|

시장보고서

상품코드

1939747

베트남의 폐기물 관리 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Vietnam Waste Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

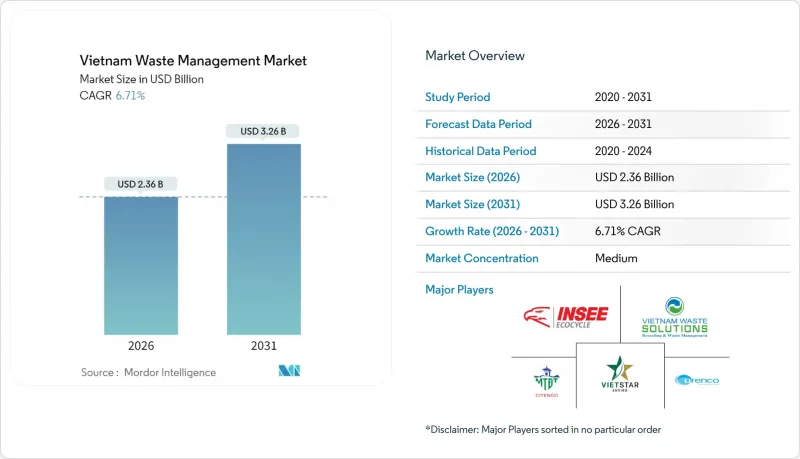

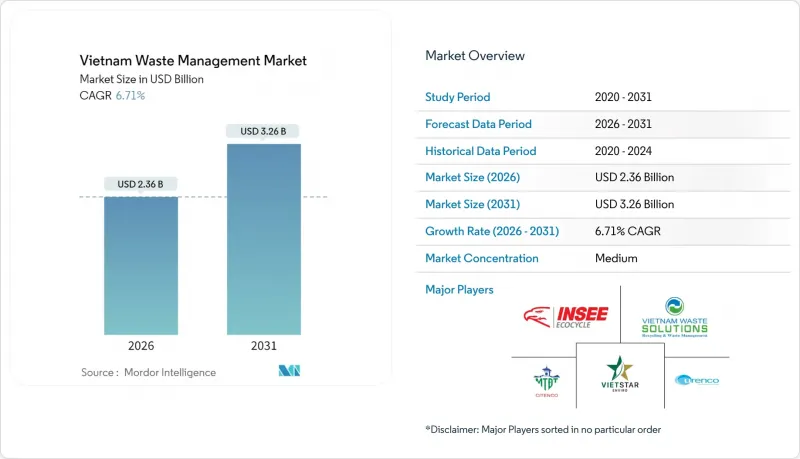

베트남 폐기물 관리 시장 규모는 2026년에 23억 6,000만 달러로 추정됩니다.

이는 2025년 22억 1,000만 달러에서 성장한 수치이며, 2031년에는 32억 6,000만 달러에 달할 것으로 예상됩니다. 2026년부터 2031년까지 CAGR 6.71%로 성장할 것으로 예상됩니다.

가속화되는 도시화, 강화되는 환경 규제, 국가 순환형 경제 로드맵은 수요 구조를 지속적으로 변화시키고 있습니다. 한편, 확대된 생산자책임재활용(EPR) 제도는 제조업체를 공식적인 재활용 경로로 유도하고 있습니다. 공중보건 캠페인과 디지털 경로 최적화 도구를 통해 호치민시와 하노이에서 발생원 분리율이 향상되어 고도처리를 위한 새로운 처리량을 창출하고 있습니다. 외국인 직접투자가 증가함에 따라 폐기물 에너지화, 폴리에스터에서 폴리에스터로 재활용, 고순도 퇴비화 기술이 지방 시장에 도입되고 있습니다. 한편, 프로젝트 개발자는 토지 취득 장벽, 지방의 수집망 부족, 지방정부의 예산 제약 등의 문제를 해결해야 하며, 이 모든 것이 인프라 구축의 지연 요인으로 작용하고 있습니다.

베트남 폐기물 관리 시장 동향 및 전망

2030년까지 폐기물 수거율 85%를 목표로 하는 국가 순환경제 로드맵

2030 순환경제 행동계획에 따라 베트남은 도시지역 95%, 농촌지역 80%의 폐기물 수거율을 달성하고 매립률을 50% 미만으로 낮추는 것을 목표로 하고 있습니다. 본 전략은 바이오매스와 도시쓰레기를 재생에너지 목표와 연계하여 폐기물 에너지화 사업자에게 정부 공인 수익기반을 제공합니다. 농업 분야에서는 연간 9,361만 톤의 폐기물이 발생하지만 재사용률은 52%에 불과합니다. 현행 규정은 2025년까지 유기질 비료 생산량을 25% 증가시키고, 2030년까지 전체 등록 비료의 30%를 유기질 비료로 만들 것을 요구하고 있습니다. 이러한 목표는 농촌의 소득 향상과 배출량 감축 목표를 통합한 것으로, 바이오차르와 퇴비화 사업을 위한 농지 시장을 개척하고 있습니다. 수거 목표가 상향 조정되면서 베트남 폐기물 관리 시장에서 원료의 가시성이 높아져 지역 처리 기지의 자금 조달 가능성이 향상되고 있습니다.

환경 규제 강화 및 집행

베트남의 법적 체계는 현재 법령 05/2025/ND-CP, 결정 611/QD-TTg, 결정 11/2025/QD-TTg를 중심으로 구성되어 있으며, 각 법령은 보다 엄격한 EPR 의무, 지역별 처리 구역 목표, 오염자 부담 회수 규칙을 도입하고 있습니다. 새로운 제도에서는 수익 면제 기준액이 상향 조정되고, 24개 인증 재활용업체가 정식으로 인가되며, 폐기물 사고 발생 당사자에게 복구 비용 전액을 부담하도록 의무화됩니다. 이러한 규제로 인해 소규모 사업자는 컴플라이언스 강화를 위한 자금 조달에 어려움을 겪는 반면, 통합형 사업자는 규모의 경제를 통해 수익을 창출할 수 있기 때문에 시장 통합이 가속화될 것입니다. 예측 가능한 시행으로 규제 리스크가 감소하고, 대규모 처리 시설에 대한 장기적인 자금 조달이 가능해집니다. 그 결과, 베트남 폐기물 관리 시장의 중기적 확장을 뒷받침하는 보다 명확하고 투자 적격성이 높은 환경이 조성될 것입니다.

매립지 용량 제한 및 부지 확보 장벽

닥꽁성 덕랍 매립지 등은 설계 용량을 초과하여 가동되고 있으며, 다오냐이 매립지 등 대체 프로젝트도 토지 취득 문제로 인해 완공이 지연되어 2025년 말로 연기되었습니다. 호치민시에는 이미 4곳의 처리시설이 1,670헥타르에 달하지만, 이전 합의에 따라 의무화된 완충지대가 부족하여 확장에 제약이 있습니다. 폐기물 발전 사업자는 더 넓은 부지와 특별 구역 지정을 필요로 하고 있으며, 승인 절차가 더욱 복잡해지고 일정이 길어지고 있습니다. 도시 주변부의 토지 부족은 토지 취득 비용을 높이고, 사업자에게는 초기 투자비용이 크고 고도의 기술력을 필요로 하는 고밀도 기술이나 수직기술로의 전환을 강요하고 있습니다.

부문 분석

2025년 기준, 베트남 폐기물 관리 시장 점유율의 55.12%는 주거용 폐기물이 차지하고 있습니다. 이는 예측 가능한 고밀도 경로로 발생하는 폐기물을 생성하는 도시 인구의 증가에 따른 결과입니다. 이를 통해 지자체 운영자는 수거시간의 최적화와 쓰레기통의 표준화를 실현하고, 가구당 비용 절감과 처리설비 업그레이드를 위한 자금을 확보하는 데 성공했습니다. 상업용 폐기물 분야의 베트남 폐기물 관리 시장 규모는 현재 소규모이지만, 2급 도시의 쇼핑센터, 물류기지, 숙박시설의 증가에 따라 2031년까지 CAGR 7.92%로 확대될 것으로 예상됩니다. 상업 고객들은 주말 수거 및 안전한 파쇄 처리와 같은 고수익 프리미엄 서비스 패키지도 받아들이고 있습니다.

산업폐기물, 의료 폐기물, 건설폐기물이 나머지 점유율을 차지하고 있으며, 각 분야별로 전문적인 수익원을 개척하고 있습니다. 유해 폐기물 처리 업체는 용제 및 슬러지 처리 인증 프리미엄을 획득하고, 백산성 병원은 결정 33/2025/QD-UBND의 엄격한 분류 규정을 준수해야 합니다. 고무 생산자들은 폐수 슬러지를 유기질 비료로 전환하기 시작했으며, 농업 분야에서 업사이클링의 가능성을 보여주고 있습니다. 정책적 압력이 강화됨에 따라 이러한 하위 부문은 확대될 것이며, 주택 폐기물 처리량은 베트남 폐기물 관리 시장 전체에서 차량 가동률의 기반이 될 것입니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측(금액, 단위 : 10억 달러)

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.09Vietnam Waste Management Market size in 2026 is estimated at USD 2.36 billion, growing from 2025 value of USD 2.21 billion with 2031 projections showing USD 3.26 billion, growing at 6.71% CAGR over 2026-2031.

Accelerating urbanization, tighter environmental laws, and a national circular-economy roadmap continue to reshape demand, while extended-producer-responsibility (EPR) rules nudge manufacturers toward formal recycling channels. Public-health campaigns and digital route-optimization tools are raising source-separation rates in Ho Chi Minh City and Hanoi, creating new volumes for advanced treatment. Rising foreign direct investment is bringing waste-to-energy, polyester-to-polyester recycling, and high-purity composting technologies to provincial markets. At the same time, project developers must work around land-acquisition hurdles, rural collection gaps, and constrained provincial budgets, all of which slow down infrastructure roll-outs.

Vietnam Waste Management Market Trends and Insights

National Circular-Economy Roadmap Targeting 85% Waste Collection by 2030

Under the 2030 circular-economy action plan, Vietnam aims for 95% urban and 80% rural waste collection, while cutting landfill use below 50%. The strategy also links biomass and municipal waste to renewable-energy targets, giving waste-to-energy developers a government-endorsed revenue story. Agriculture generates 93.61 million tons of waste annually, yet just 52% is reused; regulations now call for a 25% jump in organic-fertilizer output by 2025 and a 30% organic share of all registered fertilizers by 2030. These targets integrate rural income growth with emissions goals, opening farmland markets for biochar and compost initiatives. As collection targets rise, the Vietnam waste management market gains visibility on feedstock volumes, improving bankability for regional treatment hubs.

Tightening Environmental Legislation & Enforcement

Vietnam's legal framework now revolves around Decree 05/2025/ND-CP, Decision 611/QD-TTg, and Decision 11/2025/QD-TTg, each introducing stricter EPR obligations, regional treatment-zone targets, and polluter-pays recovery rules. The new regime lifts revenue-exemption thresholds, formalizes 24 certified recyclers, and assigns full restoration costs to parties causing waste incidents. These rules accelerate market consolidation because smaller operators struggle to finance compliance upgrades, while integrated players monetize economies of scale. Predictable enforcement also reduces regulatory risk, unlocking long-tenor funding for large treatment plants. The net effect is a clearer, more investable backdrop that underpins the Vietnam waste management market's medium-term expansion.

Limited Landfill Capacity & Land-Acquisition Hurdles

Sites such as Dak R'lap in Dak Nong are operating beyond design limits because replacement projects like Dao Nghia remain stalled over land clearance, pushing completion to late 2025. In Ho Chi Minh City, four treatment complexes already span 1,670 ha, yet buffers mandated in earlier agreements are missing, constraining expansion. Waste-to-energy developers need larger footprints and special zoning, adding another layer of approvals that extends timelines. Scarcity of peri-urban land raises acquisition costs, forcing operators to pivot toward high-density or vertical technologies that demand larger upfront capital and more technical skill.

Other drivers and restraints analyzed in the detailed report include:

- Foreign-Investor-Led Technology Transfer in Waste-to-Energy Projects

- Rising Public-Health Awareness & Urban Cleanliness Campaigns

- Capital Constraints for Provincial Waste-Infrastructure Upgrades

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Residential streams held 55.12% of the Vietnam waste management market share in 2025, underpinned by an expanding urban population that generated predictable, route-dense tonnage. As a result, municipal operators have optimized pick-up times and standardized bins, bringing down per-household costs and freeing capital for treatment upgrades. The Vietnam waste management market size for commercial waste is much smaller today, yet it is forecast to rise at an 7.92% CAGR through 2031 as shopping centers, logistics hubs, and hospitality venues multiply across Tier-2 cities. Commercial clients also accept premium service packages, such as weekend pick-up and secure shredding, that carry higher margins.

Industrial, medical, and construction waste together account for the remaining share, yet each niche opens specialized revenue streams. Hazardous-waste contractors earn certification premiums to handle solvents and sludge, while hospitals in Bac Giang must conform to Decision 33/2025/QD-UBND's strict segregation rules. Rubber producers have begun converting wastewater sludge into organic fertilizer, signaling agricultural up-cycling potential. With policy pressure mounting, these sub-segments will scale, but residential tonnage will continue to anchor fleet utilization across the Vietnam waste management market.

The Vietnam Waste Management Market Report is Segmented by Source (Residential, Commercial, Industrial, and More), by Service Type (Collection/Transportation/Sorting, and More), by Waste Type (Municipal Solid Waste, Industrial Hazardous Waste, E-Waste, Plastic Waste, Biomedical Waste, and More), and by Geography (Ho Chi Minh City, Hanoi, Da Nang, Rest of Vietnam). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- CITENCO

- URENCO (Urban Environment Company Hanoi)

- INSEE Ecocycle

- Vietnam Waste Solutions

- Vietstar Environment

- Tetra Tech Coffey Vietnam

- Thuan Thanh Environment JSC

- Sonadezi Services JSC

- DUYTAN Plastic Recycling

- Green Environment Production Services Trade Co. Ltd

- Vietnam Australia Environment JSC

- SGS Vietnam

- Tan Phat Tai Co. Ltd

- An Phat Holdings (AnEco)

- Ha Noi Urban Environment Co. Ltd

- Bac Ninh Clean & Environment JSC

- TKV Waste Treatment Centre

- Holcim Vietnam Geocycle

- Indovin Power (Waste-to-Energy)

- Green Growth Asia Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Tightening environmental legislation & enforcement

- 4.2.2 Rising public health awareness & urban cleanliness campaigns

- 4.2.3 National circular-economy roadmap targeting 85 % waste collection by 2030

- 4.2.4 Foreign-investor led technology transfer in waste-to-energy projects

- 4.2.5 Extended Producer Responsibility (EPR) expansion to packaging & electronics

- 4.3 Market Restraints

- 4.3.1 Limited landfill capacity & land-acquisition hurdles

- 4.3.2 Capital constraints for provincial waste-infrastructure upgrades

- 4.3.3 Fragmented collection system in rural communes

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Force Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Values, In USD Billion)

- 5.1 By Source

- 5.1.1 Residential

- 5.1.2 Commercial (retail, office, etc.)

- 5.1.3 Industrial

- 5.1.4 Medical (Health and Pharmaceutical)

- 5.1.5 Construction & Demolition

- 5.1.6 Others (institutional, agricultural, etc)

- 5.2 By Service Type

- 5.2.1 Collection, Transportation, Sorting & Segregation

- 5.2.2 Disposal / Treatment

- 5.2.2.1 Landfill

- 5.2.2.2 Recycling & Resource Recovery

- 5.2.2.3 Incineration & Waste-to-Energy

- 5.2.2.4 Others (Chemical Treatment, Composting, etc.)

- 5.2.3 Others (Consulting, Audit & Training, etc.)

- 5.3 By Waste Type

- 5.3.1 Municipal Solid Waste

- 5.3.2 Industrial Hazardous Waste

- 5.3.3 E-waste

- 5.3.4 Plastic Waste

- 5.3.5 Biomedical Waste

- 5.3.6 Construction & Demolition Waste

- 5.3.7 Agricultural Waste

- 5.3.8 Other Specialized Waste (radio active, etc)

- 5.4 By Geography

- 5.4.1 Ho Chi Minh City

- 5.4.2 Hanoi

- 5.4.3 Da Nang

- 5.4.4 Rest of Vietnam

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 CITENCO

- 6.4.2 URENCO (Urban Environment Company Hanoi)

- 6.4.3 INSEE Ecocycle

- 6.4.4 Vietnam Waste Solutions

- 6.4.5 Vietstar Environment

- 6.4.6 Tetra Tech Coffey Vietnam

- 6.4.7 Thuan Thanh Environment JSC

- 6.4.8 Sonadezi Services JSC

- 6.4.9 DUYTAN Plastic Recycling

- 6.4.10 Green Environment Production Services Trade Co. Ltd

- 6.4.11 Vietnam Australia Environment JSC

- 6.4.12 SGS Vietnam

- 6.4.13 Tan Phat Tai Co. Ltd

- 6.4.14 An Phat Holdings (AnEco)

- 6.4.15 Ha Noi Urban Environment Co. Ltd

- 6.4.16 Bac Ninh Clean & Environment JSC

- 6.4.17 TKV Waste Treatment Centre

- 6.4.18 Holcim Vietnam Geocycle

- 6.4.19 Indovin Power (Waste-to-Energy)

- 6.4.20 Green Growth Asia Corp.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment