|

시장보고서

상품코드

1906035

중동 및 아프리카의 화물 및 물류 시장 : 점유율 분석, 업계 동향, 통계, 성장 예측(2026-2031년)Middle East And Africa Freight And Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

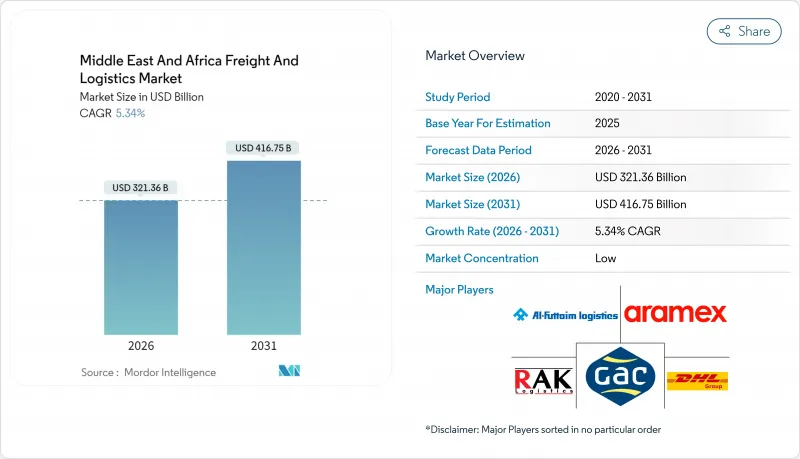

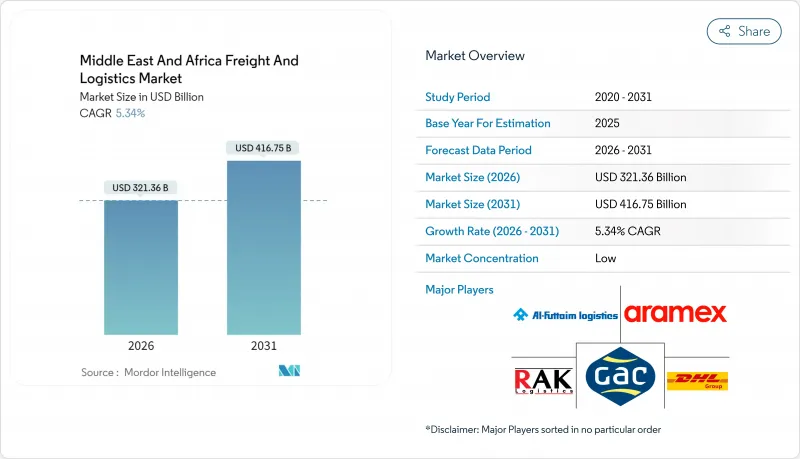

중동 및 아프리카의 화물 및 물류 시장의 규모는 2026년 3,213억 6,000만 달러에 달할 것으로 예측됩니다.

이는 2025년 3,050억 7,000만 달러에서 성장한 수치이며, 2031년에는 4,167억 5,000만 달러에 달할 것으로 전망되고 있습니다. 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 5.34%로 예측되고 있습니다.

이러한 성장 전망은 아시아, 유럽, 아프리카를 연결하는 지역의 요충지로 자리매김하는 것 외에도 홍해 항로의 혼란을 계기로 한 대규모 인프라 투자와 영구적인 수송 능력의 확충에 기반하고 있습니다. 전자상거래의 확대, 신규 멀티모달 회랑의 전개, 콜드체인 수요의 급증이 기준 화물량과 운송당 수익을 강화하고 있습니다. 국부펀드, 자유 무역 협정, 디지털 화물 플랫폼은 지정학적 변화를 완화하면서 경쟁의 치열성을 증폭시키고 있습니다. 네트워크 밀도, 기술 도입, 지속 가능한 실천을 극대화하는 사업자는 큰 수익을 얻을 전망입니다.

중동 및 아프리카의 화물 및 물류 시장의 동향 및 인사이트

전자상거래의 급성장과 크로스보더 소매

크로스보더 EC는 라스트마일 배송 빈도를 증가시키고 있으며 국내 CEP(택배)가 화물의 67.88%를 차지하는 반면 국제 CEP는 2030년까지 연평균 복합 성장률(CAGR) 5.77%로 확대될 전망입니다. 물류 사업자는 자동 분류 허브와 여러 운송 회사 API의 규모 확대를 진행하고 있으며, 이들은 제벨 알리 항구와 알 막툼 국제 공항을 연결합니다. 걸프 지역의 사업자는 AI 라우팅을 도입하고 현지 대학과 협력하여 디지털 인력 부족을 해소하기 위해 노력하고 있습니다. 옴니채널 소매업체는 창고관리, 클릭&컬렉트, 문앞 배송을 통합한 풀필먼트를 요구해 물류량을 특송 네트워크로 이동시키고 있습니다.

멀티모달 물류 인프라에 대한 대규모 투자

사우디아라비아는 2030년까지 항만, 공항, 철도에 1,333억 달러를 투입해 2026년 가동 예정인 NEOM항 최초의 완전 자동화 크레인을 실현하는 계획을 진행하고 있습니다. DP 월드의 25억 달러 사업과 2024년 과거 최고 규모인 200억 달러의 수익은 민간 자본의 높은 참여도를 보여줍니다. 자동화 및 재생에너지 통합은 체류 시간을 단축하고 비용 곡선을 개선하며 재적하 경쟁력을 재구성합니다.

도로, 철도, 항만 인프라의 불균형

내륙 아프리카 국가는 해안 게이트웨이에 의존하기 때문에 인프라 격차가 물류 비용을 밀어 올리고 있습니다. 아프리카 개발 은행은 도로 밀도 불균형과 자금 공급이 부족한 일반 해양 자산이 지속적인 병목 현상의 원인이라고 지적합니다. PPP 회랑과 유료 도로 금융 프레임워크는 광업 루트 이외에는 제한된 민간 자본만 유치합니다. 소수의 허브에 집중된 운송 능력은 기후와 노동 쟁의에 대한 취약성을 높이고 내륙 시장 침투를 저해합니다.

부문 분석

도매 및 소매업은 2025년 수익의 33.92%를 차지했지만, 제조 부문은 현지화와 공업단지의 확대에 따라 2031년까지 5.58%라는 가장 높은 CAGR을 기록할 전망입니다. 석유 및 가스, 광업 물류는 상품 유통과 에너지 안보 지출에 의해 여전히 큰 규모를 유지하고 있습니다. 건설 물류는 대형 인프라 프로젝트에 뒷받침되며 식량 안보 전략 하에서 농산물 및 식품 수송이 확대되고 있습니다.

나이지리아의 200억 달러 규모의 오기디그벤 공업단지는 특수 중량물 및 프로젝트형 카고 서비스 수요를 강화하고 있습니다. 저스트 인 타임 생산에는 자재 유입의 동기화가 필수적이며 이는 실시간 추적 및 예측 재고 분석에 대한 수요를 높이고 있습니다.

2025년 시점에서 화물 운송은 중동 및 아프리카의 화물 및 물류 시장의 59.21%를 차지하였습니다. 한편, 택배, 특송, 소포는 2031년까지 연평균 복합 성장률(CAGR) 5.57%로 성장을 견인할 전망입니다. 육로 벌크 수송은 기반을 유지하고 있으나 시간 지정 소포는 전자상거래의 영향을 받아 확대하고 있습니다. 화물 포워딩과 창고업은 꾸준한 성장을 지속하고, 온도 관리 창고는 높은 수익률을 실현하고 있습니다. '기타 활동'으로 분류되는 기술 중심의 부가가치 서비스는 급속히 확대되어 엔드 투 엔드 디지털 통합에 대한 수요를 창출하고 있습니다.

국제통합사업자는 허브 거점에 10억 단위의 설비 투자를 약속하는 반면, 알라멕스는 ADQ의 지원을 활용하여 지역 점유율 통합을 진행합니다. 로봇 기술과 AI 재고 관리 툴은 걸프 지역의 창고에서 생산성 격차를 확대하여 소형 배송, 크로스독 포워딩을 단일 인터페이스로 통합하는 플랫폼을 형성합니다.

기타 혜택

- 시장 예측(ME) 엑셀 시트

- 3개월 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 촉진요인

- 전자상거래의 급성장과 크로스보더 소매

- 멀티모달 물류 인프라에 대한 대규모 투자

- 자유무역협정(FTA) 확대와 신흥 무역회랑의 성장

- 의약품 및 신선식품용 콜드체인 수요

- 노동력 부족을 보완하는 창고 자동화

- 디지털 화물 플랫폼과 실시간 시각화 툴의 급속한 보급

- 억제요인

- 도로, 철도, 항만 인프라의 불균일성

- 복잡한 통관 규정과 국경에서의 지연

- 홍해 및 수에즈 운하의 병목 현상에 의한 혼란

- 운전기사 부족과 현지화 정책

- 가치 및 공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급자의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 지정학과 유행의 영향

제5장 시장 규모 및 성장 예측

- 물류 기능별

- 택배, 특송, 소포(CEP)

- 목적지 유형별

- 국내

- 국제

- 목적지 유형별

- 화물 포워딩

- 수송수단별

- 항공

- 해상 및 내륙 수로

- 기타

- 수송수단별

- 화물 수송

- 수송수단별

- 항공

- 철도

- 도로

- 해상 및 내륙 수로

- 파이프라인

- 수송수단별

- 창고 보관 및 저장

- 온도 관리별

- 비온도 관리

- 온도 관리

- 온도 관리별

- 기타 서비스

- 택배, 특송, 소포(CEP)

- 최종 사용자 산업별

- 농업, 어업, 임업

- 건설

- 제조업

- 석유 및 가스, 광업 및 채석업

- 도매 및 소매업

- 기타

- 지역별

- 아랍에미리트(UAE)

- 사우디아라비아

- 카타르

- 오만

- 쿠웨이트

- 나이지리아

- 남아프리카

- 기타 중동 및 아프리카

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- DHL

- Aramex

- Gulf Agency Company(GAC)

- RAK Logistics

- Al-Futtaim Logistics

- Almajdouie Group

- Gulf Warehousing Company

- RSA Global

- Saudi Transport & Investment Co.(Mubarrad)

- City Logistics

- BLG Logistics

- Kuehne Nagel

- CEVA Logistics

- DSV

- Rhenus Logistics

- ATC Allied Transport

- Barloworld Logistics

- Unitrans Supply Chain Solutions(Pty) Ltd

- Cargo Carriers(Pty) Limited

- Compass Logistics International

제7장 시장 기회 및 미래 전망

CSM 26.01.21Middle East And Africa Freight And Logistics Market size in 2026 is estimated at USD 321.36 billion, growing from 2025 value of USD 305.07 billion with 2031 projections showing USD 416.75 billion, growing at 5.34% CAGR over 2026-2031.

The growth outlook flows from the region's pivotal position linking Asia, Europe, and Africa, combined with heavy infrastructure spending and permanent capacity upgrades triggered by Red Sea shipping disruptions. E-commerce expansion, the rollout of new multimodal corridors, and a surge in cold-chain demand strengthen baseline tonnage and yield per shipment. Sovereign wealth funds, free trade agreements, and digital freight platforms reinforce competitive intensity while mitigating geopolitical volatility. Operators that maximize network density, technology adoption, and sustainable practices are positioned to capture outsized returns.

Middle East And Africa Freight And Logistics Market Trends and Insights

E-commerce boom and cross-border retail

Cross-border e-commerce lifts last-mile shipment frequency, with domestic CEP covering 67.88% of traffic while international CEP advances at a 5.77% CAGR through 2030. Logistics providers are scaling automated sortation hubs and multi-carrier APIs that link Jebel Ali Port to Al Maktoum International Airport. Gulf operators deploy AI routing and collaborate with local universities to fill digital talent gaps. Omnichannel retailers demand integrated fulfillment that merges warehousing, click-and-collect, and door delivery, shifting volume toward express networks.

Mega-investments in multimodal logistics infrastructure

Saudi Arabia earmarked USD 133.3 billion for ports, airports, and railways through 2030, including Port of NEOM's first fully automated cranes slated for 2026 launch. DP World's USD 2.5 billion program and record USD 20 billion 2024 revenue signal deep private capital engagement. Automation and renewable energy integration compress dwell times and improve cost curves, reshaping transshipment competitiveness.

Uneven road, rail, and port infrastructure

Infrastructure gaps raise logistics costs for landlocked African economies relying on coastal gateways. The African Development Bank cites road density disparities and underfunded common-user marine assets as persistent bottlenecks. PPP corridors and toll finance frameworks attract limited private capital outside mining routes. Concentrated capacity in a handful of hubs heightens vulnerability to weather or labor stoppages, stalling hinterland market penetration.

Other drivers and restraints analyzed in the detailed report include:

- Cold-chain demand for pharma and perishables

- Rapid adoption of digital freight platforms and real-time visibility tools

- Red Sea/Suez chokepoint disruptions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Wholesale and retail trade contributed 33.92% of 2025 revenue, while manufacturing posts the fastest 5.58% CAGR through 2031 as localization and industrial parks proliferate. Oil, gas, and mining logistics remain sizable, supported by commodity flows and energy security spending. Construction logistics taps infrastructure mega-projects, and agri-food shipments expand under food-security strategies.

Nigeria's USD 20 billion Ogidigben industrial park underscores demand for specialized heavy-lift and project cargo services. Just-in-time production requires synchronized inbound material flows, elevating demand for real-time tracking and predictive inventory analytics

Freight transport retained 59.21% of the Middle East and Africa freight and logistics market in 2025, while courier, express, and parcel leads growth at 5.57% CAGR to 2031. Road-based bulk remains foundational, yet time-definite parcels capture e-commerce tailwinds. Freight forwarding and warehousing post steady gains, and temperature-controlled storage earns premium margins. Technology-driven value-added services under "other" activities scale quickly, feeding demand for end-to-end digital orchestration.

International integrators pledge nine-figure capex for hubs, whereas Aramex leverages ADQ backing to consolidate regional share. Robotics and AI inventory tools widen productivity differentials in Gulf warehouses, creating platforms that fuse parcel delivery, cross-dock, and forwarding under a single interface.

The Middle East and Africa Freight and Logistics Market Report is Segmented by Logistics Function (Freight Forwarding, Freight Transport, and More), End User Industry (Agriculture, Fishing, and Forestry, Construction, Manufacturing, Oil and Gas, Mining and Quarrying, Wholesale and Retail Trade, and Others), Geography (United Arab Emirates, Saudi Arabia, Nigeria, and More). Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- DHL

- Aramex

- Gulf Agency Company (GAC)

- RAK Logistics

- Al-Futtaim Logistics

- Almajdouie Group

- Gulf Warehousing Company

- RSA Global

- Saudi Transport & Investment Co. (Mubarrad)

- City Logistics

- BLG Logistics

- Kuehne + Nagel

- CEVA Logistics

- DSV

- Rhenus Logistics

- ATC Allied Transport

- Barloworld Logistics

- Unitrans Supply Chain Solutions (Pty) Ltd

- Cargo Carriers (Pty) Limited

- Compass Logistics International

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-Commerce Boom and Cross-Border Retail

- 4.2.2 Mega-Investments in Multimodal Logistics Infrastructure

- 4.2.3 Growth of FTAs and Emerging Trade Corridors

- 4.2.4 Cold-Chain Demand for Pharma and Perishables

- 4.2.5 Warehouse Automation to Offset Labour Shortages

- 4.2.6 Rapid Adoption of Digital Freight Platforms and Real-Time Visibility Tools

- 4.3 Market Restraints

- 4.3.1 Uneven Road, Rail and Port Infrastructure

- 4.3.2 Complex Customs Rules and Border Delays

- 4.3.3 Red-Sea/Suez Chokepoint Disruptions

- 4.3.4 Driver Shortages and Localisation Policies

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Geopolitics & Pandemics

5 Market Size & Growth Forecasts

- 5.1 By Logistics Function

- 5.1.1 Courier, Express, and Parcel (CEP)

- 5.1.1.1 By Destination Type

- 5.1.1.1.1 Domestic

- 5.1.1.1.2 International

- 5.1.1.1 By Destination Type

- 5.1.2 Freight Forwarding

- 5.1.2.1 By Mode of Transport

- 5.1.2.1.1 Air

- 5.1.2.1.2 Sea and Inland Waterways

- 5.1.2.1.3 Others

- 5.1.2.1 By Mode of Transport

- 5.1.3 Freight Transport

- 5.1.3.1 By Mode of Transport

- 5.1.3.1.1 Air

- 5.1.3.1.2 Rail

- 5.1.3.1.3 Road

- 5.1.3.1.4 Sea and Inland Waterways

- 5.1.3.1.5 Pipelines

- 5.1.3.1 By Mode of Transport

- 5.1.4 Warehousing and Storage

- 5.1.4.1 By Temperature Control

- 5.1.4.1.1 Non-Temperatured Control

- 5.1.4.1.2 Temperatured Control

- 5.1.4.1 By Temperature Control

- 5.1.5 Other Services

- 5.1.1 Courier, Express, and Parcel (CEP)

- 5.2 By End User Industry

- 5.2.1 Agriculture, Fishing, and Forestry

- 5.2.2 Construction

- 5.2.3 Manufacturing

- 5.2.4 Oil and Gas, Mining and Quarrying

- 5.2.5 Wholesale and Retail Trade

- 5.2.6 Others

- 5.3 By Geography

- 5.3.1 United Arab Emirates

- 5.3.2 Saudi Arabia

- 5.3.3 Qatar

- 5.3.4 Oman

- 5.3.5 Kuwait

- 5.3.6 Nigeria

- 5.3.7 South Africa

- 5.3.8 Rest of Middle East and Africa

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 DHL

- 6.4.2 Aramex

- 6.4.3 Gulf Agency Company (GAC)

- 6.4.4 RAK Logistics

- 6.4.5 Al-Futtaim Logistics

- 6.4.6 Almajdouie Group

- 6.4.7 Gulf Warehousing Company

- 6.4.8 RSA Global

- 6.4.9 Saudi Transport & Investment Co. (Mubarrad)

- 6.4.10 City Logistics

- 6.4.11 BLG Logistics

- 6.4.12 Kuehne + Nagel

- 6.4.13 CEVA Logistics

- 6.4.14 DSV

- 6.4.15 Rhenus Logistics

- 6.4.16 ATC Allied Transport

- 6.4.17 Barloworld Logistics

- 6.4.18 Unitrans Supply Chain Solutions (Pty) Ltd

- 6.4.19 Cargo Carriers (Pty) Limited

- 6.4.20 Compass Logistics International

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment