|

시장보고서

상품코드

1906891

프랑스의 화물 및 물류 : 시장 점유율 분석, 업계 동향, 통계, 성장 예측(2026-2031년)France Freight And Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

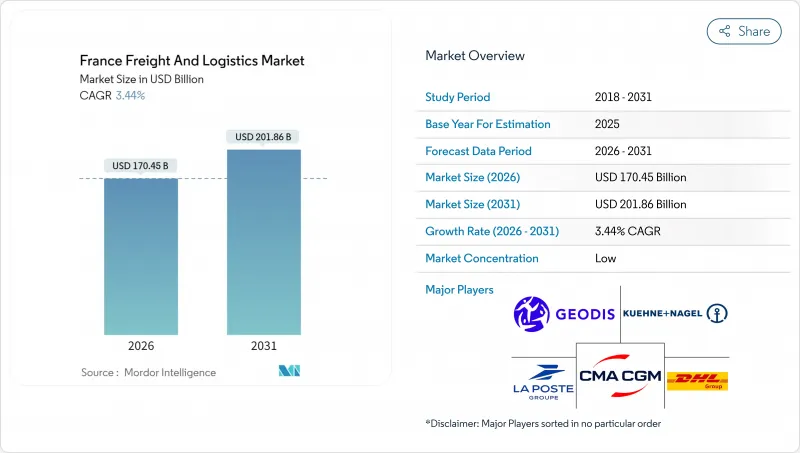

프랑스의 화물 및 물류 시장은 2025년 1,647억 8,000만 달러로 평가되었고, 2026년에 1,704억 5,000만 달러로 성장할 것으로 보입니다. 2026-2031년에 걸쳐 CAGR 3.44%로 성장이 예상되며, 2031년까지 2,000달러에 이를 것으로 예측됩니다.

지속적인 인프라 개선, 급증하는 전자상거래 소포 물동량, 그리고 종이 없는 통관 절차의 전면적 도입이 종합적으로 성장 궤도를 강화하고 있습니다. 정부의 20억 유로(22억 달러) 규모의 ‘Fonds vert’ 프로그램은 모든 운송 수단에 걸쳐 탈탄소화 프로젝트를 가속화하며, 신규 친환경 자산의 비용을 낮추는 직접 보조금과 세액 공제를 제공합니다. 합병 움직임?특히 CMA CGM의 52억 유로(57억 달러) 규모 볼로레 로지스틱스 인수?는 진정한 종단간 서비스를 제공할 수 있는 수직 통합형 공급업체를 창출합니다. 디지털 차량 텔레매틱스, 수소 취급 장비, AI 기반 위험 엔진은 자산 활용도를 높이는 동시에 배출량 발자국을 축소하여 ‘Fit-for-55’ 의무가 강화됨에 따라 경쟁 우위를 뒷받침합니다.

프랑스의 화물 및 물류 시장 동향 및 인사이트

통관 절차의 디지털화

유럽연합 관세법(Union Customs Code)에 따른 전자 신고의 전면 도입으로 규정 준수 화물의 통관 시간이 최대 30% 단축되어 고부가가치 자동차 및 항공우주 공급망에 혜택을 주고 있습니다. AI 기반 위험 엔진은 선별적 검사를 가능하게 하여 부족한 국경 관리관을 복잡한 검사에 투입할 수 있게 하고, 칼레(Calais)와 르아브르(Le Havre)의 트럭 체류 시간을 단축합니다. 화물 운송업체들은 문서 작업 흐름이 원활해지고 중개 수수료가 낮아져 프랑스의 화물 및 물류 시장의 전반적인 경쟁력이 향상되었다고 보고합니다.

전자상거래 소포 취급량 급증

소비자들이 더 엄격한 배송 시간대를 요구함에 따라 2024년 국내 소포 물량은 전년 대비 20% 이상 증가했습니다. Chronopost와 같은 운영사들은 저공해 구역 규정을 준수하기 위해 도시형 마이크로 허브를 개설하고 화물 자전거 차량을 확대했습니다. 자동 분류 및 AI 경로 최적화로 정차 밀도가 개선되어 네트워크 복잡성이 증가함에도 소포당 비용을 억제하고 있습니다.

운전자 부족과 노화하는 노동력

은퇴자가 신규 입사자를 초과함에 따라 2026년까지 운전직의 약 60%가 공석으로 남을 것으로 예상됩니다. 면허 취득 비용이 3,000유로(3,310달러)를 초과하여 젊은 지원자들의 의욕을 저하시키고 있습니다. 임금 인플레이션으로 마진이 축소되면서 소규모 차량 운영사들은 하도급을 하거나 사업을 접어야 했으며, 이는 프랑스의 화물 및 물류 산업의 경쟁 구도를 재편하고 있습니다.

부문 분석

2025년 프랑스의 화물 및 물류 시장 점유율에서 제조업이 31.21%를 차지했으며, 이는 자동차, 항공우주, 제약 산업이 고정밀 JIT(적시) 배송에 의존했기 때문입니다. 인바운드 시퀀싱과 공급업체 관리 재고(VMI)는 창고 체류 시간을 낮게 유지하여 정교한 IT 인터페이스를 보유한 공급업체에 유리합니다. 도매 및 소매 무역 부문은 2026-2031년 연평균 성장률(CAGR) 3.62%로 가장 빠르게 성장하며, 옴니채널 모델은 인구 밀집 지역 인근의 소규모 물류 센터를 선호합니다.

방위 분야의 재군비 지출에 의해 기밀 보관이나 호송 운송 수요가 지속되는 한편, 식량 안보의 우선도로부터 농산물, 식품의 운송량은 견조하게 추이합니다. 에너지 전환 정책으로 인해 화석 연료 운송이 감소하는 동안 프랑스의 화물 및 물류 시장 내 운송 경로의 수익 구조가 재구성되었습니다.

2025년 현재 화물 운송은 프랑스의 화물 및 물류 시장 규모의 59.58%를 차지했습니다. 이것은 중공업 흐름과 월경 무역에 대응하는 통합 도로, 철도, 해상 네트워크에 의해 지원됩니다. IoT 기반 차량 플랫폼은 공차 운행을 줄이고 자산 회전율을 높여 디젤 가격 상승 속에서도 마진을 유지합니다. 규모는 작지만 CEP(소포·택배) 부문이 2026-2031년 연평균 3.88% 성장률로 가장 빠르게 성장하며, 주요 도시의 당일 배송 기대를 반영합니다. 소비자와 가까운 곳으로 재고 재배치 수요가 증가하는 가운데, 화물 운송 대행은 관세 및 복합 운송 조정 측면에서 여전히 중요합니다.

엔드 투 엔드 가시성에 대한 고객의 요구로 인해 운송사들은 운송, 보관, 반품 서비스를 단일 계약으로 묶어 제공해야 합니다. 데이터 분석과 생태계 최적화 경로 설정을 마스터한 기업들이 치열한 프랑스의 화물 및 물류 시장에서 점유율을 확대하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 인구동태

- 경제 활동별 GDP 분포

- 경제활동별 GDP 성장률

- 인플레이션

- 경제적 성능과 프로파일

- 전자상거래 업계 동향

- 제조업의 동향

- 운송, 보관 부문의 GDP

- 수출 동향

- 수입 동향

- 연료 가격

- 트럭 운송 운영 비용

- 트럭 운송 차량 규모(유형별)

- 주요 트럭 공급업체

- 물류 성능

- 운송 모드별 점유율

- 해상 운송선대의 적재능력

- 정기선 운송의 접속성

- 기항지와 성능

- 화물운임 동향

- 화물 톤수 동향

- 인프라

- 규제 프레임워크(도로 및 철도)

- 규제 프레임워크(해운, 항공)

- 밸류체인 및 유통채널 분석

- 시장 성장 촉진요인

- 세관절차의 디지털화

- 전자상거래 소포 물량 급증

- 복합운송 전환을 위한 그린 세제 혜택

- EU 공급망의 근거리화

- 방위 재군비 물류 수요

- 수소 연료 보급 회랑에 대한 투자

- 시장 성장 억제요인

- 운전자 부족과 노동력의 고령화

- EU 「Fit-For-55」규제 대응에 따른 설비 투자 부담

- 철도 네트워크의 용량 병목(여객 우선)

- 도시 라스트 마일 배송 존의 포화 상태

- 시장의 기술 혁신

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 최종 사용자 산업

- 농업, 어업, 임업

- 건설업

- 제조업

- 석유 및 가스, 광업, 채석업

- 도매, 소매업

- 기타

- 물류 기능

- 택배, 특송 및 소포(CEP)

- 목적지별

- 국내

- 국제

- 목적지별

- 화물 운송

- 운송 수단별

- 항공

- 해상, 내륙 수로

- 기타

- 운송 수단별

- 화물 운송

- 운송 수단별

- 항공

- 파이프라인

- 철도

- 도로

- 해상, 내륙 수로

- 운송 수단별

- 창고 보관

- 온도 관리별

- 비온도 관리

- 온도 관리

- 온도 관리별

- 기타 서비스

- 택배, 특송 및 소포(CEP)

제6장 경쟁 구도

- 시장 집중도

- 주요 전략적 움직임

- 시장 점유율 분석

- 기업 프로파일

- Balguerie Group

- CLASQUIN

- CMA CGM Group(Including CEVA Logistics)

- DACHSER

- DHL Group

- Dimotrans Group

- DSV A/S(Including DB Schenker)

- FedEx

- FM Logistic

- GEODIS

- Groupe CAT

- Kuehne Nagel

- La Poste Group

- Rhenus Group

- Savino Del Bene SpA

- SEKO Logistics

- STEF Group

- United Parcel Service of America, Inc.(UPS)

- XPO, Inc.

- Ziegler Group

제7장 시장 기회와 장래의 전망

HBR 26.02.04The France freight and logistics market is expected to grow from USD 164.78 billion in 2025 to USD 170.45 billion in 2026 and is forecast to reach USD 201.86 billion by 2031 at 3.44% CAGR over 2026-2031.

Sustained infrastructure upgrades, fast-rising e-commerce parcel flows, and full rollout of paperless customs procedures collectively reinforce the growth trajectory. The government's EUR 2 billion (USD 2.2 billion) Fonds vert program accelerates decarbonization projects across all modes, offering direct grants and tax credits that lower the cost of new green assets. Consolidation moves-most notably CMA CGM's EUR 5.2 billion (USD 5.7 billion) purchase of Bollore Logistics-create vertically integrated providers able to sell truly end-to-end services. Digital fleet telematics, hydrogen handling equipment, and AI-enabled risk engines raise asset utilization while shrinking emissions footprints, underpinning competitive advantage as Fit-for-55 obligations tighten.

France Freight And Logistics Market Trends and Insights

Digitalization of Customs Procedures

Full deployment of electronic declarations under the Union Customs Code has cut clearance times for compliant cargo by up to 30%, benefiting high-value automotive and aerospace supply chains. AI-driven risk engines enable selective inspections, freeing scarce border officers for complex checks and reducing truck dwell times at Calais and Le Havre. Freight forwarders report smoother document workflows and lower brokerage fees, enhancing the overall competitiveness of the France freight and logistics market.

Surge in E-commerce Parcel Volumes

Domestic parcel flows grew more than 20% year-on-year in 2024 as consumers demanded tighter delivery windows; operators like Chronopost opened urban micro-hubs and expanded cargo-bike fleets to comply with low-emission zones. Automated sortation and AI route optimization improve stop density, keeping cost per parcel in check even as network complexity rises.

Driver Shortage and Ageing Workforce

An estimated 60% of driving posts could remain vacant by 2026 as retirements outpace new entrants; licensing costs exceed EUR 3,000 (USD 3,310), discouraging younger applicants. Wage inflation erodes margins, forcing small fleets to subcontract or exit, reshaping the competitive fabric of the France freight and logistics industry.

Other drivers and restraints analyzed in the detailed report include:

- Green Tax Incentives for Intermodal Shift

- Near-Shoring of EU Supply Chains

- CAPEX Burden of Fit-for-55 Compliance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Manufacturing held 31.21% of the France freight and logistics market share in 2025 as automotive, aerospace, and pharmaceuticals depended on high-precision just-in-time deliveries. Inbound sequencing and vendor-managed inventory keep warehouse dwell times low, favoring providers with sophisticated IT interfaces. Wholesale and retail trade rises the fastest at 3.62% CAGR (2026-2031), with omnichannel models favoring micro-fulfillment locations near dense populations.

Defense re-armament spending sustains demand for classified storage and escorted convoys, while agri-food volumes stay resilient on food-security priorities. Energy-transition policies reduce fossil-fuel traffic, reshaping lane profitability within the France freight and logistics market.

Freight transport delivered 59.58% of the France freight and logistics market size in 2025, supported by integrated road-rail-sea networks that cater to heavy industrial flows and cross-border trade. IoT-enabled fleet platforms cut empty-running and boost asset turns, preserving margins as diesel prices rise. CEP, though smaller, is the fastest-growing slice, with a 3.88% CAGR between 2026-2031, reflecting same-day delivery expectations in major cities. Inventory repositioning closer to consumers fuels warehousing demand, while freight forwarding retains relevance for customs and multimodal coordination.

Customer pressure for end-to-end visibility compels providers to bundle transport, storage, and returns services into single contracts. Players that master data analytics and eco-optimized routing gain share in the fiercely contested France freight and logistics market.

The France Freight and Logistics Market Report is Segmented by End User Industry (Agriculture, Fishing, and Forestry, Construction, Manufacturing, Oil and Gas, Mining and Quarrying, Wholesale and Retail Trade, and Others) and by Logistics Function (Courier, Express, and Parcel (CEP), Freight Forwarding, Freight Transport, Warehousing and Storage, and Other Services). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Balguerie Group

- CLASQUIN

- CMA CGM Group (Including CEVA Logistics)

- DACHSER

- DHL Group

- Dimotrans Group

- DSV A/S (Including DB Schenker)

- FedEx

- FM Logistic

- GEODIS

- Groupe CAT

- Kuehne+Nagel

- La Poste Group

- Rhenus Group

- Savino Del Bene SpA

- SEKO Logistics

- STEF Group

- United Parcel Service of America, Inc. (UPS)

- XPO, Inc.

- Ziegler Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Demographics

- 4.3 GDP Distribution by Economic Activity

- 4.4 GDP Growth by Economic Activity

- 4.5 Inflation

- 4.6 Economic Performance and Profile

- 4.6.1 Trends in E-Commerce Industry

- 4.6.2 Trends in Manufacturing Industry

- 4.7 Transport and Storage Sector GDP

- 4.8 Export Trends

- 4.9 Import Trends

- 4.10 Fuel Price

- 4.11 Trucking Operational Costs

- 4.12 Trucking Fleet Size by Type

- 4.13 Major Truck Suppliers

- 4.14 Logistics Performance

- 4.15 Modal Share

- 4.16 Maritime Fleet Load Carrying Capacity

- 4.17 Liner Shipping Connectivity

- 4.18 Port Calls and Performance

- 4.19 Freight Pricing Trends

- 4.20 Freight Tonnage Trends

- 4.21 Infrastructure

- 4.22 Regulatory Framework (Road and Rail)

- 4.23 Regulatory Framework (Sea and Air)

- 4.24 Value Chain and Distribution Channel Analysis

- 4.25 Market Drivers

- 4.25.1 Digitalization of Customs Procedures

- 4.25.2 Surge in E-Commerce Parcel Volumes

- 4.25.3 Green Tax Incentives for Intermodal Shift

- 4.25.4 Near-Shoring of EU Supply Chains

- 4.25.5 Defence Re-Armament Logistics Demand

- 4.25.6 Hydrogen Refuelling Corridor Investments

- 4.26 Market Restraints

- 4.26.1 Driver Shortage and Ageing Workforce

- 4.26.2 CAPEX Burden of EU Fit-For-55 Compliance

- 4.26.3 Rail Network Capacity Bottlenecks (Passenger Priority)

- 4.26.4 Saturated Urban Last-Mile Delivery Zones

- 4.27 Technology Innovations in the Market

- 4.28 Porter's Five Forces Analysis

- 4.28.1 Threat of New Entrants

- 4.28.2 Bargaining Power of Buyers

- 4.28.3 Bargaining Power of Suppliers

- 4.28.4 Threat of Substitutes

- 4.28.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 End User Industry

- 5.1.1 Agriculture, Fishing, and Forestry

- 5.1.2 Construction

- 5.1.3 Manufacturing

- 5.1.4 Oil and Gas, Mining and Quarrying

- 5.1.5 Wholesale and Retail Trade

- 5.1.6 Others

- 5.2 Logistics Function

- 5.2.1 Courier, Express, and Parcel (CEP)

- 5.2.1.1 By Destination Type

- 5.2.1.1.1 Domestic

- 5.2.1.1.2 International

- 5.2.1.1 By Destination Type

- 5.2.2 Freight Forwarding

- 5.2.2.1 By Mode of Transport

- 5.2.2.1.1 Air

- 5.2.2.1.2 Sea and Inland Waterways

- 5.2.2.1.3 Others

- 5.2.2.1 By Mode of Transport

- 5.2.3 Freight Transport

- 5.2.3.1 By Mode of Transport

- 5.2.3.1.1 Air

- 5.2.3.1.2 Pipelines

- 5.2.3.1.3 Rail

- 5.2.3.1.4 Road

- 5.2.3.1.5 Sea and Inland Waterways

- 5.2.3.1 By Mode of Transport

- 5.2.4 Warehousing and Storage

- 5.2.4.1 By Temperature Control

- 5.2.4.1.1 Non-Temperature Controlled

- 5.2.4.1.2 Temperature Controlled

- 5.2.4.1 By Temperature Control

- 5.2.5 Other Services

- 5.2.1 Courier, Express, and Parcel (CEP)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Balguerie Group

- 6.4.2 CLASQUIN

- 6.4.3 CMA CGM Group (Including CEVA Logistics)

- 6.4.4 DACHSER

- 6.4.5 DHL Group

- 6.4.6 Dimotrans Group

- 6.4.7 DSV A/S (Including DB Schenker)

- 6.4.8 FedEx

- 6.4.9 FM Logistic

- 6.4.10 GEODIS

- 6.4.11 Groupe CAT

- 6.4.12 Kuehne+Nagel

- 6.4.13 La Poste Group

- 6.4.14 Rhenus Group

- 6.4.15 Savino Del Bene SpA

- 6.4.16 SEKO Logistics

- 6.4.17 STEF Group

- 6.4.18 United Parcel Service of America, Inc. (UPS)

- 6.4.19 XPO, Inc.

- 6.4.20 Ziegler Group

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment