|

시장보고서

상품코드

1934762

동남아시아의 중고차 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)South-East Asia Used Car - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

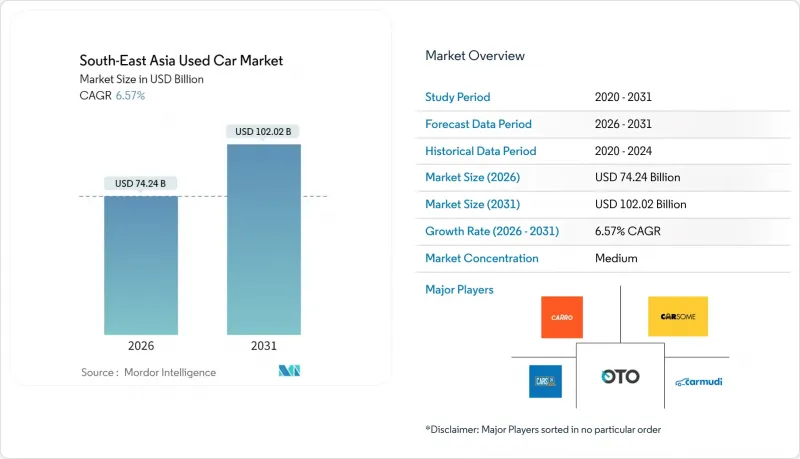

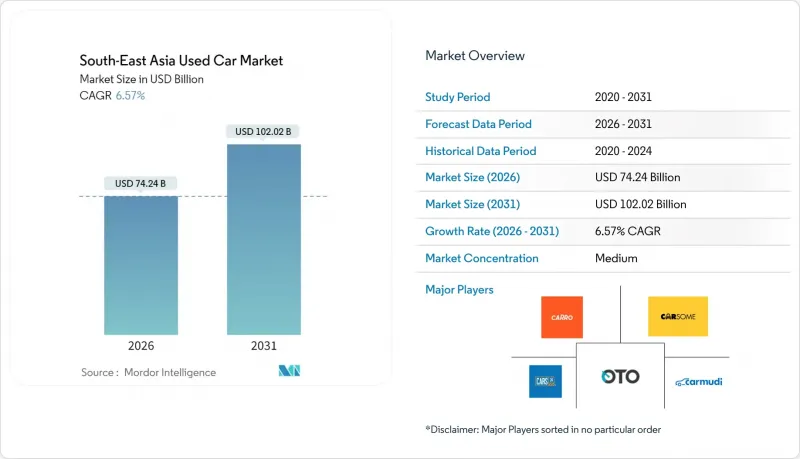

동남아시아의 중고차 시장은 2025년에 696억 6,000만 달러로 평가되었고, 2026년 742억 4,000만 달러에서 2031년까지 1,020억 2,000만 달러에 이를 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 6.57%로 예상됩니다.

이러한 확장을 뒷받침하는 요인으로는 높은 차량 회전율, 거의 신차와 동등한 SUV의 안정적인 공급, 소매 프로세스의 빠른 디지털화를 들 수 있습니다. 한편, 조직화된 딜러 네트워크는 표준화된 품질과 금융 제휴를 통해 추진력을 얻고 있습니다. 동남아시아의 중고차 시장은 가처분 소득 증가, 소형차로의 전환을 촉진하는 도시 교통 체증, 전기차 도입과 구조화된 폐차 프로그램을 촉진하는 정부 인센티브의 혜택을 누리고 있습니다. 온라인 플랫폼은 정보 격차를 줄이는 AI 기반 가격 책정을 통해 구매자의 협상력을 강화하고, 통합 금융은 은행 서비스에 대한 접근성이 제한적인 구매자 수요를 창출합니다. 말레이시아의 특정 부문에 대한 신차세 폐지와 태국의 노후 차량에 대한 유리한 수입 규제는 이 지역의 국경 간 무역의 흐름을 더욱 형성하고 있습니다.

동남아시아의 중고차 시장 동향과 인사이트

온라인 채널 및 디지털 마켓플레이스를 통한 판매 증가

디지털 마켓플레이스의 보급은 우수한 고객 확보 및 유지 메커니즘을 통해 플랫폼이 시장 점유율을 확대함에 따라 거래 패턴을 근본적으로 변화시키고 있습니다. CarSome은 2024년 1분기 EBITDA 흑자 달성, 단위당 총이익은 전년 대비 48% 개선. 동시에 구글 클라우드와의 클라우드 인프라 통합을 통해 AI 기반 고객 경험을 강화했습니다. 스마트폰 보급률이 80%가 넘는 도시 시장에서는 디지털 채널로의 전환이 가속화되고 있습니다. 이를 통해 원격 차량 검사, 디지털 문서화, 거래 마찰을 줄이는 통합 금융 솔루션이 가능해집니다. 온라인 플랫폼은 데이터 분석을 활용하여 가격 책정 알고리즘을 최적화하고, 수동 평가 프로세스에 의존하는 기존 딜러에 비해 경쟁 우위를 창출하고 있습니다.

체계적인 딜러 네트워크 및 인증 중고차 프로그램의 성장

조직화된 딜러의 확대는 특히 하이브리드 및 전기차 파워트레인으로 인해 차량의 복잡성이 증가함에 따라 표준화된 품질 보증 및 보증 보호에 대한 소비자 수요를 반영하고 있습니다. 도요타, 혼다, 메르세데스-벤츠 등의 제조업체가 종합적인 검사 프로토콜과 연장 보증을 포함한 중고차 전문 부서를 설립함에 따라 OEM(자동차 제조업체)이 지원하는 인증 중고차 프로그램이 주목을 받고 있습니다. 규제 준수 요건은 적절한 문서 관리, 세금 준수, 소비자 보호 기준을 유지하는 조직화된 딜러를 점점 더 선호하고 있으며, 비공식 시장 진출기업에 비해 구조적 우위를 점하고 있습니다. 특히 인도네시아와 베트남과 같이 규제 프레임워크가 강화된 시장에서는 정부의 세제 혜택과 간소화된 라이선스 절차를 통해 공식적인 부문 참여를 촉진하고, 조직화된 네트워크로의 전환이 가속화되고 있습니다.

비조직적 딜러와 길거리 판매소의 지배력 강화

비조직적 판매자의 확산은 시장의 전문화를 저해하고 공식적인 금융 채널에 대한 접근을 제한하고 있습니다. 이로 인해 구조적인 비효율성이 발생하여 전체 거래량을 억제하고 있습니다. 이러한 비공식 채널은 표준화된 검사 절차, 보증 규정, 대출 파트너십이 부족하여 소비자는 현금 거래에 의존할 수 밖에 없습니다. 그 결과, 잠재적 구매자 층의 상당 부분이 배제되고 있습니다. 지방 시장 침투는 여전히 길가 판매업자들이 주도하고 있으며, 이들은 지역적 인맥과 유연한 협상 기법을 활용하고 있습니다. 그러나 장기적인 고객 충성도를 구축할 수 있는 품질 보증이나 구매 후 지원 제공에는 어려움을 겪고 있습니다.

부문 분석

2025년 기준 동남아시아의 중고차 시장 점유율의 30.98%를 SUV가 차지하고 있으며, 동남아시아의 도시 환경에서 높은 지상고와 안전성의 우위가 소비자의 선호도 변화를 반영하고 있습니다. SUV 카테고리 내 전기차 부문은 정부 인센티브와 주요 도시 지역의 충전 인프라 개선에 힘입어 2031년까지 연평균 26.15%의 빠른 성장이 예상됩니다. 해치백은 가격 중심 부문에서 강력한 존재감을 유지하고 있으며, 특히 인도네시아와 베트남에서는 소형차의 저렴한 가격이 중산층의 구매력과 일치하고 있습니다. 반면, 세단은 소비자들이 실용성을 중시하는 차종으로 옮겨가면서 수요가 감소하는 추세입니다. 다목적 차량(MPV)은 가족 중심 시장에서 큰 시장 점유율을 차지하고 있으며, 미쓰비시 익스팬더와 같은 모델이 2025년 1분기 베트남 판매를 주도했습니다.

도시화가 진행됨에 따라 도심 교통부터 간헐적인 교외 주행까지 다양한 도로 상황에 대응할 수 있는 차량에 대한 수요가 증가하면서 SUV로의 전환이 가속화되고 있습니다. 베트남 시장 데이터에 따르면, 2025년 상반기에는 세단 판매량이 감소하는 추세이며, 소비자들은 가시성과 안전성 측면에서 우위를 점할 수 있는 높은 차고를 가진 차량을 점점 더 선호하고 있습니다. 이러한 추세는 중고차 시장에 연쇄적인 영향을 미치고 있으며, SUV 재고는 프리미엄 가격으로 거래가 이루어지고 있습니다. 한편, 세단의 가치는 하락 압력을 받고 있으며, 이로 인해 지역 전체 딜러의 재고 전략과 금융 리스크 평가가 근본적으로 변화하고 있습니다.

2025년 현재 동남아시아의 중고차 시장 점유율의 72.13%는 가솔린 차량이 차지하고 있습니다. 이는 이미 구축된 급유 인프라와 대체 연료 기술에 비해 낮은 초기 비용에 힘입은 결과입니다. 전기차는 CAGR 26.05%로 가장 빠르게 성장하고 있는 부문이지만, 충전 인프라 부족과 배터리 성능 저하로 인한 재판매 가치에 대한 우려가 보급에 걸림돌로 작용하고 있습니다. 디젤차는 상용차 및 대형차량 용도에 집중되고, LPG, CNG, 하이브리드 시스템 등 대체 연료는 정부의 지원정책과 연료비 우위 시장으로 보급이 진행되고 있습니다.

인도네시아에서는 전기자동차에 대한 100% 사치세 면제를 2025년까지 연장하여 보급을 촉진하고 있지만, 소비자의 구매력 감소와 신차 출시에 대한 기대감으로 2024년 판매량은 15% 감소했습니다. 중고 전기차 시장은 기술 발전의 급속한 발전으로 인한 감가상각률의 가속화와 배터리 성능이 중고 전기차에 대한 소비자의 신뢰를 제한하고 있기 때문에 여전히 개발 단계에 있습니다. 싱가포르의 동남아시아 전기차 시장의 리더십은 지역적 보급 패턴에 영향을 미치는 실증 효과를 창출하고 있습니다. 그러나 지방도시의 인프라 제약으로 인해 아세안 시장 전체에서 전기자동차의 광범위한 보급을 가로막고 있습니다.

2025년 기준 동남아시아의 중고차 시장 점유율의 37.98%를 4-6년 된 차량이 차지할 것으로 예상되며, 이는 중산층 소비자에게 감가상각, 기능성, 금융 접근성의 최적의 균형이 이루어지고 있다는 것을 의미합니다. 0-3년 경과 차량 부문은 신차 회전율 상승과 제조업체 보증이 남아있는 중고차에 대한 소비자 선호에 힘입어 2031년까지 연평균 복합 성장률(CAGR) 18.62%로 가장 빠르게 성장할 것으로 예측됩니다. 7-10년 된 차량은 가격에 민감한 부문에서 안정적인 수요를 유지하는 반면, 10년 이상 된 차량 카테고리는 배기가스 규제와 차량 현대화를 위한 폐차 장려 정책으로 인한 규제 압력에 직면해 있습니다.

중저가 차종에 집중된 것은 대출의 가용성을 반영하고 있습니다. 은행과 비은행금융회사(NBFC)는 예측 가능한 감가상각 곡선과 충분한 잔존수명이 있고, 대출 조건을 담보할 수 있는 자산을 담보로 한 대출을 선호하기 때문입니다. 2024년 베트남 경제 성장은 4-6년 경과 차량의 잠재적 시장을 확대할 것입니다. 소득 증가로 인해 소비자들은 오래된 차량을 교체하거나 처음으로 자동차를 소유할 수 있게 되었기 때문입니다. 정부의 폐차 정책은 15년 이상 된 차량을 중점 대상으로 하고 있으며, 이로 인해 4-8년 경과 차량(최신 안전장비 및 배출가스 규제 적합 기능을 갖춘 대체 차량)에 대한 인위적인 수요 가속화가 일어나고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

LSH 26.03.05The Southeast Asia used car market was valued at USD 69.66 billion in 2025 and estimated to grow from USD 74.24 billion in 2026 to reach USD 102.02 billion by 2031, at a CAGR of 6.57% during the forecast period (2026-2031).

Strong vehicle turnover, a steady pipeline of nearly-new SUVs, and rapid digitization of the retail journey underpin this expansion, while organized dealer networks gain traction through standardized quality and financing partnerships. The Southeast Asia used car market benefits from rising disposable incomes, urban congestion that favors smaller vehicle upgrades, and government incentives that stimulate both electric vehicle adoption and structured scrappage programs. Online platforms strengthen bargaining power through AI-driven pricing that narrows informational asymmetries, and integrated financing unlocks demand from underbanked buyers. Malaysia's elimination of new-car taxes on selected segments and Thailand's favorable import rules for older vehicles further shape regional cross-border trade flows.

South-East Asia Used Car Market Trends and Insights

Rising Sales Through Online Channels and Digital Marketplaces

Digital marketplace adoption fundamentally reshapes transaction patterns as platforms capture increasing market share through superior customer acquisition and retention mechanisms. Carsome achieved EBITDA positivity in Q1 2024 with 48% year-on-year gross profit per unit improvement, while consolidating cloud infrastructure with Google Cloud to enhance AI-driven customer experiences. The shift toward digital channels accelerates in urban markets where smartphone penetration exceeds 80%, enabling remote vehicle inspection, digital documentation, and integrated financing solutions that reduce transaction friction. Online platforms leverage data analytics to optimize pricing algorithms, creating competitive advantages over traditional dealerships that rely on manual valuation processes.

Growth in Organized Dealership Networks and Certified Pre-Owned Programs

Organized dealership expansion reflects consumer demand for standardized quality assurance and warranty protection, particularly as vehicle complexity increases with hybrid and electric powertrains. OEM-backed certified pre-owned programs gain traction as manufacturers like Toyota, Honda, and Mercedes-Benz establish dedicated used vehicle divisions with comprehensive inspection protocols and extended warranty coverage. Regulatory compliance requirements increasingly favor organized dealers who maintain proper documentation, tax compliance, and consumer protection standards, creating structural advantages over informal market participants. The shift toward organized networks accelerates in markets with strengthening regulatory frameworks, particularly Indonesia and Vietnam, where government initiatives promote formal sector participation through tax incentives and simplified licensing procedures.

Dominance of Unorganized Dealers and Roadside Lots

Unorganized dealer prevalence constrains market professionalization and limits access to formal financing channels, creating structural inefficiencies that suppress overall transaction volumes. These informal channels lack standardized inspection protocols, warranty provisions, and financing partnerships, forcing consumers to rely on cash transactions that exclude significant portions of the potential buyer base. Rural market penetration remains dominated by roadside dealers who leverage local relationships and flexible negotiation practices, yet struggle to provide quality assurance or post-purchase support that builds long-term customer loyalty.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Turnover of New-Car Sales Feeding Used Supply

- Availability of Integrated Financing and Insurance Solutions

- Lack of Standardized Vehicle-Condition Reporting Protocols

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

SUVs command 30.98% of the Southeast Asia used car market share in 2025, reflecting consumer preference shifts toward higher ground clearance and perceived safety advantages in Southeast Asian urban environments. The electric vehicle segment within the SUV category allows the overall segment to surge at a 26.15% CAGR through 2031, driven by government incentives and improving charging infrastructure across major metropolitan areas. Hatchbacks maintain a strong presence in price-sensitive segments, particularly in Indonesia and Vietnam, where compact vehicle affordability aligns with middle-class purchasing power. At the same time, sedans face declining demand as consumers migrate toward utility-focused vehicle formats. Multi-Purpose Vehicles (MPVs) capture significant market share in family-oriented demographics, with models like Mitsubishi Xpander leading Vietnamese sales in Q1 2025.

The shift toward SUVs accelerates as urbanization increases demand for vehicles capable of handling diverse road conditions, from city traffic to occasional rural excursions. Vietnamese market data reveals sedan sales declining in the first half of 2025, with consumers increasingly favoring higher-riding vehicles that offer superior visibility and perceived safety advantages. This trend creates cascading effects in the used car market, where SUV inventory commands premium pricing. At the same time, sedan values face downward pressure, fundamentally altering dealer inventory strategies and financing risk assessments across the region.

Gasoline-powered vehicles account for 72.13% of the Southeast Asia used car market share in 2025, supported by established refueling infrastructure and lower upfront costs than alternative fuel technologies. Electric vehicles represent the fastest-growing segment at 26.05% CAGR, though adoption faces challenges from limited charging infrastructure and battery degradation concerns that impact resale values. Diesel vehicles concentrate in commercial and heavy-duty applications, while alternative fuels, including LPG, CNG, and hybrid systems, gain traction in markets with supportive government policies and fuel cost advantages.

Indonesia's extension of 100% luxury tax exemption for electric vehicles through 2025 stimulates EV adoption, though sales declined 15% in 2024 due to reduced consumer purchasing power and anticipation of new model launches. The used EV market remains nascent due to rapid technological advancement that accelerates depreciation rates, with battery performance limiting consumer confidence in pre-owned electric vehicles. Singapore's EV market leadership in Southeast Asia creates demonstration effects that influence regional adoption patterns. However, infrastructure limitations in secondary cities constrain widespread electric vehicle penetration across the broader ASEAN market.

Vehicles aged 4-6 years captured 37.98% of the Southeast Asia used car market share in 2025, representing the optimal balance between depreciation, functionality, and financing accessibility for middle-income consumers. The 0-3 year segment grows fastest at 18.62% CAGR through 2031, driven by increasing new car turnover rates and consumer preference for near-new vehicles with remaining manufacturer warranties. Vehicles aged 7-10 years maintain steady demand in price-sensitive segments, while the 10+ year category faces regulatory pressure from emissions standards and scrappage incentives designed to modernize vehicle fleets.

The concentration in mid-life vehicles reflects financing accessibility, as banks and NBFCs prefer lending against assets with predictable depreciation curves and sufficient remaining useful life to secure loan terms. Vietnam's economic growth in 2024 expands the addressable market for 4-6 year vehicles, as rising incomes enable consumers to upgrade from older vehicles or enter car ownership for the first time. Government scrappage policies increasingly target vehicles over 15 years old, creating artificial demand acceleration for replacement vehicles in the 4-8 year age range that offer modern safety and emissions compliance features.

The Southeast Asia Used Car Market Report is Segmented by Vehicle Type (Hatchback, Sedan, SUV, MPV), Fuel Type (Gasoline, and More), Vehicle Age (0-3 Years, and More), Mileage (Under 30K Km, and More), Sales Channel (Online, Offline), Vendor Type (Organized, Unorganized), Purchase Method (Outright, and Financed), and Geography (Indonesia, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

List of Companies Covered in this Report:

- Carro

- Carsome

- Cars24 Services Pvt Ltd

- Carousell

- OLX

- iCar Asia (Carlist.my)

- myTukar

- BeliMobilGue.co.id

- Carmudi

- Oto.com

- Automart PH

- Mercedes-Benz Certified

- Toyota U Trust

- Honda Certified Pre-Owned

- BMW Premium Selection

- Nissan Intelligent Choice

- Hyundai Promise

- Mitsubishi Diamond Certified

- Isuzu Used Car Program

- LausAutoGroup (Carmix)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising sales through online channels and digital marketplaces

- 4.2.2 Growth in organized dealership networks and certified-pre-owned programs

- 4.2.3 Increasing turnover of new-car sales (especially SUVs) feeding used supply

- 4.2.4 Availability of integrated financing and insurance solutions

- 4.2.5 Government circular-economy and scrappage incentives accelerating trade-ins

- 4.2.6 AI-driven inspection/pricing platforms boosting buyer trust

- 4.3 Market Restraints

- 4.3.1 Dominance of unorganized dealers and roadside lots

- 4.3.2 Lack of standardized vehicle-condition reporting protocols

- 4.3.3 Emerging import restrictions on older used vehicles

- 4.3.4 Reduced private-car ownership in urban areas due to mobility-as-a-service

- 4.4 Value/Supply-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Vehicle Type

- 5.1.1 Hatchback

- 5.1.2 Sedan

- 5.1.3 Sport-Utility Vehicle (SUV)

- 5.1.4 Multi-Purpose Vehicle (MPV)

- 5.2 By Fuel Type

- 5.2.1 Gasoline

- 5.2.2 Diesel

- 5.2.3 Electric

- 5.2.4 Alternative Fuels (LPG/CNG/Hybrid)

- 5.3 By Vehicle Age

- 5.3.1 0 to 3 Years

- 5.3.2 4 to 6 Years

- 5.3.3 7 to 10 Years

- 5.3.4 More than 10 Years

- 5.4 By Mileage

- 5.4.1 Less than 30 000 km

- 5.4.2 30 001 to 60 000 km

- 5.4.3 60 001 to 100 000 km

- 5.4.4 More than 100 000 km

- 5.5 By Sales Channel

- 5.5.1 Online

- 5.5.2 Offline

- 5.6 By Vendor Type

- 5.6.1 Organized

- 5.6.2 Unorganized

- 5.7 By Purchase Method

- 5.7.1 Outright Purchase

- 5.7.2 Financed Purchase

- 5.7.2.1 Captive Financing

- 5.7.2.2 Bank Financing

- 5.7.2.3 Non-Banking Financial Companies (NBFC)

- 5.8 By Country (Southeast Asia)

- 5.8.1 Indonesia

- 5.8.2 Thailand

- 5.8.3 Vietnam

- 5.8.4 Malaysia

- 5.8.5 Philippines

- 5.8.6 Singapore

- 5.8.7 Other Countries (Cambodia, Laos, Myanmar, Brunei)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Carro

- 6.4.2 Carsome

- 6.4.3 Cars24 Services Pvt Ltd

- 6.4.4 Carousell

- 6.4.5 OLX

- 6.4.6 iCar Asia (Carlist.my)

- 6.4.7 myTukar

- 6.4.8 BeliMobilGue.co.id

- 6.4.9 Carmudi

- 6.4.10 Oto.com

- 6.4.11 Automart PH

- 6.4.12 Mercedes-Benz Certified

- 6.4.13 Toyota U Trust

- 6.4.14 Honda Certified Pre-Owned

- 6.4.15 BMW Premium Selection

- 6.4.16 Nissan Intelligent Choice

- 6.4.17 Hyundai Promise

- 6.4.18 Mitsubishi Diamond Certified

- 6.4.19 Isuzu Used Car Program

- 6.4.20 LausAutoGroup (Carmix)

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Improved focus on bundled value-added services (Financing, insurance, extended warranty, subscription plans)