|

시장보고서

상품코드

1906904

북미의 플라스틱 캡 및 마개 시장 : 시장 점유율 분석, 업계 동향, 통계, 성장 예측(2026-2031년)North America Plastic Caps And Closures - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

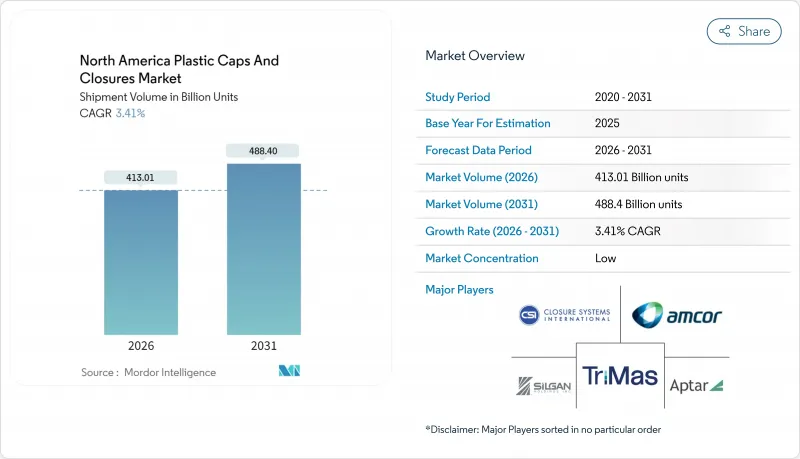

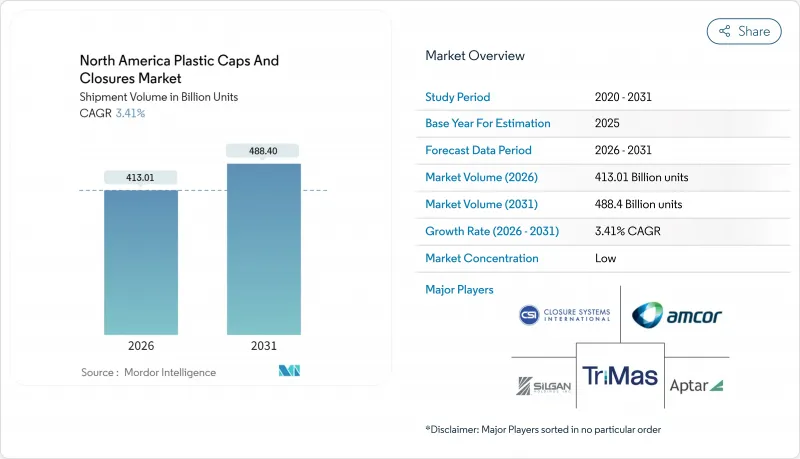

북미의 플라스틱 캡 및 마개 시장은 2025년 3,993억 9,000만개에서 2026년에는 4,130억 1,000만개로 성장할 것으로 보입니다. 2026-2031년에 걸쳐 CAGR 3.41%의 성장이 예상되며, 2031년까지 4,884억개에 이를 것으로 예측됩니다.

이러한 성장은 음료, 식품, 의약품, 퍼스널케어 전반에 걸쳐 제품 품질을 보호하는 동시에 엄격한 안전 및 지속가능성 기대치를 충족시키는 시장의 역할을 반영합니다. 기능성 음료 출시, 전자상거래 주도 의약품 판매, 주정부 차원의 재생 소재 의무화 정책은 특수 고성능 캡 수요를 지속적으로 견인하고 있습니다. 동시에 브랜드 소유자들은 순환경제 목표에 부합하는 연결형, 단일 소재, 어린이 안전 솔루션을 선호합니다. 신규 수지 사용료와 기후 관련 공급 차질로 인한 비용 압박은 제조업체들이 생산 자동화와 재활용 원료 통합을 추진하여 경쟁력을 유지하도록 유도하고 있습니다. 업계 참여자들은 또한 효율성 향상과 규모의 경제 확보를 위해 합병 및 인공지능 기반 결함 검사 시스템을 도입하고 있습니다.

북미의 플라스틱 캡 및 마개 시장 동향 및 인사이트

병 음료 및 기능성 음료 수요 급증

기능성 강화 워터, 휴식용 모크테일, 카페인 함유 스포츠 음료가 소매 채널에 지속적으로 진출하며, 전통적인 수분 보충 카테고리를 넘어 캡 수요량을 끌어올리고 있습니다. 프리미엄 포지셔닝은 최대 4배의 이산화탄소(CO2)를 보존하면서 탄산 유지와 브랜드 진열 차별화를 지원하는 내압성, 변조 방지 설계에 대한 투자를 촉진합니다. 음료 제조사들은 또한 민감한 기능성 원료를 보호하고 미국 식품의약국(FDA) 보충제 라벨링 규정을 준수하는 캡을 요구합니다. 또한 멕시코 소비자 지출 증가가 지역 음료 생산을 견인하며 가볍지만 견고한 캡에 대한 단위 수요를 확대하고 있습니다. 고속 병입 과정에서 일관된 토크 및 밀봉 성능을 제공하기 위해 제조업체가 충전업체와 협력함에 따라 공급망 안정성은 여전히 핵심 요소입니다.

브랜드 소유자의 테더형/전자상거래 대응용 캡 요구

소비자 직배송으로 인해 아마존 ISTA-6 준수 기준이 개인용품 및 음료 출시의 필수 조건이 되었습니다. 이에 브랜드 소유자들은 목 마감부에 고정되어 누출을 방지하고 운송 박스 내 캡 분실을 막는 테더형 포맷을 우선시합니다. 앳타의 '퓨처 디스크 탑'은 안전한 잠금 장치와 100% 폴리에틸렌 구조를 결합해 길가 재활용을 단순화한 대표적인 사례입니다. 식료품 소매업체 역시 자동 캡핑 라인을 효율화하고 캡-병 불일치로 인한 가동 중단 시간을 줄여주는 테더형 디자인을 선호합니다. 특허 받은 힌지 구조는 변조 방지 기능이나 소비자 편의성을 저해하지 않으면서도 다중 개폐 사이클을 지원합니다.

신규 수지에 대한 생산자 확대 책임(EPR) 수수료

캘리포니아를 비롯한 3개 주에서는 신규 수지 함량에 따라 증가하는 생산자 부담 재활용 수수료를 부과하여 캡 단위 비용을 직접 인상하고 있습니다. 생산자들은 수수료 부담을 완화하기 위해 재활용 또는 바이오 기반 원료로 포트폴리오를 전환하기 시작했으나, PCR 폴리프로필렌의 시장 공급은 여전히 제한적입니다. 관할권별 요금 체계 차이로 다중 주 충전업체의 규정 준수가 복잡해졌으며, 보고 의무는 새로운 행정 업무를 발생시킵니다. 규제 담당 인력이 부족한 중소 변환업체가 가장 큰 부담을 겪으며, 규모 있는 업체에 자산을 매각하는 통합이 가속화될 수 있습니다.

부문 분석

폴리에틸렌은 비용 효율성과 다용도 가공성을 바탕으로 2025년 플라스틱 캡 및 클로저 시장에서 41.98%의 최대 점유율을 유지했습니다. 그러나 브랜드 소유자들이 지속가능성 약속을 단일 폴리머 포장 흐름과 연계함에 따라 폴리에틸렌 테레프탈레이트(PET)가 6.45%의 연평균 복합 성장률(CAGR)로 가장 빠른 성장세를 기록했습니다. PET 캡은 이제 본질적인 재활용성과 성숙한 회수 네트워크를 활용하여 음료 및 개인 위생 부문에서 재료 순환을 완성하고 있습니다. 결정화 제어 및 첨가제 패키지의 혁신은 내열성을 향상시켜 밀봉 무결성을 저해하지 않으면서도 고온 충전 주스 생산을 가능하게 합니다. 오리진 머티리얼즈는 최근 표준 충전 라인과 호환되는 폴리에스터 수지 캡을 시연하며, 변환업체를 위한 양산 가능한 대안을 제시했습니다.

제조사들은 또한 EPR(생산자 책임 재활용) 부담금을 회피하기 위해 25%의 소비 후 PET 함량 목표를 모색하며, 식품 등급 재활용 펠릿 수요를 촉진하고 있습니다. 한편, 폴리프로필렌은 우수한 응력 균열 저항성 덕분에 공격적인 화학 및 제약 용도에서 입지를 유지하고 있습니다. 바이오 기반 폴리머는 틈새 시장이지만, 퇴비화 가능성 의무가 적용되는 분야에서 규제 당국의 관심을 받고 있습니다. 이러한 변화들은 총소유비용(TCO)과 재활용성 지표에 따라 결정되는 재료 선택의 모자이크를 형성합니다.

스크류 용기는 범용 넥 호환성에 의해 오랜 표준 사양으로서 46.85%의 쉐어를 유지(2025년 시점). 그러나, 온라인 약국에 의한 처방약의 소비자 직송 증가에 따라, 차일드 레지스턴트 캡(CRC)은 2031년까지 연평균 복합 성장률(CAGR)5.55%로 전 카테고리를 능가. FDA의 규제 강화로 특정 시판 영양 보조 식품 분말에도 CRC의 채택이 의무화되어 대응 가능한 시장 규모가 더욱 확대되고 있습니다. 베리, 세계사의 선택적 개봉 설계는 지속적인 연구개발의 성과를 나타내고 있으며, 이중안전기구와 성인용의 용이성을 융합시키고 있습니다.

분사형 변형 제품은 유량 조절로 낭비를 최소화하는 개인용 로션 및 가정용 세정제 분야에서 매력적입니다. 스냅핏 및 프레스온 솔루션은 신속한 적용과 경제적인 금형이 필요한 유제품 분야에서 여전히 유용합니다. 모든 캡 유형에서 진위 확인 및 재활용 지침을 지원하는 내장형 QR 코드는 소비자 직판 채널에서 부가가치 차별화 요소로 부상하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 병입 및 기능성 음료 수요 급증

- 브랜드 소유자의 테더형/전자상거래 대응형 캡 도입 추진

- 재활용 용이성을 위한 PP 단일 소재 캡 전환

- 온라인 의약품, 영양보조식품 시장의 급성장이 CRC 수요를 주도

- AI 기반 인라인 비전 시스템으로 불량률 및 비용 절감

- 시장 성장 억제요인

- 신규 수지에 부과되는 생산자 책임 확대(EPR) 비용

- 스크류 캡 대체용 피팅이 장착된 스탠드업 파우치 증가

- 미국/캐나다 rPET 함량 의무화로 신규 PP 수요 감소

- 음료 브랜드의 알루미늄 크라운 재밀봉 시험

- 공급망 분석

- 규제 상황

- 기술의 전망

- 지정학적 시나리오의 영향

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 재료별

- 폴리에틸렌(PE)

- 폴리에틸렌테레프탈레이트(PET)

- 폴리프로필렌(PP)

- 기타 재료

- 유형별

- 스크류식

- 디스펜서

- 비스크류

- 어린이 안전

- 최종 사용자 산업별

- 음료

- 생수

- 청량음료

- 스피릿

- 기타 음료

- 식품

- 의약품 및 헬스케어

- 화장품, 화장실

- 가정용 화학제품

- 기타 산업

- 음료

- 제조 공정별

- 사출 성형

- 압축 성형

- 3D 프린팅/래피드 프로토타이핑

- 기타 제조 공정

- 국가별

- 미국

- 캐나다

- 멕시코

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Silgan Holdings Inc.

- Amcor plc

- AptarGroup Inc.

- Closure Systems International Inc.

- TriMas Corporation

- Guala Closures SpA

- Tetra Pak Group

- O.Berk Company LLC

- BERICAP Holding GmbH

- Pano Cap Canada Ltd

- Erie Molded Plastics Inc.

- Crown Holdings Inc.

- Phoenix Closures Inc.

- Mold-Rite Plastics LLC

- Comar LLC

- Husky Technologies

- SACMI Imola SC

- Sonoco Products Company

- Plastipak Holdings Inc.

- Albea Group

제7장 시장 기회와 장래의 전망

HBR 26.02.04The North America plastic caps and closures market is expected to grow from 399.39 billion units in 2025 to 413.01 billion units in 2026 and is forecast to reach 488.4 billion units by 2031 at 3.41% CAGR over 2026-2031.

This growth reflects the market's role in safeguarding product quality across beverages, food, pharmaceuticals, and personal-care items while meeting rigorous safety and sustainability expectations. Functional beverage launches, e-commerce-driven pharmaceutical sales, and state-level recycled-content mandates continue to steer demand for specialized, high-performance closures. At the same time, brand owners favor tethered, mono-material, and child-resistant solutions that align with circular-economy goals. Cost pressures from virgin-resin fees and climate-related supply disruptions push manufacturers to automate production and integrate recycled feedstocks, ensuring competitive resilience. Industry participants also pursue mergers and AI-enabled defect-inspection systems to enhance efficiency and secure scale advantages.

North America Plastic Caps And Closures Market Trends and Insights

Demand Surge for Bottled and Functional Beverages

Enhanced waters, relaxation mocktails, and caffeinated sports drinks continue to penetrate retail channels, lifting closure volumes beyond traditional hydration categories. Premium positioning drives investments in pressure-resistant, tamper-evident designs that preserve carbonation up to 4 volumes of CO2 while supporting brand shelf differentiation. Beverage formulators also require closures that protect sensitive nutraceutical ingredients and comply with U.S. Food and Drug Administration supplement labeling. In addition, Mexican consumer spending growth bolsters regional beverage production, amplifying unit demand for lightweight yet robust caps. Supply-chain reliability remains essential as manufacturers coordinate with fillers to deliver consistent torque and seal performance during high-speed bottling.

Brand-Owner Push for Tethered / E-commerce-Ready Closures

Direct-to-consumer shipping has made Amazon ISTA-6 compliance a gating requirement for personal-care and beverage launches. Brand owners therefore prioritize tethered formats that stay attached to the neck finish, mitigate leakage, and avoid cap loss inside shipping cartons. Aptar's Future Disc Top exemplifies this, pairing a secure lock with 100% polyethylene construction that simplifies curbside recycling. Grocery retailers likewise favor tethered designs because they streamline automated capping lines and cut downtime tied to cap-to-bottle mismatches. Patented hinge geometries now support multiple open-close cycles without compromising tamper evidence or consumer convenience.

Extended Producer Responsibility (EPR) Fees on Virgin Resin

California and three other states now levy producer-funded recycling fees that climb with virgin resin intensity, directly raising closure unit costs. Producers have begun shifting portfolios toward recycled or bio-based feedstocks to blunt fee exposure, yet the market supply of PCR polypropylene remains limited. Fee schedules differ by jurisdiction, complicating compliance for multi-state fillers, while reporting obligations create new administrative tasks. Smaller converters lacking regulatory staff face the greatest burden, potentially accelerating consolidation as they sell assets to scale players.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward PP Mono-Material Caps for Easier Recycling

- On-Line Pharma and Nutraceutical Boom Fuels CRC Demand

- Rise of Stand-Up Pouches with Fitments Replacing Screw Caps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polyethylene retained the largest 41.98% slice of the plastic caps and closures market in 2025 on the back of cost efficiency and versatile processing. Nevertheless, polyethylene terephthalate marked the quickest advance at a 6.45% CAGR as brand owners linked sustainability pledges with single-polymer packaging streams. PET closures now leverage intrinsic recyclability and mature reclaim networks to close material loops in beverage and personal-care segments. Innovations in crystallinity control and additive packages lift heat-resistance, enabling hot-fill juices without sacrificing seal integrity. Origin Materials recently demonstrated polyester resin closures compatible with standard filling lines, signaling scale-ready alternatives for converters.

Manufacturers also explore post-consumer PET content targets of 25% to sidestep EPR levies, pushing demand for food-grade recycled pellets. Meanwhile, polypropylene holds ground in aggressive chemical and pharma uses because of superior stress-crack resistance. Bio-based polymers, though niche, gain regulatory attention where compostability mandates apply. Together, these shifts create a mosaic of material choices that hinge on total-cost-of-ownership and recyclability metrics.

Threaded formats, long the default due to universal neck compatibility, secured 46.85% share in 2025. Yet child-resistant closures outpaced all categories at 5.55% CAGR through 2031 as e-commerce pharmacies shipped increasing prescription volumes directly to consumers. Tightening FDA guidance now requires CRCs on certain over-the-counter nutraceutical powders, further broadening addressable volumes. Berry Global's selectively openable design illustrates ongoing R&D, merging dual-input safety with adult-friendly ergonomics.

Dispensing variants hold appeal in personal-care lotions and household cleaners where controlled flow minimizes waste. Snap-fit and press-on solutions remain useful in dairy products needing quick application and economical tooling. Across closure types, embedded QR codes supporting authenticity verification and recycling instructions emerge as value-added differentiators in direct-to-consumer channels.

The North America Plastic Caps and Closures Market Report is Segmented by Material (Polyethylene, PET, Polypropylene, and More), Type (Threaded, Dispensing, and More), End-User Industry (Beverage, Food, Pharmaceutical and Healthcare, Cosmetics and Toiletries, and More), Manufacturing Process (Injection Molding, Compression Molding, 3-D Printing, and More), and Geography. The Market Forecasts are Provided in Terms of Volume (Units).

List of Companies Covered in this Report:

- Silgan Holdings Inc.

- Amcor plc

- AptarGroup Inc.

- Closure Systems International Inc.

- TriMas Corporation

- Guala Closures SpA

- Tetra Pak Group

- O.Berk Company LLC

- BERICAP Holding GmbH

- Pano Cap Canada Ltd

- Erie Molded Plastics Inc.

- Crown Holdings Inc.

- Phoenix Closures Inc.

- Mold-Rite Plastics LLC

- Comar LLC

- Husky Technologies

- SACMI Imola S.C.

- Sonoco Products Company

- Plastipak Holdings Inc.

- Albea Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Demand surge for bottled and functional beverages

- 4.2.2 Brand-owner push for tethered / e-commerce-ready closures

- 4.2.3 Shift toward PP mono-material caps for easier recycling

- 4.2.4 On-line pharma and nutraceutical boom fuels CRC demand

- 4.2.5 AI-enabled in-line vision lowers defect rates and costs

- 4.3 Market Restraints

- 4.3.1 Extended Producer Responsibility (EPR) fees on virgin resin

- 4.3.2 Rise of stand-up pouches with fitments replacing screw caps

- 4.3.3 U.S./Canada rPET content mandates squeeze virgin PP demand

- 4.3.4 Beverage brand trials of aluminium crown re-seals

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Geopolitical Scenarios

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VOLUME)

- 5.1 By Material

- 5.1.1 Polyethylene (PE)

- 5.1.2 Polyethylene Terephthalate (PET)

- 5.1.3 Polypropylene (PP)

- 5.1.4 Other Materials

- 5.2 By Type

- 5.2.1 Threaded

- 5.2.2 Dispensing

- 5.2.3 Unthreaded

- 5.2.4 Child-Resistant

- 5.3 By End-user Industry

- 5.3.1 Beverage

- 5.3.1.1 Bottled Water

- 5.3.1.2 Soft Drinks

- 5.3.1.3 Spirits

- 5.3.1.4 Other Beverages

- 5.3.2 Food

- 5.3.3 Pharmaceutical and Healthcare

- 5.3.4 Cosmetics and Toiletries

- 5.3.5 Household Chemicals

- 5.3.6 Other Industries

- 5.3.1 Beverage

- 5.4 By Manufacturing Process

- 5.4.1 Injection Molding

- 5.4.2 Compression Molding

- 5.4.3 3-D Printing / Rapid Prototyping

- 5.4.4 Other Manufacturing Process

- 5.5 By Country

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Silgan Holdings Inc.

- 6.4.2 Amcor plc

- 6.4.3 AptarGroup Inc.

- 6.4.4 Closure Systems International Inc.

- 6.4.5 TriMas Corporation

- 6.4.6 Guala Closures SpA

- 6.4.7 Tetra Pak Group

- 6.4.8 O.Berk Company LLC

- 6.4.9 BERICAP Holding GmbH

- 6.4.10 Pano Cap Canada Ltd

- 6.4.11 Erie Molded Plastics Inc.

- 6.4.12 Crown Holdings Inc.

- 6.4.13 Phoenix Closures Inc.

- 6.4.14 Mold-Rite Plastics LLC

- 6.4.15 Comar LLC

- 6.4.16 Husky Technologies

- 6.4.17 SACMI Imola S.C.

- 6.4.18 Sonoco Products Company

- 6.4.19 Plastipak Holdings Inc.

- 6.4.20 Albea Group

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment