|

시장보고서

상품코드

1939094

스페인의 화물 및 물류 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Spain Freight And Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

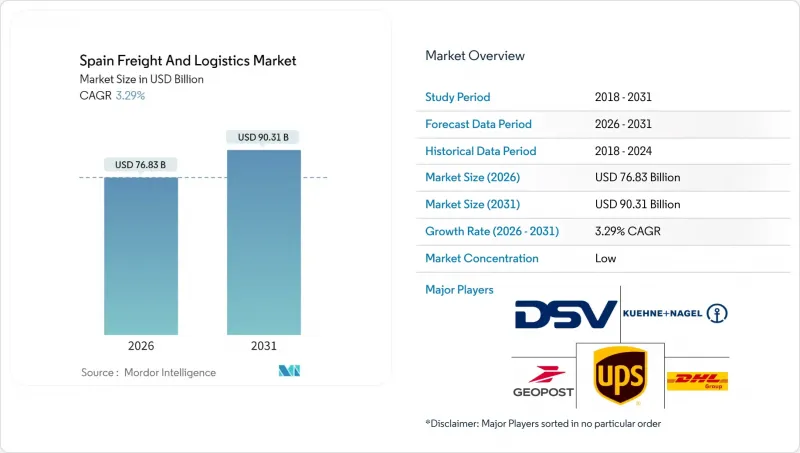

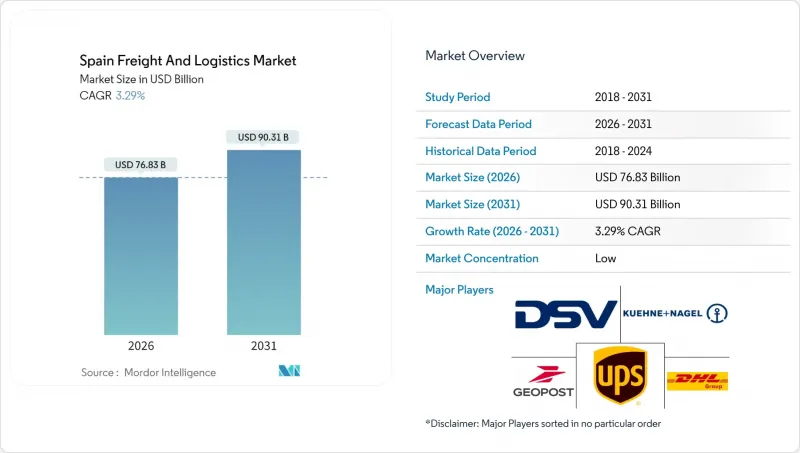

스페인의 화물 및 물류 시장은 2025년에 743억 8,000만 달러로 평가되었으며, 2026년 768억 3,000만 달러에서 2031년까지 903억 1,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년) 동안 CAGR은 3.29%로 예상됩니다.

지중해의 관문으로서 스페인의 입지와 더불어 아시아-유럽 무역이 서지중해 항구로 이동하면서 발렌시아, 바르셀로나, 알헤시라스 항구의 물동량 증가를 견인하고 있습니다. E-Commerce의 확대는 소포 처리량을 증가시켜 자동화 투자를 촉진하고 있으며, DHL이 바르셀로나에 건설한 시간당 3만 개의 소포를 분류할 수 있는 3억 5,000만 유로(3억 8,600만 달러)의 허브가 그 좋은 예입니다. 자동차 및 제약 산업을 중심으로 한 제조업의 회복은 적시(JIT) 운송 수요를 가속화하여 도로 운송의 77.62% 점유율을 뒷받침하고 있습니다. 지중해 회랑 및 항만 LNG 연료 보급 인프라에 대한 14억 유로(15억 5,000만 달러)에 달하는 공공투자는 철도 이용 촉진과 친환경 선박 기항을 촉진하고 있습니다.

스페인 화물 및 물류 시장 동향과 전망

E-Commerce의 급격한 성장이 소포 및 라스트 마일 배송량 증가로 이어짐

국내 온라인 소비가 지속적으로 증가하면서 CEP(택배) 배송량이 역대 최고치를 기록했습니다. DHL의 바르셀로나 완전 자동화 허브는 처리 능력을 확장하고 마감 시간을 단축하여 인구의 80%를 대상으로 익일 배송을 실현하고 있습니다. 스페인 우편공사(Correos)는 옴니채널 소매업체들이 선호하는 클릭 앤 콜렉트(Click & Collect)를 촉진하기 위해 2,400개 이상의 집배송 거점을 운영하고 있습니다. 국경 간 소포는 마드리드 바라하스 공항 게이트웨이를 통해 중국 사업자와의 제휴를 통해 아시아에서 유럽으로의 배송이 가속화되고 있습니다. 자율주행 보행로봇과 지방에서의 드론 배송 테스트는 운전자 부족을 완화하는 기술 주도형 라스트 마일 솔루션으로의 전환을 시사하고 있습니다. 이러한 노력들이 결합되어 스페인은 남유럽에서 소포 물류의 시험대라는 평가를 확고히 하고 있습니다.

제조업의 부활이 JIT 화물 수요를 견인합니다.

카탈루냐와 나바라의 자동차 공장은 시간 지정 트럭 운송 경로를 통해 부품 조달을 동기화했습니다. 이로 인해 재고 버퍼가 줄어들고, 프리미엄 서비스에 대한 수요가 증가하고 있습니다. 제약사는 적정 유통 기준(GDP)에 따라 온도 관리 API(원료의약품)를 발송하고, 실시간 추적의 필요성을 강화합니다. 일부 수출업체들은 지중해 회랑의 장거리 구간을 철도로 전환하여 배출가스 감축과 운전자 부족에 대한 대책을 추진하고 있습니다. 예측 분석 플랫폼은 제조업체가 생산량과 비용의 균형을 맞추는 데 도움이 되며, 통합된 컨트롤 타워를 통해 가시성을 제공하는 물류 제공업체를 우대합니다. 린 생산과 지속가능성에 대한 노력의 상호 작용이 복합운송의 혁신을 지속하고 있습니다.

심각한 운전자 부족과 임금 상승

스페인에서는 퇴직자가 신규 진입자를 초과하는 상황으로 인해 면허를 소지한 트럭 운전사가 약 2만 5,000명이 부족하며, 이는 운송 능력의 15%에 해당합니다. 마드리드와 카탈루냐 지역의 평균 연간 임금은 2025년 10% 상승하여 중소 운송업체들의 수익률을 압박하고 운임을 인상하고 있습니다. 살베센 로지스티카는 매일 550대의 장거리 트레일러를 운행하고 있으며, 서비스 유지를 위해 지속적인 채용 활동이 필요하고, 인력 확보 프로그램의 비용 부담을 실감할 수 있습니다. 운송 능력 부족으로 인해 화주들은 더 일찍 예약해야 하고, 가능한 경우 철도 운송으로 전환하는 경우도 볼 수 있습니다. 훈련 프로그램이 확대될 때까지 지속적인 부족은 도로 화물 운송의 성장에 구조적 제약을 가져올 것입니다.

부문 분석

2025년 기준 스페인 화물 및 물류 시장 점유율의 33.95%를 제조업이 차지하고 있으며, 자동차 생산의 호조, 화학 가공, 고부가가치 기계류 수출이 이를 뒷받침하고 있습니다. 자동차 공장은 라인 사이드 재고를 최소화하기 위해 동기화된 입고 흐름에 의존하고 있으며, 이로 인해 시퀀싱 센터와 셔틀 트럭에 대한 수요가 증가하고 있습니다.

도매 및 소매업은 매장 재고와 EC 풀필먼트를 통합하는 옴니채널 전략을 활용하여 2026년부터 2031년까지 CAGR 3.49%를 기록할 것으로 예상됩니다. 소매업체들은 실시간 재고 가시성과 늦은 주문 마감 시간을 요구하고 있으며, 도시 허브, 마이크로 풀필먼트, 라스트 마일 네트워크를 통합하는 사업자를 선호합니다. 이러한 추세에 따라 3PL 사업자들은 창고 보관, 운송, 반품 처리를 종합적인 계약으로 통합하여 고객 유지율을 높이고 있습니다.

화물 운송은 2025년 매출의 63.05%를 차지할 것으로 예상되며, 이는 스페인의 화물 및 물류 시장에서의 핵심적인 위치를 뒷받침합니다. 수요는 동국이 유로 및 지중해 무역의 관문으로서의 역할과 자동차, 의약품, FMCG(일용소비재) 유통의 거점으로서의 기능에서 기인합니다. 공장 게이트에서 항만까지의 대량 도로 운송이 처리량을 지배하는 반면, 철도 컨테이너 운송은 인프라 구축과 환경 규제 강화로 인해 증가 추세에 있습니다.

CEP(소량 배송)는 속도, 소량화물의 밀도, 정확한 추적을 요구하는 온라인 소매업의 혜택을 받아 2026년부터 2031년까지 CAGR 3.78%로 확대될 것으로 예상됩니다. 분류 자동화, 경로 계획 AI, 대체 배송 스테이션에 대한 투자가 CEP(택배) 업계 리더 기업을 기존 일반화물 운송업체와 차별화하고 있습니다. 서비스 격차의 확대는 2031년까지 스페인의 화물 및 물류 시장을 형성할 가능성이 높으며, 화물에서 소포로의 가치 전환을 촉진하고 있습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.09The Spain freight and logistics market was valued at USD 74.38 billion in 2025 and estimated to grow from USD 76.83 billion in 2026 to reach USD 90.31 billion by 2031, at a CAGR of 3.29% during the forecast period (2026-2031).

Spain's position as a Mediterranean gateway, coupled with Asia-Europe trade diversions toward western Mediterranean ports, lifts throughput at Valencia, Barcelona, and Algeciras. E-commerce proliferation enlarges parcel volumes and fuels automation investments, illustrated by DHL's EUR 350 million (USD 386 million) Barcelona hub capable of sorting 30,000 packages per hour. Manufacturing recovery, led by automotive and pharmaceuticals, intensifies just-in-time (J-I-T) freight needs and underpins road transport's 77.62% share. Public investments worth EUR 1.4 billion (USD 1.55 billion) in the Mediterranean Corridor and port LNG bunkering infrastructure are catalyzing rail uptake and greener vessel calls.

Spain Freight And Logistics Market Trends and Insights

E-Commerce Boom Powering Parcel and Last-Mile Volumes

Domestic online spending continues to climb, pushing CEP shipments to record highs. DHL's fully automated Barcelona hub scales processing capacity and trims cut-off times, enabling next-day coverage for 80% of the population. Correos has deployed more than 2,400 pickup points to facilitate click-and-collect, a model favored by omnichannel retailers. Cross-border parcels flow through Madrid-Barajas air gateway, where alliances with Chinese operators accelerate Asian deliveries into Europe. Autonomous sidewalk robots and rural drone pilots indicate a pivot toward tech-enabled last-mile solutions that mitigate driver shortages. Collectively, these initiatives consolidate Spain's reputation as a parcel logistics test bed for southern Europe.

Manufacturing Resurgence Driving J-I-T Freight Demand

Automotive plants in Catalonia and Navarra synchronize inbound components via time-definite trucking corridors, shrinking inventory buffers and lifting premium-service demand. Pharmaceutical producers dispatch temperature-sensitive APIs under Good Distribution Practice, reinforcing the need for real-time tracking. Select exporters switch long-haul legs to rail on the Mediterranean Corridor to reduce emissions and hedge against driver scarcity. Predictive analytics platforms help manufacturers balance throughput and cost, favoring logistics providers that offer integrated control-tower visibility. The interplay of lean production and sustainability pledges sustains multimodal freight innovation.

Severe Driver Shortages and Wage Inflation

Spain lacks roughly 25,000 licensed truck drivers, equal to 15% of capacity, as retirement outpaces new entrants. Average annual wages in Madrid and Catalonia rose 10% in 2025, squeezing margins for SME hauliers and lifting freight rates. Salvesen Logistica operates 550 long-haul trailers daily and must continually recruit to maintain service, illustrating the cost burden of retention programs. Capacity shortfalls compel shippers to book farther in advance, and some switch to rail where feasible. Persistent shortages pose structural limits on road freight growth until training initiatives scale.

Other drivers and restraints analyzed in the detailed report include:

- Public-Sector Spend on Mediterranean and Atlantic Corridors

- Outsourced Cold-Chain Uptake in Iberia

- Fuel-Price Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Manufacturing accounted for 33.95% of the Spain freight and logistics market share in 2025, underpinned by strong automotive output, chemical processing, and high-value machinery exports. Automotive plants rely on synchronized inbound flows to minimize line-side inventory, stimulating growth in sequencing centers and shuttle trucks.

Wholesale and retail trade, slated for a 3.49% CAGR (2026-2031), capitalizes on omnichannel strategies that fuse store inventory with e-commerce fulfillment. Retailers demand real-time stock visibility and later order cut-offs, favoring integrators that combine urban hubs, micro-fulfillment, and last-mile networks. The dynamic encourages 3PLs to bundle warehousing, transport, and returns handling into unified contracts that deepen customer stickiness.

Freight transport produced 63.05% of revenue in 2025, confirming its centrality to the Spain freight and logistics market. Demand stems from the country's role as an entry point for Euro-Mediterranean trade and a distribution base for automotive, pharma, and FMCG flows. Bulk road movements from factory gates to ports dominate volumes, while rail intermodal units rise on infrastructure upgrades and green mandates.

CEP, expanding at a projected 3.78% CAGR (2026-2031), benefits from online retail that demands speed, small-parcel density, and precise tracking. Investment in sortation automation, route-planning AI, and alternative delivery stations differentiates CEP leaders from traditional general-cargo hauliers. The widening service gap reinforces the freight-to-parcel value migration likely to shape the Spain freight and logistics market through 2031.

The Spain Freight and Logistics Market Report is Segmented by End User Industry (Agriculture, Fishing, and Forestry, Construction, Manufacturing, Oil and Gas, Mining and Quarrying, Wholesale and Retail Trade, and Others) and by Logistics Function (Courier, Express, and Parcel (CEP), Freight Forwarding, Freight Transport, Warehousing and Storage, and Other Services). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Across Logistics

- Alfil Logistics

- Americold

- Careers Logistics Group

- CMA CGM Group (Including CEVA Logistics)

- Correos

- DHL Group

- DSV A/S (Including DB Schenker)

- FedEx

- GEODIS

- Geopost (including DPD Group and SEUR)

- Grupo Sese

- ID Logistics

- Kuehne+Nagel

- Lineage, Inc.

- Marcotran

- Rhenus Group

- Salvesen Logistica SA

- TSB Trans

- United Parcel Service of America, Inc. (UPS)

- XPO, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Demographics

- 4.3 GDP Distribution by Economic Activity

- 4.4 GDP Growth by Economic Activity

- 4.5 Inflation

- 4.6 Economic Performance and Profile

- 4.6.1 Trends in E-Commerce Industry

- 4.6.2 Trends in Manufacturing Industry

- 4.7 Transport and Storage Sector GDP

- 4.8 Export Trends

- 4.9 Import Trends

- 4.10 Fuel Price

- 4.11 Trucking Operational Costs

- 4.12 Trucking Fleet Size by Type

- 4.13 Major Truck Suppliers

- 4.14 Logistics Performance

- 4.15 Modal Share

- 4.16 Maritime Fleet Load Carrying Capacity

- 4.17 Liner Shipping Connectivity

- 4.18 Port Calls and Performance

- 4.19 Freight Pricing Trends

- 4.20 Freight Tonnage Trends

- 4.21 Infrastructure

- 4.22 Regulatory Framework (Road and Rail)

- 4.23 Regulatory Framework (Sea and Air)

- 4.24 Value Chain and Distribution Channel Analysis

- 4.25 Market Drivers

- 4.25.1 E-Commerce Boom Powering Parcel and Last-Mile Volumes

- 4.25.2 Manufacturing Resurgence Driving J-I-T Freight Demand

- 4.25.3 Public-Sector Spend on Mediterranean and Atlantic Corridors

- 4.25.4 Outsourced Cold-Chain Uptake in Iberia

- 4.25.5 LNG Bunkering Infrastructure in Major Ports

- 4.25.6 Logistics Real-Estate Yield Compression Spurring Supply

- 4.26 Market Restraints

- 4.26.1 Severe Driver Shortages and Wage Inflation

- 4.26.2 Fuel-Price Volatility

- 4.26.3 Peak-Season Port Bottlenecks for Reefer Cargo

- 4.26.4 Slow Customs Digitalisation for Canary Flows

- 4.27 Technology Innovations in the Market

- 4.28 Porter's Five Forces Analysis

- 4.28.1 Threat of New Entrants

- 4.28.2 Bargaining Power of Buyers

- 4.28.3 Bargaining Power of Suppliers

- 4.28.4 Threat of Substitutes

- 4.28.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 End User Industry

- 5.1.1 Agriculture, Fishing, and Forestry

- 5.1.2 Construction

- 5.1.3 Manufacturing

- 5.1.4 Oil and Gas, Mining and Quarrying

- 5.1.5 Wholesale and Retail Trade

- 5.1.6 Others

- 5.2 Logistics Function

- 5.2.1 Courier, Express, and Parcel (CEP)

- 5.2.1.1 By Destination Type

- 5.2.1.1.1 Domestic

- 5.2.1.1.2 International

- 5.2.1.1 By Destination Type

- 5.2.2 Freight Forwarding

- 5.2.2.1 By Mode of Transport

- 5.2.2.1.1 Air

- 5.2.2.1.2 Sea and Inland Waterways

- 5.2.2.1.3 Others

- 5.2.2.1 By Mode of Transport

- 5.2.3 Freight Transport

- 5.2.3.1 By Mode of Transport

- 5.2.3.1.1 Air

- 5.2.3.1.2 Pipelines

- 5.2.3.1.3 Rail

- 5.2.3.1.4 Road

- 5.2.3.1.5 Sea and Inland Waterways

- 5.2.3.1 By Mode of Transport

- 5.2.4 Warehousing and Storage

- 5.2.4.1 By Temperature Control

- 5.2.4.1.1 Non-Temperature Controlled

- 5.2.4.1.2 Temperature Controlled

- 5.2.4.1 By Temperature Control

- 5.2.5 Other Services

- 5.2.1 Courier, Express, and Parcel (CEP)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Across Logistics

- 6.4.2 Alfil Logistics

- 6.4.3 Americold

- 6.4.4 Careers Logistics Group

- 6.4.5 CMA CGM Group (Including CEVA Logistics)

- 6.4.6 Correos

- 6.4.7 DHL Group

- 6.4.8 DSV A/S (Including DB Schenker)

- 6.4.9 FedEx

- 6.4.10 GEODIS

- 6.4.11 Geopost (including DPD Group and SEUR)

- 6.4.12 Grupo Sese

- 6.4.13 ID Logistics

- 6.4.14 Kuehne+Nagel

- 6.4.15 Lineage, Inc.

- 6.4.16 Marcotran

- 6.4.17 Rhenus Group

- 6.4.18 Salvesen Logistica SA

- 6.4.19 TSB Trans

- 6.4.20 United Parcel Service of America, Inc. (UPS)

- 6.4.21 XPO, Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment