|

시장보고서

상품코드

1940629

미국의 플라스틱 뚜껑 및 마개 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)United States (US) Plastic Caps And Closures - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

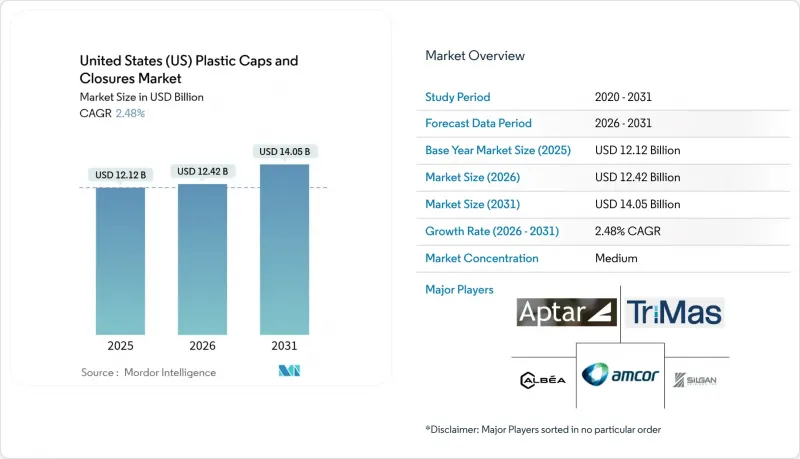

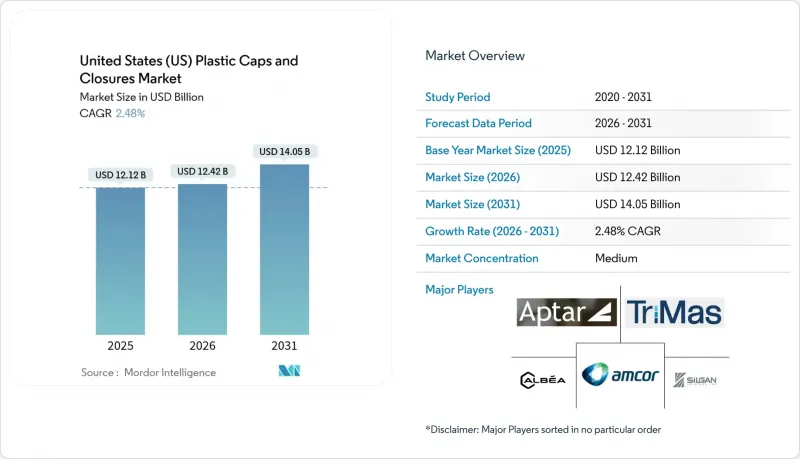

미국의 플라스틱 뚜껑 및 마개 시장은 2025년에 121억 2,000만 달러로 평가되었고, 2026년 124억 2,000만 달러에서 2031년까지 140억 5,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 2.48%로 예상됩니다.

이러한 완만한 성장 속도는 규제 준수 비용, 수지 가격 변동, 음료, 의약품, EC 포장 분야 수요 급증 등이 복합적으로 작용한 결과입니다. 끈 달린 캡에 대한 법규, 강화된 어린이 안전 기준, NFC 인증 기술에 대한 브랜드들의 관심이 높아지면서 소재 선택과 제조 방식에 대한 재검토가 진행되고 있습니다. 폴리프로필렌(PP)은 저비용과 우수한 차단 성능으로 지배적인 위치를 유지하고 있지만, 폴리에틸렌 테레프탈레이트(PET)는 브랜드가 경량화 및 순환성 목표를 추구하면서 점유율을 확대하고 있습니다. 비용 효율적인 사출 성형과 프리미엄 스마트 클로저 기능을 결합한 제조업체는 미국의 플라스틱 뚜껑 및 마개 시장에서 새로운 기회를 포착할 수 있는 가장 유리한 위치에 있습니다.

미국의 플라스틱 뚜껑 및 마개 시장 동향과 인사이트

편의성 높은 포장 음료 수요 급증

이동이 잦은 소비 습관과 기능성 수분 보충 제품 출시로 인해, 쉽게 열고 다시 밀봉할 수 있는 뚜껑이 있는 일회용 PET 병에 대한 수요가 지속적으로 증가하고 있습니다. 음료 충전 제조업체들은 21 CFR S211.132의 변조 방지 규정을 준수하면서 한 손으로 조작할 수 있는 스포츠 캡이나 플립탑 형태의 클로저를 지정하는 경향이 증가하고 있습니다. 브랜드 소유주들은 캡에 NFC 태그나 QR코드를 결합하여 구매 후 참여와 로열티 프로그램을 촉진하고 캡을 디지털 미디어 매체로 활용하고 있습니다. 프리미엄 워터, 에너지 음료, 인스턴트 커피가 선반 공간을 차지하는 가운데, 캡 제조업체는 산소 흡수 라이너, 일체형 스파우트, 브랜드 아이덴티티를 강화하는 컬러 매칭 마감과 같은 부가가치 제품을 판매할 수 있는 기회를 얻게 되었습니다. 미국의 플라스틱 뚜껑 및 마개 시장은 이러한 요구 사항의 혜택을 받고 있습니다. 부가가치 설계가 탄산음료의 완만한 물량 성장을 보완하고 있기 때문입니다.

확대되는 의약품 포장 요구 사항

고령화와 처방약 치료의 보급에 따라 미국 소비자제품안전위원회(CPSC)의 토크 및 푸시-턴 테스트를 통과하고, 어린이 안전 기능을 갖추고 고령자도 사용하기 쉬운 캡에 대한 수요가 증가하고 있습니다. 자동 조제 캐비닛을 도입하는 병원이나 약국에서는 투약 실수를 방지하기 위해 매우 균일한 토크 범위와 라이너의 무결성이 요구됩니다. 현재 24개 주에서 규제 물질로 관리되는 합법적인 대마초 제품은 중독 방지 포장 기준을 충족해야 하며, 이는 인증된 재밀봉 시스템의 고부가가치 틈새 시장을 창출하고 있습니다. 마이크로 센서와 타임스탬프 기능이 내장된 스마트 클로저는 치료 순응도를 추적하고 잠재적인 오용을 경고하는 데 도움이 되며, 전문 컨버터 회사들이 헬스케어 기술 분야와 제휴할 수 있는 관문이 되고 있습니다.

수지 가격 변동성

멕시코만 연안에 집중된 폴리올레핀 원료는 허리케인이나 예상치 못한 크래커 가동 중단의 영향을 받기 쉬우며, 몇 주 안에 PP/PE 현물 가격이 30-50% 상승할 수 있습니다. 캡 제조업체는 추가 요금 전가가 늦어지고, 가격 급등 시 수익률이 압박을 받아 신규 금형 투자가 억제됩니다. 일부 컨버터는 선물 계약으로 수지 구매를 헤지하고 있지만, 변동성은 여전히 고정 가격 지수화를 중시하는 장기 음료 공급 계약을 복잡하게 만들고 있습니다. 2026-2027년 가동 예정인 신규 셰일가스 크래커는 생산능력 증가를 약속하는 한편, 단기적인 리스크 프로파일로 인해 재고 슬림화 및 다중 조달 전략이 요구되고 있습니다.

부문 분석

폴리프로필렌은 화학적 안정성과 고속 사출 성형 라인에 대한 적합성을 강점으로 미국의 플라스틱 뚜껑 및 마개 시장의 41.12%를 점유하고 있습니다. 음료 충전업체들이 경량 스크류 캡을 표준화하는 한편, 가정용 화학제품 분야에서는 내용매성이 우수한 PP 소재의 플립 캡이 지속적으로 선호되고 있어 이 부문은 낮은 한 자릿수 성장이 예상됩니다. PET는 점유율이 한 자릿수에 불과하지만, 저밀도와 병에서 캡으로 재활용하는 공정과의 호환성으로 인해 2031년까지 연평균 복합 성장률(CAGR) 3.45%로 가장 빠르게 성장할 것으로 예측됩니다. 이러한 장점은 사이클 타임과 폐기물을 줄이는 Origin Materials의 새로운 열성형 공정을 통해 더욱 강화되었습니다.

상위 2가지 소재 외에 고밀도 폴리에틸렌(HDPE)은 펑크 저항과 어린이 안전 토크 범위가 요구되는 의약품 바이알의 주요 소재이며, 저밀도 폴리에틸렌(LDPE)은 조미료와 퍼스널케어 크림의 디스펜싱 노즐에 선호됩니다. 특수 바이오폴리머는 점유율이 2% 미만이지만, 브랜드의 지속가능성 요구사항이 비용을 능가하는 분야에서 채택이 확대되고 있습니다. 이러한 추세에 따라 가공업체가 선택할 수 있는 재료의 폭이 넓어지고, 수지 공급업체는 가격뿐만 아니라 순환성에 대한 노력으로 차별화를 꾀해야 하는 상황에 처해 있습니다.

음료 분야는 2025년 기준 미국의 플라스틱 뚜껑 및 마개 시장 규모의 30.05%를 차지할 것으로 예측됩니다. 이는 생수 및 탄산음료 리필 수요가 많기 때문입니다. 그러나 탄산음료 부문의 성숙에 따라 성장이 둔화되는 추세이며, 기능성 음료와 스포츠음료는 고수익성 스포츠캡으로 전환이 진행되고 있습니다. 반면, 의약품용 캡은 처방약 물량 증가와 주정부 대마초 시장에서 인증된 아동용/노인용 SKU 추가에 따라 연간 4.79%의 성장률을 보일 것으로 예측됩니다. 병원에서는 1회용 블리스 터 팩으로 전환이 진행 중, 점적용 병이나 경구용 현탁액의 캡 밀봉 방식이 여전히 주류이며, 일부 치료법이 파우치나 펜형 용기로 전환되더라도 기초 수요는 유지될 것입니다.

식품 분야는 안정적인 성장세를 유지하고 있으며, 변조 방지성과 누출 방지성을 중시하는 EC 시장의 확대가 기여하고 있습니다. 화장품 및 세면도구 분야에서는 고급스러운 오버캡, 메탈릭 마감, 브랜드 컬러와의 조화가 요구되어 소량이지만 수익성이 높은 틈새 시장을 형성하고 있습니다. 가정용 화학제품 분야에서는 안전 밀봉과 투약 정확도가 중요해지면서 견고한 라이너 시스템과 토크 관리의 중요성이 재인식되고 있습니다. 이러한 조합은 성공적인 공급업체가 음료 수요에 지나치게 의존하지 않고 여러 성장 분야에 맞게 캡 제품군을 맞춤화하는 이유를 뒷받침합니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

LSH 26.03.10The United States plastic caps and closures market was valued at USD 12.12 billion in 2025 and estimated to grow from USD 12.42 billion in 2026 to reach USD 14.05 billion by 2031, at a CAGR of 2.48% during the forecast period (2026-2031).

This measured pace reflects a mix of regulatory compliance costs, resin price swings, and surging demand from beverages, pharmaceuticals, and e-commerce packaging. Legislation on tethered caps, stricter child-resistant rules, and brand interest in NFC-enabled authentication are reshaping material choices and production methods. Polypropylene (PP) retains a dominant footprint due to its low cost and strong barrier performance, while polyethylene terephthalate (PET) is gaining share as brands pursue lightweighting and circularity objectives. Manufacturers that combine cost-efficient injection molding with premium smart-closure features are best positioned to capture emerging opportunities in the United States plastic caps and closures market.

United States (US) Plastic Caps And Closures Market Trends and Insights

Surge in Demand for Convenient Packaged Beverages

On-the-go consumption habits and functional hydration launches continue to pull volume through single-serve PET bottles fitted with easy-open, resealable tops. Beverage fillers increasingly specify closures compatible with sports caps and flip-top formats that support one-handed operation while complying with 21 CFR S211.132 tamper-evident rules. Brand owners are pairing NFC tags and QR codes on caps to drive post-purchase engagement and loyalty programs, turning closures into a digital media surface. As premium water, energy drinks, and ready-to-drink coffee command shelf space, closure makers gain opportunities to upsell oxygen-scavenging liners, integrated spouts, and color-matched finishes that reinforce brand identity. The United States plastic caps and closures market benefits from these requirements because value-added designs offset modest volume growth in carbonated soft drinks.

Expanding Pharmaceutical Packaging Requirements

An aging population and wider access to prescription therapies elevate demand for child-resistant, senior-friendly caps that pass Consumer Product Safety Commission torque and push-turn protocols. Hospitals and pharmacies rolling out automated dispensing cabinets also require highly consistent torque ranges and liner integrity to prevent dosage errors. Legal cannabis products-now regulated as controlled substances in 24 states-must meet poison-prevention packaging standards, spawning a premium niche for certified reclosable systems. Smart closures embedding micro-sensors or time-stamp features help track therapy adherence and flag potential misuse, giving specialty converters an entry point into health-tech partnerships.

Volatility in Resin Prices

Polyolefin feedstocks clustered along the Gulf Coast remain vulnerable to hurricanes and unplanned cracker outages that can lift spot PP and PE prices by 30-50% within weeks. Closure makers pass through surcharges with a lag, compressing margins and curbing investment in new tooling during spikes. Some converters hedge resin purchases via futures contracts, yet volatility still complicates long-term beverage supply agreements that favor fixed-price indexation. While new shale-gas crackers slated for 2026-2027 promise incremental capacity, the near-term risk profile encourages leaner inventories and multiple-sourcing strategies.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Lightweight Plastic Over Metal Closures

- Growth of E-commerce Requiring Tamper-Evident Designs

- Competition from Sustainable Alternative Materials

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polypropylene commands 41.12% share of the United States plastic caps and closures market, anchored by its chemical stability and suitability for high-speed injection molding lines. The segment is expected to post low-single-digit growth as beverage fillers standardize lightweight screw tops and household chemicals continue to favor PP flip caps for solvent resistance. PET, while only a mid-single-digit share contributor, is forecast as the fastest-growing at a 3.45% CAGR through 2031 thanks to its low density and compatibility with bottle-to-cap recycling streams, an advantage amplified by Origin Materials' novel thermoforming route that lowers cycle time and waste.

Moving beyond the top two, high-density polyethylene remains the material of choice for pharmaceutical vials that demand puncture resistance and child-safe torque ranges, whereas low-density polyethylene is preferred in dispensing nozzles for condiments and personal-care creams. Specialty bio-polymers, though under 2% share, gain traction where brand sustainability mandates override cost. Collectively, these dynamics widen the material toolbox available to converters and force resin suppliers to differentiate on circularity credentials, not just price.

Beverages accounted for 30.05% of the United States plastic caps and closures market size in 2025 due to vast bottled-water volumes and carbonated soft drink refills. Growth, however, moderates as carbonated segments mature, while functional beverages and sports drinks shift toward higher-margin sports caps. Pharmaceutical closures, in contrast, will grow 4.79% annually as prescription drug volumes climb and state cannabis markets add SKUs that mandate certified child-resistant or senior-friendly designs. Hospitals converting to unit-dose blister packs still rely on closure-sealed infusion bottles and oral suspensions, sustaining baseline demand even as some therapies migrate to pouches or pens.

Food products maintain a stable trajectory, helped by e-commerce adoption, which places a premium on tamper-evident and leak-proof attributes. Cosmetics and toiletries reach for premium overcaps, metallized finishes, and color harmony with brand palettes, making them a lucrative niche despite modest volumes. Household chemicals emphasize safety seals and dosing accuracy, reinforcing the importance of robust liner systems and torque control. Together, the mix underscores why successful suppliers tailor closure portfolios to multiple growth vectors instead of over-relying on beverage volumes.

The United States Plastic Caps and Closures Market Report is Segmented by Material (PET, PP, LDPE, and More), End-User Industry (Beverage, Food, Pharmaceutical and Healthcare, and More), Cap Type (Screw Closures, Tethered Caps, and More), and Manufacturing Technology (Injection Molding, Compression Molding, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Silgan Holdings Inc.

- AptarGroup, Inc.

- Amcor plc

- Albea S.A.

- TriMas Corporation

- Tetra Pak International S.A.

- Guala Closures S.p.A.

- MJS Packaging, Inc.

- O. Berk Company, LLC

- Closure Systems International, Inc.

- BERICAP GmbH & Co. KG

- Crown Holdings, Inc.

- Evergreen Packaging LLC

- Phoenix Closures, Inc.

- Portola Packaging, Inc.

- Plastipak Packaging, Inc.

- Mold-Rite Plastics, LLC

- Smurfit WestRock

- SIG Combibloc Group AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in demand for convenient packaged beverages

- 4.2.2 Expanding pharmaceutical packaging requirements

- 4.2.3 Shift toward lightweight plastic over metal closures

- 4.2.4 Growth of e-commerce requiring tamper-evident designs

- 4.2.5 Adoption of tethered cap legislation

- 4.2.6 Reshoring via high-speed compression-molding capacity

- 4.3 Market Restraints

- 4.3.1 Volatility in resin prices

- 4.3.2 Competition from sustainable alternative materials

- 4.3.3 Prospective federal single-use-plastic restrictions

- 4.3.4 Micro-plastic scrutiny driving liner-less closures

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Degree of Competition

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Polyethylene Terephthalate (PET)

- 5.1.2 Polypropylene (PP)

- 5.1.3 Low Density Polyethylene (LDPE)

- 5.1.4 High-Density Polyethylene (HDPE)

- 5.1.5 Other Materials

- 5.2 By End-user Industry

- 5.2.1 Beverage

- 5.2.2 Food

- 5.2.3 Pharmaceutical and Healthcare

- 5.2.4 Cosmetics and Toiletries

- 5.2.5 Household Chemicals

- 5.2.6 Other End-user industries

- 5.3 By Cap Type

- 5.3.1 Screw Closures

- 5.3.2 Tethered Caps

- 5.3.3 Flip-top and Snap-on Caps

- 5.3.4 Child-resistant Closures

- 5.3.5 Luxury/Premium Decorative Closures

- 5.3.6 Dispensing Caps

- 5.4 By Manufacturing Technology

- 5.4.1 Injection Molding

- 5.4.2 Compression Molding

- 5.4.3 3-Piece and In-line Assembly

- 5.4.4 Digitally Printed Smart Closures

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Silgan Holdings Inc.

- 6.4.2 AptarGroup, Inc.

- 6.4.3 Amcor plc

- 6.4.4 Albea S.A.

- 6.4.5 TriMas Corporation

- 6.4.6 Tetra Pak International S.A.

- 6.4.7 Guala Closures S.p.A.

- 6.4.8 MJS Packaging, Inc.

- 6.4.9 O. Berk Company, LLC

- 6.4.10 Closure Systems International, Inc.

- 6.4.11 BERICAP GmbH & Co. KG

- 6.4.12 Crown Holdings, Inc.

- 6.4.13 Evergreen Packaging LLC

- 6.4.14 Phoenix Closures, Inc.

- 6.4.15 Portola Packaging, Inc.

- 6.4.16 Plastipak Packaging, Inc.

- 6.4.17 Mold-Rite Plastics, LLC

- 6.4.18 Smurfit WestRock

- 6.4.19 SIG Combibloc Group AG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment