|

시장보고서

상품코드

1910503

오프로드 차량 시장 : 점유율 분석, 업계 동향, 통계, 성장 예측(2026-2031년)Off-road Vehicle - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

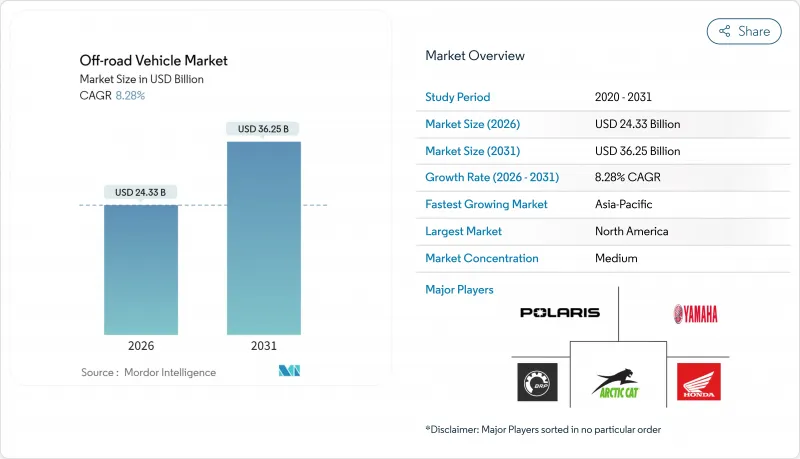

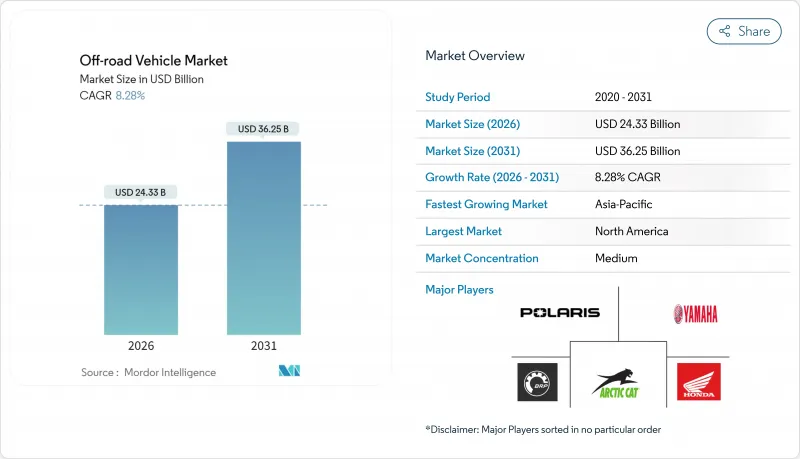

2026년 오프로드 차량 시장 규모는 243억 3,000만 달러로 추정되며, 2025년 224억 7,000만 달러에서 성장한 수치입니다. 2031년에는 362억 5,000만 달러에 이르고, 2026년부터 2031년까지 CAGR은 8.28%를 나타낼 전망입니다.

이 성장은 아웃도어 레크리에이션 참가자 증가, 전동화의 가속, 유틸리티 용도의 확대가 함께 발생하고 있으며, 주요 제조업체간의 주기적인 수익 변동을 상쇄하고 있습니다. 트레일 인프라에 대한 자금 투입 증가, 정밀 농업 도입 확대, 군사 기동성 근대화 프로그램이 수요 기반을 더욱 확대하는 한편, 전동 파워 스티어링(EPS), 텔레매틱스, 첨단 서스펜션 시스템을 중심으로 한 기술 융합이 소비자 및 상업 바이어 모두에 대한 가치 제안을 강화하고 있습니다. 2024년 주요 공급업체에서 수익이 축소되었음에도 불구하고 오프로드 차량 시장은 전기 모델에 대한 다양화, 특수 방위 계약, 구독형 연결 서비스로의 전개를 통해 탄력성을 보여 장기적인 수익원을 확고히 하고 있습니다.

세계 오프로드 차량 시장 동향과 인사이트

야외 레크리에이션 관광 급증

2024년 아웃도어레크리에이션은 미국 GDP에 1조 2,000억 달러(국내총생산의 2.3%에 상당)를 공헌해 다수의 고용을 지원했습니다. 참가자 증가에 따라, 트레일 주행이나 오버랜딩용의 ATV 및 UTV 구입이 촉진되었습니다. 같은 해 오토바이와 ATV는 경제 부가가치의 대부분을 창출해 오프로드 차량 시장에서의 강한 수요를 뒷받침하고 있습니다. 주 조성 프로그램이 효과를 증폭 : 콜로라도의 야외 레크리에이션 기금은 액세스 프로젝트에 엄청난 자금을 배분하고 오레곤의 매칭 보조금은 지방 제조 클러스터를 육성했습니다. 트레일 시스템은 강력한 파급 효과를 만들어냅니다. 미네소타 주 스노모빌 네트워크는 일년 내내 많은 수의 관광 수입을 창출하고 지역 경제에 대한 승수 효과를 강화하고 계절 차량 판매를 안정화시키고 있습니다.

방위기관에 의한 전술용 ATV/UTV 조달

방위기관은 국경경비, 특수작전, 어려운 지형에 있어서의 군수활동을 위한 경량기동자산을 요구하고 있습니다. 인도가 최근에 실시 예정인 북부 국경용 입찰에서는 전술적 유연성을 극대화하기 위해 헬리콥터 매달기 능력, 4인승 레이아웃, 자율 항행 옵션이 명기되어 있습니다. 핀란드가 주도하는 유럽의 FAMOUS 프로그램은 -46℃에서의 시동 내성과 용융기의 수륙 양용 기능을 갖춘 차량에 의한 북극권에서의 운용성에 초점을 맞추었습니다. 미국은 매년 일정액을 할당해, 공차 중량 4,500 파운드(약 2,041 kg) 이하, 항속 거리 250 마일(약 402 km)을 요건으로 하는 초경량 전투 차량(ULCV)의 조달을 진행하고 있습니다. 이러한 복수 프로그램의 추진에 의해 벤더 각 사는 장갑 키트, 대드론 센서 및 하이브리드 파워트레인을 탑재 가능한 모듈러 섀시의 개발을 촉진합니다. 민간 수요의 주기적인 변동에도 불구하고 수주 잔고를 견고하게 유지하고 있습니다.

전동 파워트레인용 리튬 공급망의 박박

현재 중국은 세계 리튬 정제의 5분의 3 이상, 배터리 제조의 5분의 4를 담당하고 있으며, 수요 급증에 따라 세계 OEM 제조업체는 위험에 노출되고 있습니다. 미국은 인플레이션 억제법에 따라 국내 가공에 대한 자금을 배분했지만, 허가 취득의 장벽이나 지역사회의 우려에 의해 광산 개설이 늦어지고 있습니다. 전기화학적 추출기술의 신흥기업은 환경부하가 낮은 해결책을 약속하고 있지만 아직 상업화 전 단계입니다. 공급원의 다양화가 실현될 때까지는 전지 가격의 변동이 계속될 가능성이 있으며, 특히 가격에 민감한 개발 도상 시장에서 전기식 ATV의 보급을 가속시키는 총 비용의 균형(TCO 패리티) 달성을 제약할 우려가 있습니다.

부문 분석

2025년 탑승자 수용력, 적재 기능, 서스펜션 성능을 융합한 UTV 및 사이드 바이 사이드는 오프로드 차량 시장 점유율의 50.68%를 차지했습니다. 레크리에이션, 농업 및 방위 주문 수요에 힘입어 해당 부문은 견고한 시장 규모를 달성하고 있습니다. 전기식 UTV 파생 모델은 현재 8.32%라는 가장 빠른 CAGR을 기록하고 있습니다. 이는 OEM 제조업체가 15kWh 배터리 팩을 도입하여 최고 속도 80km/h, 충전 시간 3시간 미만을 실현하고 있기 때문입니다.

전지형 대응차(ATV) 수요는 차폭 제한이 엄격하고 좁은 폭 섀시가 유리한 지역에서 견고하게 추이하고 있습니다. 한편, 수륙 양용차나 스노모빌 등 틈새 플랫폼에 대한 수요는 기후 조건이 가혹한 지역에서 지속되고 있습니다. 경쟁 차별화는 조정 가능한 서스펜션, 폴라리스의 동적 라이브 밸브 구조 및 터치 스크린 라이드 명령 시스템을 통한 캐빈 디지털화에 의존합니다. 따라서 차종 포트폴리오는 기존의 내연기관(ICE)의 생산량과 신흥의 전동화 성장축의 밸런스를 취하여 추진 시스템에 관한 불확실성에 대한 헤지를 가능하게 하고 있습니다.

스포츠 레크리에이션 분야는 2025년 시점에서 오프로드 차량 시장의 41.05%를 차지해 수백만의 미국인이 아웃도어 활동에 참가하는 기록적인 트레일 이용의 혜택을 받고 있습니다. 군·법 집행기관용 수요는 헬리콥터 매달림 대응의 경량 전술 이동 수단이나 하이브리드 정음 감시 모드를 요구하는 조달 기관에 의해 CAGR8.35%로 확대가 전망됩니다.

농업 및 임업 분야에서는 PTO 구동 작업기를 탑재한 중배기량 UTV가 채택되어 건설회사는 원격지물류용으로 고적재 유닛을 조달합니다. 가이드 첨부 오버랜딩 원정이라는 신규 관광 컨셉이 이용 사례를 더욱 확대. 따라서 다목적 적응성은 소비자의 선택적 지출이 감소하더라도 기본 판매량을 유지합니다.

2025년 시점에서 내연 기관은 오프로드 차량 시장 점유율의 83.05%를 차지하고 있으며, 이는 연료 공급 인프라의 보급과 성숙한 공급망에 의해 지원되고 있습니다. 한편 배터리 전기자동차 모델은 정책 추진과 배터리 비용 저하를 반영하여 8.30%라는 가장 높은 CAGR을 기록하고 있습니다.

하이브리드식 레인지 익스텐더는 10kWh 팩과 콤팩트 발전기를 결합하여 저속 토크를 손상시키지 않고 가동 시간을 연장하여 고객의 불안을 해소합니다. 수소연료전지 프로토타입은 연구개발 단계이지만, 한랭지에서의 신속한 연료 보급을 필요로 하는 대형 구조 차량의 길을 보여줍니다. 추진 시스템의 다양화는 규제 위험을 줄이는 동시에 배터리 임대와 재활용을 중심으로 새로운 공급업체 생태계를 창출합니다.

지역별 분석

북미는 2025년 오프로드 차량 시장 점유율의 37.84%를 차지했습니다. 이것은 야외 레크리에이션의 GDP 기여도와 주 보조금의 광범위한 트레일 네트워크를 기반으로합니다. 스노우 벨트 지역의 주들은 관광 수입을 자극하는 정비 프로그램에 연간 거액을 투자. 위스콘신주와 알래스카주는 대상 트레일 유지비의 100%를 보조하여 경기감속기에도 안정된 수요를 지지했습니다. 딜러 금융 제휴(예: 셰필드 금융 및 폴라리스 계약 갱신)는 구매자의 대출 액세스를 용이하게 하고 쇼룸의 판매 회전율을 유지합니다. 그러나 캐나다 각 주의 보호 구역 규제는 운영상의 복잡성을 일으키고 OEM 제조업체는 허가 기준을 충족하기 때문에 정숙성이 높은 파워트레인 및 배출가스 규제 적합 엔진공급을 강요받고 있습니다.

아시아태평양은 2031년까지 8.42%라는 가장 빠른 CAGR을 달성할 전망입니다. 도시화가 진행되는 중산계급 소비자가 아웃도어 라이프 스타일 브랜드를 받아들여 정부가 지방의 교통망 정비에 자금을 투입하고 있기 때문입니다. 인도의 ATV 판매는 어드벤처 관광의 마케팅과 농업 기계화의 추진으로 크게 증가했습니다. CFMOTO와 같은 지역 OEM 제조업체는 수직 통합 공급망을 활용하여 경쟁력 있는 가격 설정을 실현하고 수출 계약을 획득함과 동시에 세계 시장 점유율의 5분의 2를 차지하고 있습니다.

유럽의 성장은 늦었지만, 규제의 추진은 전동화의 요구와 일치하고 있습니다. 비도로기계용 스테이지 V 배출가스 규제로 후처리장치 및 대체 파워트레인에 대한 연구개발비가 증가하여 간접적으로 하이브리드 및 연료전지 컨셉의 혁신을 촉진하고 있습니다. 2028년 시행의 신 NRMM규칙에서는 소규모 생산 기준을 70대로 설정해 신흥전기자동차 제조업체가 인증 취득을 용이하게 할 수 있는 길을 열었습니다. 북유럽 국가에서는 관광 진흥을 위해 장기적인 트레일 유지 보조금을 도입하고 있으며, 독일과 오스트리아가 알프스 지역에 대해서도 유사한 시책을 검토 중입니다. 그 결과, 규제 대응 부담이 단기적인 판매 대수를 억제하는 한편, 장기적인 수요는 저배출 모델로 이행하고, 유럽 공급자는 프리미엄 가격 설정을 통해 투자 회수가 가능해집니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 야외 레크리에이션 관광의 급증

- 방위기관에 의한 전술용 ATV/UTV 조달

- 중소규모 농장의 급속한 기계화

- 첨단 전동 파워 스티어링(EPS) 및 텔레매틱스 채택

- 드론 촬영용 저소음 전동 ATV 수요

- 북유럽의 트레일 유지 보조금이 확대되는 라이딩 네트워크

- 시장 성장 억제요인

- 높은 초기 비용 및 생애 주기 비용

- 전기 파워트레인용 리튬 공급망의 부족 현상

- 부상 관련 규제 강화 및 속도 제한 도입

- 보호 구역에서의 사용 금지

- 가치/공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측(금액(달러) 및 수량(단위))

- 차량 유형별

- 전지형 대응차(ATV)

- 유틸리티 태스크 차량(UTV)/사이드 바이 사이드

- 더트 및 오프로드 바이크

- 스노모빌

- 수륙양용 및 특수 오프로드차

- 용도별

- 스포츠 및 레크리에이션

- 농업 및 임업

- 산업 및 건설

- 군사 및 법 집행 기관

- 기타 상용(관광, 수색 및 구조)

- 추진 유형별

- 내연기관(가솔린/디젤)

- 하이브리드

- 배터리 전기자동차

- 수소 연료전지

- 엔진 배기량별(cc)

- 400cc 미만

- 400-800cc

- 800cc 이상

- 출력(kW)별

- 50kW 미만

- 50-100kW

- 100kW 초과

- 드라이브 유형별

- 이륜 구동

- 사륜구동 / 전륜 구동

- 좌석수별

- 1인 탑승

- 2인 탑승

- 3인 이상 탑승

- 지역별

- 북미

- 미국

- 캐나다

- 기타 북미

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 프랑스

- 영국

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 이집트

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Polaris Inc.

- Bombardier Recreational Products Inc.(Can-Am)

- Yamaha Motor Corp.

- Textron Inc.(Arctic Cat)

- Kawasaki Heavy Industries Ltd.

- Suzuki Motor Corp.

- Honda Motor Co. Ltd.

- CFMOTO Powersports Inc.

- Kwang Yang Motor Co. Ltd. (Kymco)

- American LandMaster

- Tracker Off-Road(Bass Pro Shops)

- Kubota Corp.(RTV)

- John Deere(Gator)

- Mahindra & Mahindra Ltd.

- Segway Powersports

- Hisun Motors Corp.

- Linhai Group

- TGB(Taiwan Golden Bee)

- DRR USA

제7장 시장 기회와 장래의 전망

SHW 26.01.26Off-road Vehicle Market size in 2026 is estimated at USD 24.33 billion, growing from 2025 value of USD 22.47 billion with 2031 projections showing USD 36.25 billion, growing at 8.28% CAGR over 2026-2031.

This growth arises from a confluence of rising outdoor recreation participation, accelerating electrification, and expanding utility applications that continue to offset cyclical revenue fluctuations among leading manufacturers. Growing trail infrastructure funding, precision-farming uptake, and military mobility modernization programs further widen demand pools, while technology convergence around electronic power steering (EPS), telematics, and advanced suspension systems enhances value propositions for both consumer and commercial buyers. Even with revenue contractions at major suppliers during 2024, the off-road vehicle market shows resilience through diversification into electric variants, specialty defense contracts, and subscription-based connectivity services that solidify long-term revenue streams.

Global Off-road Vehicle Market Trends and Insights

Surge In Outdoor Recreational Tourism

Outdoor recreation contributed USD 1.2 trillion to U.S. GDP in 2024, equal to 2.3% of national output and supporting multiple jobs. Participation increased, spurring ATV and UTV purchases for trail riding and overlanding. In 2024, motorcycling and ATVing generated a large share of value-added economic output, underscoring strong demand in the off-road vehicle market. State grant programs amplify the effect: Colorado's Outdoor Recreation Fund distributed a massive amount to access projects, while Oregon's matching grants nurtured rural manufacturing clusters. Trail systems create powerful spillovers; Minnesota's snowmobile network generates significant annual tourism revenue, reinforcing the sector's multiplier effect on local economies and stabilizing seasonal vehicle sales.

Tactical ATV/UTV Procurement By Defense Forces

Defense agencies seek light mobility assets for border patrol, special operations, and logistics in difficult terrain. India's upcoming northern-border tender specifies helicopter-sling capability, four-seat layouts, and autonomous navigation options to maximize tactical flexibility. Europe's FAMOUS program, coordinated by Finland, focuses on Arctic operability with vehicles tolerating -46 °C start-up and amphibious functionality for thaw periods. The United States allocates some amount annually to acquire Ultra-Light Combat Vehicles with 4,500-pound curb-weight caps and 250-mile range requirements. Such multi-program momentum encourages vendors to develop modular chassis that accept armor kits, counter-drone sensors, and hybrid powertrains, strengthening order backlogs despite civilian cyclical swings.

Lithium Supply-Chain Crunch For E-Powertrains

China currently refines more than three-fifths of global lithium and fabricates four-fifths of batteries, creating exposure for global OEMs as demand surges. The United States allocated funding under the Inflation Reduction Act for domestic processing, but permitting hurdles and community concerns are delaying mine openings. Electro-chemical extraction startups promise lower-impact solutions yet remain pre-commercial. Until diversified supply materializes, battery prices may remain volatile, constraining the total-cost parity that accelerates electric ATV adoption, particularly in price-sensitive developing markets.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Mechanization Of Midsize Farms

- Adoption Of Advanced EPS & Telematics

- Rising Injury-Related Regulations & Speed Caps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

UTVs and side-by-sides captured 50.68% of the off-road vehicle market share in 2025 by blending passenger capacity, cargo utility, and suspension sophistication. The segment reached a robust level of off-road vehicle market size, buoyed by recreation, agriculture, and defense orders. Electric UTV derivatives now post the fastest 8.32% CAGR as OEMs introduce 15 kWh battery packs delivering 80 km/h top speed and sub-3-hour recharge cycles.

Demand for all-terrain vehicles (ATVs) remains robust in regions with strict width restrictions that favor narrower chassis. In contrast, niche demand for amphibious and snowmobile platforms persists where climatic extremes prevail. Competitive differentiation hinges on adjustable suspension, Polaris's DYNAMIX live valve architecture, and cabin digitization through touchscreen ride-command systems. The vehicle-type portfolio, therefore, balances legacy ICE volumes against emerging electric growth vectors, enabling OEMs to hedge against propulsion uncertainty.

Sports and recreation account for 41.05% of the off-road vehicle market in 2025, benefiting from record trail participation as millions of Americans venture outdoors. Military and law enforcement demand will escalate at an 8.35% CAGR as procurement agencies seek light tactical mobility with helicopter-sling compatibility and hybrid silent-watch modes.

Agriculture and forestry absorb mid-displacement UTVs outfitted with PTO-driven implements, while construction firms requisition high-payload units for remote-site logistics. Emerging tourism concepts such as guided overlanding expeditions further widen commercial use cases. Multi-role adaptability, therefore, sustains baseline volumes even when consumer discretionary spending dips.

Internal-combustion engines commanded 83.05% of the off-road vehicle market share in 2025, backed by ubiquitous fueling infrastructure and mature supply chains. Battery-electric models, however, record the steepest 8.30% CAGR, reflecting policy push and falling cell costs.

Hybrid range-extender concepts bridge customer anxiety by pairing 10 kWh packs with compact generators, extending runtime without compromising low-speed torque. Hydrogen fuel-cell prototypes remain R&D efforts but signal pathways for heavy-duty rescue fleets requiring rapid cold-weather refueling. Propulsion diversification mitigates regulatory risks while inviting new supplier ecosystems around battery leasing and recycling.

The Off-Road Vehicle Market Report is Segmented by Vehicle Type (All-Terrain Vehicles and More), Application (Sports & Recreation and More), Propulsion Type (Internal-Combustion and More), Engine Displacement (Less Than 400 Cc and More), Power Output (Less Than 50 KW and More), Drive Type (2-Wheel Drive and More), Seating Capacity, and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

North America secured 37.84% of off-road vehicle market share in 2025, underpinned by the outdoor recreation GDP contribution and extensive trail networks subsidized by state grants. Snowbelt states invested huge amount annually in grooming programs that stimulated in tourism receipts, while Wisconsin and Alaska reimbursed 100% of eligible trail maintenance costs, anchoring steady demand even during economic slowdowns. Dealer financing partnerships, such as Sheffield Financial's renewal with Polaris, ease credit access for buyers and sustain showroom turnover. Nevertheless, conservation-area restrictions across Canadian provinces introduce operational complexity, nudging OEMs to supply quieter powertrains and emission-compliant engines to satisfy permitting criteria.

Asia-Pacific delivers the fastest 8.42% CAGR through 2031 as urbanizing middle-class consumers embrace outdoor lifestyle brands and governments fund rural connectivity. India's ATV sales grew drastically which was supported by adventure-tourism marketing and agricultural mechanization drives. Regional OEMs such as CFMOTO leverage vertically integrated supply chains to offer competitive pricing, enabling them to capture export contracts and reach two-fifth global market share.

Europe's growth lags but regulatory thrust aligns with electrification imperatives. Stage V emission norms for non-road machinery elevate R&D spending on after-treatment and alternative powertrains, indirectly spurring innovation in hybrid and fuel-cell concepts. New NRMM rules effective 2028 set small-series thresholds of 70 units, granting boutique electric startups manageable certification pathways. Nordic countries deploy long-run trail-maintenance subsidies to catalyze tourism, a template that Germany and Austria now evaluate for alpine regions. Consequently, although compliance burdens restrain short-term volumes, long-term demand will pivot toward low-emission models, allowing European suppliers to recoup investments through premium pricing.

- Polaris Inc.

- Bombardier Recreational Products Inc. (Can-Am)

- Yamaha Motor Corp.

- Textron Inc. (Arctic Cat)

- Kawasaki Heavy Industries Ltd.

- Suzuki Motor Corp.

- Honda Motor Co. Ltd.

- CFMOTO Powersports Inc.

- Kwang Yang Motor Co. Ltd. (Kymco)

- American LandMaster

- Tracker Off-Road (Bass Pro Shops)

- Kubota Corp. (RTV)

- John Deere (Gator)

- Mahindra & Mahindra Ltd.

- Segway Powersports

- Hisun Motors Corp.

- Linhai Group

- TGB (Taiwan Golden Bee)

- DRR USA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge In Outdoor Recreational Tourism

- 4.2.2 Tactical ATV/UTV Procurement By Defense Forces

- 4.2.3 Rapid Mechanization Of Midsize Farms

- 4.2.4 Adoption Of Advanced EPS & Telematics

- 4.2.5 Demand For Low-Noise E-Atvs For Drone Cinematography

- 4.2.6 Nordic Trail-Maintenance Subsidies Expanding Riding Networks

- 4.3 Market Restraints

- 4.3.1 High Upfront & Lifecycle Costs

- 4.3.2 Lithium Supply-Chain Crunch For E-Powertrains

- 4.3.3 Rising Injury-Related Regulations & Speed Caps

- 4.3.4 Conservation-Area Usage Bans

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Vehicle Type

- 5.1.1 All-Terrain Vehicles (ATV)

- 5.1.2 Utility Task Vehicles (UTV) / Side-by-Sides

- 5.1.3 Dirt / Off-road Motorcycles

- 5.1.4 Snowmobiles

- 5.1.5 Amphibious & Specialty ORVs

- 5.2 By Application

- 5.2.1 Sports & Recreation

- 5.2.2 Agriculture & Forestry

- 5.2.3 Industrial & Construction

- 5.2.4 Military & Law-Enforcement

- 5.2.5 Other Commercial (tourism, search-and-rescue)

- 5.3 By Propulsion Type

- 5.3.1 Internal-Combustion (Gasoline / Diesel)

- 5.3.2 Hybrid

- 5.3.3 Battery-Electric

- 5.3.4 Hydrogen Fuel-Cell

- 5.4 By Engine Displacement (cc)

- 5.4.1 Less than 400 cc

- 5.4.2 400 - 800 cc

- 5.4.3 More than 800 cc

- 5.5 By Power Output (kW)

- 5.5.1 Less than 50 kW

- 5.5.2 50 - 100 kW

- 5.5.3 More than 100 kW

- 5.6 By Drive Type

- 5.6.1 2-Wheel Drive

- 5.6.2 4-Wheel / All-Wheel Drive

- 5.7 By Seating Capacity

- 5.7.1 1 Rider

- 5.7.2 2 Riders

- 5.7.3 More than or equal to 3 Passengers

- 5.8 By Geography

- 5.8.1 North America

- 5.8.1.1 United States

- 5.8.1.2 Canada

- 5.8.1.3 Rest of North America

- 5.8.2 South America

- 5.8.2.1 Brazil

- 5.8.2.2 Argentina

- 5.8.2.3 Rest of South America

- 5.8.3 Europe

- 5.8.3.1 Germany

- 5.8.3.2 France

- 5.8.3.3 United Kingdom

- 5.8.3.4 Italy

- 5.8.3.5 Spain

- 5.8.3.6 Russia

- 5.8.3.7 Rest of Europe

- 5.8.4 Asia-Pacific

- 5.8.4.1 China

- 5.8.4.2 Japan

- 5.8.4.3 India

- 5.8.4.4 South Korea

- 5.8.4.5 Australia

- 5.8.4.6 Rest of Asia-Pacific

- 5.8.5 Middle East and Africa

- 5.8.5.1 United Arab Emirates

- 5.8.5.2 Saudi Arabia

- 5.8.5.3 Turkey

- 5.8.5.4 Egypt

- 5.8.5.5 South Africa

- 5.8.5.6 Rest of Middle East and Africa

- 5.8.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Polaris Inc.

- 6.4.2 Bombardier Recreational Products Inc. (Can-Am)

- 6.4.3 Yamaha Motor Corp.

- 6.4.4 Textron Inc. (Arctic Cat)

- 6.4.5 Kawasaki Heavy Industries Ltd.

- 6.4.6 Suzuki Motor Corp.

- 6.4.7 Honda Motor Co. Ltd.

- 6.4.8 CFMOTO Powersports Inc.

- 6.4.9 Kwang Yang Motor Co. Ltd. (Kymco)

- 6.4.10 American LandMaster

- 6.4.11 Tracker Off-Road (Bass Pro Shops)

- 6.4.12 Kubota Corp. (RTV)

- 6.4.13 John Deere (Gator)

- 6.4.14 Mahindra & Mahindra Ltd.

- 6.4.15 Segway Powersports

- 6.4.16 Hisun Motors Corp.

- 6.4.17 Linhai Group

- 6.4.18 TGB (Taiwan Golden Bee)

- 6.4.19 DRR USA

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment