|

시장보고서

상품코드

1939007

아시아태평양의 화물 및 물류 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Asia Pacific Freight And Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

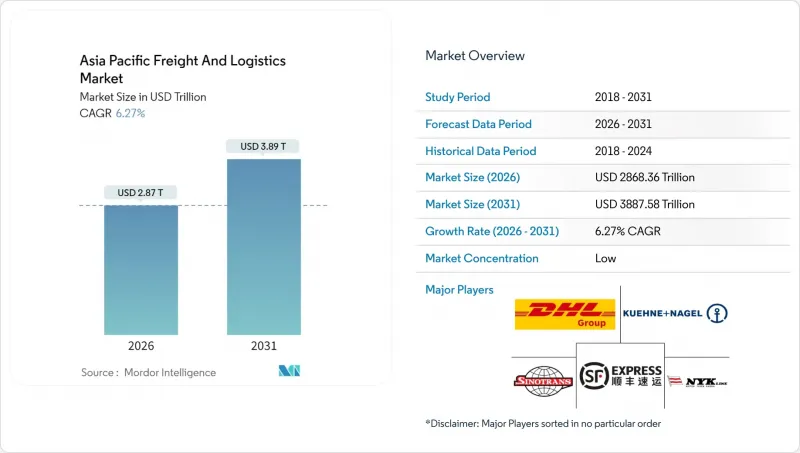

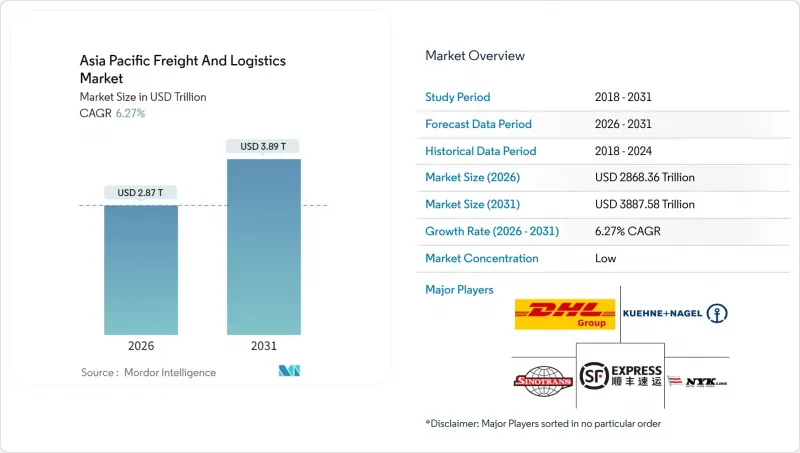

아시아태평양의 화물 및 물류 시장 규모는 2026년에 2조 8,683억 6,000만 달러에 달할 것으로 예측됩니다.

이는 2025년 2조 6,983억 8,800만 달러에서 성장한 수치이며, 2031년에는 3조 8,875억 8,800만 달러에 달할 것으로 예상됩니다. 2026년부터 2031년까지 CAGR 6.27%로 확대될 전망입니다.

탄탄한 역내 무역, 세계 공급망 재구축, 정책 주도의 인프라 구축과 함께 아시아태평양의 화물 및 물류 시장은 지속적으로 확대될 것으로 예상됩니다. 동남아시아로의 제조업 이전과 국경 간 E-Commerce 거래량 증가가 맞물려 운송 경로의 밀도와 서비스 구성을 재구성하면서 기존 동서 간선로의 의존도를 완화하고 있습니다. 동시에 공공부문의 대형 프로젝트가 항만, 고속도로, 철도망의 잠재력을 발휘하여 아시아태평양의 화물 및 물류 시장의 장기적인 경쟁력을 강화하고 있습니다. 기후변화와 보안 위험의 증가로 화주들은 거점 다변화와 디지털 가시성 확보에 투자하고 있으며, 이는 아시아태평양의 화물 및 물류 시장 전반에 걸쳐 수익성 높은 엔드투엔드 물류 솔루션에 대한 수요를 뒷받침하고 있습니다.

아시아태평양 화물 및 물류 시장 동향과 인사이트

급증하는 E-Commerce 택배 물량

모바일 단말기의 보급과 마켓플레이스의 침투가 가속화되면서 아시아 도시 지역의 소포 취급량이 역대 최고치를 갱신하고 있습니다. 주요 CEP 사업자(택배 사업자)들은 2025년 두 자릿수 취급량 증가를 보고하고 있으며, 자동분류센터와 마이크로 풀필먼트 허브의 급속한 확장을 촉구하고 있습니다. 소포 밀도의 향상으로 단위 배송비가 압축되고 경쟁력 있는 가격 책정이 가능해지면서 온라인 소비가 더욱 가속화되고 있습니다. 도시 정부는 교통체증 대책으로 도로변 배송 구역과 비수기 화물 규제를 도입하여 간접적으로 기술을 활용한 라스트 마일 플랫폼에 대한 수요를 촉진하고 있습니다. 이러한 요인들로 인해 아시아태평양의 화물 및 물류 시장은 고빈도 및 소량 배송의 패러다임으로 전환하고 있습니다.

제조업의 변화와 동남아시아로의 니어쇼어링(Nearshoring)

2024년, 아세안에 대한 외국인 직접투자 규모는 3,290억 달러를 넘어섰습니다. 이는 전자, 자동차, 재생에너지 기업들이 단일 국가에 집중되어 있던 생산기지를 분산시킨 결과입니다. 베트남의 수출 성장과 태국의 동부 경제 회랑은 현대 산업 클러스터가 부품 및 완제품의 새로운 유통을 창출하고 보세 창고, 특수 취급 절차, 동기화된 복합 운송 능력을 필요로 한다는 것을 보여주는 좋은 예입니다. 니어쇼어링 공장이 성숙해짐에 따라 백홀 불균형이 줄어들고 아시아태평양의 화물 및 물류 시장 전체에서 운송업체와 포워더의 운임 효율성이 향상되고 있습니다.

분절된 세관 제도와 서류 절차

아세안 단일 창구 도입에도 불구하고, 역내 운송에 있어 서로 다른 서류 규정으로 인해 며칠의 추가 일수가 발생하고 있습니다. 일부 시장에서는 통관 지연과 수작업이 주요 요인으로 작용하여 물류비용이 GDP의 16%를 초과하는 경우도 있습니다. 블록체인의 시범 운영과 신뢰할 수 있는 거래자 프로그램은 유망하지만, 시행 상황의 편차가 확장성을 저해하고 있습니다. 중소 수출업체들은 불균형적인 컴플라이언스 부담으로 인해 아시아태평양의 화물 및 물류 시장 참여에 제약을 받고 있습니다. 조화로운 디지털 통관 표준을 향한 진전은 여전히 중기적 과제입니다.

부문 분석

2025년 제조업의 매출 점유율 35.74%는 전자, 자동차, 기계 산업 체인이 요구하는 동기화된 국경 간 물류에 기인합니다. 이 부문은 계약 요금의 기반이 되며, 포워더, 창고업자, 운송업자의 기반 밀도를 형성합니다.

그러나 도매 및 소매업은 CAGR 6.62%(2026-2031년)로 가장 빠르게 성장하는 고객층입니다. 옴니채널 소매업체들은 신속한 풀필먼트 시스템에 의존하고 있으며, 지역 물류센터, 재고 유예 전략, 반품 관리 역량에 대한 투자를 촉진하고 있습니다. 이러한 요구는 아시아태평양의 화물 및 물류 시장 전반에 걸쳐 서비스 메뉴의 재구성을 촉진하고 있습니다.

화물 운송은 2025년 매출 점유율의 60.12%를 차지하여 아시아태평양의 화물 및 물류 시장 규모에서 핵심적인 역할을 강조하고 있습니다. 제조 투입재와 완제품의 대량 운송으로 인해 풀트럭 운송과 컨테이너 운송 노선은 고밀도를 유지하고 있지만, 수요가 소량-단납기 운송으로 전환됨에 따라 성장이 둔화되는 추세입니다.

디지털 커머스의 모멘텀과 높아지는 소비자 서비스 기대치에 힘입어 택배, 특송, 소포의 매출은 2026년부터 2031년까지 연평균 6.74% 증가할 것으로 예상됩니다. 통합사업자는 급증하는 소포 처리에 대응하기 위해 허브에 고속 분류기 및 무인운반차를 도입하고 있습니다. 향후 운송 수단 배분은 CEP(택배)로 더욱 기울어질 것이며, 아시아태평양 화물 및 물류 시장에서 화물 운송의 점유율은 감소할 것으로 예상됩니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.09Asia-Pacific freight and logistics market size in 2026 is estimated at USD 2,868.36 billion, growing from 2025 value of USD 2,698.38 billion with 2031 projections showing USD 3,887.58 billion, growing at 6.27% CAGR over 2026-2031.

Robust intra-Asian trade, the re-ordering of global supply chains, and policy-driven infrastructure upgrades position the Asia-Pacific freight and logistics market for sustained expansion. Manufacturing relocations into Southeast Asia, coupled with rising cross-border e-commerce volumes, are reshaping route density and service mix while tempering reliance on the traditional East-West mainline. At the same time, public-sector megaprojects are unlocking latent capacity in ports, highways, and rail links, reinforcing the long-term competitiveness of the Asia-Pacific freight and logistics market. Heightened climate and security risks are prompting shippers to diversify nodes and invest in digital visibility, supporting demand for higher-margin end-to-end logistics solutions across the Asia-Pacific freight and logistics market.

Asia Pacific Freight And Logistics Market Trends and Insights

Exploding E-commerce Parcel Volumes

Surging mobile adoption and marketplace penetration are pushing parcel counts to record highs across urban Asia. Leading CEP operators reported double-digit shipment growth in 2025, prompting rapid roll-out of automated sortation centers and micro-fulfillment hubs. Larger parcel densities are compressing unit delivery costs, enabling competitive pricing that further accelerates online spending. Urban governments are responding with curbside delivery zones and off-peak freight rules to manage congestion, indirectly reinforcing demand for technology-enabled last-mile platforms. Together, these forces are moving the Asia-Pacific freight and logistics market toward a higher-frequency, small-lot delivery paradigm.

Manufacturing Shift and Near-shoring into Southeast Asia

Foreign direct investment into ASEAN surpassed USD 329 billion in 2024, as electronics, automotive, and renewable-energy firms diversified production footprints away from single-country concentration. Vietnam's export growth and Thailand's Eastern Economic Corridor exemplify how modern industrial clusters are creating fresh flows of components and finished goods that require bonded warehousing, special-handling protocols, and synchronized multimodal capacity. As near-shored plants mature, backhaul imbalances are narrowing, unlocking rate efficiencies for carriers and forwarding agents across the Asia-Pacific freight and logistics market.

Fragmented Customs Regimes and Paperwork

Despite the ASEAN Single Window, disparate documentation rules still add several days to intra-regional transit. Logistics costs in some markets exceed 16% of GDP, driven largely by clearance delays and manual processes. While blockchain pilots and trusted-trader programs show promise, uneven implementation hinders scalability. Smaller exporters shoulder disproportionate compliance burdens, constraining their participation in the Asia-Pacific freight and logistics market. Progress toward harmonized digital customs standards remains a medium-term necessity.

Other drivers and restraints analyzed in the detailed report include:

- Government Megaprojects Upgrading Ports, Rail and Roads

- End-to-End Supply-chain Digitalization and Visibility Tools

- Chronic Congestion at Tier-1 Ports / Airports

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Manufacturing's 35.74% revenue share in 2025 derives from electronics, automotive, and machinery chains requiring synchronized cross-border logistics. The segment anchors contract rates and builds base density for forwarders, warehousing providers, and carriers.

Wholesale and retail trade, however, is the fastest-expanding customer pool with a 6.62% CAGR (2026-2031). Omnichannel retailers rely on responsive fulfillment frameworks, driving investment in regional distribution centers, inventory postponement strategies, and returns management capacity. These needs are recasting service menus across the Asia-Pacific freight and logistics market.

Freight transport accounted for 60.12% of 2025 revenue share, underscoring its anchor role in the Asia-Pacific freight and logistics market size. Bulk flows of manufacturing inputs and finished goods keep full-truckload and container lanes dense, yet growth is tapering as demand shifts toward smaller, faster consignments.

Courier, express, and parcel revenues are projected to rise 6.74% CAGR between 2026-2031, powered by digital-commerce momentum and rising consumer service expectations. Integrators are retrofitting hubs with high-speed sorters and autonomous guided vehicles to process soaring parcel counts. Over time, modal allocation is expected to tilt further toward CEP, moderating freight transport's share of the Asia-Pacific freight and logistics market.

The Asia Pacific Freight and Logistics Market Report is Segmented by End User Industry (Agriculture, Fishing, and Forestry, Construction, Manufacturing, and More), by Logistics Function (Courier, Express, and Parcel (CEP), Freight Forwarding, Freight Transport, Warehousing and Storage, and Other Services), and by Country (China, India, Indonesia, Malaysia, Japan, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- A.P. Moller - Maersk

- C.H. Robinson

- CJ Logistics Corporation

- DHL Group

- DP World

- DSV A/S (Including DB Schenker)

- Expeditors International of Washington, Inc.

- FedEx

- J&T Express

- JD Logistics

- Kuehne+Nagel

- LOGISTEED, Ltd. (Including Alps Logistics)

- NYK (Nippon Yusen Kaisha) Line

- SF Express (KEX-SF)

- SG Holdings Co., Ltd.

- Sinotrans, Ltd.

- Toll Group

- United Parcel Service of America, Inc. (UPS)

- XPO, Inc.

- YCH Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Demographics

- 4.3 GDP Distribution by Economic Activity

- 4.4 GDP Growth by Economic Activity

- 4.5 Inflation

- 4.6 Economic Performance and Profile

- 4.6.1 Trends in E-Commerce Industry

- 4.6.2 Trends in Manufacturing Industry

- 4.7 Transport and Storage Sector GDP

- 4.8 Export Trends

- 4.9 Import Trends

- 4.10 Fuel Price

- 4.11 Trucking Operational Costs

- 4.12 Trucking Fleet Size by Type

- 4.13 Major Truck Suppliers

- 4.14 Logistics Performance

- 4.15 Modal Share

- 4.16 Maritime Fleet Load Carrying Capacity

- 4.17 Liner Shipping Connectivity

- 4.18 Port Calls and Performance

- 4.19 Freight Pricing Trends

- 4.20 Freight Tonnage Trends

- 4.21 Infrastructure

- 4.22 Regulatory Framework (Road and Rail)

- 4.22.1 Australia

- 4.22.2 China

- 4.22.3 India

- 4.22.4 Indonesia

- 4.22.5 Japan

- 4.22.6 Malaysia

- 4.22.7 Thailand

- 4.22.8 Vietnam

- 4.23 Regulatory Framework (Sea and Air)

- 4.23.1 Australia

- 4.23.2 China

- 4.23.3 India

- 4.23.4 Indonesia

- 4.23.5 Japan

- 4.23.6 Malaysia

- 4.23.7 Thailand

- 4.23.8 Vietnam

- 4.24 Value Chain and Distribution Channel Analysis

- 4.25 Market Drivers

- 4.25.1 Exploding E-Commerce Parcel Volumes

- 4.25.2 Manufacturing Shift and Near-Shoring into SE Asia

- 4.25.3 Government Megaprojects Upgrading Ports, Rail and Roads

- 4.25.4 End-To-End Supply-Chain Digitalization and Visibility Tools

- 4.25.5 Cross-Border B2B2C Hubs Enabling 3-5-Day Delivery

- 4.25.6 ESG-Linked Green-Corridor Incentives and Sustainable-Fuel Credits

- 4.26 Market Restraints

- 4.26.1 Fragmented Customs Regimes and Paperwork

- 4.26.2 Chronic Congestion at Tier-1 Ports / Airports

- 4.26.3 Carbon-Pricing Schemes Hiking Export Freight Costs

- 4.26.4 Digital-Talent Shortages in Tier-2/3 Logistics Nodes

- 4.27 Technology Innovations in the Market

- 4.28 Porter's Five Forces Analysis

- 4.28.1 Threat of New Entrants

- 4.28.2 Bargaining Power of Buyers

- 4.28.3 Bargaining Power of Suppliers

- 4.28.4 Threat of Substitutes

- 4.28.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 End User Industry

- 5.1.1 Agriculture, Fishing, and Forestry

- 5.1.2 Construction

- 5.1.3 Manufacturing

- 5.1.4 Oil and Gas, Mining and Quarrying

- 5.1.5 Wholesale and Retail Trade

- 5.1.6 Others

- 5.2 Logistics Function

- 5.2.1 Courier, Express, and Parcel (CEP)

- 5.2.1.1 By Destination Type

- 5.2.1.1.1 Domestic

- 5.2.1.1.2 International

- 5.2.1.1 By Destination Type

- 5.2.2 Freight Forwarding

- 5.2.2.1 By Mode of Transport

- 5.2.2.1.1 Air

- 5.2.2.1.2 Sea and Inland Waterways

- 5.2.2.1.3 Others

- 5.2.2.1 By Mode of Transport

- 5.2.3 Freight Transport

- 5.2.3.1 By Mode of Transport

- 5.2.3.1.1 Air

- 5.2.3.1.2 Pipelines

- 5.2.3.1.3 Rail

- 5.2.3.1.4 Road

- 5.2.3.1.5 Sea and Inland Waterways

- 5.2.3.1 By Mode of Transport

- 5.2.4 Warehousing and Storage

- 5.2.4.1 By Temperature Control

- 5.2.4.1.1 Non-Temperature Controlled

- 5.2.4.1.2 Temperature Controlled

- 5.2.4.1 By Temperature Control

- 5.2.5 Other Services

- 5.2.1 Courier, Express, and Parcel (CEP)

- 5.3 Country

- 5.3.1 Australia

- 5.3.2 China

- 5.3.3 India

- 5.3.4 Indonesia

- 5.3.5 Japan

- 5.3.6 Malaysia

- 5.3.7 Thailand

- 5.3.8 Vietnam

- 5.3.9 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 A.P. Moller - Maersk

- 6.4.2 C.H. Robinson

- 6.4.3 CJ Logistics Corporation

- 6.4.4 DHL Group

- 6.4.5 DP World

- 6.4.6 DSV A/S (Including DB Schenker)

- 6.4.7 Expeditors International of Washington, Inc.

- 6.4.8 FedEx

- 6.4.9 J&T Express

- 6.4.10 JD Logistics

- 6.4.11 Kuehne+Nagel

- 6.4.12 LOGISTEED, Ltd. (Including Alps Logistics)

- 6.4.13 NYK (Nippon Yusen Kaisha) Line

- 6.4.14 SF Express (KEX-SF)

- 6.4.15 SG Holdings Co., Ltd.

- 6.4.16 Sinotrans, Ltd.

- 6.4.17 Toll Group

- 6.4.18 United Parcel Service of America, Inc. (UPS)

- 6.4.19 XPO, Inc.

- 6.4.20 YCH Group

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment