|

시장보고서

상품코드

1911425

산업용 패스너 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Industrial Fasteners - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

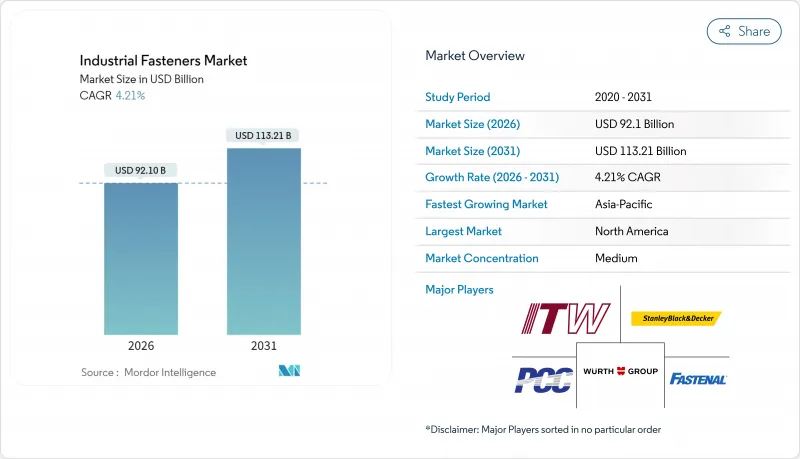

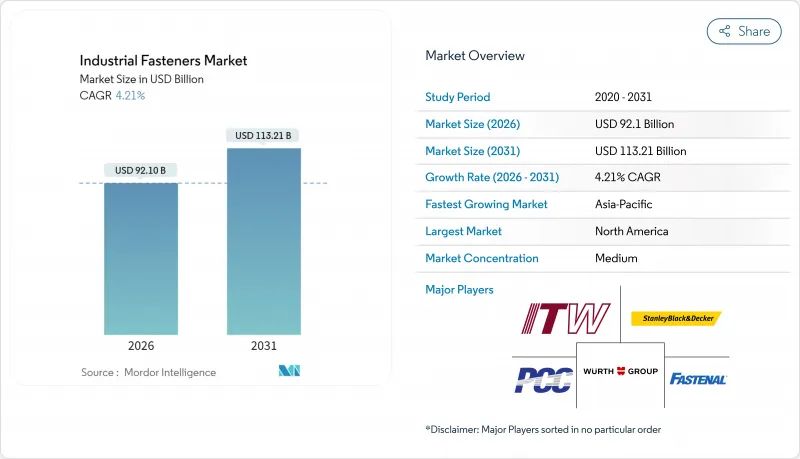

산업용 패스너 시장은 2025년 883억 8,000만 달러에서 2026년에는 921억 달러에 이를 것으로 예측됩니다. 2026-2031년에 걸쳐 CAGR 4.21%로 성장을 지속하여 2031년까지 1,132억 1,000만 달러에 달할 전망입니다.

제조 자동화, 중장비 업그레이드, 정밀 조립 요구사항이 복잡한 장비 전반에 걸쳐 신뢰할 수 있는 고강도 접합부를 필요로 함에 따라 수요가 뒷받침되고 있습니다. 인더스트리 4.0 플랫폼 도입은 토크 및 예압 데이터를 수집하는 스마트 센서 장착 패스너 사용을 가속화하여 제조업체의 가동 중단 시간 단축과 추적성 향상에 기여하고 있습니다. 리쇼어링 및 현지화 전략은 리드 타임을 단축하고 세계의 물류 위험 노출을 줄여 산업용 패스너 시장을 강화하고 있습니다. 한편, 아시아와 북미 지역의 인프라 갱신 및 산업 역량 확장에 대한 투자 증가로 구조용 및 특수 제품에 대한 대량 주문이 꾸준히 이어지고 있습니다.

세계의 산업용 패스너 시장 동향 및 인사이트

정밀 마이크로 패스너가 필요한 산업용 자동화 장비

전자, 의료 기기 및 반도체 공장은 이제 1그램도 채 되지 않는 무게이지만 1초 미만의 사이클 시간으로 반복적인 클램프 하중을 전달해야 하는 마이크로 나사를 지정하고 있습니다. JR Automation과 같은 통합업체들은 마이크론 단위의 배치 정밀도를 보고하며, 이는 맞춤형 체결 기하학 구조, 1 N*m 미만의 토크, 그리고 빠른 부하 사이클에서 갈림 현상을 완화하는 고급 코팅에 대한 수요를 촉진합니다. 전동 공구 공급업체들은 모든 조임 이벤트를 기록하고 MES 대시보드에 무선으로 데이터를 전송하는 무선 트랜스듀서 제어 렌치로 대응하고 있으며, 이는 Panasonic의 AccuPulse 플랫폼에서 선보인 기능입니다. 제조업체들은 재작업 스테이션 감소 및 택트 타임 단축 등 즉각적인 품질-비용 이점을 언급하며, 대량 자동화 라인에서의 산업용 패스너 시장 성장세를 강화하고 있습니다. 더 많은 공장이 디지털화됨에 따라, 설계자들은 추적성을 위한 ID 칩이 통합되고 볼 피더를 통해 걸림 없이 공급될 수 있는 패스너를 점점 더 요구하고 있습니다. 이 추세는 이미 전자제품에서 자동차 배터리 모듈 및 협동 로봇 조인트로 확산되어 향후 2년간 지속적인 성장을 보장하고 있습니다.

제조업의 회귀가 국내 산업용 패스너 수요 주도

지정학적 불확실성과 팬데믹 시대의 항만 혼잡으로 인해 미국 및 EU OEM 업체들은 단가뿐만 아니라 총 도착 비용을 재평가하게 되었습니다. 현재 미국에서 소비되는 패스너의 약 3분의 2가 국내에서 생산되며, 이는 10년 전 관찰된 해외 생산 추세와 정반대입니다. 현지 공급업체들은 보다 긴밀한 엔지니어링 협력, 낮은 재고 완충 효과, 공공 인프라 수주에 포함된 ‘미국산 구매 조항(Buy-America clauses)’ 준수의 혜택을 누리고 있습니다. 지역 작업장과 다국적 기업 모두에서 냉간 성형 라인, 열처리로, 자동 분류 셀에 대한 자본 투자가 가속화되면서 산업용 패스너 시장 전반의 가동률이 상승하고 있습니다. 인건비는 아시아보다 여전히 높지만, OEM들은 운송비 절감과 노후화 위험 감소가 결정적인 장점이라고 언급합니다. 리쇼어링 동향은 특히 단축 공급망에 유리한 중-고강도 등급을 중심으로 2028년까지 시장 규모에 긍정적 추동력을 유지할 것으로 전망됩니다.

기존의 산업용 패스너를 대체하는 첨단 접합 기술

대량 생산 장비 제조사들은 영구적 접합이 허용되는 인클로저 및 섀시에 구조용 접착제, 레이저 용접, 마찰 교반 용접을 시험 적용 중입니다. 리벳이나 볼트와 접착제 필렛을 결합한 하이브리드 설계는 부품 수를 줄이고 하중 분배를 개선하여 일부 OEM이 조립체당 기계식 패스너 사용량을 줄이도록 유도하고 있습니다. 알루미늄 압출 제조업체들은 경량 프레임에 마찰 교반 용접을 도입하는 데 특히 적극적이어서 특정 응용 부문에서 볼트 소비량을 감소시키고 있습니다. 그럼에도 펌프, 기어박스, 공정 밸브 어셈블리 등 유지보수가 빈번한 환경에서는 여전히 분리 가능한 접합부가 필요하여 산업용 패스너 시장의 핵심 기반을 유지하고 있습니다. 향후 3년간 이 억제요인의 실제 영향력은 분리 가능성과 무게 절감 사이의 균형에 의해 결정될 것입니다.

부문 분석

금속 패스너는 2025년 수익의 91.45%를 차지하고 중장비, 산업용 로봇, 프레스 라인에서는 800MPa를 넘는 인장 강도가 요구되었습니다. AISI 316과 같은 스테인리스 스틸 등급은 내식성이 최우선인 식품 가공 및 의약품 오토클레이브에서 프리미엄 틈새 시장을 획득하고 있습니다. 합금강 및 탄소강 볼트는 구조 프레임, 기어박스 케이싱, 노 도어에서 표준 옵션으로 산업용 패스너 시장을 계속 지원하고 있습니다. 티타늄 및 니켈 합금 특수품은 터빈 하우징이나 석유화학 반응기에 사용되고 있습니다만, 스폰지 생산에 따른 공급 제약에 의해 납기 연장이 주기적으로 발생하고 있습니다. 이러한 동향이 성숙 시장이면서도 신흥국에서의 생산 능력 확대에 의한 점증적 성장을 계속하는 금속 부문의 기반이 되고 있습니다.

플라스틱 패스너는 전체 물량의 8.55%에 불과하지만 2031년까지 연평균 6.72% 성장률로 빠르게 확대되고 있습니다. 나일론 나사는 이제 PLC 캐비닛과 LED 드라이버 하우징에서 절연 강도와 화학적 불활성으로 가치를 더하며 일상적으로 사용됩니다. 폴리카보네이트 클립은 충격에 강하고 수명 종료 시 재활용이 용이해 AGV 차량의 센서 모듈을 고정하는 데 활용됩니다. 스마트 미터 어셈블리용 경량 인클로저 수요 급증은 폴리머 채택을 더욱 촉진합니다. 클린룸 산업 전반에 자동화가 확산되면서 엔지니어들은 입자 발생을 차단하기 위해 PVDF 및 PEEK 패스너를 선택하고 있습니다. 이에 따라 플라스틱 계열 산업용 패스너 시장 규모는 2031년까지 97억 달러에 근접할 전망이며, 이는 소재 포트폴리오 전반에 걸친 명확한 다각화 추세를 보여줍니다.

외부 나사 제품(볼트, 나사, 스터드)은 2025년 산업용 패스너 시장 수익의 44.30%를 차지했습니다. M24 직경을 초과하는 볼트는 크레인, 프레스 및 압출기 어셈블리에서 주류이며 M6 미만의 기계 나사는 서보 모터 마운트 및 선형 액추에이터를 고정하는 데 사용됩니다. 이 부문은 국제표준화기구(ISO)의 규격통일의 혜택을 누리고 있으며, 다국적 OEM 제조업체의 재고관리 전략을 간소화하고 있습니다. 호환성은 린 생산을 지원하는 자동 빈 충전 시스템도 뒷받침해 산업용 패스너 시장에서 대량 생산의 성장을 강화하고 있습니다.

항공우주 등급 패스너는 출하량에서 차지하는 비중은 작지만 연평균 5.88%의 성장률을 보이고 있습니다. 산업용 가스 터빈 및 고정밀 공작기계에서 초합금 볼트는 650°C를 초과하는 주기적 열 부하를 견딥니다. 선행 토크 너트가 장착된 섕크 그립 볼트와 같은 진동 저항형 구성은 항공우주 부문의 가치를 고주기 프레스 슬라이드로 이전합니다. 방위 계약이 증가함에 따라 NADCAP 인증 열처리 및 실험실 시설을 보유한 공급업체들은 프리미엄 가격을 적용받고 있습니다. 항공우주 등급 제품군의 산업용 패스너 시장 규모는 2031년까지 15억 3,000만 달러가 추가될 것으로 예상되며, 이는 임무 핵심 산업 환경에서 고성능 접합부의 광범위한 수용을 반영합니다.

지역별 분석

아시아는 2025년 세계의 매출의 44.60%를 차지했으며, 중국, 인도 및 아세안 국가들의 제조업 업그레이드를 배경으로 7.38%의 연평균 복합 성장률(CAGR)로 확장될 것으로 전망됩니다. 로봇 도입에 대한 재정적 인센티브와 대규모 산업 단지 개발이 결합되어 대량 생산용 탄소강 및 프리미엄 스테인리스강 카테고리 모두에 꾸준한 주문이 유입되고 있습니다. 중국의 반도체 장비 현지화는 초고청정 및 무입자 패스너에 대한 특수 수요를 창출하는 반면, 인도의 ‘메이크 인 인디아’ 정책은 대구경 볼트를 필요로 하는 중장비의 현지 생산을 촉진합니다. 이러한 프로젝트들은 종합적으로 1차 및 지역 공급업체 전반에 걸쳐 산업용 패스너 시장을 확대합니다.

북미는 방위 조달, 에너지 인프라 현대화, 자동차 및 전자제품 조립의 리쇼어링에 힘입어 핵심 거점으로 남아 있습니다. 미국 OEM 업체들은 물류 차질과 환율 변동 완화를 위해 국내 패스너 조달을 확대했습니다. 멕시코의 신흥 허브는 미국 구매자와의 근접성을 활용해 경차 플랫폼 및 소비자 전자제품 최종 조립용 패스너를 공급합니다. 캐나다는 광산 삽과 오일샌드 처리 라인에 극한 온도용 패스너가 필요한 자원 채굴 장비를 통해 성장세를 유지합니다. 전반적으로 안정적인 프로젝트 파이프라인이 지역 산업용 패스너 시장의 중간 단일자리 수치 성장을 유지합니다.

유럽은 독일의 정밀 기계 부문, 이탈리아의 공작기계 수출, 프랑스의 항공우주 공급망을 통해 견실한 가치를 창출합니다. 지속가능성을 우선시하는 규제 프레임워크는 재료 추적성과 폐쇄형 재활용을 장려하여 공급업체들이 QR 코드 식별 및 재생 금속 함량 도입을 촉진합니다. 브렉시트 이후 복잡성으로 일부 공급 흐름이 대륙 허브로 전환되었으나, 영국 해상풍력 설비는 아연도금 구조용 볼트에 대한 틈새 수요를 유지하고 있습니다. 인더스트리 4.0 도입이 가속화됨에 따라 해당 지역 산업용 패스너 시장은 2031년까지 연평균 3.74% 성장률을 기록할 것으로 전망됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 자동차 전기화로 인한 배터리 장착용 패스너 수요 증가

- 내진 건축 규제로 인한 고강도 구조용 볼트 수요 증가

- 대형 직경 부식 방지 볼트가 필요한 해상 풍력 설비

- 항공우주용 패스너 공급 체인의 현지화

- 산업용 자동화 기기용 정밀 마이크로 패스너

- 신흥 경제국의 인프라 자극책

- 시장 성장 억제요인

- 내장 모듈의 금속 패스너 대체로서 접착제 및 테이프

- 변동성 있는 니켈/몰리브덴 가격으로 인한 스테인리스강 원가 상승

- 중소 제조업체의 인증 부담(AS9100, IATF 16949)

- 티타늄 합금 부족에 의한 항공우주용 패스너 생산 능력 제약

- 가치/공급망 분석

- 규제와 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측(금액, 10억 달러)

- 원재료별

- 금속

- 탄소강

- 합금강

- 스테인리스 스틸

- 비철금속(알루미늄, 티타늄, 구리)

- 플라스틱

- 나일론

- 폴리카보네이트

- PVC 및 기타

- 금속

- 제품별

- 외부 나사

- 볼트

- 나사

- 스터드

- 내부 나사

- 너트

- 인서트

- 비나사 패스너

- 리벳

- 와셔

- 핀 및 클립

- 항공우주 등급 패스너

- 티타늄 패스너

- 초합금 패스너

- 외부 나사

- 용도별

- 자동차

- 항공우주 및 방위

- 건축 및 건설

- 산업기계 및 로봇공학

- 가전제품 및 전자기기

- 배관 및 에어컨 설비 제품

- 기타 산업용도

- 판매 채널별

- OEM

- 애프터마켓/MRO

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 중동

- 이스라엘

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 이집트

- 기타 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Acument Global Technologies, Inc.

- Arconic Corporation

- LISI Group

- Nifco Inc.

- Hilti Corporation

- Stanley Black and Decker, Inc.

- MacLean-Fogg Company

- MISUMI Group Inc.

- Precision Castparts Corp.

- SFS Group

- Illinois Tool Works Inc.

- Fastenal Company

- Wurth Group

- Bossard Group

- PennEngineering

- Bulten AB

- KAMAX Holding GmbH

- Sundram Fasteners Ltd.

- Shanghai Prime Machinery Co. Ltd.

- TriMas Corporation

- Nitto Seiko Co., Ltd.

제7장 시장 기회와 장래의 전망

HBR 26.01.29The industrial fasteners market is expected to grow from USD 88.38 billion in 2025 to USD 92.1 billion in 2026 and is forecast to reach USD 113.21 billion by 2031 at 4.21% CAGR over 2026-2031.

Demand is supported by manufacturing automation, heavy-machinery upgrades, and precision-assembly requirements that call for reliable, high-strength joints across complex equipment. Adoption of Industry 4.0 platforms is accelerating the use of smart, sensor-enabled fasteners that capture torque and preload data, helping manufacturers cut downtime and enhance traceability. Reshoring and localization strategies are reinforcing the industrial fasteners market by shortening lead times and reducing exposure to global logistics risks. Meanwhile, rising investment in infrastructure renewal and industrial capacity expansions in Asia and North America underpins a steady flow of large-volume orders for structural and specialty products.

Global Industrial Fasteners Market Trends and Insights

Industrial Automation Equipment Requiring Precision Micro-Fasteners

Electronics, medical-device, and semiconductor plants now specify micro-screws that weigh a fraction of a gram yet must deliver repeatable clamp loads at cycle times below one second. Integrators such as JR Automation report micron-level placement accuracy, and this drives demand for bespoke fastening geometries, torques under 1 N*m, and advanced coatings that mitigate galling under rapid load cycles. Power-tool suppliers are responding with cordless transducer-controlled wrenches that log every tightening event and transmit data wirelessly to MES dashboards, a capability showcased in Panasonic's AccuPulse platform. Manufacturers cite immediate quality-cost benefits, including fewer rework stations and shorter takt times, reinforcing the industrial fasteners market trajectory in high-volume automated lines. As more plants digitize, specifiers increasingly insist on fasteners that integrate ID chips for traceability and can be fed through bowl feeders without jamming. The trend has already migrated from electronics to automotive battery modules and collaborative-robot joints, ensuring sustained growth over the next two years

Manufacturing Reshoring Driving Domestic Industrial Fastener Demand

Geopolitical uncertainty and pandemic-era port congestion have prompted US and EU OEMs to reevaluate total landed costs rather than unit price alone. Roughly two-thirds of fasteners consumed in the United States are now produced domestically, a reversal of the offshoring trend observed a decade earlier. Local suppliers benefit from closer engineering collaboration, lower inventory buffers, and compliance with Buy-America clauses embedded in public-infrastructure awards. Capital investment in cold-heading lines, heat-treatment furnaces, and automated sorting cells is accelerating at both regional job shops and multinational firms, lifting utilization rates across the industrial fasteners market. While labor costs remain higher than in Asia, OEMs cite freight savings and reduced obsolescence risk as decisive advantages. The reshoring dynamic is expected to maintain a positive thrust on market volumes through at least 2028, especially for medium-to-high-strength grades that favor short supply chains.

Advanced Joining Technologies Substituting Traditional Industrial Fasteners

High-volume equipment producers are trialing structural adhesives, laser welding, and friction-stir welding for enclosures and chassis where permanent bonds are acceptable. Hybrid designs that combine a rivet or bolt with adhesive fillets reduce component counts and improve load distribution, compelling some OEMs to specify fewer mechanical fasteners per assembly. Aluminum extrusion manufacturers are particularly active in adopting friction-stir welding for lightweight frames, eroding bolt consumption in select applications. Nonetheless, maintenance-heavy environments such as pumps, gearboxes, and process-valve assemblies still require removable joints, preserving a large core base for the industrial fasteners market. The balance between removability and weight savings will define this restraint's real-world impact over the next three years.

Other drivers and restraints analyzed in the detailed report include:

- Heavy Machinery Modernization in Emerging Industrial Markets

- Industry 4.0 Implementation Requiring Smart Fastening Solutions

- Raw Material Cost Volatility Affecting Industrial Fastener Pricing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Metal fasteners held 91.45% of 2025 revenue as heavy-duty machinery, industrial robots, and press lines demanded tensile strengths above 800 MPa. Stainless-steel grades such as AISI 316 captured a premium niche in food processing and pharmaceutical autoclaves where corrosion resistance is paramount. Alloy-steel and carbon-steel bolts remain the default choices for structural frames, gearbox casings, and furnace doors, underpinning the industrial fasteners market. Titanium and nickel-alloy specialty items serve turbine housings and petrochemical reactors, yet supply constraints tied to sponge production cause periodic lead-time extensions. These dynamics underpin a metal segment that, while mature, continues to accrue incremental gains from capacity expansions in emerging economies.

Plastic fasteners, though only 8.55% of volume, are scaling quickly on a 6.72% CAGR through 2031. Nylon screws are now routine in PLC cabinets and LED driver housings, where dielectric strength and chemical inertness add value. Polycarbonate clips secure sensor modules in AGV fleets because they resist impact and allow simplified recycling at end-of-life. Fast-growing demand for lightweight enclosures in smart-meter assemblies further propels polymer uptake. As automation spreads across clean-room industries, engineers are turning to PVDF and PEEK fasteners to eliminate particulate shedding. Consequently, the industrial fasteners market size for plastic variants is projected to approach USD 9.7 billion by 2031, highlighting a clear diversification trend across material portfolios.

Externally threaded products-bolts, screws, studs-delivered 44.30% of industrial fasteners market revenue in 2025. Bolts exceeding M24 diameter dominate crane, press, and extruder assemblies, while machine screws below M6 secure servo-motor mounts and linear actuators. The segment benefits from International Organization for Standardization (ISO) harmonization, which simplifies stocking strategies for multinational OEMs. Interchangeability also supports automatic bin-filling systems that underpin lean manufacturing, reinforcing high-volume growth in the industrial fasteners market.

Aerospace-grade fasteners, although a small slice of shipments, are advancing at 5.88% CAGR. In industrial gas turbines and high-precision machine tools, super-alloy bolts resist cyclical thermal loads exceeding 650 °C. Vibration-resistant configurations-such as shank-grip bolts with prevailing-torque nuts-bring transfer value from aerospace to high-cycle press slides. As defense contracts ramp, suppliers with NADCAP-certified heat-treatment and lab facilities enjoy premium pricing. The industrial fasteners market size for aerospace-grade variants is projected to add USD 1.53 billion by 2031, reflecting broader acceptance of high-performance joints in mission-critical industrial settings.

The Industrial Fasteners Market Report is Segmented by Raw Materials (Metal, Plastic), Products (Externally Threaded Fasteners, Internally Threaded Fasteners, Non-Threaded Fasteners, Aerospace Grade Fasteners), by Application (Automotive, Aerospace, Building and Construction, Industrial Machinery, Home Appliances, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia generated 44.60% of global revenue in 2025 and is projected to expand at 7.38% CAGR on the back of manufacturing upgrades across China, India, and ASEAN nations. Fiscal incentives for robotics adoption, combined with large-scale industrial park developments, funnel steady orders into both high-volume carbon-steel and premium stainless-steel categories. China's localization of semiconductor equipment drives specialty demand for ultra-clean, particle-free fasteners, while India's Make-in-India policy pushes local production of heavy machinery that relies on large-diameter bolts. Collectively, these projects elevate the industrial fasteners market across tier-one and regional suppliers.

North America remains a critical node, supported by defense procurement, energy-infrastructure modernization, and reshoring of automotive and electronics assembly. US OEMs have ramped domestic fastener sourcing to mitigate logistics shocks and currency swings. Emerging hubs in Mexico supply fasteners for light-vehicle platforms and consumer-electronics final assembly, leveraging proximity to US buyers. Canada retains momentum through resource extraction equipment that demands extreme-temperature fasteners in mining shovels and oil-sands processing lines. Overall, stable project pipelines maintain mid-single-digit gains in the regional industrial fasteners market.

Europe contributes robust value through Germany's precision-machinery sector, Italy's machine-tool exports, and France's aerospace supply chain. Regulatory frameworks that prioritize sustainability encourage material traceability and closed-loop recycling, motivating suppliers to adopt QR-coded identification and reclaimed-metal content. Post-Brexit complexity has redirected some supply flows toward continental hubs, but UK offshore-wind installations sustain niche demand for galvanized structural bolts. With Industry 4.0 adoption accelerating, the region's industrial fasteners market is forecast to register a 3.74% CAGR through 2031.

- Acument Global Technologies, Inc.

- Arconic Corporation

- LISI Group

- Nifco Inc.

- Hilti Corporation

- Stanley Black and Decker, Inc.

- MacLean-Fogg Company

- MISUMI Group Inc.

- Precision Castparts Corp.

- SFS Group

- Illinois Tool Works Inc.

- Fastenal Company

- Wurth Group

- Bossard Group

- PennEngineering

- Bulten AB

- KAMAX Holding GmbH

- Sundram Fasteners Ltd.

- Shanghai Prime Machinery Co. Ltd.

- TriMas Corporation

- Nitto Seiko Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Automotive Electrification Boosting Demand for Battery-Ready Fasteners

- 4.2.2 Seismic-Resistant Building Codes Driving High-Strength Structural Bolts

- 4.2.3 Offshore Wind Installations Requiring Large-Diameter Corrosion-Resistant Bolts

- 4.2.4 Localization of Aerospace Fastener Supply Chains

- 4.2.5 Precision Micro-Fasteners for Industrial Automation Equipment

- 4.2.6 Infrastructure Stimulus Programs in Emerging Economies

- 4.3 Market Restraints

- 4.3.1 Adhesives and Tapes Substituting Metal Fasteners in Interior Modules

- 4.3.2 Volatile Nickel/Molybdenum Prices Inflating Stainless-Steel Costs

- 4.3.3 Certification Burden (AS9100, IATF 16949) for Small Manufacturers

- 4.3.4 Titanium Alloy Shortages Limiting Aerospace Fastener Capacity

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Consumers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, USD BN)

- 5.1 By Raw Material

- 5.1.1 Metal

- 5.1.1.1 Carbon Steel

- 5.1.1.2 Alloy Steel

- 5.1.1.3 Stainless Steel

- 5.1.1.4 Non-Ferrous (Aluminum, Titanium, Copper)

- 5.1.2 Plastic

- 5.1.2.1 Nylon

- 5.1.2.2 Polycarbonate

- 5.1.2.3 PVC and Others

- 5.1.1 Metal

- 5.2 By Product

- 5.2.1 Externally Threaded Fasteners

- 5.2.1.1 Bolts

- 5.2.1.2 Screws

- 5.2.1.3 Studs

- 5.2.2 Internally Threaded Fasteners

- 5.2.2.1 Nuts

- 5.2.2.2 Inserts

- 5.2.3 Non-Threaded Fasteners

- 5.2.3.1 Rivets

- 5.2.3.2 Washers

- 5.2.3.3 Pins and Clips

- 5.2.4 Aerospace-Grade Fasteners

- 5.2.4.1 Titanium Fasteners

- 5.2.4.2 Super-Alloy Fasteners

- 5.2.1 Externally Threaded Fasteners

- 5.3 By Application

- 5.3.1 Automotive

- 5.3.2 Aerospace and Defense

- 5.3.3 Building and Construction

- 5.3.4 Industrial Machinery and Robotics

- 5.3.5 Home Appliances and Electronics

- 5.3.6 Plumbing and HVAC Products

- 5.3.7 Other Industrial Applications

- 5.4 By Sales Channel

- 5.4.1 OEM

- 5.4.2 Aftermarket / MRO

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Middle East

- 5.5.4.1 Israel

- 5.5.4.2 Saudi Arabia

- 5.5.4.3 United Arab Emirates

- 5.5.4.4 Turkey

- 5.5.4.5 Rest of Middle East

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Egypt

- 5.5.5.3 Rest of Africa

- 5.5.6 South America

- 5.5.6.1 Brazil

- 5.5.6.2 Argentina

- 5.5.6.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Acument Global Technologies, Inc.

- 6.4.2 Arconic Corporation

- 6.4.3 LISI Group

- 6.4.4 Nifco Inc.

- 6.4.5 Hilti Corporation

- 6.4.6 Stanley Black and Decker, Inc.

- 6.4.7 MacLean-Fogg Company

- 6.4.8 MISUMI Group Inc.

- 6.4.9 Precision Castparts Corp.

- 6.4.10 SFS Group

- 6.4.11 Illinois Tool Works Inc.

- 6.4.12 Fastenal Company

- 6.4.13 Wurth Group

- 6.4.14 Bossard Group

- 6.4.15 PennEngineering

- 6.4.16 Bulten AB

- 6.4.17 KAMAX Holding GmbH

- 6.4.18 Sundram Fasteners Ltd.

- 6.4.19 Shanghai Prime Machinery Co. Ltd.

- 6.4.20 TriMas Corporation

- 6.4.21 Nitto Seiko Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment