|

시장보고서

상품코드

1907263

유럽의 화물 및 물류 : 시장 점유율 분석, 업계 동향, 통계, 성장 예측(2026-2031년)Europe Freight And Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

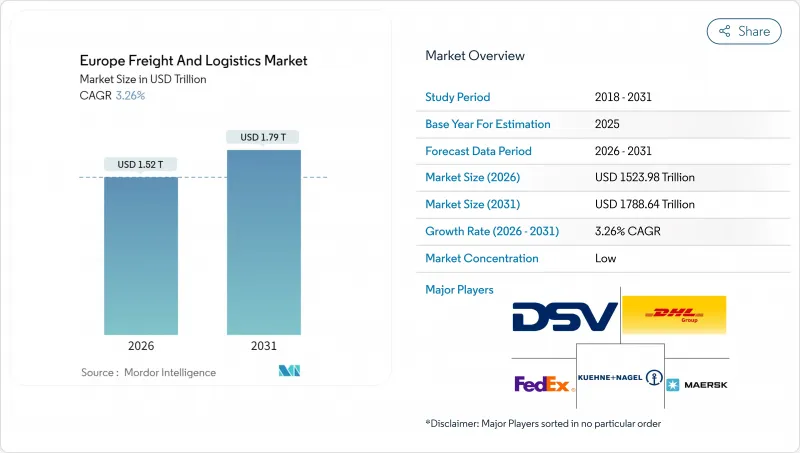

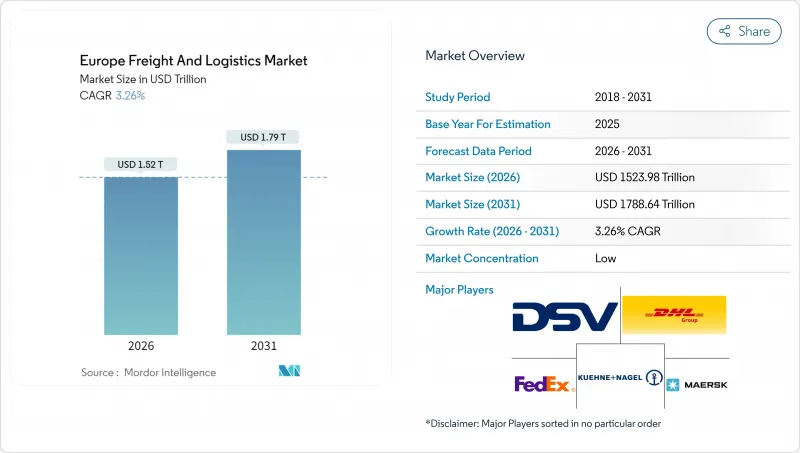

유럽의 화물 및 물류 시장은 2025년에 1조 4,758억 8,000만 달러로 평가되었으며, 2026년 1조 5,239억 8,000만 달러에서 2031년까지 1조 7,886억 4,000만 달러에 이를 것으로 예상됩니다.

예측 기간(2026-2031년)의 CAGR은 3.26%를 나타낼 전망입니다.

이 견조한 전망은 동대륙이 세계 무역 회랑에서 중심적인 역할을 하고 있는 것, 스마트 인프라에 대한 지속적인 투자, 공급망의 탈탄소화를 촉진하는 정책 압력에 기인하고 있습니다. 화물수송은 물류기능 중 가장 큰 점유율을 유지하고 있지만, 국경을 넘은 전자상거래가 유통모델을 재구축하는 가운데 택배·속달·소포(CEP) 업무가 가장 빠른 성장을 기록하고 있습니다. 범유럽 5G 회랑에 의한 실시간 네트워크 가시화와 도로 수송보다 철도를 우대하는 EU 그린딜 시책이 함께, 수송 루트의 경제성이 재구축되고 있습니다. 동시에 고적층 제조업의 급속한 회귀, 자동화 택배박스의 보급 확대, 동유럽으로의 방위관련 물류 유입이 통합형 '유럽의 화물 및 물류 시장' 솔루션에 대한 새로운 수요를 환기하고 있습니다. 규모를 추구하는 주요 기업에 의한 M&A의 활성화, 콜드체인 자산에 대한 투자, 비용 절감과 안전성 향상을 약속하는 자율주행 야드트럭의 파일럿 인증 경쟁이 격화하는 가운데 경쟁 환경은 더욱 엄격해지고 있습니다.

유럽의 화물 및 물류 시장 동향 및 인사이트

범유럽 5G 회랑이 실시간 물류 시각화를 변화

디지털·유럽은 5G 인프라에 75억 유로(82억 7,000만 달러)를 투입해 물류 회랑을 최우선 과제로 자리매김하고 있습니다. 이 기반으로 센서를 풍부하게 탑재한 트럭·열차·선박이 위치 정보·상태·기상 데이터를 매밀리초 단위로 통신 가능하게 됩니다. FERNRIDE사는 2024년에 TUV SUD 인증을 취득하여 자율주행 트럭의 야드 프로덕션 환경에서의 운용을 실현했습니다. 예지 보전 분석은 이미 유럽 화물 및 물류 시장의 콜드체인에서 가동 중지 시간을 최대 20% 줄이고 냉장화물의 손실률을 줄였습니다.

EU 그린딜이 도로에서 철도로의 모달 이동을 가속

Fit-for-55 입법 패키지는 2030년까지 55%의 탄소 삭감을 의무화하여 화주가 장거리 트럭에서 철도와 수로로의 전환을 촉진합니다. 프랑스 단독으로도 2030년까지 인터모달 터미널에 11억 유로(12억 1,000만 달러)를 예산화하고 있습니다. 그러나 2024년 상반기의 철도화물 운송량은 전년 동기 대비 2.8% 감소하여 운송 모드 전환의 야심을 막는 용량 부족이 노출되었습니다. 해운 및 도로 운송에 대한 EU 배출권 거래 제도(EU ETS)의 추가 과징금 상승으로 유럽의 화물 및 물류 산업에서 철도 운송의 대안은 점차 비용 경쟁력을 높이고 있습니다.

운전자 부족의 위기가 임금 상승 나선을 유발

국제도로운송연합(IRU)의 시산에 의하면 운전자 부족은 50만명 규모이며, 2028년까지 74만 5,000명으로 부상할 가능성이 있습니다. 사업자 측은 연률 15-25%의 임금 인상을 실시하고 있으며, 주요 수송 루트에서의 도로화물 운임은 18-22% 상승하고 있습니다. 온도 관리 장치는 수요가 높은 허브에서 자격있는 운전자가 6만 유로의 급여 패키지를 요구하기 때문에 더 심각한 영향을 받고 있습니다.

부문 분석

2025년, 유럽 화물 및 물류 시장 점유율의 32.01%를 제조업이 차지했고 자동차, 기계, 화학제품이 핵심을 이루었습니다. 2조 달러 규모의 리쇼어링 투자로 운송량이 대륙간 루트로 편향되어 견조한 계약 물류 파이프라인이 유지되고 있습니다.

도매·소매업은 소비자용 EC 보급률 73%를 원동력으로 2026년부터 2031년에 걸쳐 연평균 CAGR 3.47%를 나타낼 전망입니다. 옴니채널 모델은 하이퍼로컬 배송을 요구하며 마이크로 완성 시설이 유리합니다. 건설물류는 차세대 EU 지출로부터 적당한 혜택을 받는 반면, 재생가능 에너지 프로젝트는 터빈 블레이드와 배터리 화학을 위한 특수화물 운송 경로를 도입하고 있습니다.

화물 운송은 유럽 화물 및 물류 시장 규모의 핵심이며 2025년에는 수익의 62.74%를 차지했습니다. CEP 사업은 규모가 작은 것으로, 2026년부터 2031년에 걸쳐 3.70%의 연평균 복합 성장률(CAGR)로 보다 급속히 확대되고 있습니다. 성장의 기반은 국경 간 EC에 있으며 국제 소포는 5.33%의 속도로 진전하고 있습니다. 디지털 통관 게이트웨이는 통관 사이클을 최대 2일간 단축하여 B2C 분야에서 반복 수요 증가로 이어지고 있습니다.

유럽의 화물 및 물류 시장은 자동 분류 시스템, 인공지능 루트 계획, 온도 관리 사물함과 같은 CEP 네트워크의 고도화에 의해 형성되고 있습니다. 다음날 배송의 실현에는 확장 가능한 도시형 프루필먼트 거점이 불가결하므로 창고 서비스도 동시에 확대하고 있습니다. 화물 운송은 멀티 모달 운송의 조합으로 적응을 추진하고 있으며 EU의 순환형 경제 규칙 하에서 역물류, 라벨링, 키팅 등 부가가치 서비스가 중요성을 늘리고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 지원(3개월간)

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 인구 동태

- 경제 활동별 GDP 분포

- 경제 활동별 GDP 성장률

- 인플레이션

- 경제적 성능과 프로파일

- 전자상거래 업계 동향

- 제조업의 동향

- 운송 및 저장 부문 GDP

- 수출 동향

- 수입 동향

- 연료 가격

- 트럭 운송 운영 비용

- 트럭 운송 차량 규모(유형별)

- 주요 트럭 공급업체

- 물류 성과

- 모달 점유율

- 해상 선박 적재 능력

- 정기선 해운 연결성

- 항만 기항 및 성과

- 화물 가격 동향

- 화물 톤수 동향

- 인프라

- 규제 프레임워크(도로 및 철도)

- 프랑스

- 독일

- 이탈리아

- 네덜란드

- 북유럽 국가

- 러시아

- 스페인

- 영국

- 규제 프레임워크(해양 및 항공)

- 프랑스

- 독일

- 이탈리아

- 네덜란드

- 북유럽 국가

- 러시아

- 스페인

- 영국

- 밸류체인 및 유통채널 분석

- 시장 성장 촉진요인

- 범유럽 5G 회랑의 전개

- EU 그린딜에 의한 모달 시프트 촉진책

- 중요 제조업의 국내 회귀

- 주요 도시권을 넘는 B2C 소구 배송의 급속한 밀도 확대

- 우크라이나 정세 후 방위 물류 수요 증가

- 자율 주행 야드 트럭의 시험 운용이 규모 확대 단계에 도달

- 시장 성장 억제요인

- 드라이버 부족으로 인플레이션 나선형

- 철도 네트워크의 용량 병목

- 항만노동조합에 의한 혼란

- 카본, 보더, 어저스트먼트 대응 코스트

- 시장에서의 기술 혁신

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 최종 사용자 산업

- 농업, 어업 및 임업

- 건설

- 제조

- 석유 및 가스, 광업 및 채석업

- 도매 및 소매

- 기타

- 로지스틱스 기능

- 택배, 특송 및 소포(CEP)

- 목적지 유형별

- 국내

- 국제

- 목적지 유형별

- 화물 운송 대행

- 운송 수단별

- 항공

- 해상 및 내륙 수로

- 기타

- 운송 수단별

- 화물 운송

- 운송 수단별

- 항공

- 파이프라인

- 철도

- 도로

- 해상 및 내륙 수로

- 운송 수단별

- 창고 및 보관

- 온도 관리 방식별

- 비온도 관리

- 온도 관리

- 온도 관리 방식별

- 기타 서비스

- 택배, 특송 및 소포(CEP)

- 국가

- 덴마크

- 핀란드

- 프랑스

- 독일

- 아이슬란드

- 이탈리아

- 네덜란드

- 노르웨이

- 러시아

- 스페인

- 스웨덴

- 영국

- 기타 유럽

제6장 경쟁 구도

- 시장 집중도

- 주요 전략적 움직임

- 시장 점유율 분석

- 기업 프로파일

- AP Moller-Maersk

- CH Robinson

- CMA CGM Group(Including CEVA Logistics)

- DACHSER

- DHL Group

- DSV A/S(Including DB Schenker)

- Expeditors International of Washington, Inc.

- FedEx

- GEFCO

- Hapag-Lloyd

- Hellmann Worldwide Logistics

- International Distributions Services(Including GLS)

- Kuehne Nagel

- La Poste Group

- Mainfreight

- Panattoni Europe

- Rhenus Group

- SNCF Group

- United Parcel Service of America, Inc.(UPS)

- XPO, Inc.

제7장 시장 기회와 향후 전망

KTH 26.01.20The Europe freight and logistics market was valued at USD 1475.88 billion in 2025 and estimated to grow from USD 1523.98 billion in 2026 to reach USD 1788.64 billion by 2031, at a CAGR of 3.26% during the forecast period (2026-2031).

The solid outlook stems from the continent's central role in global trade corridors, continued investments in smart infrastructure, and policy pressure to decarbonize supply chains. Freight transport retains the largest logistics function share, while courier, express, and parcel (CEP) activities record the fastest growth as cross-border e-commerce reorders distribution models. Real-time network visibility enabled by the Pan-European 5G corridor, together with EU Green Deal incentives that favor rail over road, is reshaping route economics. Simultaneously, the rapid reshoring of high-value manufacturing, wider deployment of automated parcel machines, and defense-related flows into Eastern Europe spur fresh demand for integrated "Europe freight and logistics market" solutions. Competitive dynamics intensify as scale players pursue M&A, invest in cold-chain assets, and race to certify autonomous yard-truck pilots that promise cost and safety gains.

Europe Freight And Logistics Market Trends and Insights

Pan-European 5G Corridor Transforms Real-Time Logistics Visibility

Digital Europe dedicates EUR 7.5 billion (USD 8.27 billion) to 5G infrastructure, with logistics lanes topping the priority list. This backbone enables sensor-rich trucks, trains, and vessels to communicate location, condition, and weather data every millisecond. FERNRIDE secured TUV SUD certification in 2024, allowing autonomous trucks to operate in live yard environments. Predictive maintenance analytics already trim downtime by up to 20% and reduce chilled-cargo loss rates in the "Europe freight and logistics market" cold chain.

EU Green Deal Accelerates Modal Shift from Road to Rail

The Fit-for-55 legislative package compels a 55% carbon cut by 2030, encouraging shippers to swap long-haul trucks for rail or waterways. France alone earmarked EUR 1.1 billion (USD 1.21 billion) for intermodal terminals through 2030. Yet rail freight fell 2.8% year-on-year in H1 2024, exposing capacity shortfalls that hinder modal ambitions. Rising EU ETS surcharges on maritime and road make the rail alternative progressively cost-competitive in the Europe freight and logistics industry.

Driver Shortage Crisis Triggers Wage Inflation Spiral

The International Road Transport Union calculates a 500,000-driver shortfall that could swell to 745,000 by 2028. Operators have raised wages 15-25% annually, driving road freight rates up 18-22% in major corridors. Temperature-controlled units feel the pinch more acutely, as qualified drivers command EUR 60,000 packages in high-demand hubs.

Other drivers and restraints analyzed in the detailed report include:

- Critical Manufacturing Reshoring Drives Logistics Demand

- B2C Parcel Density Expands Beyond Tier-1 Cities

- Port Labour Disruptions Create Vessel Backlogs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Manufacturing supplied 32.01% of the Europe freight and logistics market share in 2025, anchored by automotive, machinery, and chemicals. Reshoring capital outlays of USD 2 trillion tilt volumes toward continental routes, sustaining robust contract-logistics pipelines.

Wholesale and retail trade, powered by 73% consumer e-commerce penetration, grows at 3.47% CAGR (2026-2031). Omnichannel models demand hyper-local distribution, favoring micro-fulfillment facilities. Construction logistics benefits moderately from Next Generation EU spending, while renewable-energy projects introduce special-cargo lanes for turbine blades and battery chemicals.

Freight transport remained the backbone of the Europe freight and logistics market size, accounting for 62.74% revenue in 2025. CEP operations, though smaller, are scaling faster at a 3.70% CAGR between 2026-2031. Growth is rooted in cross-border e-commerce, with international parcels advancing at a 5.33% pace. Digital customs gateways shorten clearance cycles by up to two days, translating into repeat B2C volumes.

The Europe freight and logistics market is increasingly shaped by CEP network upgrades such as automated sortation, AI-guided route planning, and temperature-controlled lockers. Warehousing services rise in tandem, as next-day delivery promises hinge on expandable urban fulfillment nodes. Freight forwarding adapts through multimodal bundles, while value-added services-reverse logistics, labeling, kitting-gain relevance under EU circular-economy rules.

The Europe Freight and Logistics Market Report Segments the Industry Into End User Industry (Agriculture, Fishing, and Forestry, Construction, Manufacturing, Oil and Gas, Mining and Quarrying, Wholesale and Retail Trade, and More), by Logistics Function (Courier, Express, and Parcel, Freight Forwarding, Freight Transport, and More), and Country (Denmark, Finland, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- A.P. Moller - Maersk

- C.H. Robinson

- CMA CGM Group (Including CEVA Logistics)

- DACHSER

- DHL Group

- DSV A/S (Including DB Schenker)

- Expeditors International of Washington, Inc.

- FedEx

- GEFCO

- Hapag-Lloyd

- Hellmann Worldwide Logistics

- International Distributions Services (Including GLS)

- Kuehne+Nagel

- La Poste Group

- Mainfreight

- Panattoni Europe

- Rhenus Group

- SNCF Group

- United Parcel Service of America, Inc. (UPS)

- XPO, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Demographics

- 4.3 GDP Distribution by Economic Activity

- 4.4 GDP Growth by Economic Activity

- 4.5 Inflation

- 4.6 Economic Performance and Profile

- 4.6.1 Trends in E-Commerce Industry

- 4.6.2 Trends in Manufacturing Industry

- 4.7 Transport and Storage Sector GDP

- 4.8 Export Trends

- 4.9 Import Trends

- 4.10 Fuel Price

- 4.11 Trucking Operational Costs

- 4.12 Trucking Fleet Size by Type

- 4.13 Major Truck Suppliers

- 4.14 Logistics Performance

- 4.15 Modal Share

- 4.16 Maritime Fleet Load Carrying Capacity

- 4.17 Liner Shipping Connectivity

- 4.18 Port Calls and Performance

- 4.19 Freight Pricing Trends

- 4.20 Freight Tonnage Trends

- 4.21 Infrastructure

- 4.22 Regulatory Framework (Road and Rail)

- 4.22.1 France

- 4.22.2 Germany

- 4.22.3 Italy

- 4.22.4 Netherlands

- 4.22.5 Nordics

- 4.22.6 Russia

- 4.22.7 Spain

- 4.22.8 United Kingdom

- 4.23 Regulatory Framework (Sea and Air)

- 4.23.1 France

- 4.23.2 Germany

- 4.23.3 Italy

- 4.23.4 Netherlands

- 4.23.5 Nordics

- 4.23.6 Russia

- 4.23.7 Spain

- 4.23.8 United Kingdom

- 4.24 Value Chain and Distribution Channel Analysis

- 4.25 Market Drivers

- 4.25.1 Pan-European 5G Corridor Roll-Out

- 4.25.2 EU Green Deal Modal-Shift Incentives

- 4.25.3 Reshoring of Critical Manufacturing

- 4.25.4 Rapid B2C Parcel Density Beyond Tier-1 Cities

- 4.25.5 Defence-Logistics Uptick Post-Ukraine

- 4.25.6 Autonomous Yard-Truck Pilots Reaching Scale

- 4.26 Market Restraints

- 4.26.1 Driver-Shortage Inflation Spiral

- 4.26.2 Rail Network Capacity Bottlenecks

- 4.26.3 Port Labour-Union Disruptions

- 4.26.4 Carbon-Border Adjustment Compliance Costs

- 4.27 Technology Innovations in the Market

- 4.28 Porter's Five Forces Analysis

- 4.28.1 Threat of New Entrants

- 4.28.2 Bargaining Power of Buyers

- 4.28.3 Bargaining Power of Suppliers

- 4.28.4 Threat of Substitutes

- 4.28.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 End User Industry

- 5.1.1 Agriculture, Fishing, and Forestry

- 5.1.2 Construction

- 5.1.3 Manufacturing

- 5.1.4 Oil and Gas, Mining and Quarrying

- 5.1.5 Wholesale and Retail Trade

- 5.1.6 Others

- 5.2 Logistics Function

- 5.2.1 Courier, Express, and Parcel (CEP)

- 5.2.1.1 By Destination Type

- 5.2.1.1.1 Domestic

- 5.2.1.1.2 International

- 5.2.1.1 By Destination Type

- 5.2.2 Freight Forwarding

- 5.2.2.1 By Mode of Transport

- 5.2.2.1.1 Air

- 5.2.2.1.2 Sea and Inland Waterways

- 5.2.2.1.3 Others

- 5.2.2.1 By Mode of Transport

- 5.2.3 Freight Transport

- 5.2.3.1 By Mode of Transport

- 5.2.3.1.1 Air

- 5.2.3.1.2 Pipelines

- 5.2.3.1.3 Rail

- 5.2.3.1.4 Road

- 5.2.3.1.5 Sea and Inland Waterways

- 5.2.3.1 By Mode of Transport

- 5.2.4 Warehousing and Storage

- 5.2.4.1 By Temperature Control

- 5.2.4.1.1 Non-Temperature Controlled

- 5.2.4.1.2 Temperature Controlled

- 5.2.4.1 By Temperature Control

- 5.2.5 Other Services

- 5.2.1 Courier, Express, and Parcel (CEP)

- 5.3 Country

- 5.3.1 Denmark

- 5.3.2 Finland

- 5.3.3 France

- 5.3.4 Germany

- 5.3.5 Iceland

- 5.3.6 Italy

- 5.3.7 Netherlands

- 5.3.8 Norway

- 5.3.9 Russia

- 5.3.10 Spain

- 5.3.11 Sweden

- 5.3.12 United Kingdom

- 5.3.13 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 A.P. Moller - Maersk

- 6.4.2 C.H. Robinson

- 6.4.3 CMA CGM Group (Including CEVA Logistics)

- 6.4.4 DACHSER

- 6.4.5 DHL Group

- 6.4.6 DSV A/S (Including DB Schenker)

- 6.4.7 Expeditors International of Washington, Inc.

- 6.4.8 FedEx

- 6.4.9 GEFCO

- 6.4.10 Hapag-Lloyd

- 6.4.11 Hellmann Worldwide Logistics

- 6.4.12 International Distributions Services (Including GLS)

- 6.4.13 Kuehne+Nagel

- 6.4.14 La Poste Group

- 6.4.15 Mainfreight

- 6.4.16 Panattoni Europe

- 6.4.17 Rhenus Group

- 6.4.18 SNCF Group

- 6.4.19 United Parcel Service of America, Inc. (UPS)

- 6.4.20 XPO, Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment