|

시장보고서

상품코드

1910449

통증 관리 시장 : 점유율 분석, 업계 동향, 통계, 성장 예측(2026-2031년)Pain Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

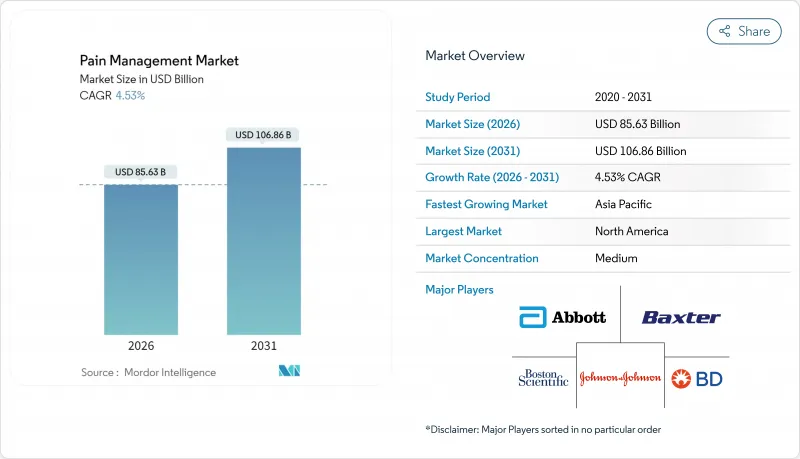

통증 관리 시장 규모는 2026년에는 856억 3,000만 달러로 추정되고 있으며, 2025년 819억 2,000만 달러에서 성장한 수치입니다. 2031년까지 1,068억 6,000만 달러에 이르고, 2026년부터 2031년까지 연평균 복합 성장률(CAGR) 4.53%로 성장할 것으로 전망되고 있습니다.

평균 수명 연장, 오피오이드 규제 강화, 연결형 신경 조절 플랫폼의 보급 확대가 이 성장 궤도를 지원하고 있습니다. 의료 종사자들은 현재 비-오피오이드 약리학과 장치 기반 치료법을 결합한 멀티모달 요법을 선호하고 있으며, 이러한 변화는 투약량보다 지속적인 치료 결과를 평가하는 지불자 측 인센티브에 의해 더욱 강화되고 있습니다. 디지털 건강과의 통합은 시간이 지남에 따라 모니터링을 개선하고 치료 강도를 환자가보고하는 실시간 통증 점수로 조정하는 동시에 재입원을 억제합니다. 한편, 기존의 오피오이드 제조업체에 대한 ESG(환경, 사회, 거버넌스) 감사의 강화는 의존성이 없는 대체약이나 AI 구동형 투약 알고리즘의 개발 기업으로의 자본 유입을 가속화하고 있습니다.

세계 통증 관리 시장 동향과 인사이트

연령에 따른 만성 통증 유병률 상승

45세 이상의 인구 증가와 함께 만성 근골격통 및 신경장애성 통증의 발생률이 가장 높아지고 있습니다. 2024년에는 미국 성인의 24.3%가 만성 통증을 보고해 65세 이상으로 유병률이 피크에 달했습니다. 유럽의 메타 분석에서는 당뇨병, 관절염, 수술후 증후군을 주인으로 하여 성인의 유병률은 21.45%로 산출되고 있습니다. 지속적인 통증을 앓고 있는 환자는 같은 연령대에 비해 건강 관리 비용이 2배가 걸리고, 고소득 국가에서는 연간 1만 2,167달러의 생산성을 잃고 있습니다. 이 때문에 지불기관은 의약품, 의료기기, 행동요법을 조합한 장기 프로그램에 자금을 투입하고 있습니다. 만성 통증을 독립 질환으로 인식함으로써 전용 상환 코드가 도입되어 세계적으로 전문 클리닉의 수용 체제가 확충되고 있습니다.

신경 조절 요법의 효능에 대한 임상 검증

획기적인 비용 효과 연구는 척수 자극 요법과 최상의 약물 요법을 함께 사용하면 10년동안 비용 효과를 유지하고 일반적인 지불 의사 역치에서 약물 관리를 능가하는 효과를 나타냈습니다. 후근 신경절 기술은 초기 비용이 높은 것, 국소 신경 장애 증후군에 대한 더 높은 품질 조정 생존 연도(QALY)를 제공합니다. 폐루프 플랫폼은 유도 복합 활동 전위에 따라 진폭을 자동으로 조정하고 생리 상태의 변화에 따라 지속적인 진통 효과를 유지합니다. 규제당국은 획기적인 의료기기 지정을 통해 시장 진입을 가속화하고 심사기간 단축과 벤처투자 촉진을 도모하고 있습니다. 특정 EU 회원국의 상환 범위 확대는 신경조절의 지속가치가 인정되었음을 뒷받침하고 병원 구매 의욕과 의사 채택률을 높입니다.

임베디드 디바이스의 고액 설비 투자비 및 운영비

환자 1인당 미화 2만-5만 달러의 임베디드 펄스 발생기는 신흥 경제국의 공적 예산을 크게 상회합니다. 4-7년마다의 교환 수술에는 마취 및 입원비가 추가되어 지불자의 허용 범위를 넘습니다. 의료기술평가기관은 현재 고액의 신경조절치료의 상환승인 전에 10년간의 실임상 데이터를 요구하고 있습니다. 이에 반해 제조업체는 충전식 전지로의 이행이나 자동 프로그래밍에 의한 임상의의 관여 삭감으로 대응하고 있습니다. 리스 모델이나 성과 연동형 계약도 등장하기 시작하고 있습니다만, 자본 집약성은 여전히 저소득 및 중소득국에 있어서의 장벽이 되고 있습니다.

부문 분석

2025년 시점의 통증 관리 시장 점유율은 약제가 68.92%를 차지했고 신경장애성 통증 치료에 사용되는 NSAIDs, 항경련제, 선택적 항우울제가 기반이 되고 있습니다. 지침 작성자가 오피오이드 절약 요법을 권장하는 동안 나트륨 채널 차단제를 포함한 비 오피오이드 기반 신약의 개발은 기세를 유지하고 있습니다. 금액 기준으로 의약품 부문은 아시아태평양과 라틴아메리카에서 일반 의약품의 보급을 배경으로 전년 대비 32억 달러 증가를 기록했습니다. 의료기기는 의약품을 웃도는 CAGR 9.99%로 성장하고 2031년까지 통증 관리 시장 규모에 약 110억 달러가 추가될 것으로 예상됩니다.

폐루프 척수 자극 장치와 후근 신경절 자극 시스템은 이러한 급성장을 견인하고 실시간 생리적 피드백을 활용하여 진폭과 펄스 폭을 미세 조정합니다. 진통제 주입 펌프는 소형화가 진행되는 한편, 임상의의 대시보드에 정보를 제공하는 블루투스 대응 투여 기록 기능을 획득하고 있습니다. 2024년과 2025년에 FDA가 인정한 브레이크스루 디바이스는 심사 사이클을 6-9개월 단축하여 상업 전개를 가속화하고 있습니다. 가치 기반 조달이 확산되는 가운데, 병원 구매 담당자는 총 소유 비용을 중시하는 경향이 강해지고 있으며, 이 지표에서는 장수명 배터리를 갖춘 충전식 자극 장치가 유리합니다.

지역별 분석

북미는 2025년에도 38.10%의 매출을 유지했습니다. 성숙한 상환 제도, 광범위한 외래수술센터(ASC) 네트워크, 신속한 FDA 승인 프로세스가 이를 지원합니다. 오피오이드 판매를 둘러싼 소송의 계속에 의해 비의존성 치료법에의 다양화가 진행되어, 신경조절 요법이나 비오피오이드 진통제에 대한 수요를 증가시키고 있습니다. 2025년 미국에서 추가로 실시되는 메디케이드 확대로 종합적 통증 관리 프로그램의 대상 환자층이 더욱 확대됩니다.

유럽은 균형 잡힌 성숙 단계를 보여줍니다. 서유럽 국가에서는 점진적인 성장이 지속되는 반면, 동유럽 시장에서는 EU의 결속 기금에 의한 지원하에 의료기기의 도입이 가속화되고 있습니다. 유럽 의약품청의 롤링 리뷰 절차에 따라 2025년에는 바이오시밀러 및 신규 진통제의 평균 승인 기간이 15% 단축되었습니다. 각국의 의료기술평가기관은 생활의 질(QOL) 결과를 중시하는 경향이 강해지고 있으며, 검증된 신경조절적응증에 대한 상환범위의 확대를 촉진하고 있습니다.

아시아태평양은 2031년까지 연평균 복합 성장률(CAGR) 10.55%로 가장 높은 성장률을 보입니다. 중국의 「건강 중국 2030」계획은 만성 통증을 중점 과제로 자리매김하고, 2차 의료 기관에 의한 전문 통증 클리닉의 설치를 가능하게 합니다. 2025년에 제정된 인도의 원격 의료 가이드라인은 비지정 의약품의 전자 처방전을 합법화하고 디지털 진료 플랫폼을 촉진합니다. 그러나 보험가입률의 변동과 의료제공업체 시장의 분단은 여전히 고비용의 임베디드 의료기기의 도입을 제한하고 있으며, 인구동태적인 잠재력에 비해 절대적인 시장 규모를 제약하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 노화에 따른 만성 통증 환자 증가 경향

- 신경조절요법의 효능에 대한 임상적 검증

- 오피오이드 사용을 억제하는 다각적 치료 프로토콜로의 전환

- 통증 치료에 있어서의 외래 수술 시설의 급속한 보급

- 폐쇄 루프 자극 플랫폼을 위한 벤처 자금 조달

- AI 기반 환자 맞춤형 투약 알고리즘

- 시장 성장 억제요인

- 이식형 의료기기의 고액의 설비투자비용(CAPEX)/운영비용(OPEX)

- 신흥 시장에서의 상환제한

- 연결형 펌프의 사이버 보안 위험

- 오피오이드 제조업체에 대한 ESG 심사

- 공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자 및 소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 통증 관리 방법별

- 의약품

- 오피오이드

- 비마약성 진통제

- 비스테로이드성 소염진통제(NSAIDs)

- 마취제

- 항경련제

- 항우울제

- 의료기기

- 신경 조절 기기

- TENS

- 척수자극기(SCS)

- 척수신경절 자극기(DRG)

- 미주 신경 및 말초 신경 자극기

- 진통제 주입 펌프

- 경막 내 펌프

- 외부 PCA 펌프

- 고주파 절제 시스템

- 신경 조절 기기

- 의약품

- 용도별

- 신경장애성 통증

- 암 통증

- 근골격계의 통증

- 안면통 및 편두통

- 수술 후 및 급성 통증

- 의료 제공 환경별

- 병원

- 외래수술센터(ASC)

- 재택치료 및 원격 모니터링

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Abbott Laboratories

- Baxter International Inc.

- Becton, Dickinson and Company

- Boston Scientific Corporation

- Endo International plc

- Fresenius SE & Co. KGaA

- Grunenthal GmbH

- Hikma Pharmaceuticals

- Hisamitsu Pharmaceutical

- Insulet Corporation

- Johnson & Johnson(DePuy Synthes, Ethicon)

- Medtronic plc

- Nevro Corp.

- Novartis AG

- Omron Healthcare

- Pfizer Inc.

- Smiths Medical (ICU Medical)

- Stryker Corporation

- Terumo Corporation

- Teva Pharmaceutical Industries

제7장 시장 기회와 장래의 전망

SHW 26.01.26pain management market size in 2026 is estimated at USD 85.63 billion, growing from 2025 value of USD 81.92 billion with 2031 projections showing USD 106.86 billion, growing at 4.53% CAGR over 2026-2031.

Greater life expectancy, stringent opioid regulations and expanding use of connected neuromodulation platforms anchor this growth trajectory. Clinicians now favor multimodal regimens that blend non-opioid pharmacology with device-based therapies, a shift reinforced by payer incentives rewarding durable outcomes over pill counts. Digital health integration improves longitudinal monitoring, aligning treatment intensity with real-time patient-reported pain scores while curbing hospital readmissions. Heightened ESG scrutiny of legacy opioid makers meanwhile accelerates capital flows toward developers of non-addictive alternatives and AI-driven dosing algorithms.

Global Pain Management Market Trends and Insights

Ageing-Related Rise in Chronic Pain Prevalence

Growing cohorts aged >= 45 now represent the highest incidence of chronic musculoskeletal and neuropathic complaints. In 2024, 24.3% of U.S. adults reported chronic pain, with prevalence peaking in the 65+ group. European meta-analysis places adult prevalence at 21.45%, propelled by diabetes, arthritis, and postsurgical syndromes. Patients living with persistent pain incur double the healthcare expenditure of age-matched peers and lose USD 12,167 annually in productivity within high-income countries. Payers, therefore, channel funds toward longitudinal programs combining pharmaceutical, device, and behavioral elements. Recognition of chronic pain as a standalone disease entity further unlocks dedicated reimbursement codes and specialty clinic capacity worldwide.

Clinical Validation of Neuromodulation Efficacy

Landmark cost-utility studies show spinal cord stimulation paired with best medical therapy remains cost-effective over 10 years, outperforming pharmacologic management at typical willingness-to-pay thresholds. Dorsal root ganglion technology delivers even higher quality-adjusted life years for focal neuropathic syndromes, despite steeper upfront costs. Closed-loop platforms now auto-adjust amplitude based on evoked compound action potentials, sustaining analgesia as physiologic states shift. Regulatory bodies accelerate market entry through Breakthrough Device designations, trimming review times and incentivizing venture investment. Expanded reimbursement in select EU member states confirms recognition of durable neuromodulation value, increasing hospital purchasing confidence and physician adoption rates.

High CAPEX/OPEX for Implantable Devices

Implantable pulse generators priced between USD 20,000 - 50,000 per patient exceed many public-sector budgets in emerging economies. Replacement surgeries every 4-7 years add anesthesia and hospitalization charges, straining payer tolerance. Health technology assessment agencies now demand ten-year real-world evidence before approving high-cost neuromodulation reimbursement lines. Manufacturers react by migrating to rechargeable batteries and automated programming that lower clinician touchpoints. Leasing models and outcome-based contracts have begun surfacing, yet capital intensity remains a gating factor across low- and middle-income settings.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Opioid-Sparing Multimodal Protocols

- Rapid ASC Adoption for Pain Procedures

- Limited Reimbursement in Emerging Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Drugs retained 68.92% of pain management market share in 2025, anchored by NSAIDs, anticonvulsants and selective antidepressants used for neuropathic indications. Non-opioid innovations, including sodium-channel blockers, sustain momentum as guideline authors promote opioid-sparing regimens. In value terms, the drugs segment added USD 3.2 billion year-over-year, supported by strong generic uptake in Asia-Pacific and Latin America. Devices are set to outpace pharmaceuticals at a 9.99% CAGR, adding roughly USD 11 billion to the pain management market size by 2031.

Closed-loop spinal cord stimulators and dorsal root ganglion systems headline this surge, leveraging real-time physiologic feedback to fine-tune amplitude and pulse width. Analgesic infusion pumps shrink in form factor while gaining Bluetooth-enabled dosage logs that feed clinician dashboards. FDA Breakthrough Device designations granted in 2024 and 2025 shave six to nine months from review cycles, accelerating commercial rollout. As value-based procurement spreads, hospital buyers increasingly weigh total cost of ownership, a metric favoring rechargeable stimulators with extended battery life.

The Pain Management Market Report is Segmented by Mode of Pain Management (Drugs [Opioids and Non-Narcotic Analgesics] and Devices [Neuro-Modulation Devices and More]), Application (Neuropathic Pain, Cancer Pain, Facial Pain & Migraine and More), Setting of Care (Hospitals, Ambulatory Surgical Centers and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 38.10% revenue in 2025, supported by mature reimbursement, extensive ASC networks and swift FDA clearance pathways. Continued litigation over opioid marketing drives diversification toward non-addictive modalities, inflating demand for neuromodulation and non-opioid analgesics. Medicaid expansion in additional U.S. states during 2025 further widens patient pools for comprehensive pain management programs.

Europe displays balanced maturation; Western states sustain incremental gains while Eastern markets accelerate device adoption under EU cohesion funding. The European Medicines Agency's rolling review procedures shortened average approval times for biosimilars and novel analgesics by 15% in 2025. National health technology assessment bodies increasingly recognize quality-of-life outcomes, prompting broader reimbursement for validated neuromodulation indications.

Asia-Pacific delivers the fastest regional CAGR at 10.55% through 2031. China's Healthy 2030 blueprint earmarks chronic pain as a priority, enabling tier-two hospitals to establish specialty pain clinics. India's telemedicine guidelines passed in 2025 legitimize e-prescriptions of non-schedule drugs, spurring digital consultation platforms. However, uneven insurance penetration and fragmented provider markets still limit uptake of high-cost implantables, constraining absolute market size relative to demographic potential.

- Abbott Laboratories

- Baxter

- Beckton Dickinson

- Boston Scientific

- Endo International

- Fresenius

- Grunenthal GmbH

- Hikma Pharmaceuticals

- Hisamitsu Pharmaceutical

- Insulet

- Johnson & Johnson (DePuy Synthes, Ethicon)

- Medtronic

- Nevro

- Novartis

- OMRON

- Pfizer

- Smiths Group

- Stryker

- Terumo

- Teva Pharmaceutical Industries

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Ageing-Related Rise in Chronic Pain Prevalence

- 4.2.2 Clinical Validation of Neuro-Modulation Efficacy

- 4.2.3 Shift Toward Opioid-Sparing Multimodal Protocols

- 4.2.4 Rapid ASC Adoption for Pain Procedures

- 4.2.5 Venture Funding for Closed-Loop Stimulation Platforms

- 4.2.6 AI-Driven, Patient-Specific Dosing Algorithms

- 4.3 Market Restraints

- 4.3.1 High CAPEX/OPEX for Implantable Devices

- 4.3.2 Limited Reimbursement in Emerging Markets

- 4.3.3 Cyber-Security Risks in Connected Pumps

- 4.3.4 ESG Scrutiny on Opioid Manufacturers

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Mode of Pain Management

- 5.1.1 Drugs

- 5.1.1.1 Opioids

- 5.1.1.2 Non-narcotic Analgesics

- 5.1.1.2.1 NSAIDs

- 5.1.1.2.2 Anesthetics

- 5.1.1.2.3 Anticonvulsants

- 5.1.1.2.4 Antidepressants

- 5.1.2 Devices

- 5.1.2.1 Neuro-modulation Devices

- 5.1.2.1.1 TENS

- 5.1.2.1.2 Spinal Cord Stimulation (SCS)

- 5.1.2.1.3 Dorsal Root Ganglion (DRG)

- 5.1.2.1.4 Vagus & Peripheral Nerve Stimulators

- 5.1.2.2 Analgesic Infusion Pumps

- 5.1.2.2.1 Intrathecal Pumps

- 5.1.2.2.2 External PCA Pumps

- 5.1.2.3 Radio-frequency Ablation Systems

- 5.1.2.1 Neuro-modulation Devices

- 5.1.1 Drugs

- 5.2 By Application

- 5.2.1 Neuropathic Pain

- 5.2.2 Cancer Pain

- 5.2.3 Musculoskeletal Pain

- 5.2.4 Facial Pain & Migraine

- 5.2.5 Post-operative & Acute Pain

- 5.3 By Setting of Care

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgical Centers

- 5.3.3 Home-care & Remote Monitoring

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 Baxter International Inc.

- 6.3.3 Becton, Dickinson and Company

- 6.3.4 Boston Scientific Corporation

- 6.3.5 Endo International plc

- 6.3.6 Fresenius SE & Co. KGaA

- 6.3.7 Grunenthal GmbH

- 6.3.8 Hikma Pharmaceuticals

- 6.3.9 Hisamitsu Pharmaceutical

- 6.3.10 Insulet Corporation

- 6.3.11 Johnson & Johnson (DePuy Synthes, Ethicon)

- 6.3.12 Medtronic plc

- 6.3.13 Nevro Corp.

- 6.3.14 Novartis AG

- 6.3.15 Omron Healthcare

- 6.3.16 Pfizer Inc.

- 6.3.17 Smiths Medical (ICU Medical)

- 6.3.18 Stryker Corporation

- 6.3.19 Terumo Corporation

- 6.3.20 Teva Pharmaceutical Industries

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment