|

시장보고서

상품코드

1906154

ID 거버넌스 및 관리(IGA) 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Identity Governance And Administration - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

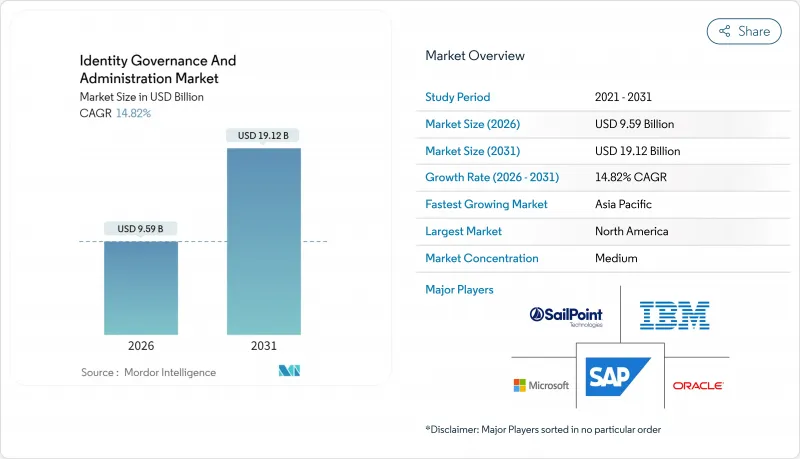

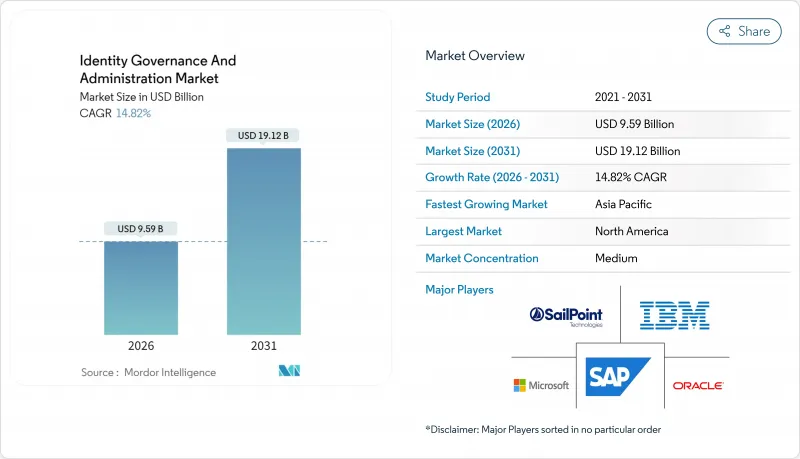

2026년 ID 거버넌스 및 관리 시장의 규모는 95억 9,000만 달러로 추정되며, 2025년 83억 6,000만 달러에서 성장하여, 2031년에는 191억 2,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지의 연평균 복합 성장률(CAGR)은 14.82%를 나타낼 전망입니다.

하이브리드 IT 환경에 대한 의존도가 높아지고 스푸핑 사기가 82% 급증함에 따라 보안 지출은 신원 중심 제어로 향하고 있습니다. 클라우드 제공 모델은 현재 신규 도입의 대부분을 뒷받침하고 있으며, 탄력적인 스케일링과 신속한 가치 실현의 필요성을 반영하고 있습니다. 지역별 지출 패턴은 분단화가 진행되고 있습니다. 북미는 성숙한 제로 트러스트 프로그램을 통해 도입 페이스를 리드하는 한편, 아시아는 현지 기업의 디지털화 가속화와 클라우드 네이티브 툴로의 비약적 이행에 의해 전체적인 성장을 견인하고 있습니다. 서비스 분야는 최대 수익원을 유지하며, 이는 사내 도입을 방해하는 기술 격차와 신원에 관한 매니지드 전문 지식에 대한 수요 증가를 반영합니다. 한편, 벤더 각사는 인증 워크플로와 머신러닝의 통합을 진행하여 권한 리뷰의 자동화와 검출 정밀도의 향상을 도모하고 있습니다. 이러한 변화는 경쟁 환경을 빠르게 변화시키고 있으며, 인접한 권한 접근 및 비인간 신원 분야에서 시장 기회를 확대하고 있습니다.

세계의 ID 거버넌스 및 관리 시장의 동향 및 인사이트

지속적인 액세스 인증을 위한 AI 구동 IGA 도입 증가

AI 탑재 툴은 현재 사용자와 비인간의 권한을 거의 실시간으로 검사하고, 고위험 이상을 식별함으로써 인증 피로를 최소화합니다. 이러한 기능을 도입한 기업은 리스크 감지의 정확성 향상과 관리 비용의 경감을 보였으며, 이 조합에 의해 거버넌스가 광대한 멀티 클라우드 환경으로 확장되고 있습니다. 생성형 AI는 또한 복잡한 권한 설명을 자연어로 재기록하여 비즈니스 매니저의 참여를 확대함과 동시에 고객센터의 대응 사이클을 단축하고 있습니다. 금융 서비스 및 기술 분야의 초기 도입 사례는 수동 검토가 비현실적이 된 세계적으로 분산된 노동력에 본 모델이 적합하다는 것을 시사합니다. 설명 가능한 AI 리뷰 엔진에 대한 신뢰를 높이는 조직이 늘어남에 따라 성장세는 더욱 높아질 것으로 예측됩니다.

유럽의 고도로 규제된 부문에서 PAM과 IGA 스위트의 융합

금융기관과 중요한 인프라 사업자는 권한 접근 통제와 광범위한 수명 주기 거버넌스를 융합시켜 툴 스프롤을 간소화합니다. 통합 제품군은 관리자 권한과 표준 사용자 권한 간의 중복을 줄이고 공격자가 목표로 하는 허점을 방지합니다. 주요 PAM 공급업체의 최근 인수는 거버넌스 모듈의 통합과 유럽의 디지털 업무 탄력성 법을 준수하는 컴플라이언스 지원 워크플로 제공을 위한 경쟁을 돋보이게 합니다. 조기 도입 기업은 감사 지적 사항의 감소와 증거 수집의 신속화를 보이고 있으며, 전 세계 자회사 전체적으로 통합 아키텍처 도입의 비즈니스 케이스가 강화되고 있습니다.

아이덴티티 엔지니어링 분야의 인력 부족이 복잡한 도입을 제약

디렉토리 아키텍처, 권한 모델 설계, 규제 매핑에 익숙한 전문가의 수요는 공급을 능가하고 있습니다. 대다수의 기업은 대규모 도입의 주요 장벽으로 인재 부족을 꼽고 있습니다. 이 갭은 임금 상승을 초래하고 특히 사이버 보안 인재가 부족한 신흥 시장에서는 프로젝트 기간의 장기화를 초래하고 있습니다. 벤더는 규범적 템플릿이나 매니지드 서비스로 대응하고 있지만, 많은 조직에서는 내부 전문 지식이 부족하기 때문에 정책 자동화 등의 고급 기능의 도입을 진전시키지 못하고 있습니다.

부문 분석

2025년 ID 거버넌스 및 관리 시장에서 수익의 56.42%는 서비스가 차지하였으며 이는 다양한 용도 환경을 통합하는 데 필요한 컨설팅 및 배포 노력을 반영합니다. 온프레미스, SaaS 및 운영 기술 계층에 걸친 권한 매핑에는 특히 감사 수준의 증거가 요구되는 규제 업계에서 도입 담당자의 존재가 필수적입니다. SaaS형 거버넌스 플랫폼의 등장으로 지출의 일부가 성과 기반의 매니지드 서비스로 이행하고 있습니다. 공급자는 소프트웨어 구독과 일상적인 관리 업무를 고정 요금 모델에 통합합니다.

그러나 소프트웨어 구독은 서비스 분야를 능가하는 성장률을 보여줍니다. AI 강화 사용자 프로비저닝, 지속적인 인증, 권한 세션 분석이 17.25%의 연평균 복합 성장률(CAGR) 전망을 보이면서 독립형 액세스 관리 도구에서 예산을 흡수하고 있습니다. 각 공급업체는 모든 워크플로에 자동화를 통합하고 수동 조작 포인트를 줄임으로써 기존의 복잡성이 도입 장벽이었던 중견 시장에 대한 기회를 개척하고 있습니다. 이러한 동향을 통해 고객이 장기적인 비용 효율성을 추구하는 가운데 소프트웨어가 점유율 확대를 도모하는 기반이 갖추어져 있습니다.

2025년의 ID 거버넌스 및 관리 시장 규모의 60.74%를 클라우드 도입이 차지하였고 부문 내에서 가장 높은 16.02%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측되고 있습니다. 기업은 신속한 온보딩, 탄력적인 스케일링, 기능 릴리스에 대한 즉각적인 액세스를 중시하고 있습니다. 멀티클라우드 환경에서는 IaaS, SaaS 및 플랫폼 서비스를 가로지르는 거버넌스가 필수적이며 중앙 집중식 관리 아키텍처가 선호하는 옵션이 되었습니다.

데이터 주권에 관한 법령이나 에어 갭 환경에 의해 로컬 관리가 요구되는 상황에서는 온프레미스 도입이 계속됩니다. 주권 클라우드 구축은 구독의 경제성을 훼손하지 않고 거주 규정을 충족하는 전용 지역 인스턴스를 제공함으로써 이러한 간격을 줄이고 있습니다. 정책 엔진을 클라우드에서 실행하면서 민감한 ID 저장소를 현장에 유지하는 하이브리드 모델은 대규모 레거시 환경을 보유한 조직에 마이그레이션 경로를 제공합니다.

지역별 분석

북미는 2025년 수익의 32.54%를 차지하였고 성숙한 제로 트러스트 구상과 AI 구동형 분석을 축으로 지속적으로 혁신을 계속하는 플랫폼 벤더의 집중이 기반이 되고 있습니다. 금융서비스와 의료 분야의 업계 고유 규제가 기반 수요를 끌어올리는 한편, 정부기관이 대규모 참조 도입을 추진함으로써 민간 기업의 도입 리스크 경감에 공헌하고 있습니다.

아시아태평양은 16.75%의 연평균 복합 성장률(CAGR)로 확대될 것으로 예상되며 중국, 인도, 주요 ASEAN 국가들의 적극적인 디지털 경제 정책이 견인 역할을 합니다. 통신 사업자 통합, 소버린 클라우드 투자, 모바일 퍼스트 소비자 서비스의 보급은 기업에 신원 관리의 신속한 현대화를 촉구하고 있습니다. 국내 소프트웨어 벤더는 현지화의 강점을 살려, 국가기술 개발지침의 대상이 되는 고객에 대한 침투를 도모하여 경쟁 격화를 가속화하고 있습니다.

유럽은 여전히 중요한 시장이며, GDPR(EU 개인정보보호규정), 부문별 지침, ESG(환경, 사회 및 지배구조) 관련 조달 규정이 조직에 감사 대응 거버넌스의 도입을 촉구하고 있습니다. 북유럽 국가에서는 벤더 평가의 엄격화가 더욱 진행되어 윤리적인 신원 확인이 조달 체크리스트에 포함되어 있습니다. 한편 중동에서는 거주지 준거 클라우드 인스턴스를 우선하여 대규모 전자정부 프로젝트와 데이터 주권의 요구를 조화시키고 있습니다. 남미와 아프리카에서는 은행, 커뮤니케이션, 공공 부문의 파일럿 사업을 통해 시장에 진출하여 신속한 투자 회수 효과를 보여주면서 보다 광범위한 도입을 촉진하고 있습니다.

기타 혜택

- 시장 예측(ME) 엑셀 시트

- 3개월 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 촉진요인

- 지속적인 액세스 인증을 위한 AI 구동형 IGA 도입 확대

- 유럽의 고도로 규제된 업계에서 PAM과 IGA 스위트의 융합

- 제로 트러스트 및 패스워드리스화의 대처가 북미에서의 롤 마이닝 툴 보급을 가속화

- 아시아태평양에서의 통신 사업자 간 M&A 활동이 통신 사업자용 IGA 도입을 촉진

- 주권 클라우드 의무화가 중동에서 국내 IGA 플랫폼을 촉진

- ESG 연동형 벤더 평가 요건이 북유럽 국가에서 감사 수준의 신원 확인을 추진

- 억제요인

- 아이덴티티 엔지니어링 분야에서의 스킬 부족이 복잡한 도입을 제한

- 기존 IT 환경에서 API의 무질서한 확대로 통합 비용 상승

- 단편화된 데이터 거주지법이 다국적 기업의 세계 전개를 지연시킴

- 레거시 ERP 환경에서의 역할 기반의 액세스 정리에 의한 투자 회수의 지연

- 가치 및 공급망 분석

- 규제 전망

- 기술 전망

- Porter's Five Forces

- 공급자의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 투자분석

제5장 시장 규모 및 성장 예측

- 컴포넌트별

- 솔루션

- 액세스 인증 및 리뷰

- 사용자 프로비저닝 및 디프로비저닝

- 권한적 거버넌스

- 비밀번호 관리

- 서비스

- 전문 서비스

- 매니지드 서비스

- 솔루션

- 전개 모드별

- 온프레미스

- 클라우드

- 기업 규모별

- 대기업

- 중소기업

- 최종 사용자 업계별

- 은행, 금융서비스 및 보험

- IT 및 통신

- 의료 및 생명과학

- 에너지 및 유틸리티

- 정부 및 공공 방위

- 제조업

- 소매업 및 전자상거래

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 북유럽 국가(스웨덴, 노르웨이, 덴마크, 핀란드)

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ASEAN(싱가포르, 인도네시아, 말레이시아, 태국, 베트남, 필리핀)

- 기타 아시아태평양

- 중동

- GCC(사우디아라비아, 아랍에미리트(UAE), 카타르, 오만, 쿠웨이트, 바레인)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- SailPoint Technologies Holdings Inc.

- IBM Corporation

- Microsoft Corporation

- Oracle Corporation

- Broadcom Inc.(CA Technologies)

- SAP SE

- Okta Inc.

- One Identity LLC

- Saviynt Inc.

- CyberArk Software Ltd.

- Ping Identity Holding Corp.

- ForgeRock(Thales Group)

- Hitachi ID Systems

- Evidian(Atos)

- Quest Software Inc.

- Micro Focus(OpenText)

- RSA Security LLC

- Wipro Limited

- Cognizant Technology Solutions Corp.

- Omada Identity

- Zilla Security

- SecZetta

제7장 시장 기회 및 미래 전망

CSM 26.01.28The identity governance and administration market size in 2026 is estimated at USD 9.59 billion, growing from 2025 value of USD 8.36 billion with 2031 projections showing USD 19.12 billion, growing at 14.82% CAGR over 2026-2031.

Heightened reliance on hybrid IT estates combined with an 82% surge in impersonation-led fraud is steering security spending toward identity-centric controls.Cloud delivery models now anchor most new deployments, reflecting the need for elastic scaling and quicker time-to-value. Regional spending patterns are fragmenting: North America sets the adoption pace through mature zero-trust programs, while Asia propels overall growth as local enterprises accelerate digitization and leapfrog to cloud-native tools. Services retain the largest revenue pool, mirroring the skills gap that hampers in-house roll-outs and drives demand for managed identity expertise. Meanwhile, vendors are embedding machine learning into certification workflows, automating entitlement reviews and raising detection accuracy, a shift that is rapidly altering competitive positioning and widening addressable opportunities in adjacent privileged access and non-human identity segments.

Global Identity Governance And Administration Market Trends and Insights

Rising Adoption of AI-Driven IGA for Continuous Access Certification

AI-enabled tools now inspect user and non-human entitlements in near real time, minimizing certification fatigue by spotlighting high-risk anomalies. Enterprises deploying these capabilities report sharper risk detection and administrative cost relief, a combination that scales governance to sprawling multicloud estates. Generative AI is also rewriting complex entitlement descriptions into natural language, widening participation among business managers and reducing help-desk cycles. Early roll-outs in financial services and tech verticals suggest the model is suited for globally dispersed workforces where manual reviews have become impractical. Growth momentum is therefore expected to intensify as more organizations build trust in explainable AI review engines.

Convergence of PAM & IGA Suites Among Highly-Regulated Sectors in Europe

Financial institutions and critical infrastructure operators are rationalizing tool sprawl by fusing privileged access controls with broader lifecycle governance. Unified suites reduce overlap between administrator and standard user entitlements, closing gaps that attackers target. Recent acquisitions by leading PAM providers underscore a race to integrate governance modules and to deliver compliance-ready workflows aligned with Europe's Digital Operational Resilience Act. Early adopters report fewer audit findings and faster evidence gathering, reinforcing the business case for integrated architectures across global subsidiaries.

Skill Shortage in Identity Engineering Limiting Complex Deployments

Demand for specialists versed in directory architecture, entitlement modelling, and regulatory mapping continues to outstrip supply. A majority of enterprises cite talent scarcity as the principal hurdle to large-scale implementations. The gap drives wage inflation and elongates project timelines, especially in emerging markets where cybersecurity skill pools remain shallow. Vendors are responding with prescriptive templates and managed offerings, yet many organizations still defer advanced features such as policy automation because internal expertise is absent.

Other drivers and restraints analyzed in the detailed report include:

- Zero-Trust & Passwordless Initiatives Accelerating Role Mining Tools in North America

- M&A Activity Among Telcos Driving Telco-Grade IGA Roll-Outs in APAC

- API-Sprawl Elevating Integration Cost for Brownfield IT Environments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services generated 56.42% of 2025 revenue in the identity governance and administration market, reflecting the consulting and integration effort needed to harmonize diverse application estates. Implementers remain indispensable for mapping entitlements across on-premises, SaaS, and operational technology layers, particularly in regulated sectors that demand audit-grade evidence. The arrival of SaaS-delivered governance platforms is shifting some expenditure toward outcome-based managed services, with providers bundling software subscriptions and day-to-day administration into fixed-fee models.

Software subscriptions are, however, outpacing services in growth terms. AI-enhanced user provisioning, continuous certification, and privileged session analytics underpin a 17.25% CAGR outlook, drawing budget from stand-alone access management tools. Vendors are weaving automation into every workflow, shrinking manual touchpoints, and opening mid-market opportunities where previous complexity deterred adoption. This dynamic positions software to capture incremental share as customers seek long-term cost efficiencies.

Cloud deployments accounted for 60.74% of the identity governance and administration market size in 2025 and are projected to register the segment's steepest 16.02% CAGR. Enterprises value rapid onboarding, elastic scaling, and instant access to feature releases. Multicloud realities now require governance that spans infrastructure-as-a-service, SaaS, and platform services, making centrally-hosted architectures the preferred option.

On-premises installations persist where data-sovereignty statutes or air-gapped environments dictate local control. Sovereign-cloud constructs are narrowing this divide by offering dedicated regional instances that satisfy residency rules without sacrificing subscription economics. Hybrid models, in which policy engines run in the cloud while sensitive identity stores remain on-site, provide transitional paths for organizations with large legacy footprints.

The Identity Governance and Administration Market Report is Segmented by Component (Solutions, Services), Deployment Mode (On Premise, Cloud), Enterprise Size (Large Enterprises, Small and Medium Enterprises), End User Vertical (Banking, Financial Services, and Insurance, IT and Telecom, Energy and Utilities, Government and Public Defense, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 32.54% of 2025 revenue, underpinned by mature zero-trust initiatives and a concentration of platform vendors that continually innovate around AI-driven analytics. Sector-specific mandates in financial services and healthcare boost baseline demand, while government agencies sponsor large-scale reference deployments that de-risk adoption for private firms.

Asia-Pacific is projected to expand at a 16.75% CAGR, buoyed by aggressive digital-economy policies in China, India, and key ASEAN states. Telco consolidation, sovereign-cloud investments, and widespread mobile-first consumer services force enterprises to modernize identity controls rapidly. Domestic software suppliers leverage localisation advantages to penetrate accounts subject to national technology-development directives, amplifying competitive intensity.

Europe remains a pivotal battleground where GDPR, sectoral directives, and ESG-linked procurement rules compel organisations to adopt audit-ready governance. The Nordics push vendor assessment rigor even further, embedding ethical identity verification into sourcing checklists. Meanwhile, the Middle East prioritises residency-compliant cloud instances to harmonise expansive e-government projects with data-sovereignty imperatives. South America and Africa enter the market through banking, telecom, and public-sector pilots that demonstrate rapid ROI and spur broader adoption.

- SailPoint Technologies Holdings Inc.

- IBM Corporation

- Microsoft Corporation

- Oracle Corporation

- Broadcom Inc. (CA Technologies)

- SAP SE

- Okta Inc.

- One Identity LLC

- Saviynt Inc.

- CyberArk Software Ltd.

- Ping Identity Holding Corp.

- ForgeRock (Thales Group)

- Hitachi ID Systems

- Evidian (Atos)

- Quest Software Inc.

- Micro Focus (OpenText)

- RSA Security LLC

- Wipro Limited

- Cognizant Technology Solutions Corp.

- Omada Identity

- Zilla Security

- SecZetta

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Adoption of AI-driven IGA for Continuous Access Certification

- 4.2.2 Convergence of PAM and IGA Suites Among Highly-Regulated Sectors in Europe

- 4.2.3 Zero-Trust and Passwordless Initiatives Accelerating Role Mining Tools in North America

- 4.2.4 MandA Activity Among Telcos Driving Telco-grade IGA Roll-outs in APAC

- 4.2.5 Sovereign-Cloud Mandates Fueling Domestic IGA Platforms in Middle East

- 4.2.6 ESG-Linked Vendor Assessment Requirements Pushing Audit-grade Identity Proof in Nordics

- 4.3 Market Restraints

- 4.3.1 Skill Shortage in Identity Engineering Limiting Complex Deployments

- 4.3.2 API-Sprawl Elevating Integration Cost for Brownfield IT Environments

- 4.3.3 Fragmented Data-Residency Laws Slowing Global Rollouts for Multinationals

- 4.3.4 Delayed ROI from Role-Based Access Clean-ups in Legacy ERP Estates

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.1.1 Access Certification and Review

- 5.1.1.2 User Provisioning / De-provisioning

- 5.1.1.3 Privileged Governance

- 5.1.1.4 Password Management

- 5.1.2 Services

- 5.1.2.1 Professional Services

- 5.1.2.2 Managed Services

- 5.1.1 Solutions

- 5.2 By Deployment Mode

- 5.2.1 On-premise

- 5.2.2 Cloud

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By End-user Vertical

- 5.4.1 Banking, Financial Services and Insurance

- 5.4.2 IT and Telecom

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 Energy and Utilities

- 5.4.5 Government and Public Defense

- 5.4.6 Manufacturing

- 5.4.7 Retail and e-Commerce

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Nordics (Sweden, Norway, Denmark, Finland)

- 5.5.3.6 Rest of Europe

- 5.5.4 APAC

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 ASEAN (Singapore, Indonesia, Malaysia, Thailand, Vietnam, Philippines)

- 5.5.4.6 Rest of APAC

- 5.5.5 Middle East

- 5.5.5.1 GCC (Saudi Arabia, UAE, Qatar, Oman, Kuwait, Bahrain)

- 5.5.5.2 Turkey

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SailPoint Technologies Holdings Inc.

- 6.4.2 IBM Corporation

- 6.4.3 Microsoft Corporation

- 6.4.4 Oracle Corporation

- 6.4.5 Broadcom Inc. (CA Technologies)

- 6.4.6 SAP SE

- 6.4.7 Okta Inc.

- 6.4.8 One Identity LLC

- 6.4.9 Saviynt Inc.

- 6.4.10 CyberArk Software Ltd.

- 6.4.11 Ping Identity Holding Corp.

- 6.4.12 ForgeRock (Thales Group)

- 6.4.13 Hitachi ID Systems

- 6.4.14 Evidian (Atos)

- 6.4.15 Quest Software Inc.

- 6.4.16 Micro Focus (OpenText)

- 6.4.17 RSA Security LLC

- 6.4.18 Wipro Limited

- 6.4.19 Cognizant Technology Solutions Corp.

- 6.4.20 Omada Identity

- 6.4.21 Zilla Security

- 6.4.22 SecZetta

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment