 분야로 부상했으며, 탄소섬유 강화 폴리머는 열적 안정성을 유지한 채 알루미늄 대비 30%의 무게 절감 효과를 제공합니다. 유리섬유 강화 열가소성 플라스틱으로 성형된 차체 패널은 비용 경쟁력 있는 경량화를 가능케 하며, 내장재에 적용된 천연섬유 적층재는 지속가능성 인증을 확대합니다. 자동차 제조사들은 강성, 충돌 안전성 및 수명 주기 배출량을 최적화하기 위해 탄소, 유리 및 바이오 보강재를 혼합한 다중 소재 구조로 수렴하고 있습니다. 공급망은 2026-2028년 모델 출시 기간 동안 병목 현상을 방지하기 위해 북미, 유럽 및 동아시아 전역에서 토우 용량과 인증 프리프레그 라인을 확장하며 대응 중입니다.

풍력 터빈 블레이드 제조의 용도 확대

2024년 글로벌 풍력 설비 설치량은 17%, 2025년에는 35% 증가하며 2035년 예상 목표인 누적 용량 450GW에 접근하고 있습니다. 차세대 해상 풍력 터빈은 이제 15MW를 초과하며, 맞춤형 복합재료 레이업으로만 구현 가능한 110m 이상의 긴 블레이드가 필요합니다. 10년 말까지 블레이드 제조에 연간 100만 톤 이상의 유리 및 탄소 보강재가 소비될 전망으로, 유리섬유 용융 용량과 고탄성 탄소 공급에 대한 압박이 가중될 것입니다. 유리섬유 강화 플라스틱이 미터당 비용 기준으로는 여전히 우세하지만, 블레이드 끝단 변형과 블레이드 루트 질량을 억제하기 위한 선택적 탄소 스파 캡이 확산 중입니다. 유럽에서는 용접 가능한 블레이드 뿌리 접합부를 위한 열가소성 블레이드를 시범 운영 중이며, 이는 시멘트 가마 공동 처리 없이 재활용 경로를 가능하게 할 잠재력을 지닙니다. 해당 분야의 신흥 블레이드 순환성 규정은 OEM 및 제조업체에게 재료 추적성과 수지 재조성을 시급한 우선 과제로 만들고 있습니다.

복합재료의 높은 비용

탄소섬유 복합재료는 일반적으로 납품 기준 강철 대비 5-10배의 가격으로, 비용 민감 부문에의 진입을 저해합니다. 항공우주 등급 프리프레그는 오토클레이브 경화, 엄격한 환경 제어, 광범위한 비파괴 검사를 필요로 하며, 각각 단위 비용을 상승시킵니다. 자동차 프로그램도 유사한 장벽에 직면하여, 유리한 중량 대비 이점에도 불구하고 탄소섬유 사용이 대부분 프리미엄 브랜드로 제한됩니다. 생산 규모는 여전히 핵심 장벽으로 남아 있습니다. 섬유 방사 라인과 전구체 공장이 자본 집약적이기 때문입니다. 국립 재생에너지 연구소(NREL)의 열성형 공정과 같은 혁신은 재활용 가능한 탄소 시트의 비용을 90-95% 절감할 수 있지만, 상용화에는 수년에 걸친 인증 캠페인이 필요합니다. 원자재 가격이 하락하거나 설계 엔지니어가 우수한 시스템 수준 절감 효과를 확보하기 전까지는 많은 잠재적 도입업체들이 대량 대체를 미룰 수 있습니다.

부문 분석

폴리머 매트릭스 복합재료(PMC)는 2024년 매출의 56.21%를 차지하며, 균형 잡힌 성능과 제조 용이성을 위한 선호 옵션으로서 복합재료 시장의 입지를 공고히 했습니다. 열경화성 에폭시는 항공우주, 해양 및 풍력 블레이드 분야에서 여전히 주류를 이루고 있으나, 재활용 가능한 열가소성 플라스틱이 자동차 및 소비재 시장에서 점유율을 꾸준히 잠식하고 있습니다. 상용 열가소성 UD 테이프 라인은 이제 폭이 1m를 초과하여 배터리 트레이 및 시트 구조물에 대한 고속 프레스 성형에 유리합니다. 동시에 세라믹 매트릭스 복합재료(CMC)에 기인한 복합재료 시장 규모는 2025년부터 2030년까지 연평균 8.57% 성장률을 기록할 것으로 전망되며, 이는 항공우주 추진 시스템과 집중형 태양열 발전 수신기의 수요 증가에 힘입은 것입니다. CMC는 1,600°C 이상의 고온을 견디며 니켈 초합금을 대체하고 냉각 수요를 대폭 줄여 타의 추종을 불허하는 열효율을 실현합니다. 초기 투자 비용은 상당하지만, 양산이 안정화되면 경량화, 연료 소모 감소, 유지보수 비용 절감을 통해 초기 프리미엄을 상쇄하는 수명 주기 가치 제안을 제공합니다. 금속 매트릭스 복합재료는 전자 기판 캐리어 및 브레이크 로터용으로 탁월한 열전도성과 내마모성을 바탕으로 소규모 틈새 시장을 차지하고 있습니다. 적층 제조 공정과 5축 CNC 마무리 가공 기술이 설계 가능 영역을 확장하며, 향후 5년간 점진적인 시장 침투가 예상됩니다.

지역 분석

아시아태평양 지역은 2024년 매출의 45.12%를 차지하며 복합재료 시장을 주도하고 있으며, 중국의 해상 풍력 설비 확대, 인도의 지하철 네트워크 확장, 동남아시아의 전력망 인프라 업그레이드에 힘입어 2030년까지 7.91% 성장할 것으로 전망됩니다. 지역별 복합재료 시장 규모는 탄소섬유 생산 능력 확대의 혜택도 받습니다. 한국의 효성은 항공우주 및 수소 탱크 수요를 충족하기 위해 연간 생산량을 9,000톤으로 증대 중입니다. 일본의 가치 사슬은 고정밀 토우 스프레딩 및 프리프레그 기술에 집중되어 국내 항공기 프로그램과 수출 고객 모두를 지원합니다.

북미는 지속적인 항공우주 납품, 재생에너지에 대한 연방 투자, 부활하는 레저용 해양 부문으로 인해 근소한 차이로 뒤를 잇고 있습니다. 미국 에너지부는 풍력 터빈 복합재료 재활용을 촉진하기 위해 2천만 달러를 배정하며 순환경제를 향한 정책 추진력을 시사했습니다. 캐나다 주정부들은 바이오 기반 열가소성 플라스틱 분야의 국내 지적재산권 유지를 목표로, 학술 연구개발과 사출 오버몰딩 파일럿 라인을 결합한 첨단 소재 클러스터를 후원하고 있습니다.

유럽은 정교한 설계 역량과 엄격한 환경 규제로 바이오 수지 및 폐쇄형 공정 채택을 촉진합니다. 2024년 말 공급망 차질과 에너지 비용 급등으로 생산량이 감소했음에도 유럽은 전 세계 생산량의 22% 점유율을 유지합니다. 베스타스의 순환형 블레이드 및 저배출 타워와 같은 이니셔티브는 EU 기후 정책이 OEM의 우선순위를 종합적 지속가능성으로 전환시키고 있음을 보여줍니다. 동유럽 국가들은 숙련된 노동력과 서부 시장과의 근접성을 활용하여 풀트루전 및 필라멘트 와인딩 공장 투자 유치를 추진 중입니다.

남미와 중동, 아프리카는 규모는 작지만, 인프라 현대화 및 담수화 프로젝트에서 복합재료 솔루션을 요구함에 따라 비례 이상의 성장률을 기록하고 있습니다. 브라질 풍력 회랑, 사우디 담수화 염수 라인, 남아프리카 전기 버스 차체가 주목할 만한 수요 지역입니다. 다국적 기업들의 기술 이전과 현지 보강재 공급(사이살, 황마)이 결합되어 현지 혁신을 촉진하고 수입 부품과의 비용 격차를 점차 좁혀가고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- E-모빌리티에 있어서의 전기 주도형 탄소섬유 수요

- 풍력 터빈 제조에 있어서의 용도의 확대

- 대량 생산 자동차 산업에서의 열가소성 복합재료 채택 확대

- 재료 과학 분야의 기술 발전

- 항공우주 및 방위산업에서 복합재료의 사용 증가

- 시장 성장 억제요인

- 복합재료의 높은 비용

- 재활용의 과제

- 자동 레이업 공정에서의 숙련된 노동력 부족

- 밸류체인 분석

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모와 성장 예측

- 매트릭스 재료별

- 폴리머 매트릭스 복합재료(PMC)

- 열경화성 수지

- 열가소성 수지

- 세라믹/탄소 매트릭스 복합재료(CMC)

- 기타 매트릭스(금속 매트릭스 복합재료)

- 폴리머 매트릭스 복합재료(PMC)

- 보강 섬유별

- 유리섬유

- 탄소섬유

- 아라미드섬유

- 기타 섬유(천연섬유/바이오섬유)

- 최종 이용 산업별

- 자동차 및 운수

- 풍력에너지

- 항공우주 및 방위

- 파이프 및 탱크

- 건설

- 전기 및 전자

- 스포츠 및 레크리에이션

- 기타 최종 사용자 산업(헬스케어, 해양 등)

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 태국

- 말레이시아

- 인도네시아

- 베트남

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 튀르키예

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 콜롬비아

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 나이지리아

- 카타르

- 이집트

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 전략적 동향

- 시장 점유율(%)/랭킹 분석

- 기업 프로파일

- 3M

- Arkema

- BASF

- CPIC BRASIL Fibras de Vidro Ltda

- DuPont

- Exel Composites

- Gurit Services AG

- Hexcel Corporation

- HS HYOSUNG ADVANCED MATERIALS

- Lanxess

- Mitsubishi Chemical Group Corporation.

- Nippon Graphite Fiber Co., Ltd.

- Owens Corning

- SGL Carbon

- Syensqo

- Teijin Limited

- Toray Industries Inc.

제7장 시장 기회와 장래의 전망

HBR 25.11.27The Composite Material Market size is estimated at USD 67.65 billion in 2025, and is expected to reach USD 86.67 billion by 2030, at a CAGR of 5.08% during the forecast period (2025-2030).

Robust demand for lightweight, high-performance materials in transportation, energy, infrastructure and electronics is widening the application portfolio, while continuous process automation is lowering cycle times and defects. Asia-Pacific, holding 45.12% of global revenue in 2024, remains the epicenter of volume growth as wind-turbine expansion, electrification programs and large-scale infrastructure projects accelerate regional consumption. Rapid progress in ceramic matrix technologies, steady substitution of metals by polymer matrix grades and an improving supply base for specialty reinforcements are strengthening competitive barriers for late entrants. Recycling limitations, however, continue to cloud long-term circularity targets and could restrain adoption if end-of-life solutions do not keep pace with installation rates.

Global Composite Material Market Trends and Insights

Electrification-Driven Carbon-Fiber Demand in E-Mobility

Electric vehicles integrate roughly 450 lb of plastics and polymer composites-an 18% rise compared with internal-combustion platforms-because every 10% curb in curb weight typically stretches driving range by 6-8%. Battery enclosures have become a flagship application, where carbon-fiber reinforced polymers deliver a 30% mass cut versus aluminum without sacrificing thermal stability. Body panels molded from glass-fiber reinforced thermoplastics enable cost-competitive lightweighting, while natural-fiber laminates in interior trim broaden sustainability credentials. Automakers are converging on multi-material architectures that blend carbon, glass and bio reinforcements to optimise stiffness, crashworthiness and lifecycle emissions. Supply chains are responding by expanding tow capacity and qualified prepreg lines across North America, Europe and East Asia to avert bottlenecks during the 2026-2028 model-launch window.

Increasing Usage in the Manufacturing of Wind Turbine Blades

Global wind installations climbed 17% in 2024 and 35% in 2025, pushing cumulative capacity toward the 450 GW mark envisaged for 2035. Next-generation offshore machines now exceed 15 MW, requiring blades longer than 110 m that can only be realised with tailored composite lay-ups. More than 1 million t of glass and carbon reinforcements will be consumed annually for blade manufacture by the end of the decade, intensifying pressure on glass-fiber melt capacity and high-modulus carbon supply. While glass-fiber reinforced plastics continue to dominate on a cost-per-meter basis, selective carbon spar caps are proliferating to curb tip deflection and blade-root mass. Europe is piloting thermoplastic blades for weldable root joints, potentially enabling recycling routes that avoid co-processing in cement kilns. The sector's emerging blade-circularity regulations make material traceability and resin reformulation urgent priorities for OEMs and fabricators.

High Cost of Composite Materials

Carbon-fiber composites typically price at five-to-ten times steel on a delivered-part basis, deterring penetration into cost-sensitive segments. Aerospace-grade prepregs entail autoclave curing, tight environmental controls and extensive non-destructive testing, each inflating unit expense. Automotive programs confront similar hurdles, confining carbon-fiber usage largely to premium marques despite favorable weight-benefit ratios. Production scale remains a pivotal barrier, since fiber-spinning lines and precursor plants run capital-intensive. Breakthroughs such as National Renewable Energy Laboratory's thermoforming route promise 90-95% cost savings for recyclable carbon sheets, yet commercial deployment will require multi-year qualification campaigns. Until raw-material prices drop or design engineers capture superior system-level savings, many potential adopters may defer high-volume substitution.

Other drivers and restraints analyzed in the detailed report include:

- Growing Adoption of Thermoplastic Composites in Mass-Production Automotive

- Increasing Use of Composites in the Aerospace and Defense Industry

- Challenges in Recycling Composite Materials

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polymer matrix composites (PMCs) delivered 56.21% of 2024 revenue, reinforcing the composites market as the preferred option for balanced performance and manufacturability. Thermoset epoxies remain mainstream in aerospace, marine and wind blades, yet recyclable thermoplastics are steadily eroding share in automotive and consumer goods. Commercial thermoplastic UD-tape lines now exceed 1 m wide, favouring high-throughput press forming for battery trays and seat structures. In parallel, the composites market size attributable to ceramic matrix composites is projected to post an 8.57% CAGR between 2025 and 2030, propelled by aerospace propulsion and concentrated solar-power receivers. CMCs withstand more than 1 600 °C, replacing nickel super-alloys and slashing cooling demands, thereby unlocking unrivalled thermal efficiencies. Investment outlays are significant, but once quiver production stabilises, their life-cycle value proposition offsets initial premiums through weight savings, fuel burn reductions and lower maintenance. Metal matrix composites occupy a smaller niche that thrives on extraordinary thermal conductivity and wear resistance for electronic substrate carriers and brake rotors. Additive-manufacturing pathways and five-axis CNC finishing are broadening design envelopes, hinting at incremental penetration in the latter half of the decade.

The Composites Market Report Segments the Industry by Matrix Material (Polymer Matrix Composites (PMC), Ceramic/Carbon Matrix Composites (CMCs), Other Matrices), Reinforcement Fiber (Glass Fiber, Carbon Fiber, and More), End-Use Industry (Automotive and Transportation, Wind Energy, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific anchors the composites market with 45.12% revenue in 2024 and is projected to grow at 7.91% through 2030 as China escalates offshore wind installations, India expands metro rail networks and Southeast Asia upgrades grid infrastructure. The regional composites market size also benefits from escalating carbon-fiber capacity; South Korea's Hyosung is lifting annual output to 9 000 t to meet aerospace and hydrogen-tank demand. Japan's value chain focuses on high-precision tow spreading and prepreg technologies, serving both domestic air-frame programs and export customers.

North America trails closely, propelled by sustained aerospace deliveries, federal investments in renewable energy and a resurgent recreational-marine segment. The United States Department of Energy earmarked USD 20 million to advance wind-turbine composite recycling, signalling policy momentum toward circularity. Canadian provinces sponsor advanced-materials clusters that couple academic R&D with injection over-molding pilot lines, aiming to retain domestic IP around bio-based thermoplastics.

Europe commands sophisticated design capabilities and stringent environmental regulations that foster rapid adoption of bio-resins and closed-loop processes. Although supply-chain disruptions and energy-cost spikes trimmed production in late-2024, the bloc maintains a 22% share of global volumes. Initiatives such as Vestas's circular blades and low-emission towers illustrate how EU climate policy is steering OEM priorities toward holistic sustainability. Eastern European nations, leveraging skilled labor and proximity to Western markets, are courting investment in pultrusion and filament-winding plants.

South America and the Middle East & Africa, while collectively smaller, are registering outsized percentage gains as infrastructure modernization and desalination projects specify composite solutions. Brazilian wind corridors, Saudi desalination brine lines and South African electric-bus bodies are notable demand pockets. Technology transfer from multinational players, combined with local reinforcement supply (sisal, jute), is catalysing indigenous innovation and gradually narrowing cost gaps with imported parts.

- 3M

- Arkema

- BASF

- CPIC BRASIL Fibras de Vidro Ltda

- DuPont

- Exel Composites

- Gurit Services AG

- Hexcel Corporation

- HS HYOSUNG ADVANCED MATERIALS

- Lanxess

- Mitsubishi Chemical Group Corporation.

- Nippon Graphite Fiber Co., Ltd.

- Owens Corning

- SGL Carbon

- Syensqo

- Teijin Limited

- Toray Industries Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Electrification-Driven Carbon-Fiber Demand in E-Mobility

- 4.2.2 Increasing Usage in the Manufacturing of Wind Turbine

- 4.2.3 Growing Adoption of Thermoplastic Composites in Mass-Production Automotive

- 4.2.4 Technological Advancement in the Field of Material Science

- 4.2.5 Increasing Use of Composites in the Aerospace and Defense Industry

- 4.3 Market Restraints

- 4.3.1 High Cost of Composite Material

- 4.3.2 Challenges in Recycling of these Materials

- 4.3.3 Skilled-Labour Gap in Automated Lay-up Processes

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Matrix Material

- 5.1.1 Polymer Matrix Composites (PMC)

- 5.1.1.1 Thermoset Resins

- 5.1.1.2 Thermoplastic Resins

- 5.1.2 Ceramic/Carbon Matrix Composites (CMCs)

- 5.1.3 Other Matrices (Metal Matrix Composites)

- 5.1.1 Polymer Matrix Composites (PMC)

- 5.2 By Reinforcement Fiber

- 5.2.1 Glass Fiber

- 5.2.2 Carbon Fiber

- 5.2.3 Aramid Fiber

- 5.2.4 Other Fibers (Natural/Bio Fiber)

- 5.3 By End-use Industry

- 5.3.1 Automotive and Transportation

- 5.3.2 Wind Energy

- 5.3.3 Aerospace and Defense

- 5.3.4 Pipes and Tanks

- 5.3.5 Construction

- 5.3.6 Electrical and Electronics

- 5.3.7 Sports and Recreation

- 5.3.8 Other End user Industries (Healthcare, Marine, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Thailand

- 5.4.1.6 Malaysia

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Turkey

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Nigeria

- 5.4.5.4 Qatar

- 5.4.5.5 Egypt

- 5.4.5.6 United Arab Emirates

- 5.4.5.7 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Strategic Moves

- 6.2 Market Share (%)/Ranking Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, Recent Developments)}

- 6.3.1 3M

- 6.3.2 Arkema

- 6.3.3 BASF

- 6.3.4 CPIC BRASIL Fibras de Vidro Ltda

- 6.3.5 DuPont

- 6.3.6 Exel Composites

- 6.3.7 Gurit Services AG

- 6.3.8 Hexcel Corporation

- 6.3.9 HS HYOSUNG ADVANCED MATERIALS

- 6.3.10 Lanxess

- 6.3.11 Mitsubishi Chemical Group Corporation.

- 6.3.12 Nippon Graphite Fiber Co., Ltd.

- 6.3.13 Owens Corning

- 6.3.14 SGL Carbon

- 6.3.15 Syensqo

- 6.3.16 Teijin Limited

- 6.3.17 Toray Industries Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment