|

시장보고서

상품코드

1906183

기복기 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Global Insufflation Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

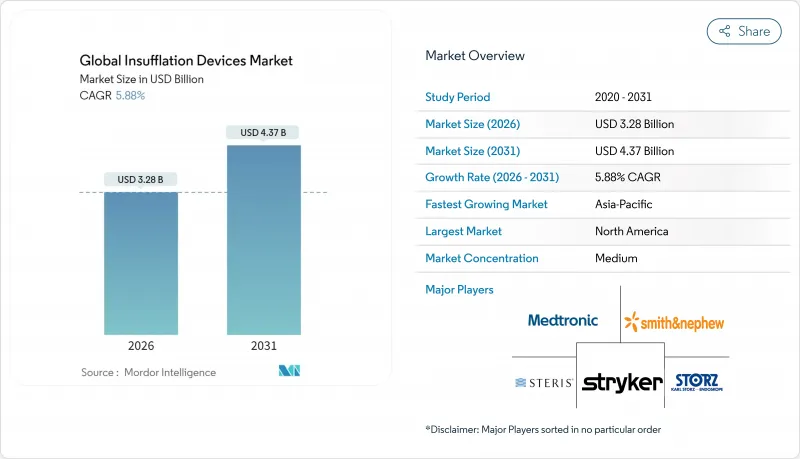

2026년 기복기 시장의 규모는 32억 8,000만 달러로 추정되며, 2025년 31억 달러에서 성장할 것으로 예상됩니다.

2031년까지 43억 7,000만 달러에 달하고, 2026년부터 2031년에 걸쳐 CAGR 5.88%로 확대될 전망입니다.

저침습 수술의 건수 증가, 환자 회복의 신속화에 관한 확고한 근거, 총 치료비 감소를 요구하는 지불자측의 압력에 의해 수요가 가속화되고 있습니다. 로봇 플랫폼과의 급속한 통합, FDA의 AI 대응 수술 소프트웨어에 대한 지침 발표, 복잡한 사례의 외래 환경으로의 전환이 경쟁 차별화를 촉진하고 있습니다. 북미의 의료 제공업체는 성과 연동형 계약에 따라 기존 시스템을 계속 업데이트하는 반면, 아시아의 신흥 병원에서는 저렴한 시스템을 일단 도입하는 것을 우선시하고 있습니다. 이러한 요인들이 결합되어 성능 기준이 더 높아지고 조기 도입자와 후발자 간의 기술 도입 격차가 확대되고 있습니다.

세계의 기복기 시장의 동향 및 인사이트

저침습 수술의 보급 확대

담낭 적출술, 대장 절제술, 흉부 개입 치료에서 저침습 기술이 주류가 되면서 의료용 기복기 시장은 신뢰성이 높은 고유량 기술로 향하고 있습니다. 복강경하 담낭 적출술은 이미 96%를 돌파하였으며 비만 수술과 부인과 및 종양학 분야에서도 개복 수술을 대체하고 있습니다. 메디케어의 데이터에 따르면, 2023년에는 340만명의 환자가 ASC(외래수술센터)에서 치료를 받았고, 가스 주입에 의해 당일 퇴원을 가능하게 하는 외래 수술로의 이행이 현저히 나타나고 있습니다. ERAS(수술 후 회복 촉진 프로그램)에서는 체온 유지 및 위장관 기능 회복 촉진을 위해 가온 가습 가스가 필수적입니다. 이러한 변화가 결합되어 의료용 기복기 시장에서 기복기의 수요가 상승세를 유지하고 있습니다.

유량제어 및 가온가습식 기복기의 기술적 진보

가온가습식 기복기는 체온을 유지하고, 수술 후의 경련을 줄이며, 저체온증을 예방하므로 의료용 기복기 시장에서 프리미엄 제품의 도입을 촉진하고 있습니다. AirSeal과 같은 시스템은 저압에서 기복을 유지하고 피하기종을 억제하는 동시에 수술 연기를 여과합니다. 스트라이커사의 PneumoClear는 분당 50리터의 유량과 0.051 미크론까지의 미립자 제거 기능을 결합하여 로봇 지원과 표준 복강경 수술의 시인성을 향상시킵니다. 내장 센서가 실시간으로 유량을 자동 조절하여 수동적인 통기에서 스마트 통기로의 전환을 나타내고 있습니다. 이러한 혁신은 임상 적응 범위를 확대하고 의료용 기복기 시장에서 공급업체의 경쟁 우위를 강화하고 있습니다.

외래수술센터(ASC) 확대

2023년 미국의 약 6,300곳의 ASC(외래수술센터)에서는 환자 1인당 수술건수가 5.7% 증가하여 메디케어 지출 68억 달러를 계상했습니다. 병원 외래 부문에 비해 뛰어난 ASC의 비용 이점은 지불자와 환자 모두를 유치하여 신속하게 설치할 수 있는 휴대용 기복기에 대한 수요를 높이고 있습니다. 현재 26개 주에서 시행되고 있는 연기 배출 규제로 통합 필터가 의무화되어 장비의 업데이트 사이클이 가속화되고 있습니다(ascfocus.org). 법 규제의 압력과 수술건수 증가가 더하여 ASC는 의료용 기복기 시장에서 전략적인 수요 거점으로서의 지위를 확립하고 있습니다.

부문 분석

기복기는 수술실의 기간설비로, 병원이 수술실 정보시스템과 통합 가능한 네트워크 대응 콘솔을 표준화하는 가운데 2025년에는 72.12%의 수익을 차지하였습니다. 방대한 설치 기반은 장기 서비스 계약과 정기적인 소프트웨어 업그레이드를 지원하여 지속적인 수익원을 확대하고 있습니다. 한편, 일회용 튜브, 필터, 밸브 등의 소모품은 일회용을 권장하는 감염 관리 지침에 의해 6.98%의 연평균 복합 성장률(CAGR)을 기록하고 있습니다. 소모품 부문의 기복기 시장 내 규모는 수술건수와 연동하여 확대가 예상되고, 자본재와 소모품을 세트로 판매하는 벤더에게 수익성이 높은 지속적 수입원이 됩니다.

북미 및 유럽의 병원에서는 가치 기반 패키지 계약이 증가하는 경향이 있으며, 고가의 콘솔과 소모품의 안정적인 공급을 보장하는 거래가 이루어지고 있습니다. 한편 제조업체는 튜브 세트에 압력 센서와 RFID 칩을 통합하여 자동 교정 및 재고 추적을 가능하게 함으로써 공급망 업무의 효율화를 실현하고 있습니다. 이러한 스마트한 일회용 제품은 프리미엄 가격 설정을 뒷받침하여 신흥 경제권의 비용을 중시하는 구매자에 의한 이익률의 축소를 완화해 기복기 시장을 견조한 성장 궤도에 위치시키고 있습니다.

지역별 분석

북미는 2025년 세계 수익의 38.20%를 차지하였고 견조한 설비투자 예산, 로봇 수술의 급속한 보급, 단기 입원을 장려하는 지원적인 환급 프레임워크에 기반을 두고 있습니다. 미국 규제 당국은 2025년 AI 대응 수술용 소프트웨어에 대한 초안 가이드라인을 발표하여 차세대 기복기에 분석 기능과 예측 알고리즘을 통합할 것을 제조업체에 요구하고 있습니다. 캐나다의 의료 시스템은 노후화된 복강경 수술 장치의 업그레이드에 필요한 자금을 확보하고 있으며, 멕시코의 민간 병원 그룹은 현금 흐름 관리를 위해 장기 서비스 계약을 통해 공급자와 공동 투자를 실시했습니다.

유럽에서는 각국의 보건 서비스가 수술실 효율화 프로그램을 추진하면서 안정적인 성장을 유지하고 있습니다. 독일의 97%에 달하는 복강경 충수 절제술 이행률은 MIS 문화의 정착을 나타내며 유럽 내시경 외과학회의 COVID 후기 가이드라인은 프로토콜 조화를 가속화하고 있습니다. 남유럽 시장에서는 EU 부흥 기금을 활용하여 수술실 환기 및 연기 배출 시스템의 업그레이드가 진행되고 있으며, 부족한 펌프를 턴키 패키지에 통합하는 사례가 나타나고 있습니다.

아시아태평양은 8.92%의 연평균 복합 성장률(CAGR)로 기세를 이끌고 있습니다. 중국의 신속한 의료기기 승인과 수량 기준 조달의 확대는 다국적 기업과 현지 혁신 기업 모두에 문을 열고 있습니다. 인도에서는 10만명당 13.5명에 불과한 외과 전문의 부족 현상이 확장 가능한 MIS 인프라를 필요로 하는 치료 거점 설립을 위한 정부-민간 연계를 촉진하고 있습니다. 이미 로봇 분야의 대국인 일본과 한국은 8K 관절경과 통합된 AI 강화 기복기를 시험적으로 운용하고 있습니다.

남미, 중동 및 아프리카에서는 선택적인 상승 여지가 있습니다. 브라질 레퍼런스 센터는 최고급 콘솔을 구입하고 있지만 교육 부족과 통화 변동으로 인해 광범위한 도입이 어렵습니다. 걸프 협력 회의(GCC) 회원국은 그린필드 병원 프로젝트에 통기 능력을 통합하고 석유 달러 예산을 활용하여 완벽한 로봇 수술 시스템을 도입하고 있습니다. 사하라 이남 아프리카에서는 CO2 물류 문제를 극복하기 위해 가스가 없는 기술을 채택하는 경향이 있으며, 질소 혁신자에게 저렴한 비용의 진입 경로를 제공하는 계기가 되었습니다.

기타 혜택

- 시장 예측(ME) 엑셀 시트

- 3개월 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 촉진요인

- 저침습 수술의 보급률 상승

- 유량제어 가온가습식 기복기의 기술적 진보

- 비만 수술 및 부인과 수술에서의 도입 확대

- 외래수술센터(ASC)의 확대

- 차세대 로봇 플랫폼과의 통합

- 교차 오염 억제를 위한 일회용 통기 튜브로의 이행

- 억제요인

- 수술 후 이산화탄소 관련 합병증(예 : 고탄산가스혈증)

- 첨단 장비의 높은 자본 비용

- 신흥 시장에서의 숙련된 복강경 외과의 부족

- 의료용 이산화탄소 공급을 제약하는 환경 규제

- 가치 및 공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급자의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 제품 유형별

- 주입 시스템

- 일회용 튜브 및 부속품

- 용도별

- 복강경 수술

- 비만 수술

- 부인과 수술

- 심장외과 수술

- 기타 외과 수술

- 최종 사용자별

- 병원

- 외래수술센터(ASC)

- 전문 클리닉 및 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Karl Storz SE & Co. KG

- Stryker Corporation

- Richard Wolf GmbH

- Johnson & Johnson(Ethicon)

- Olympus Corporation

- Medtronic plc

- CONMED Corporation

- Smith & Nephew plc

- B. Braun Melsungen AG

- Teleflex Incorporated

- Applied Medical Resources

- WOM World of Medicine GmbH

- Bracco Diagnostics Inc.

- Fujifilm Holdings Corp.

- Hoya Corp.(Pentax Medical)

- Steris plc

- Alesi Surgical Ltd.(Insuflow)

제7장 시장 기회 및 미래 전망

CSM 26.01.28Insufflation devices market size in 2026 is estimated at USD 3.28 billion, growing from 2025 value of USD 3.10 billion with 2031 projections showing USD 4.37 billion, growing at 5.88% CAGR over 2026-2031.

Rising volumes of minimally invasive procedures, stronger evidence of quicker patient recovery, and payer pressure for total-episode cost reductions are accelerating demand. Rapid integration of insufflation systems with robotic platforms, the rollout of FDA guidance for AI-enabled surgical software, and the shift of complex cases into ambulatory settings are sharpening competitive differentiation. North American providers continue to refresh installed bases for performance-linked contracts, whereas emerging Asian hospitals prioritize first-time purchases of affordable systems. Together, these forces are setting a higher performance bar and widening the technology adoption gap between early and late movers.

Global Insufflation Devices Market Trends and Insights

Rising Prevalence of Minimally-Invasive Surgeries

Minimally invasive techniques now dominate gallbladder removal, colorectal resection and thoracic interventions, pushing the medical insufflation systems market toward reliable, high-flow technology. Laparoscopic approaches already exceed 96% of cholecystectomies and increasingly replace open procedures in bariatric and gynecologic oncology practices. Medicare data show 3.4 million ASC beneficiaries in 2023, underscoring outpatient migration where insufflation enables same-day discharge. Enhanced Recovery After Surgery (ERAS) pathways rely on heated, humidified gas to preserve core temperature and accelerate bowel function. Collectively, these shifts keep demand for insufflators on an upward trajectory within the medical insufflation systems market.

Technological Advances in Flow-Controlled & Heated-Humidified Insufflators

Heated-humidified insufflators maintain core temperature, cut postoperative shivering and prevent hypothermia, driving premium adoption in the medical insufflation systems market. Systems such as AirSeal sustain pneumoperitoneum at low pressure, curtailing subcutaneous emphysema while filtering surgical smoke. Stryker's PneumoClear couples 50 L/min flow with particulate removal down to 0.051 microns, improving visibility in robotic and standard laparoscopy. Embedded sensors automatically modulate flow in real time, marking a shift from passive to smart insufflation. These innovations widen clinical indications and reinforce the competitive edge of vendors in the medical insufflation systems market.

Expansion of Ambulatory Surgical Centers

Roughly 6,300 U.S. ASCs performed 5.7% more procedures per beneficiary in 2023, channeling USD 6.8 billion in Medicare spending. ASC cost advantages over hospital outpatient departments attract payers and patients, heightening the call for portable, rapid-setup insufflators. Smoke-evacuation laws now enforced in 26 states mandate integrated filtration, accelerating equipment refresh cycles ascfocus.org. The convergence of legislative pressure and volume growth positions ASCs as a strategic demand hub for the medical insufflation systems market.

Other drivers and restraints analyzed in the detailed report include:

- Growing Adoption in Bariatric & Gynecologic Procedures

- Post-operative CO2-Related Complications

- High Capital Cost of Advanced Units

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Insufflation systems anchor surgical suites, delivering 72.12% revenue in 2025 as hospitals standardize on network-ready consoles that integrate with OR information systems. The sizeable installed base underpins long-term service contracts and periodic software upgrades that lift recurring revenue streams. In contrast, accessories such as single-use tubing, filters, and valves are registering a 6.98% CAGR, propelled by infection-control guidelines that favor disposables. The insufflation devices market size for accessories is projected to rise in lockstep with procedure volumes, creating a lucrative annuity stream for vendors bundling consumables with capital units.

Hospitals in North America and Europe increasingly negotiate value-based packages, exchanging higher console prices for guaranteed consumable supply deals. Meanwhile, manufacturers embed pressure sensors and RFID chips into tubing sets, enabling auto-calibration and stock tracking that streamline supply-chain workflows. These smart disposables support premium pricing, cushioning margin pressure from cost-sensitive buyers in emerging economies and keeping the insufflation devices market on a robust growth trajectory.

The Insufflation Devices Market Report is Segmented by Product Type (Insufflation Systems, Disposable Tubing & Accessories), Application (Laparoscopic Surgery, Bariatric Surgery, Gynecological Surgery, Cardiac Surgery, Other Surgeries), End User (Hospitals, Ambulatory Surgical Centers, Specialty Clinics & Others), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 38.20% of global revenue in 2025, anchored by robust capital budgets, rapid robotic uptake, and a supportive reimbursement framework that rewards shorter stays. U.S. regulators issued 2025 draft guidance for AI-enabled surgical software, encouraging manufacturers to embed analytics and predictive algorithms in next-gen insufflators. Canadian health systems are earmarking funds to refresh aging laparoscopic stacks, while Mexico's private hospital groups co-invest with suppliers via long-term service agreements to manage cash flow.

Europe maintains stable growth as national health services pursue operating-room efficiency programs. Germany's 97% laparoscopic appendectomy standard demonstrates entrenched MIS culture, while the European Association for Endoscopic Surgery's post-COVID guidelines accelerate protocol harmonization. Southern European markets use EU recovery funds to upgrade OR ventilation and smoke evacuation systems, often bundling insufficient pumps in turnkey packages.

Asia-Pacific leads on momentum with a 8.92% CAGR. China's expedited device approvals and expanded volume-based procurement have opened doors for both multinationals and local innovators. India's shortage of 13.5 surgical specialists per 100,000 citizens fuels public-private partnerships to establish treatment hubs that require scalable MIS infrastructure. Japan and South Korea, already robotic heavyweights, are piloting AI-enhanced insufflators that integrate with 8K arthroscopes.

South America, the Middle East, and Africa offer selective upside. Brazilian reference centers buy top-tier consoles, whereas broader adoption is hamstrung by training deficits and currency volatility. Gulf Cooperation Council nations incorporate insufflation capacity in greenfield hospital projects, leveraging petrodollar budgets to acquire full robotic suites. Sub-Saharan initiatives lean toward gasless technology to overcome CO2 logistic hurdles, providing low-cost entry lanes for frugal innovators.

- Karl Storz

- Stryker

- Richard Wolf

- Johnson & Johnson

- Olympus

- Medtronic

- Conmed

- Smiths Group

- B. Braun

- Teleflex

- Applied Medical Resources

- W.O.M. World of Medicine GmbH

- Bracco

- Fujifilm Holdings Corp.

- Hoya Corp. (Pentax Medical)

- Steris plc

- Alesi Surgical Ltd. (Insuflow)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising prevalence of minimally-invasive surgeries

- 4.2.2 Technological advances in flow-controlled & heated-humidified insufflators

- 4.2.3 Growing adoption in bariatric & gynecologic procedures

- 4.2.4 Expansion of ambulatory surgical centers

- 4.2.5 Integration with next-generation robotic platforms

- 4.2.6 Shift toward single-use insufflation tubing to curb cross-contamination

- 4.3 Market Restraints

- 4.3.1 Post-operative CO2-related complications (e.g., hypercapnia)

- 4.3.2 High capital cost of advanced units

- 4.3.3 Shortage of skilled laparoscopic surgeons in emerging markets

- 4.3.4 Environmental regulations constraining medical-grade CO2 supply

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Insufflation Systems

- 5.1.2 Disposable Tubing & Accessories

- 5.2 By Application

- 5.2.1 Laparoscopic Surgery

- 5.2.2 Bariatric Surgery

- 5.2.3 Gynecological Surgery

- 5.2.4 Cardiac Surgery

- 5.2.5 Other Surgeries

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgical Centers

- 5.3.3 Specialty Clinics & Others

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 GCC

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Karl Storz SE & Co. KG

- 6.3.2 Stryker Corporation

- 6.3.3 Richard Wolf GmbH

- 6.3.4 Johnson & Johnson (Ethicon)

- 6.3.5 Olympus Corporation

- 6.3.6 Medtronic plc

- 6.3.7 CONMED Corporation

- 6.3.8 Smith & Nephew plc

- 6.3.9 B. Braun Melsungen AG

- 6.3.10 Teleflex Incorporated

- 6.3.11 Applied Medical Resources

- 6.3.12 W.O.M. World of Medicine GmbH

- 6.3.13 Bracco Diagnostics Inc.

- 6.3.14 Fujifilm Holdings Corp.

- 6.3.15 Hoya Corp. (Pentax Medical)

- 6.3.16 Steris plc

- 6.3.17 Alesi Surgical Ltd. (Insuflow)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment