|

시장보고서

상품코드

1911467

북미의 산업용 패스너 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)North America Industrial Fasteners - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

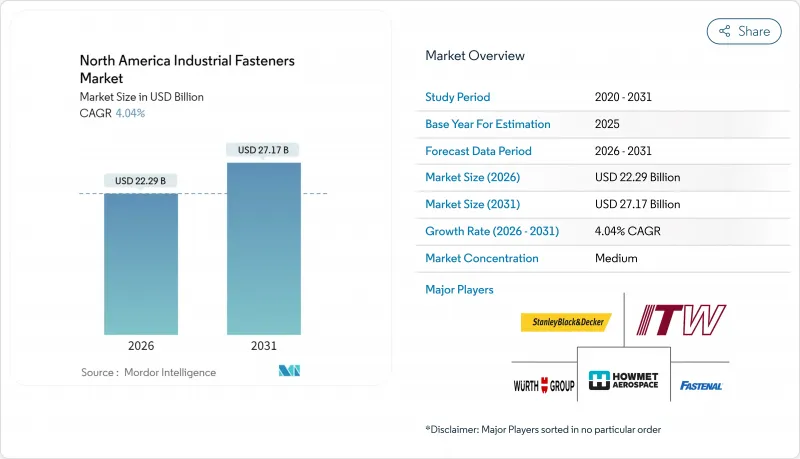

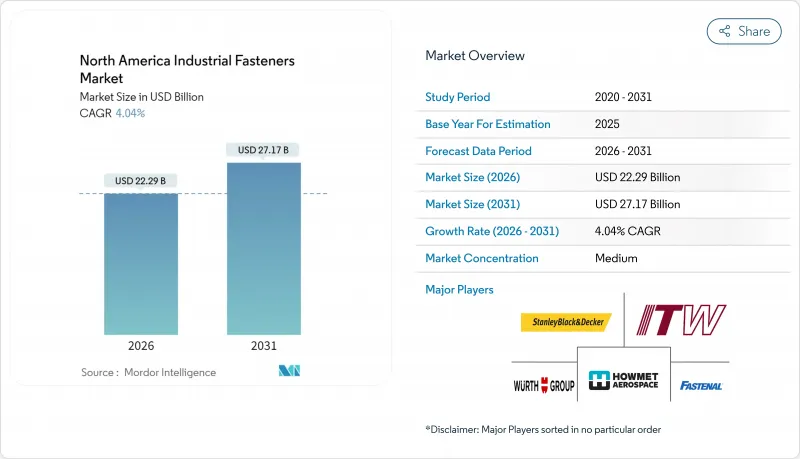

북미의 산업용 패스너 시장 규모는 2026년에 222억 9,000만 달러로 추정되고 있습니다. 이는 2025년 214억 2,000만 달러에서 성장한 수치이며, 2031년에는 271억 7,000만 달러에 달할 것으로 예측되고 있습니다. 2026-2031년 CAGR 4.04%로 성장이 전망되고 있습니다.

건전한 인프라 투자, 전기자동차 생산 증가, 국내 제조를 선도하는 리쇼어링 계획은 투입 비용 변동에도 불구하고 성장세를 유지하고 있습니다. 주택 및 상업, 토목 프로젝트에 있어서 건설 활동이 기반 수요를 지지해, 자동차 및 항공우주 프로그램이 고부가가치 수요량을 추가하고 있습니다. 디지털 추적성, 내식성 코팅, 용도 특화 설계를 통합하는 공급업체는 가격 결정력을 강화하고 있습니다. 최종 사용자는 조립 시간 단축, 서비스 수명 연장 및 컴플라이언스 대응을 용이하게 하는 엔지니어링 솔루션을 계속 중시하고 있습니다. 경쟁의 격렬함은 중간 정도에 머물고 있습니다. 주요 기존 기업은 규모의 경제, 깊은 유통망, 전략적 인수를 활용하여 입지를 굳히고 있습니다.

북미의 산업용 패스너 시장 동향 및 인사이트

건설 부문의 기세가 패스너 수요 지원

1조 2,000억 달러 규모의 인프라 투자 및 고용 창출법에 근거한 건설 지출에 의해 고강도 볼트, 앵커, 나사봉을 필요로 하는 교량, 교통 허브, 유틸리티 프로젝트가 안정적으로 공급되고 있습니다. 텍사스 주와 플로리다 주에서의 주택 개수 및 집합 주택 착공에 의해 건축자재 판매업자는 대량의 벌크 나사나 못을 계속적으로 주문하고 있습니다. 조립식 및 모듈식 건축 기술은 크레인 설치 시 신속하게 조정할 수 있으며 공차를 유지하는 정밀 설계의 패스너를 선호합니다. 공급망 관리자는 부식성 연안 지역 및 차가운 기후 조건을 견디는 코팅을 지정하는 경향이 강해져 평생 유지 보수 비용을 줄일 수 있습니다. 완전한 추적성을 갖춘 인증 로트를 재고하는 유통업체는 미국 제품 구매 의무(Buy-American)에 대한 준거와 즉시 납품을 요구하는 계약을 획득하고 있습니다.

자동차의 전동화가 체결 부품의 요건 변화

배터리 전기자동차 플랫폼은 배터리 팩의 열 사이클 관리 및 전기 절연을 담당하는 전용 스터드, 슬리브 너트, 리벳을 채택하고 있습니다. 미국 조립 라인을 확대하는 자동차 제조업체는 경량 섀시에서 갈바닉 부식을 억제하는 알루미늄 대응 체결 부품을 필수로 하고 있습니다. 고속 로봇 조립은 일관된 토크 텐션 성능에 대한 수요를 촉진하고 공급자에게 더 엄격한 치수 공차를 요구합니다. 전기 픽업 트럭 및 SUV의 생산 확대에 따라 1대당 평균 패스너 사용량이 증가하여 APQP 및 PPAP 기준에 적합한 엔지니어링 부품의 고가격화를 지원하고 있습니다. 셀 제조업체와의 협업은 차세대 고체 전지용 체결 방법의 공동 개발을 가속화하고 있습니다.

구조용 접착제의 과제는 기존의 체결 부품에 도전하는 것입니다.

전기자동차, 항공기 인테리어, 소비자용 전자 기기의 경량화 전략은 보수성이 중요하지 않은 부분에서 기계식 하드웨어를 접착 접합으로 대체하고 있습니다. 접착제는 하중을 고르게 분산시켜 응력 집중을 줄이고 드릴 구멍 가공을 줄입니다. 볼트 수를 줄인 접착 및 결합한 하이브리드 접합 기술은 설치 시간과 부품 수를 줄이고 전체 패스너 수요를 억제합니다. 이에 반해, 체결 부품 공급업체는 유지보수성을 고려한 이동식 설계를 추진함과 동시에 토크 관리가 필수 안전상 중요한 영역에 주력함으로써 대응하고 있습니다. 분해하기 쉬운 코팅 기술의 연구 개발은 접착제와의 직접적인 경쟁이 아니라 그 보완을 목적으로 합니다.

부문 분석

2025년 북미의 산업용 패스너 시장에서 금속 패스너는 76.80%를 차지했습니다. 이는 건설, 기계 및 운송 분야에서 강도 대 비용의 우위를 반영합니다. 탄소강 볼트는 고속도로 교량의 고정에, 스테인리스 스틸 그레이드는 식품 가공 및 제약 플랜트에서 사용되고 있습니다. 알루미늄 패스너는 항공우주 패널과 EV 배터리 인클로저를 지원하여 중량 감소가 단가를 상쇄합니다. 지배적 지위에도 불구하고, 강재 가격의 주기적인 변동은 이익률을 압박하고, 제조업체는 2차 가공의 자동화와 스크랩 관리의 강화를 강요받고 있습니다. 이 부문은 주와 성을 넘어서는 조달을 단순화하는 표준화된 사양의 혜택을 계속 받고 있습니다.

복합재료 및 특수재료는 2031년까지 연평균 복합 성장률(CAGR) 5.14%로 가장 빠르게 성장이 전망되는 분야입니다. 유리 섬유 강화 폴리머, 세라믹, 고온 합금은 금속이 부식, 전기 전도성 및 자기 간섭에 약점을 갖는 성능 갭을 채웁니다. 해상 풍력 발전기 나셀에서는 탄소섬유 스터드가 희생 코팅없이 해수 침식을 견뎌냅니다. 반도체 제조 공장에서는 클린 룸에서 입자 비산을 피하기 위해 PEEK 나사를 지정합니다. 성장은 재료과학의 지속적인 혁신과 리드타임 단축을 위한 최종 시장 인근의 성형능력 확대에 달려 있습니다. 현재 가격 프리미엄은 보급량을 제한하고 있지만, 가혹한 환경에서는 라이프 사이클 비용 분석이 비금속 옵션을 유리하게 평가하기 때문에 채택이 꾸준히 증가하고 있습니다. 이러한 동향은 북미 산업용 패스너 시장의 장기적인 전망을 강화하고 있습니다.

2025년 시점에서 목재 판매점, 정비 공장, 도매업체용으로 공급되는 표준 등급 하드웨어가 북미 산업용 패스너 시장 규모의 62.10%를 차지했습니다. 대경 육각 볼트, 거친 나사, 못은 일상적인 수리 및 조립 작업을 위해 대량의 통 포장 패키지로 출하됩니다. 자동 냉간 단조 라인에 의한 규모의 경제가 실현되어, 수입 압력에 저항하는 경쟁력 있는 가격 설정이 가능해지고 있습니다. 그러나 상품화는 이익률을 낮추고 생산자를 원재료 가격 변동의 위험에 노출시키고 있습니다.

항공우주, 방위, 에너지 분야에 있어서 내열합금, 고정밀 나사, 독자 코팅이 요구되기 때문에 고성능 패스너는 연률 4.98%의 성장이 전망됩니다. 초합금 스터드는 제트 엔진 케이싱을 고정하고 2상 스테인리스 볼트는 주기적인 압력을 견디는 해저 파이프라인을 체결합니다. AS9100과 NADCAP과 같은 인증 시스템은 리드 타임을 연장하지만, 일단 승인되면 공급업체를 고정하고 매력적인 수익을 가능하게 합니다. 많은 기업들이 복잡한 형상의 프로토타입을 제작하기 때문에 고가의 금형을 필요로 하지 않는 적층 조형의 파일럿 도입을 진행하고 있습니다. 이러한 특수 부품의 용도 확대는 가치 밀도를 높이고, 생산량이 늘어나고 있어도 수익을 지지해, 북미 산업용 패스너 시장의 프리미엄층을 지지하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 건설 부문의 성장

- 자동차 및 항공우주 제조 확대

- 내식성 코팅의 진보

- 북미의 전기자동차(EV) 공급망의 급속한 성장

- 미국 제품 구입법에 의한 현지 조달 촉진

- 디지털 추적 가능성 및 스마트 패스너 구상

- 시장 성장 억제요인

- 구조용 접착제의 채용 확대

- 철강 및 비철금속 가격의 변동성

- 도금에 대한 엄격한 환경 규제

- 특수품에 있어서 리쇼어링 주도의 생산 능력 부족

- 업계 밸류체인 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 거시 경제 동향이 시장에 미치는 영향

제5장 시장 규모 및 성장 예측

- 소재별

- 금속

- 플라스틱

- 복합재료 및 특수재료

- 등급별

- 표준

- 고성능

- 제품 유형별

- 외부 나사

- 내나사

- 비나사

- 용도 특화형 및 특수 용도

- 최종 사용자 용도별

- OEM

- 자동차 및 자동차 산업

- 내연기관 경자동차

- 내연기관(ICE) 중형, 대형 트럭 및 버스

- 전기자동차

- 항공우주

- 기계 및 자본재

- 전기 및 전자 기기

- 가공 금속

- 의료기기

- 기타 OEM 용도

- 자동차 및 자동차 산업

- 보수, 수리 및 운용(MRO)

- 건설

- OEM

- 코팅 및 마무리별

- 무도장(미코팅)

- 아연 도금

- 용융 아연 도금

- PTFE 및 특수 코팅

- 국가별

- 미국

- 캐나다

- 멕시코

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Illinois Tool Works Inc.

- Howmet Aerospace Inc.

- Stanley Black and Decker, Inc.

- Wurth Group

- Fastenal Company

- Fontana Gruppo(Acument Global Technologies, Inc.)

- LISI Group

- Nifco Inc.

- Bulten AB

- ARaymond Group

- Marmon Holdings, Inc.(Berkshire Hathaway)

- Hilti Corporation

- KAMAX Holding GmbH and Co. KG

- Bossard Holding AG

- PennEngineering and Manufacturing Corp.

- Simpson Manufacturing Co., Inc.

- Precision Castparts Corp.(SPS Technologies)

- TriMas Corporation

- Agrati Group

- SFS Group AG

- Optimas Solutions

제7장 시장 기회 및 장래 전망

AJY 26.01.30North America industrial fasteners market size in 2026 is estimated at USD 22.29 billion, growing from 2025 value of USD 21.42 billion with 2031 projections showing USD 27.17 billion, growing at 4.04% CAGR over 2026-2031.

Healthy infrastructure outlays, rising electric-vehicle production, and reshoring programs that prioritize domestic manufacturing sustain momentum despite input-cost volatility. Construction activity across residential, commercial, and civil projects underpins baseline demand, while automotive and aerospace programs add high-value volume. Suppliers that integrate digital traceability, corrosion-resistant coatings, and application-specific designs strengthen pricing power. End-users continue to favor engineered solutions that cut assembly time, extend service life, and ease compliance. Competitive intensity remains moderate as leading incumbents leverage scale, distribution depth, and targeted acquisitions to solidify positions.

North America Industrial Fasteners Market Trends and Insights

Construction sector momentum sustains fastener demand

Construction outlays stemming from the USD 1.2 trillion Infrastructure Investment and Jobs Act maintain a steady pipeline of bridges, transit hubs, and utility projects that rely on high-strength bolts, anchors, and threaded rods. Residential remodeling and multifamily starts in Texas and Florida keep builders' merchants ordering large volumes of bulk screws and nails. Prefabricated and modular building techniques favor precision-engineered fasteners that align quickly and hold tolerances during crane placement. Supply-chain managers increasingly specify coatings that withstand corrosive coastal or cold-climate conditions to cut lifetime maintenance. Distributors stocking certified lots with full traceability win contracts that require Buy-American compliance and immediate delivery.

Automotive electrification reshapes fastener requirements

Battery-electric vehicle platforms include specialized studs, sleeve nuts, and rivets that manage thermal cycles and electrical isolation within battery packs. Automakers expanding U.S. assembly lines mandate aluminum-compatible fasteners that curb galvanic corrosion in lightweight chassis. High-speed robotic assembly drives demand for consistent torque-tension performance, pushing suppliers toward tighter dimensional tolerances. As production of electric pickups and SUVs scales, average fastener content per unit rises, supporting premium pricing for engineered parts certified to APQP and PPAP standards. Collaborations with cell manufacturers accelerate the co-development of fastening methods for next-generation solid-state batteries.

Structural adhesives challenge traditional fasteners

Lightweighting strategies in electric cars, aircraft interiors, and consumer electronics substitute bonded joints for mechanical hardware where serviceability is non-critical. Adhesives distribute loads evenly, lowering stress concentrations and reducing drill-hole preparation. Hybrid joining techniques that pair bonding with fewer bolts cut installation time and part counts, trimming overall fastener demand. Fastener suppliers counteract by promoting removable designs for maintenance and by targeting safety-critical zones where torque-auditable joints remain mandatory. R&D into disassembly-friendly coatings seeks to complement adhesive use rather than compete directly.

Other drivers and restraints analyzed in the detailed report include:

- Advances in corrosion-resistant coatings

- Rapid growth of the North American EV supply chain

- Steel price volatility creates margin pressure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Metal fasteners accounted for 76.80% of the North America industrial fasteners market in 2025, reflecting their strength-to-cost advantage in construction, machinery, and transportation. Carbon-steel bolts anchor highway bridges, while stainless grades service food-processing and pharmaceutical plants. Aluminum fasteners support aerospace panels and EV battery enclosures where weight savings offset higher unit prices. Despite dominance, cyclical shifts in steel prices can compress margins, prompting producers to automate secondary operations and tighten scrap control. The segment continues to benefit from standardized specifications that simplify procurement across state and provincial lines.

Composite and specialty materials represent the fastest-growing slice at a 5.14% CAGR through 2031. Glass-fiber reinforced polymers, ceramics, and high-temperature alloys fill performance gaps where metals suffer corrosion, electrical conductivity, or magnetic interference. In offshore wind nacelles, carbon-fiber studs resist seawater attack without sacrificial coatings. Semiconductor fabs specify PEEK screws to avoid particle shedding inside cleanrooms. Growth hinges on continued material-science breakthroughs and expanded molding capacity near end-markets to shorten lead times. Price premiums limit volume penetration today, yet adoption rises steadily as life-cycle cost analyses favor non-metallic options in harsh environments. These dynamics fortify the long-term outlook for the North America industrial fasteners market.

Standard-grade hardware supplied to lumber yards, maintenance shops, and bulk distributors captured 62.10% of the North America industrial fasteners market size in 2025. Large-diameter hex bolts, coarse-thread screws, and nails ship in high-volume keg packs to support routine repair and erection work. Automated cold-heading lines deliver economies of scale, allowing competitive pricing that resists import pressure. Nevertheless, commoditization breeds thin margins and exposes producers to raw-material swings.

High-performance fasteners are projected to grow 4.98% annually as aerospace, defense, and energy sectors specify heat-resistant alloys, close-tolerance threads, and proprietary coatings. Super-alloy studs secure jet-engine casings, while duplex-stainless bolts fasten subsea pipelines subjected to cyclic pressure. Qualification regimes such as AS9100 and NADCAP extend lead times but lock in suppliers once approved, enabling attractive returns. Many firms adopt additive-manufacturing pilots to prototype complex geometries without costly tooling. Expanded use of such specials lifts value density, bolstering revenue even if tonnage lags, and supports the premium tier of the North America industrial fasteners market.

The North America Industrial Fasteners Market is Segmented by Material (Metal, Plastic, and Composite and Specialty), Grade (Standard and High-Performance), Product Type (Externally Threaded, Internally Threaded, and More), End-User Application (OEM, MRO, and Construction), Coating/Finish (Plain, Zinc-Plated, and More), and Country (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Illinois Tool Works Inc.

- Howmet Aerospace Inc.

- Stanley Black and Decker, Inc.

- Wurth Group

- Fastenal Company

- Fontana Gruppo (Acument Global Technologies, Inc.)

- LISI Group

- Nifco Inc.

- Bulten AB

- ARaymond Group

- Marmon Holdings, Inc. (Berkshire Hathaway)

- Hilti Corporation

- KAMAX Holding GmbH and Co. KG

- Bossard Holding AG

- PennEngineering and Manufacturing Corp.

- Simpson Manufacturing Co., Inc.

- Precision Castparts Corp. (SPS Technologies)

- TriMas Corporation

- Agrati Group

- SFS Group AG

- Optimas Solutions

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth of the Construction Sector

- 4.2.2 Expansion of Automotive and Aerospace Manufacturing

- 4.2.3 Advances in Corrosion-Resistant Coatings

- 4.2.4 Rapid Growth of North American EV Supply Chain

- 4.2.5 Buy-American Acts Driving Local Sourcing

- 4.2.6 Digital Traceability and Smart-Fastener Initiatives

- 4.3 Market Restraints

- 4.3.1 Rising Adoption of Structural Adhesives

- 4.3.2 Volatility in Steel and Non-Ferrous Metal Prices

- 4.3.3 Stringent Environmental Regulations on Plating

- 4.3.4 Reshoring-led Capacity Bottlenecks for Specials

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Material

- 5.1.1 Metal

- 5.1.2 Plastic

- 5.1.3 Composite and Specialty

- 5.2 By Grade

- 5.2.1 Standard

- 5.2.2 High-Performance

- 5.3 By Product Type

- 5.3.1 Externally Threaded

- 5.3.2 Internally Threaded

- 5.3.3 Non-Threaded

- 5.3.4 Application-Specific/Specialty

- 5.4 By End-User Application

- 5.4.1 OEM

- 5.4.1.1 Motor Vehicles/Automotive

- 5.4.1.1.1 ICE Light Vehicles

- 5.4.1.1.2 ICE Medium and Heavy Trucks/Buses

- 5.4.1.1.3 Electric Vehicles

- 5.4.1.2 Aerospace

- 5.4.1.3 Machinery and Capital Goods

- 5.4.1.4 Electrical and Electronics

- 5.4.1.5 Fabricated Metals

- 5.4.1.6 Medical Equipment

- 5.4.1.7 Other OEM Applications

- 5.4.1.1 Motor Vehicles/Automotive

- 5.4.2 Maintenance, Repair and Operations (MRO)

- 5.4.3 Construction

- 5.4.1 OEM

- 5.5 By Coating/Finish

- 5.5.1 Plain (Uncoated)

- 5.5.2 Zinc-Plated

- 5.5.3 Hot-Dip Galvanized

- 5.5.4 PTFE and Specialty Coatings

- 5.6 By Country

- 5.6.1 United States

- 5.6.2 Canada

- 5.6.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Illinois Tool Works Inc.

- 6.4.2 Howmet Aerospace Inc.

- 6.4.3 Stanley Black and Decker, Inc.

- 6.4.4 Wurth Group

- 6.4.5 Fastenal Company

- 6.4.6 Fontana Gruppo (Acument Global Technologies, Inc.)

- 6.4.7 LISI Group

- 6.4.8 Nifco Inc.

- 6.4.9 Bulten AB

- 6.4.10 ARaymond Group

- 6.4.11 Marmon Holdings, Inc. (Berkshire Hathaway)

- 6.4.12 Hilti Corporation

- 6.4.13 KAMAX Holding GmbH and Co. KG

- 6.4.14 Bossard Holding AG

- 6.4.15 PennEngineering and Manufacturing Corp.

- 6.4.16 Simpson Manufacturing Co., Inc.

- 6.4.17 Precision Castparts Corp. (SPS Technologies)

- 6.4.18 TriMas Corporation

- 6.4.19 Agrati Group

- 6.4.20 SFS Group AG

- 6.4.21 Optimas Solutions

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet Need Assessment