|

시장보고서

상품코드

1934582

중국의 재생에너지 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)China Renewable Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

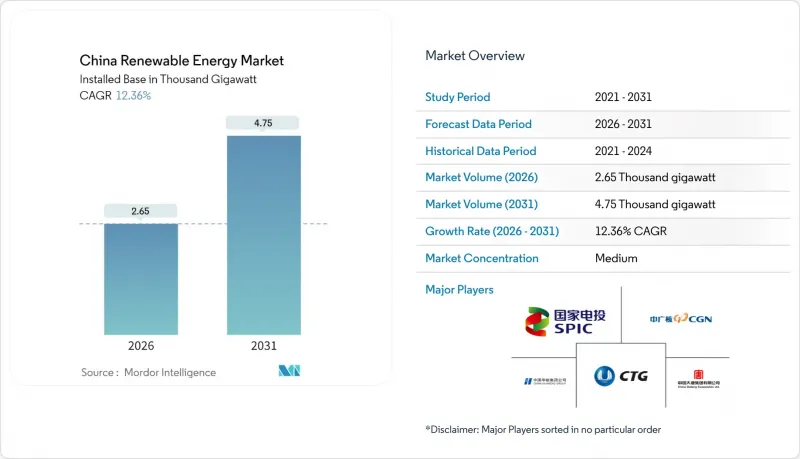

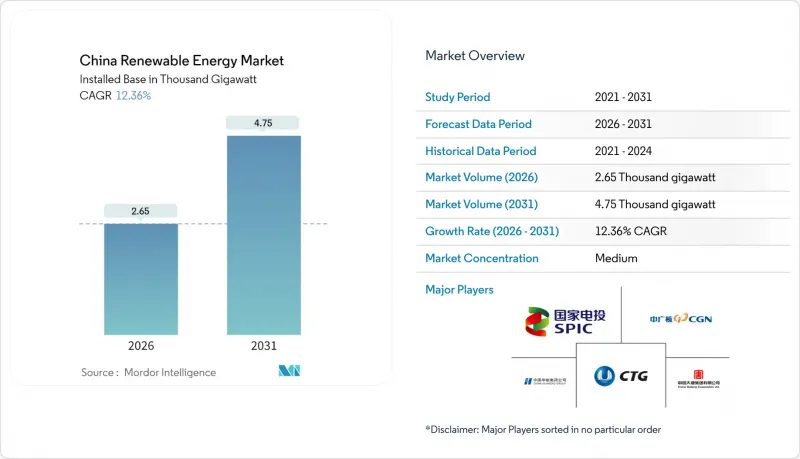

2026년 중국의 재생에너지 시장 규모는 2,650기가와트로 추정되며, 2025년 2,360기가와트에서 성장하여 2031년에는 4,750기가와트에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR)은 12.36%를 나타낼 것으로 예측됩니다.

베이징시는 2060년 탄소중립 달성을 위해 청정에너지 도입에 박차를 가하고 있습니다. 2025년 에너지법에 포함된 정책 개혁, 태양광 및 풍력 발전의 균등화 발전비용(LCOE)의 급격한 하락, 기업용 전력구매계약(PPA)의 확대가 결합되어 지속적인 설비 증설을 촉진하는 한편, 국영 전력회사는 증가하는 재생에너지 출력을 흡수하기 위해 초고압 송전망의 업그레이드를 추진하고 있습니다. 업그레이드를 추진하고 있습니다. 탄탄한 제조 생태계가 설비 가격을 낮게 유지하고, 성(省)급 재생에너지 할당량 처벌이 상업 및 산업 구매자 수요를 더욱 자극하고 있습니다. 동시에, 890억 달러에 달하는 송전망 투자와 새로운 시장 기반 가격 책정 규칙은 수익 모델을 재구성하고 발전 사업자에게 비용 최적화와 경쟁력 강화를 요구하고 있습니다.

중국의 재생에너지 시장 동향과 전망

정부의 2060년 탄소중립 의무와 정책적 인센티브

중앙정부의 탈탄소화 공약은 재정 이전을 보장하기 위해 지방 지도부가 달성해야 할 법적 구속력 있는 용량 할당에 반영되어 있습니다. 14차 5개년 계획에서는 2030년까지 풍력과 태양광을 합해 1,200GW를 도입할 것을 주문하고 있으며, 이는 2024년 기준치의 2배에 해당합니다. 할당량을 달성하지 못한 부처는 예산 지원을 잃게 되므로, 전력회사들은 대차대조표를 보호하기 위해 재생에너지 조달에 박차를 가하고 있습니다. 병행되는 녹색인증서 시장에서는 발전사업자가 전력과 함께 환경적 속성을 판매할 수 있어 프로젝트 수익을 최대 200bp까지 높일 수 있습니다. ISO 14064 보고 의무화는 광동성과 상하이시의 탄소거래 시범사업에서 산업 배출원의 재생가능에너지 조달을 더욱 촉진할 것입니다. 이러한 누적 효과로 인해 중국의 재생에너지 시장의 장기적인 가시성을 확보할 수 있습니다.

태양광-육상풍력 발전 LCOE 급락

대규모 태양광 발전은 현재 일조량이 많은 지역에서 1kWh당 0.02달러 미만의 에너지 공급을 실현하고 있으며, 신규 석탄화력보다 30-40% 저렴한 비용으로 발전할 수 있습니다. 폴리실리콘공급과잉으로 2024년 현물가격은 kg당 40위안까지 하락하여 모듈 제조업체는 와트당 0.10달러 미만의 패널을 제공할 수 있게 되었습니다. 6MW-8MW의 터빈 도입으로 전체 플랜트 비용이 절감되어 풍력 발전 비용이 0.03달러/kWh까지 낮아졌습니다. 여러 성의 입찰에서 0.28위안/kWh에 낙찰되어 화력 발전소는 피크 시간대 역할에 국한되어 재생에너지를 위한 송전 용량을 확보했습니다. 이러한 가격 우위는 중국의 재생에너지 시장의 장기적인 성장을 확고히 하고 있습니다.

계통 출력 억제 및 송전 병목 현상

서부 수성에서는 2027년 이후 완공 예정인 초고압 송전선로 건설이 진행되고 있음에도 불구하고 피크 출력 시 억제율이 10%를 초과하고 있습니다. 북서부 송전망은 2024년 1,000억kWh의 청정 전력을 수출했지만, 이는 재생에너지 발전량의 60%에 불과해 미활용 용량의 문제를 부각시키고 있습니다. 2024년 말까지 추가되는 전력 저장 용량은 70GW를 넘어섰지만, 변동성 재생에너지의 급속한 확대에 필요한 유연성에는 아직 미치지 못하고 있습니다. 시장 기반 조정은 한정된 송전 용량을 둘러싼 프로젝트 간 경쟁으로 인해 단기적으로 발전량 억제를 강화할 수 있으며, 중국의 재생에너지 시장의 일부 지역에서의 확장을 억제할 수 있습니다.

부문 분석

태양광 부문은 2025년 전체 용량의 46.20%를 차지할 것으로 예상되며, 현재 중국의 재생에너지 시장 규모의 기반이 되고 있습니다. 이는 10년에 걸친 비용 절감의 결과로 와트당 0.10달러 미만의 모듈을 실현한 결과입니다. kWh당 0.28위안이라는 입찰 결과는 수익률을 압박하고 있으며, 제조업체들은 수익 유지를 위해 수출 수요와 수직적 통합을 모색하고 있습니다. 풍력발전은 설치 용량의 약 35%를 차지하며, 2024년 상반기에는 해상풍력에서 3.39GW가 추가될 예정입니다. 이를 통해 자원개발 영역을 확대하는 심해저 터빈 설계의 효용성을 입증했습니다. 양수 발전을 포함한 수력 발전은 중요한 유연성을 제공하며, 2025년까지 50GW의 신규 양수 발전 프로젝트가 계획되어 있습니다.

해양 에너지는 아주 작은 규모로 시작했지만, 2031년까지 연평균 복합 성장률(CAGR) 77.17%로 예측되며 중국의 재생에너지 시장 내에서 가장 높은 성장률을 보이고 있습니다. 절강성과 복건성에서 1MW-5MW 규모의 조력 터빈 시험 운영에서 40% 이상의 설비 이용률을 달성했으며, 2028년까지 kWh당 0.08달러로 비용을 절감하는 것을 목표로 20억 위안의 중앙 정부 보조금이 투입될 예정입니다. 장비 제조업체들은 해상풍력 공급망을 조류발전에 적용하여 상용화를 가속화하고, 육상 자산에 의존하지 않는 중국의 재생에너지 시장의 다변화를 추진하고 있습니다.

중국의 재생에너지 시장 보고서는 기술별(태양광, 풍력, 수력, 바이오에너지, 지열, 해양에너지) 및 최종사용자별(전력회사, 상업/산업, 주거용)로 분류되어 있습니다. 시장 규모와 예측은 설치 용량(GW) 단위로 제공됩니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

LSH 26.03.05China Renewable Energy Market size in 2026 is estimated at 2.65 Thousand gigawatt, growing from 2025 value of 2.36 Thousand gigawatt with 2031 projections showing 4.75 Thousand gigawatt, growing at 12.36% CAGR over 2026-2031.

Beijing accelerates clean energy deployment in pursuit of its 2060 carbon neutrality pledge. Policy reforms embedded in the 2025 Energy Law, rapid declines in the levelized cost of solar and wind, and the expansion of corporate power-purchase agreements (PPAs) combine to fuel sustained capacity additions, while state utilities upgrade their ultra-high-voltage grids to absorb the rising renewable output. Robust manufacturing ecosystems keep equipment prices low, and provincial renewable-quota penalties further stimulate demand among commercial and industrial buyers. Simultaneously, transmission investments of USD 89 billion and new market-based pricing rules are reshaping revenue models, compelling generators to optimize costs and enhance their competitiveness.

China Renewable Energy Market Trends and Insights

Government 2060 Carbon-Neutrality Mandate & Policy Incentives

Central government decarbonization pledges translate into legally binding capacity quotas that provincial leaders must meet to secure fiscal transfers. The Fourteenth Five-Year Plan orders 1,200 GW of combined wind and solar by 2030, double the 2024 baseline. Provinces falling short lose budget support, so utilities accelerate renewable procurement to protect balance sheets. A parallel green-certificate market lets generators sell environmental attributes in addition to electricity, lifting project returns by up to 200 basis points. Mandatory ISO 14064 reporting further pushes industrial emitters toward renewable sourcing within carbon-trading pilots in Guangdong and Shanghai. The cumulative effect secures long-run visibility for the Chinese renewable energy market.

Rapid LCOE Decline for Solar PV & On-Shore Wind

Utility-scale solar power now delivers energy below USD 0.02 per kWh, 30%-40% cheaper than new coal in high-irradiance provinces. Polysilicon oversupply pushed spot prices to CNY 40 per kg in 2024, allowing module makers to offer sub-USD 0.10 per-watt panels. Wind energy costs have fallen to USD 0.03 per kWh as 6 MW to 8 MW turbines reduce balance-of-plant expenses. Several provincial auctions cleared at CNY 0.28 per kWh, forcing thermal units into peaking roles and freeing grid capacity for renewables. The price edge cements long-term growth in the Chinese renewable energy market.

Grid Curtailment & Transmission Bottlenecks

Curtailment in several western provinces exceeds 10% during peak output despite ongoing construction of ultra-high-voltage lines slated for completion after 2027. The Northwest grid exported 100 billion kWh of clean power in 2024, only 60% of its renewable generation, highlighting stranded capacity. Storage additions topped 70 GW by end-2024 but still trail the flexibility required for rapid variable-renewable growth. Market-based dispatch could intensify short-term curtailment as projects compete for limited transmission capacity, tempering expansion in certain parts of the Chinese renewable energy market.

Other drivers and restraints analyzed in the detailed report include:

- Boom in Hybrid Renewable-Storage Project Approvals

- Provincial Renewable-Quota Penalties Driving Captive Corporate PPAs

- Raw-Material Supply-Chain Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The solar segment stood at 46.20% of total capacity in 2025, anchoring the current Chinese renewable energy market size and underscoring the decade-long cost decline that produced sub-USD 0.10-per-watt modules. Auction results at CNY 0.28 per kWh compress margins, so manufacturers seek export demand and vertical integration to sustain returns. Wind contributed about 35% of installed capacity, with offshore additions of 3.39 GW in the first half of 2024, validating deep-water turbine designs that expand resource areas. Hydropower, including pumped storage, provides essential flexibility, and 50 GW of new pumped-storage projects are scheduled by 2025.

Ocean energy started from a negligible base but is projected to post an 77.17% CAGR to 2031, the highest within the Chinese renewable energy market. Zhejiang and Fujian pilots using 1 MW to 5 MW tidal turbines deliver capacity factors above 40%, and RMB 2 billion in central subsidies targets cost cuts toward USD 0.08 per kWh by 2028. Equipment makers adapt offshore-wind supply chains to tidal applications, accelerating commercialization and diversifying the Chinese renewable energy market away from land-based assets.

The China Renewable Energy Market Report is Segmented by Technology (Solar Energy, Wind Energy, Hydropower, Bioenergy, Geothermal, and Ocean Energy) and End-User (Utilities, Commercial and Industrial, and Residential). The Market Sizes and Forecasts are Provided in Terms of Installed Capacity (GW).

List of Companies Covered in this Report:

- China Three Gorges Corporation

- State Power Investment Corporation (SPIC)

- China Huaneng Group

- China Huadian Corporation

- China Datang Corporation Renewable Power

- China General Nuclear (CGN) New Energy

- Sinohydro Corporation

- China Yangtze Power Co. Ltd

- Xinjiang Goldwind Science & Technology Co. Ltd

- Dongfang Electric Corporation Ltd

- Ming Yang Smart Energy

- Envision Energy

- Sinovel Wind Group Co. Ltd

- JinkoSolar Holdings Co. Ltd

- Trina Solar Co. Ltd

- LONGi Green Energy Technology Co. Ltd

- JA Solar Technology Co. Ltd

- Canadian Solar Inc. (China ops)

- Sungrow Power Supply Co. Ltd

- TBEA Co. Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government 2060 carbon-neutrality mandate & policy incentives

- 4.2.2 Rapid LCOE decline for solar PV & on-shore wind

- 4.2.3 Grid-parity policies & green-power trading liberalisation

- 4.2.4 Provincial renewable-quota penalties driving captive corporate PPAs

- 4.2.5 Boom in hybrid renewable-storage project approvals

- 4.2.6 Mandatory rooftop PV on new public buildings

- 4.3 Market Restraints

- 4.3.1 Grid curtailment & transmission bottlenecks

- 4.3.2 Raw-material supply-chain volatility (polysilicon, rare-earths)

- 4.3.3 Land-use conflicts causing stricter project permitting

- 4.3.4 Feed-in-tariff phase-out & low auction prices

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

- 4.8 PESTLE Analysis

5 Market Size & Growth Forecasts

- 5.1 By Technology

- 5.1.1 Solar Energy (PV and CSP)

- 5.1.2 Wind Energy (Onshore and Offshore)

- 5.1.3 Hydropower (Small, Large, PSH)

- 5.1.4 Bioenergy

- 5.1.5 Geothermal

- 5.1.6 Ocean Energy (Tidal and Wave)

- 5.2 By End-User

- 5.2.1 Utilities

- 5.2.2 Commercial and Industrial

- 5.2.3 Residential

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 China Three Gorges Corporation

- 6.4.2 State Power Investment Corporation (SPIC)

- 6.4.3 China Huaneng Group

- 6.4.4 China Huadian Corporation

- 6.4.5 China Datang Corporation Renewable Power

- 6.4.6 China General Nuclear (CGN) New Energy

- 6.4.7 Sinohydro Corporation

- 6.4.8 China Yangtze Power Co. Ltd

- 6.4.9 Xinjiang Goldwind Science & Technology Co. Ltd

- 6.4.10 Dongfang Electric Corporation Ltd

- 6.4.11 Ming Yang Smart Energy

- 6.4.12 Envision Energy

- 6.4.13 Sinovel Wind Group Co. Ltd

- 6.4.14 JinkoSolar Holdings Co. Ltd

- 6.4.15 Trina Solar Co. Ltd

- 6.4.16 LONGi Green Energy Technology Co. Ltd

- 6.4.17 JA Solar Technology Co. Ltd

- 6.4.18 Canadian Solar Inc. (China ops)

- 6.4.19 Sungrow Power Supply Co. Ltd

- 6.4.20 TBEA Co. Ltd

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment