|

시장보고서

상품코드

1906195

금속 분말 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Metal Powder - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

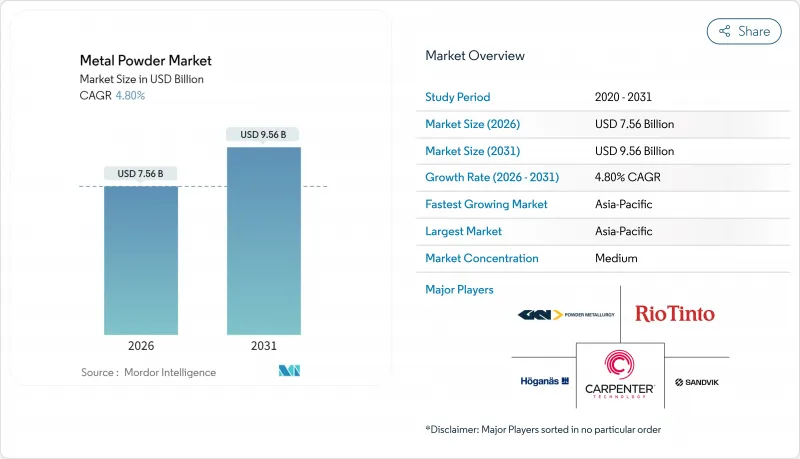

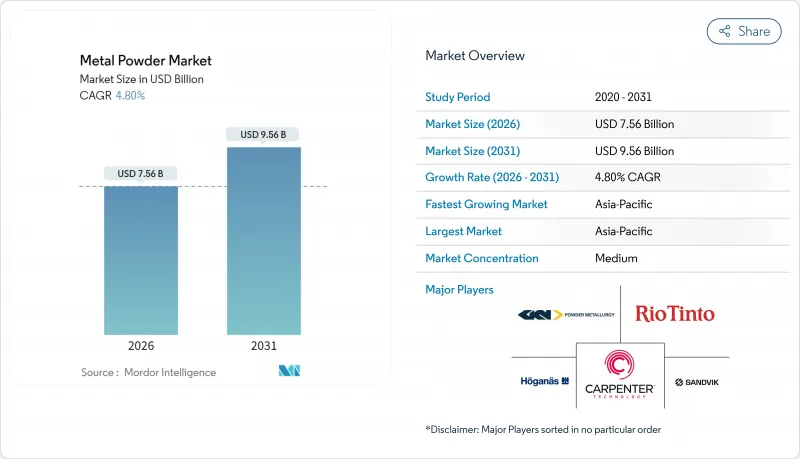

2026년 금속 분말 시장의 규모는 75억 6,000만 달러로 추정되며, 2025년 72억 1,000만 달러에서 성장하여, 2031년에는 95억 6,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지는 CAGR 4.8%로 확대될 전망입니다.

수요는 자동차의 전동화, 항공우주분야의 근대화 및 적층제조기술의 산업화에 뒷받침되고 있으며, 이에 따라 저합금철 등급에서 맞춤형 니켈 및 티탄계 조성물에 이르는 폭넓은 분말에 대한 수요가 창출되고 있습니다. 차량 및 항공기의 경량화 프로그램, 전동 구동계의 보급, 3D 프린팅 구조 부품의 도입 확대가 소비량 증가 추세를 유지하고 있습니다. 한편, 분말 제조업체는 원료 가격의 변동과 환경 규제의 강화에 직면하고 있으며, 이들은 컴플라이언스 비용을 밀어 올리는 한편, 더 깨끗한 분무 기술에 대한 투자를 촉진하고 있습니다. 경쟁 우위는 대량 생산의 프레스 및 소결 계약과 소량 및 고이익률 부가제조 사이에서 유연하게 대응할 수 있는 공급업체로 이행하고 있어 프로세스 다양화의 필요성을 더욱 강화하고 있습니다.

세계의 금속 분말 시장의 동향 및 전망

자동차 및 항공 분야에서 추진되는 경량화

자동차 제조업체는 전기자동차의 항속 거리 연장 및 유로 7 브레이크 배출 가스 규제에 대응하기 위해 차량 무게를 줄이려는 시도를 계속하고 있습니다. 이에 따라 연자성 복합재용으로 설계된 고밀도 철계 및 알루미늄 분말의 도입이 확대되고 있습니다. 아르셀로미탈사가 새롭게 개발한 철 분말은 저배출 브레이크 시스템을 타겟으로 하고 있으며, NASA와 Planse AG의 TiAl 시트 프로그램은 기존의 니켈기 초합금에 비해 25-35%의 중량 저감을 목표로 하는 항공업계의 전환을 나타내고 있습니다. 북미의 출하 상황은 이 동향을 뒷받침하고 있으며, 항공우주용 합금이 터빈 디스크나 구조용 브라켓 용도로 높은 가격을 유지하고 있음에도 불구하고, 철계 분말의 70%가 자동차용 수주에 국한되어 있습니다.

적층 제조 기술의 도입 확대

금속 분말 시장은 첨단 구형성과 유동 안정성을 요구하는 적층 제조 기술의 영향을 받고 있습니다. 나노디멘션사의 데스크톱 메탈사 인수 합의에 의해 분말층 용융법과 바인더 제트 기술에 특화된 2억 4,600만 달러의 수익 기반이 통합되었습니다. 테크나사는 항공우주 프로토타입의 제조시간 단축을 위해 60µm 및 90µm층용으로 조정된 조립 Ti64 분말을 상품화하고 있습니다. 미국 에너지부(DOE)가 지원하는 AMAZEMET rePowder는 불규칙한 재생 금속을 구형 원료로 변환하여 사용 가능한 스크랩 폭을 넓힙니다. Hoganas의 CustomAM 플랫폼은 플라즈마와 질소 원자화를 결합하여 의료용 임플란트 설계자가 맞춤형 분말을 실험실 규모에서 톤 단위로 확장할 수 있습니다. ASTM 및 ASME의 인증 작업 흐름은 안전성이 매우 중요한 원자력 부품용 분말 사양의 성숙을 보여줍니다.

직업 및 환경 위험

OSHA의 가연성 분진 가이드라인은 금속 분말 처리 현장에 대해 광범위한 환기 설비, 작업자 훈련, 문서화를 의무화하고 설비 투자와 운영 비용을 모두 증가시키고 있습니다. NFPA는 가연성 금속의 취급, 마감 및 재활용을 포괄하는 통일 규격 NFPA 660으로 여러 문서를 통합하고 있습니다. EPA의 배출 기준에서는 연마 블라스트 공정에서의 여과 장치 설치와 연삭 시의 분진 저감이 요구되고, 분체 도장 부스에는 순발화 리스크 대책으로 상시 작동식 스프링클러의 설치가 의무화되고 있습니다. 이러한 규제는 엄격한 시행지역에서의 생산능력 확대를 제약하고 폐루프식 저배출 아토마이저로의 이행을 가속화하고 있습니다.

부문 분석

2025년, 철 분말은 자동차용 싱크로나이저, 기어, 구조 부품에서의 확립된 용도에 뒷받침되어 금속 분말 시장 점유율의 43.46%를 차지했습니다. 생산량의 대부분은 여전히 프레스 및 소결 철계 등급이 차지하고 있으며 태평양금속의 월 1만 5,000톤의 스테인리스강 생산 능력이 이를 뒷받침하고 있습니다. 그러나 항공우주, 의료, 방위 프로그램에서 고강도 중량비를 실현하는 티타늄, 니켈, 고융점 합금이 지정되면서 특수 합금은 2031년까지 연평균 CAGR 5.55%로 보다 빠른 성장할 것으로 전망됩니다. 아이페리온X사가 미국 국방부와 체결한 수소 보조 열환원법 도입 계약(4,710만 달러)은 미국이 티타늄 공급망의 자국화를 목표로 하는 자세를 뒷받침합니다. 힌달코사의 100억 달러 규모 알루미늄 생산 확대 계획(오디샤주 제련소 20만톤/년 증설 포함)은 전기자동차 케이스 및 재생에너지용 케이블 수요에 대응하는 생산 능력을 확보합니다.

철강 원료의 경제성과 고부가가치 합금의 가격 형성이 결합되어, 분말 제조업체는 생산 포트폴리오의 밸런스 조정을 요구받고 있습니다. 공급업체는 전합금화 원료에 의한 등급 라인업의 확충을 진행시키고, 프레스 후의 혼합 공정을 줄임으로써 기계적 특성의 일관성을 향상시키고 있습니다. 이로써 다운스트림 사용자는 안전성이 매우 중요한 부품에 필수적인 재현성을 획득하고, 금속 분말 시장은 고이익률 제품으로의 구조적 전환을 계속하고 있습니다.

2025년에도 가스, 물, 플라즈마의 각 공정이 서로 다른 유동성 및 순도 요구를 충족하기 때문에 원자화법은 매출의 69.10%를 차지했습니다. VDM Metals의 신형 진공 불활성 가스 분무기는 초합금 분말층 용융법을 위한 항공우주 등급 제품 확보를 위한 지속적인 설비 투자를 보여줍니다. 습식 야금 처리는 CAGR 5.2%로 소규모이지만, 아연 함유 잔사나 니켈 함유 슬러지를 회수하여 순환형 경제의 목표와 부합하고 있습니다.

신기술은 입자 크기 분포를 줄이고 에너지 사용량을 줄입니다. Metal Powder Works는 봉재를 용해시키지 않고 균일한 칩으로 변환하여 스크랩률과 탄소 실적을 줄입니다. 전극 유도 가스 분무는 종래의 진공 유도 방법보다 미세한 구형 입자를 생성하여 초박형 인쇄층의 새로운 영역을 개척합니다. 한편, 전해 및 환원 공정은 하드 페이싱 및 브레이징 페이스트에 필요한 고순도 분말 틈새 시장에서의 지위를 유지합니다.

지역별 분석

아시아태평양은 2025년 매출액의 44.05%를 차지하였으며, 2031년까지 연평균 복합 성장률(CAGR) 5.3%라는 가장 빠른 성장이 예상됩니다. 중국의 구리 캐소드 생산량은 전년 대비 14.27% 증가하였고 알루미늄 생산량은 2.6% 증가하였으며 이는 풍부한 자원을 뒷받침하고 있습니다. 인도에서는 JSW 스틸의 78억 달러 규모 오디샤 복합시설 외에도 JFE와의 6억 6,000만 달러 규모 전자강판 합작사업으로 생산능력을 확대하여 3만명의 고용을 창출하고 있습니다. 일본과 한국은 전자기기 및 정밀 기계 가공 분야에서 우위성을 유지하는 한편, 지역 정책은 인프라 투자나 재활용 사업(대표적으로 미쓰이 물산의 MTC 사업 출자)을 뒷받침하고 있습니다.

북미에서는 혁신 주도의 수주가 안정적으로 추이하고 있습니다. 아이페리온X사의 티타늄 계약은 전략적 자율성을 확보하고 GE 에어로스페이스의 적층 제조 설비 확충은 제트 엔진 조립 거점 주변에 분말 수요를 집중시킵니다. 캐나다는 니켈 코발트 정광을 공급하고 멕시코는 미국 OEM 프로그램을 위한 기어박스 변속기 분말 부품공급에서 필수적인 지위를 유지하고 있습니다.

유럽에서는 엄격한 배출 규제와 첨단 적층 제조 간의 균형을 맞추고 있습니다. 핀란드의 수소 DRI 플랜트는 강재 분말의 저탄소화 미래를 제시합니다. 독일은 경량 구동계 분말의 연구에 자금을 투입하고 프랑스는 터빈 블레이드 HIP 프로그램을 추진하고 있습니다. 호가나스사는 2018년 이후 스코프 1+2 탄소 배출량을 46% 저감하고 원료의 51%를 2차 원료로 전환했다고 보고하고 있습니다. 중동 및 유럽은 자동차용 2차 소결거점이 되며 영국은 항공우주용 적층 제조기준의 확립을 추진하고 있습니다.

남미, 중동 및 아프리카는 신흥 시장으로 남아 있습니다. 브라질의 철광석 매장량은 소결용 분말을 지원하지만 인프라 부족은 부가가치 제품의 보급을 늦춥니다. 걸프 국가들은 수소 및 태양광 투자를 검토하고 있으며 이는 특수 합금 분말 수요로 이어질 수 있습니다. 아프리카 국가들은 배터리용 금속 채굴을 모색하지만 물류와 정책의 안정성은 투자 일정을 좌우합니다.

기타 혜택

- 시장 예측(ME) 엑셀 시트

- 3개월 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 촉진요인

- 자동차 및 항공 분야에서의 경량화 추진

- 적층 제조 기술의 도입 급증

- 전자기기의 소형화에 대한 수요 증가

- 신재생에너지부품에 대한 수요 증가

- 방위용 극초음속 합금에 대한 수요 증가

- 억제요인

- 직업 및 환경상의 위험성

- 원재료 가격의 변동성

- 중요 부품에서의 분말의 균일성 한계

- 밸류체인 분석

- Porter's Five Forces

- 공급자의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모 및 성장 예측

- 유형

- 철

- 청동

- 알루미늄

- 실리콘

- 니켈

- 기타 유형(티타늄 등)

- 프로세스

- 미립화

- 화합물 저감

- 전기분해

- 기타 공정(습식 야금법 등)

- 제조방법

- 프레스 및 소결(기존 분말 야금)

- 금속 사출 성형

- 적층 제조 및 3D 프린팅

- 기타 방법(열간 등방성 프레스 등)

- 최종 사용자 산업

- 운송

- 전기 및 전자기기

- 의료

- 화학 및 야금

- 방위

- 건설

- 기타 최종 사용자 산업(적층 제조 서비스 사업국 등)

- 지역

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 태국

- 인도네시아

- 베트남

- 말레이시아

- 필리핀

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 튀르키예

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 콜롬비아

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 카타르

- 남아프리카

- 나이지리아

- 이집트

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율(%) 및 순위 분석

- 기업 프로파일

- Advanced Technology & Materials Co., Ltd.

- Alcoa Corporation

- ATI

- Aubert & Duval

- BASF

- CNPC Powder

- CRS Holdings, LLC.

- Erasteel

- GKN Powder Metallurgy

- HC Starck Tungsten GmbH

- Hitachi High-Tech India Private Limited

- Hoganas AB

- JFE Steel Corporation

- Kymera International

- Metalysis Ltd.

- Polema

- Linde Plc

- Outokumpu

- Rio Tinto Metal Powders

- Sandvik AB

- Seiko Epson Corporation

- Tekna

- Valimet

제7장 시장 기회 및 미래 전망

CSM 26.01.21Metal Powder Market size in 2026 is estimated at USD 7.56 billion, growing from 2025 value of USD 7.21 billion with 2031 projections showing USD 9.56 billion, growing at 4.8% CAGR over 2026-2031.

Demand is anchored in automotive electrification, aerospace modernization, and the industrialization of additive manufacturing, which together create a broad pull for powders ranging from low-alloy iron grades to bespoke nickel- and titanium-based compositions. Light-weighting programs in vehicles and aircraft, the proliferation of electric drive trains, and the rising adoption of 3D-printed structural parts keep consumption on an upward track. At the same time, powder makers face raw-material price swings and tightening environmental rules that boost compliance costs yet also spur investments in cleaner atomization technologies. Competitive momentum is tilting toward suppliers that can flex between high-volume press-and-sinter contracts and low-volume, high-margin additive jobs, reinforcing the need for process diversity.

Global Metal Powder Market Trends and Insights

Light-weighting Push in Auto & Aero Sectors

Automotive OEMs continue to cut vehicle mass to extend electric-vehicle range and meet Euro 7 brake-emission norms, prompting broader uptake of high-density ferrous and aluminum powders designed for soft-magnetic composites. ArcelorMittal's newly developed steel powders target low-emission braking systems, while NASA and Plansee AG's TiAl sheet program shows aviation's pivot toward 25-35% weight savings over legacy Ni-base superalloys. North American shipments underscore the trend, with 70% of ferrous powder tonnage tied to automotive orders, even as aerospace alloys command premium pricing in turbine disk and structural bracket applications.

Surge in Additive Manufacturing Adoption

The metal powder market is increasingly shaped by additive manufacturing, which demands highly spherical, flow-stable powders. Nano Dimension's agreement to acquire Desktop Metal consolidates a USD 246 million revenue base devoted to powder-bed fusion and binder-jet technologies. Tekna has commercialized coarse Ti64 fractions tailored for 60 µm and 90 µm layers to cut build times in aerospace prototypes. DOE-backed AMAZEMET rePowder converts irregular reclaimed metal into spherical feedstock, widening the usable scrap pool. Hoganas' CustomAM platform, combining plasma and nitrogen atomization, lets medical-implant designers scale bespoke powders from lab batches to tons. ASTM and ASME qualification workstream signals the maturing of powder specifications for safety-critical nuclear parts.

Occupational & Environmental Hazards

OSHA combustible-dust guidelines mandate extensive ventilation, worker training, and documentation for metal-powder sites, lifting both capital and operating spend. NFPA is transitioning multiple documents into the unified NFPA 660 standard to cover handling, finishing, and recycling of combustible metals. EPA effluent limits now require filtration on abrasive blasting plus dust minimization during grinding, while powder-coating booths must install continuous-duty sprinklers to address flash-fire risk. Collectively, these rules constrain capacity expansions in regions with stringent enforcement and speed the shift toward closed-loop, low-emission atomizers.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Demand for Electronics Miniaturization

- Growing Demand for Renewable-Energy Components

- Raw-Material Price Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Iron powders carried 43.46% of metal powder market share in 2025, aided by entrenched use in automotive synchronizers, gears, and structural parts. Volumetric heft still stems from press-and-sinter ferrous grades, supported by Pacific Metals' 15,000 t/month stainless capacity. Specialty alloys, however, claim faster growth at 5.55% CAGR through 2031 as aerospace, medical, and defense programs specify titanium, nickel, and refractory blends for elevated strength-to-weight ratios. IperionX's USD 47.1 million DoD contract to deploy Hydrogen-Assisted Metallothermic Reduction validates US ambitions for a native titanium supply chain. Hindalco's USD 10 billion aluminum build-out, including a 200,000 TPA Odisha smelter step-up, ensures capacity for electric-vehicle housings and renewable-energy cabling.

The interplay of commodity iron economics and premium alloy pricing encourages powder makers to balance output portfolios. Suppliers widen grade catalogs with pre-alloyed feeds that reduce post-press blending, improving mechanical consistency. In turn, downstream users gain repeatability essential for safety-critical parts, keeping the metal powder market in structural transition toward higher-margin mix.

Atomization retained 69.10% revenue in 2025, as gas, water, and plasma routes satisfy divergent flowability and purity demands. VDM Metals' new vacuum inert gas atomizer demonstrates ongoing capital deployment to secure aerospace-grade outputs for superalloy powder-bed fusion. Hydrometallurgical processing, while only a 5.2% CAGR pocket, recovers zinc-rich residues and nickel-bearing sludges, dovetailing with circular-economy targets.

Emergent techniques tighten particle-size bands and cut energy use. Metal Powder Works converts barstock into uniform chips without melting, trimming scrap rates and carbon footprints. Electrode-induction gas atomization yields finer spheres than legacy vacuum induction, opening new territories for ultra-thin printable layers. Meanwhile, electrolysis and reduction processes keep niche footholds for high-purity powders required in hard-facing and brazing pastes.

The Metal Powder Market Report is Segmented by Type (Iron, Bronze, Aluminum, and More), Process (Atomization, Reduction of Compounds, and More), Manufacturing Method (Press and Sinter, and More), End-User Industry (Transportation, Electrical and Electronics, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific led with 44.05% revenue in 2025 and is projected to post the fastest 5.3% CAGR to 2031. China's copper-cathode output grew 14.27% year on year, and aluminum production rose 2.6%, underscoring resource depth. India widens capacity through JSW Steel's USD 7.8 billion Odisha complex plus a USD 660 million electrical-steel joint venture with JFE that adds 30,000 jobs. Japan and South Korea sustain electronics and precision machining leadership, while regional policy favors infrastructure investment and recycling ventures exemplified by Mitsui's stake in MTC Business.

North America shows steady, innovation-driven orders. IperionX's titanium contract secures strategic autonomy, while GE Aerospace's additive build-out clusters powder demand near jet-engine assembly hubs. Canada supplies nickel and cobalt concentrates, and Mexico remains integral for gearbox and transmission powder parts shipped into US OEM programs.

Europe balances stringent emissions rules with high-value manufacturing. Finland's hydrogen-DRI plant signals a low-carbon future for steel powders. Germany funds lightweight drivetrain powder research; France pushes turbine-blade HIP programs. Hoganas documents a 46% drop in scope 1+2 carbon since 2018, shifting 51% of feedstock to secondary streams. Central and Eastern Europe host automotive tier-2 sintering hubs, while the UK advances aerospace additive standards.

South America, the Middle East, and Africa remain emergent. Brazil's iron-ore reserves support sinter-base powders, yet infrastructure gaps slow additive uptake. Gulf nations eye hydrogen and solar investments that may translate into demand for specialty alloy powders. African states explore battery-metal mining, though logistics and policy stability condition investment timelines.

- Advanced Technology & Materials Co., Ltd.

- Alcoa Corporation

- ATI

- Aubert & Duval

- BASF

- CNPC Powder

- CRS Holdings, LLC.

- Erasteel

- GKN Powder Metallurgy

- H.C. Starck Tungsten GmbH

- Hitachi High-Tech India Private Limited

- Hoganas AB

- JFE Steel Corporation

- Kymera International

- Metalysis Ltd.

- Polema

- Linde Plc

- Outokumpu

- Rio Tinto Metal Powders

- Sandvik AB

- Seiko Epson Corporation

- Tekna

- Valimet

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Light-weighting push in auto & aero sectors

- 4.2.2 Surge in additive manufacturing adoption

- 4.2.3 Increasing demand for electronics miniaturization

- 4.2.4 Growing demand for renewable-energy components

- 4.2.5 Increasing requirement for defense hypersonics alloy demand

- 4.3 Market Restraints

- 4.3.1 Occupational & environmental hazards

- 4.3.2 Raw-material price volatility

- 4.3.3 Powder consistency limits in critical parts

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 Type

- 5.1.1 Iron

- 5.1.2 Bronze

- 5.1.3 Aluminum

- 5.1.4 Silicon

- 5.1.5 Nickel

- 5.1.6 Other Types (Titanium, etc.)

- 5.2 Process

- 5.2.1 Atomization

- 5.2.2 Reduction of Compounds

- 5.2.3 Electrolysis

- 5.2.4 Other Processes (Hydrometallurgical Routes, etc.)

- 5.3 Manufacturing Method

- 5.3.1 Press and Sinter (Conventional PM)

- 5.3.2 Metal Injection Molding

- 5.3.3 Additive Manufacturing / 3D Printing

- 5.3.4 Other Methods (Hot Isostatic Pressing, etc.)

- 5.4 End-User Industry

- 5.4.1 Transportation

- 5.4.2 Electrical and Electronics

- 5.4.3 Medical

- 5.4.4 Chemical and Metallurgical

- 5.4.5 Defense

- 5.4.6 Construction

- 5.4.7 Other End-User Industries (Additive Manufacturing Service Bureaus, etc.)

- 5.5 Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Thailand

- 5.5.1.6 Indonesia

- 5.5.1.7 Vietnam

- 5.5.1.8 Malaysia

- 5.5.1.9 Philippines

- 5.5.1.10 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 NORDIC Countries

- 5.5.3.8 Turkey

- 5.5.3.9 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Qatar

- 5.5.5.4 South Africa

- 5.5.5.5 Nigeria

- 5.5.5.6 Egypt

- 5.5.5.7 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, Recent Developments)

- 6.4.1 Advanced Technology & Materials Co., Ltd.

- 6.4.2 Alcoa Corporation

- 6.4.3 ATI

- 6.4.4 Aubert & Duval

- 6.4.5 BASF

- 6.4.6 CNPC Powder

- 6.4.7 CRS Holdings, LLC.

- 6.4.8 Erasteel

- 6.4.9 GKN Powder Metallurgy

- 6.4.10 H.C. Starck Tungsten GmbH

- 6.4.11 Hitachi High-Tech India Private Limited

- 6.4.12 Hoganas AB

- 6.4.13 JFE Steel Corporation

- 6.4.14 Kymera International

- 6.4.15 Metalysis Ltd.

- 6.4.16 Polema

- 6.4.17 Linde Plc

- 6.4.18 Outokumpu

- 6.4.19 Rio Tinto Metal Powders

- 6.4.20 Sandvik AB

- 6.4.21 Seiko Epson Corporation

- 6.4.22 Tekna

- 6.4.23 Valimet

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

- 7.2 Increasing Developments in Healthcare Industries