|

시장보고서

상품코드

1939095

영국의 석유 및 가스 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)United Kingdom Oil And Gas - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

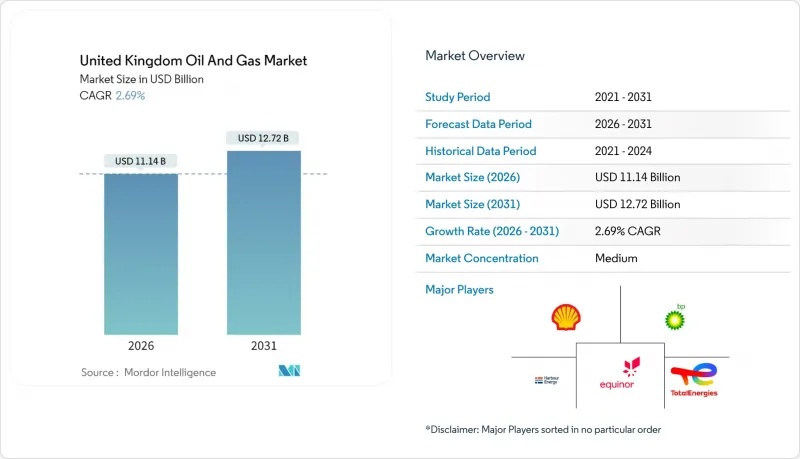

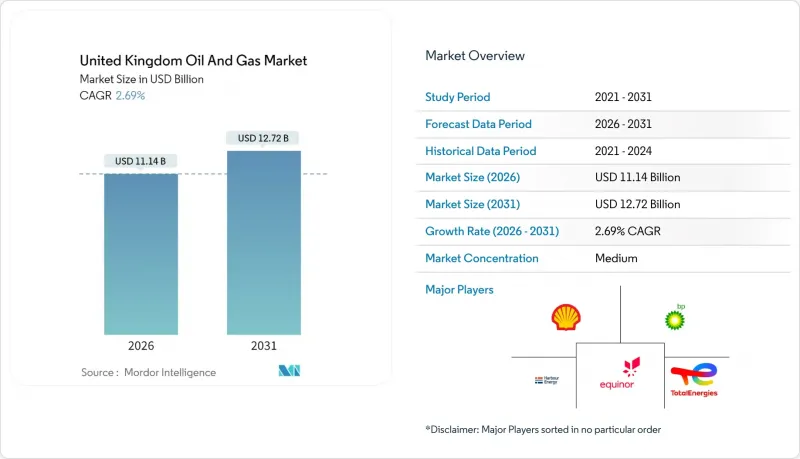

영국의 석유 및 가스 시장은 2025년 108억 5,000만 달러에서 2026년에는 111억 4,000만 달러로 성장하며, 2026-2031년에 CAGR 2.69%로 추이하며, 2031년까지 127억 2,000만 달러에 달할 것으로 예측됩니다.

성숙한 북해 유전에서 최대한의 가치를 끌어내는 전략적 전환과 신규 탐사 속도를 의도적으로 늦추는 것이 이러한 꾸준한 확장을 지원하고 있습니다. 사업자들은 2020년 이후 채굴 비용을 15-20% 절감하여 재정적 부담이 증가하는 상황에서도 수익성을 유지하고 있습니다. 2024년 투자액은 규제 당국의 예상보다 1.5배 높은 60억 파운드를 넘어섰으며, 주로 수명 연장 프로그램과 탄소 포집 인프라를 지원하는 미드스트림 공정의 업그레이드에 사용되었습니다. 독립 기업 간 통합이 가속화되고, 총 20억 달러가 넘는 2건의 주목할 만한 인수합병이 이루어졌습니다. 이를 통해 비용 시너지를 창출하고 폐업의 효율성을 높였습니다. 동시에 해상 풍력발전의 시험 운영과 플랫폼의 전기화를 통해 디젤 연료 소비를 줄이고, 배출 규제 준수와 생산 안정성을 동시에 달성할 수 있음을 입증했습니다.

영국 석유 및 가스 시장 동향과 인사이트

북해의 채굴 비용 절감으로 운영 효율성 향상

북해의 채굴 비용이 크게 하락하여 세계 에너지 시장의 도전 속에서 영국 사업자에게 경쟁 우위를 가져다주고 있습니다. 해저 시스템의 기술적 혁신과 시추 기술 향상으로 2020년 이후 배럴당 채굴 비용이 15-20% 절감되어 재정적 압박이 가중되는 상황에서도 생산의 지속가능성을 유지할 수 있게 되었습니다. 이러한 비용 절감의 궤적은 특히 에너지 안보에 대한 우려가 높아지는 가운데 국내 생산의 가치가 상승하면서 영국 유전이 국제적인 대안에 비해 유리한 위치에 놓이게 되었습니다. 효율성 향상은 첨단 저류층 관리 시스템과 최적화된 생산 스케줄링을 통해 회수율을 극대화하고 운영비용을 최소화하는 등 효율성이 향상되었습니다. 사업자들은 이러한 비용 개선을 통해 수익성 저하로 인해 조기 폐기될 가능성이 있는 성숙 자산에 대한 지속적인 투자를 정당화하고 유전의 수명을 연장하는 데 활용하고 있습니다.

영국 북해이동협정의 인센티브가 투자 우선순위를 재구성

영국 북해 전환 협정은 순배출량 제로 목표를 향해 측정 가능한 진전을 보이는 사업자에게 체계적인 재정적 인센티브를 제공함으로써 업계 전반의 자본 배분 결정에 근본적인 변화를 가져왔습니다. 투자 공제 및 강화된 감가상각율은 탄소 포집, 이용 및 저장(CCUS) 기술을 사업에 통합하는 기업을 장려하고, 대상 프로젝트는 적격 지출의 최대 40%에 해당하는 가속화된 세제 혜택을 받을 수 있습니다. 이 정책 프레임워크는 2024년 이후 20억 파운드 이상의 CCUS 투자를 약속하고 있으며, 기존에 수익성이 없던 프로젝트가 실현 가능한 개발 기회로 전환되고 있습니다. 이 협정은 배출량 감축에 있으며, 기술적 리더십을 보이는 사업자에게 경쟁 우위를 제공하고, 저탄소 탄화수소 생산으로의 전환을 효과적으로 지원합니다. ISO 14001 환경경영 인증은 이러한 혜택을 받기 위해 점점 더 중요해지고 있으며, 기업은 컴플라이언스 프로세스에 많은 투자를 하고 있습니다.

가속화된 CCS 과세로 인해 사업자의 현금 흐름이 압박을 받고 있습니다.

업스트림 사업자에 대한 탄소 포집 및 저장(CCS) 과징금 조기 도입으로 영국 대륙붕 전역에 즉각적인 재정적 압박이 발생하고 있습니다. 주요 생산업체들의 컴플라이언스 비용은 연간 1억 5천만-2억 파운드에 달하는 것으로 추산됩니다. 이 규제 프레임워크는 개별 프로젝트 참여 여부와 관계없이 사업자가 국가 CCS 인프라 구축에 기여하도록 의무화하고 있으며, 산업별 과세를 통해 광범위한 에너지 전환 목표를 실질적으로 보조하는 구조로 되어 있습니다. 이러한 부과 구조는 추가 비용을 흡수할 수 있는 규모를 갖추지 못한 중소 독립 사업자에게 불균형적으로 영향을 미치고, 한계 사업자가 대규모 파트너를 찾거나 시장에서 완전히 철수하는 움직임을 가속화할 수 있습니다. 부과 요건을 준수하기 위해서는 모니터링 및 보고 기능이 강화되어야 하며, 이는 운영상의 복잡성을 증가시키고 리소스를 더욱 압박하게 됩니다.

부문 분석

2025년 업스트림 부문이 71.65%의 압도적인 시장 점유율을 차지한다는 것은 영국 석유 및 가스 사업에서 채굴 활동이 여전히 핵심적인 역할을 하고 있음을 보여줍니다. 그러나 중류 부문이 2031년까지 4.18%의 연평균 복합 성장률(CAGR)을 보일 것이라는 점은 인프라 및 가공 투자에 대한 근본적인 전환을 의미합니다. 업스트림 활동은 북해 자산의 가치를 극대화하는 유전 수명 연장 프로그램, 향상된 채유 기술 및 기존 북해 자산의 가치를 극대화하는 프로그램의 혜택을 누리고 있습니다. 하버 에너지와 같은 사업자들은 2024년 생산 능력 통합을 위해 13억 달러 이상을 자산 인수에 투자했습니다. 중류 부문의 성장 가속화는 탄소 포집-이용-저장(CCUS) 프로젝트에 필요한 핵심 인프라에 기인하며, CO2 수송 및 수소 생산을 위해 파이프라인 네트워크와 처리 시설의 대대적인 업그레이드가 요구되고 있습니다. 다운스트림 사업은 정제제품 수요로 안정적인 실적을 유지하고 있지만, 전기화 추세와 재생 연료 의무화로 인한 장기적인 역풍을 맞고 있습니다.

중류 인프라 투자는 특히 동해안 클러스터에 집중되어 있으며, 케라스 미드스트림의 H2NorthEast 시설은 1GW의 블루 수소 생산 능력을 갖추고 있으며, 이를 위해 대규모 파이프라인 개보수 및 신규 압축 스테이션 설치가 필수적입니다. 영국 석유 및 가스 시장의 중류 사업 규모는 2025년 21억 9,000만 달러에 달할 것으로 예상되며, 연간 성장률은 업계 평균보다 1.5% 포인트 더 높을 것으로 예측됩니다. 영국의 가스 수송 시스템은 7,600km가 넘는 고압 파이프라인 네트워크를 보유하고 있으며, 내셔널 그리드는 연간 25억 파운드를 네트워크 유지 및 강화 프로젝트에 투자하고 있습니다. 이는 기존 가스 수송과 새로운 수소 응용 분야 모두를 지원하고 있습니다. 부유식 생산저장하역설비(FPSO)의 도입으로 처리능력이 확대되어 기존에는 개발이 어려웠던 매장량 개발이 가능해졌습니다. 한편, 저장 인프라는 전략적 석유 비축 요건과 계절적 수요 평준화 요구의 혜택을 받고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSA 26.03.05The United Kingdom Oil And Gas market is expected to grow from USD 10.85 billion in 2025 to USD 11.14 billion in 2026 and is forecast to reach USD 12.72 billion by 2031 at 2.69% CAGR over 2026-2031.

A strategic shift toward squeezing maximum value from mature North Sea reservoirs, paired with a deliberate slowdown in greenfield exploration, underpins this measured expansion. Operators have reduced lifting costs by 15-20% since 2020, thereby protecting profitability even as fiscal burdens increase. The 2024 investment outlay of more than £6 billion, half again above regulator expectations, flowed mainly into life-extension programs and midstream upgrades that support carbon-capture infrastructure. Consolidation among independents accelerated, with two headline acquisitions totaling more than USD 2 billion, unlocking cost synergies and decommissioning efficiencies. At the same time, floating-wind pilots and on-platform electrification cut diesel burn, proving that emissions compliance and production stability can coexist.

United Kingdom Oil And Gas Market Trends and Insights

Declining North Sea Lifting Costs Drive Operational Efficiency

North Sea lifting costs have decreased substantially, creating competitive advantages for UK operators amid global energy market challenges. Technological breakthroughs in subsea systems and enhanced drilling techniques have cut per-barrel extraction costs by 15-20% since 2020, sustaining production viability despite heightened fiscal pressures. This cost reduction trajectory positions UK fields favorably against international alternatives, particularly as energy security concerns elevate domestic production value. The efficiency gains result from advanced reservoir management systems and optimized production scheduling, which maximize recovery rates while minimizing operational expenses. Operators leverage these cost improvements to extend field life and justify continued investment in mature assets that might otherwise face early decommissioning.

UK North Sea Transition Deal Incentives Reshape Investment Priorities

The UK North Sea Transition Deal offers structured fiscal incentives to operators demonstrating measurable progress toward net-zero emissions targets, thereby fundamentally altering capital allocation decisions across the sector. Investment allowances and enhanced depletion rates reward companies that integrate carbon capture, utilization, and storage technologies into their operations, with qualifying projects receiving accelerated tax relief worth up to 40% of eligible expenditures. This policy framework has catalyzed over £2 billion in committed CCUS investments since 2024, transforming previously uneconomical projects into viable development opportunities. The deal creates competitive advantages for operators demonstrating technological leadership in emissions reduction, effectively subsidizing the transition toward lower-carbon hydrocarbon production. ISO 14001 environmental management certification has become increasingly critical for accessing these incentives, with operators investing heavily in compliance processes.

Accelerated CCS Levy Strains Operator Cash Flows

The introduction of accelerated carbon capture and storage levies on upstream operators has created immediate financial pressure across the UK Continental Shelf, with compliance costs estimated at £150-200 million annually for major producers. This regulatory framework requires operators to contribute to national CCS infrastructure development regardless of their individual project participation, effectively subsidizing broader energy transition objectives through sector-specific taxation. The levy structure disproportionately impacts smaller independents who lack the scale to absorb these additional costs, potentially accelerating consolidation as marginal operators seek larger partners or exit the market entirely. Compliance with the levy requirements demands enhanced monitoring and reporting capabilities, which add operational complexity and further strain resources.

Other drivers and restraints analyzed in the detailed report include:

- Floating Wind Platform Integration Reduces Operational Carbon Intensity

- Teesside and Humber Industrial Clusters Create Blue Hydrogen Demand

- Offshore Wind Grid Integration Reduces Peak Gas Demand

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The upstream segment's commanding 71.65% market share in 2025 reflects the continued centrality of extraction activities to UK oil and gas operations, yet the midstream segment's 4.18% CAGR through 2031 signals a fundamental shift toward infrastructure and processing investments. Upstream activities benefit from enhanced recovery techniques and extended field life programs that maximize value from existing North Sea assets. Operators like Harbour Energy have invested over USD 1.3 billion in asset acquisitions during 2024 to consolidate production capabilities. The midstream segment's accelerated growth stems from critical infrastructure requirements for carbon capture, utilization, and storage projects, with pipeline networks and processing facilities requiring substantial upgrades to handle CO2 transport and hydrogen production. Downstream operations maintain steady performance through refined product demand, though the segment faces long-term headwinds from electrification trends and renewable fuel mandates.

Midstream infrastructure investments are particularly concentrated in the East Coast Cluster, where Kellas Midstream's H2NorthEast facility represents a 1 GW blue hydrogen production capability that necessitates extensive pipeline modifications and the installation of new compression stations. The UK oil and gas market size for midstream operations reached USD 2.19 billion in 2025, with annual growth rates exceeding the sector average by 1.5 percentage points. The UK's gas transmission system spans over 7,600 km of high-pressure pipelines, with National Grid investing £2.5 billion annually in network maintenance and enhancement projects that support both traditional gas transport and emerging hydrogen applications. Processing capabilities are expanding through the deployment of floating production, storage, and offloading vessels, which enable the development of previously stranded reserves. Meanwhile, storage infrastructure benefits from strategic petroleum reserve requirements and seasonal demand balancing needs.

The United Kingdom Oil and Gas Market is Segmented by Sector (Upstream, Downstream, and Midstream), Location (Onshore and Offshore), and Service (Construction, Maintenance and Turn-Around, and Decommissioning). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Shell plc

- BP plc

- Harbour Energy plc

- TotalEnergies SE

- Equinor ASA

- Chevron Corp.

- Centrica plc

- Valaris plc

- INEOS Group Ltd

- ConocoPhillips UK Ltd

- EnQuest plc

- Ithaca Energy plc

- Neptune Energy Group

- Cadent Gas Ltd

- Dana Petroleum Ltd

- ESSO UK Ltd

- BG Group Ltd

- Premier Oil (Chrysaor)

- Wood plc

- Subsea 7 SA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Declining North Sea lifting costs

- 4.2.2 UK "North Sea Transition Deal" incentives

- 4.2.3 Surge in floating-wind-powered platforms (E&P cost cuts)

- 4.2.4 Re-industrialisation of Teesside & Humber (blue hydrogen demand)

- 4.2.5 AI-enabled seismic imaging success rates

- 4.3 Market Restraints

- 4.3.1 Accelerated CCS levy on upstream operators

- 4.3.2 Grid-connected offshore wind cannibalising peak-time gas demand

- 4.3.3 Heightened decommissioning bond requirements

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Crude-Oil Production & Consumption Outlook

- 4.8 Natural-Gas Production & Consumption Outlook

- 4.9 Installed Pipeline Capacity Analysis

- 4.10 Unconventional Resources CAPEX Outlook (tight oil, oil sands, deep-water)

- 4.11 Porter's Five Forces

- 4.11.1 Bargaining Power of Suppliers

- 4.11.2 Bargaining Power of Consumers

- 4.11.3 Threat of New Entrants

- 4.11.4 Threat of Substitutes

- 4.11.5 Intensity of Competitive Rivalry

- 4.12 PESTLE Analysis

5 Market Size & Growth Forecasts

- 5.1 By Sector

- 5.1.1 Upstream

- 5.1.2 Midstream

- 5.1.3 Downstream

- 5.2 By Location of Deployment

- 5.2.1 Onshore

- 5.2.2 Offshore

- 5.3 By Service

- 5.3.1 Construction

- 5.3.2 Maintenance and Turn-around

- 5.3.3 Decommissioning

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Shell plc

- 6.4.2 BP plc

- 6.4.3 Harbour Energy plc

- 6.4.4 TotalEnergies SE

- 6.4.5 Equinor ASA

- 6.4.6 Chevron Corp.

- 6.4.7 Centrica plc

- 6.4.8 Valaris plc

- 6.4.9 INEOS Group Ltd

- 6.4.10 ConocoPhillips UK Ltd

- 6.4.11 EnQuest plc

- 6.4.12 Ithaca Energy plc

- 6.4.13 Neptune Energy Group

- 6.4.14 Cadent Gas Ltd

- 6.4.15 Dana Petroleum Ltd

- 6.4.16 ESSO UK Ltd

- 6.4.17 BG Group Ltd

- 6.4.18 Premier Oil (Chrysaor)

- 6.4.19 Wood plc

- 6.4.20 Subsea 7 SA

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment