|

시장보고서

상품코드

1940765

미국의 FTL(Full-Truck-Load) : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)United States Full-Truck-Load (FTL) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

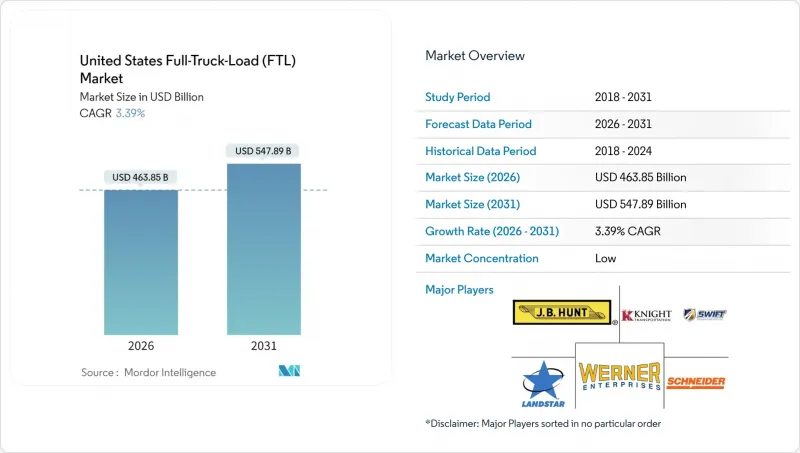

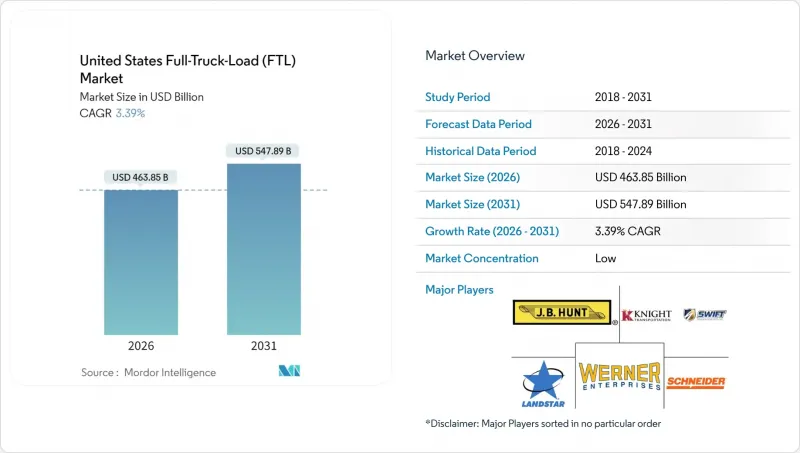

미국의 FTL(Full-Truck-Load) 시장은 2025년 4,486억 5,000만 달러에서 2026년에는 4,638억 5,000만 달러에 이르고, 2026-2031년 CAGR 3.39%로 성장을 지속하여 2031년까지 5,478억 9,000만 달러에 달할 것으로 예측됩니다.

이러한 성장은 전자상거래의 소량화, 근해 제조, 전용 계약 운송 증가로 형성된 탄탄한 화물 구성에 기인합니다. 운전자 부족과 디젤 가격 변동이 계속되는 가운데, 운송 회사는 예측 가능한 일정에 따라 유통 센터를 보충하는 밀집된 배송 회랑에 대응하기 위해 네트워크 조정을 계속하고 있습니다. 연방 정부의 인프라 지출은 건축자재 흐름을 활발하게 유지하고, 대마초 합법화 및 의약품 콜드체인 요구 사항은 고가 틈새 시장을 창출하고 있습니다. 전략적 노선 최적화, 90% 이상의 자산 가동률, 기술을 활용한 배차 관리는 미국 풀트럭로드(FTL) 시장에서 더 이상 차별화 요인이 아닌 기본 요건이 되었습니다.

미국 풀트럭 적재(FTL) 시장 동향 및 인사이트

급성장하는 이커머스의 소용량화

아마존의 풀필먼트 시설이 빠르게 확장되고 옴니채널로 전환함에 따라, 업스트림 물류센터와 라스트마일 크로스도크 지점 간의 풀트럭로드(FTL) 노선이 지속적으로 운영되고 있습니다. 예측 가능한 보충 일정을 통해 운송 회사는 전용 노선 계약을 확보할 수 있으며, 현재 FreightPower 플랫폼 운송의 95% 이상이 드롭 앤 훅(drop-and-hook) 모델입니다. 반품량 증가는 역물류에 대한 수요를 창출하고, 균형 잡힌 백홀과 우수한 자산 회전율을 뒷받침하고 있습니다. 이러한 움직임은 미국 FTL(Full Truckload) 시장에서 자산 기반 차량에 유리한 서비스 신뢰성에 대한 기대감을 뒷받침하고 있습니다.

제조업의 회귀와 니어쇼어화 추세

520억 달러 규모의 'CHIPS and Science Act'로 인해 미국 남동부 및 남서부 지역에 반도체 공장 건설이 가속화되어 고부가가치 설비 및 건축자재가 지속적으로 유입되고 있습니다. 멕시코의 근해 자동차 생산은 국경 횡단 운송 경로를 활성화시켰고, 현재 몬테레이, 라레도, 애틀랜타를 연결하는 복합 운송 옵션이 마련되었습니다. 운송 거리는 단축되지만 운행 빈도가 증가함에 따라 운행 횟수가 증가하고 특수 트레일러 수요가 자극되어 미국 전체 FTL(Full Truckload) 시장 전체 운송량이 증가하고 있습니다.

운전자 부족과 인건비 급등

개인 사업자의 이탈로 인해 슈나이더의 독립 차량 수는 2024년 3분기에 전년 동기 대비 12% 감소했습니다. 이는 업계 전반의 기업이적 역량이 줄어들고 있음을 반영합니다. 설비 압류가 증가함에 따라 신용 리스크는 2008년과 비슷한 수준에 이르렀고, 운송 물량은 더 높은 비용의 회사 소속 운전기사로 이동하고 있습니다. 거액 배상 판결의 위험으로 보험료가 급등하고, 대형 운송업체의 연간 간접비가 1,000만 달러 증가했습니다. AI를 활용한 채용 및 건강 관리 도구는 49%의 투자 수익률을 보이고 있지만, 노동력 부족은 여전히 미국 FTL(Full Truckload) 시장의 장거리 운송 능력을 압박하고 있습니다.

부문 분석

제조업은 2025년 미국 FTL 시장의 31.55%를 차지하며 2026년부터 2031년까지 4.03%의 연평균 복합 성장률(CAGR)을 유지할 것으로 예상되며, 운송량의 핵심 분야이자 성장 동력으로서의 입지를 확고히 하고 있습니다. 반도체 공장 건설, 자동차 산업의 국내 회귀, 기계 설비 교체로 인해 중서부 및 남동부 지역의 운송 경로 밀도가 확대되고 있습니다. 제조업과 관련된 미국의 풀트럭로드(FTL) 시장 규모는 예측 기간 동안 305억 달러 이상 증가할 것으로 예측됩니다. 이는 예측 가능한 원자재 유입과 완제품의 유출이 뒷받침된 결과입니다. 전용 플랫베드 차량과 온도 관리 설비는 정밀 부품 운송에 있어 그 중요성이 커지고 있으며, 이 틈새 시장에서는 운송업체들이 프리미엄 요금을 책정하고 있습니다. 경쟁적 차별화는 실시간 가시성과 적시성에 의존하고 있으며, AI 경로 계획 및 센서 장착 트레일러에 대한 투자를 촉진하고 있습니다. 따라서 미국 풀트럭로드(FTL) 업계에서는 수익성을 높이고 운송업체의 경쟁력을 강화하는 특수차량으로 자산 구성이 변화하고 있습니다.

제조업 외에는 연방 인프라 프로젝트와 견조한 주택 수요를 배경으로 건설업의 운송량이 증가하는 추세입니다. 도소매업은 크로스도크 네트워크를 활용하여 EC 주문의 집적화, 석유-가스-광업 노선은 설비 재배치 리듬에 따라 안정적입니다. 농업의 계절적 생산은 유연한 운송력 모델을 지원하고, 신흥 대마초 물류는 고수익률과 규제 대응이 복잡한 화물을 통해 화물 구성을 더욱 다양화하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 지원(3개월)

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

LSH 26.03.10The United States full-truck-load market is expected to grow from USD 448.65 billion in 2025 to USD 463.85 billion in 2026 and is forecast to reach USD 547.89 billion by 2031 at 3.39% CAGR over 2026-2031.

This growth arises from a resilient freight mix shaped by e-commerce parcelization, near-shore manufacturing, and the escalating use of dedicated contract carriage. Carriers continue adjusting networks to serve dense fulfillment corridors that replenish distribution centers on predictable schedules, even as driver shortages and diesel-price volatility persist. Federal infrastructure spending keeps construction material flows lively, while cannabis legalization and pharmaceutical cold-chain requirements create premium-priced niches. Strategic lane optimization, asset utilization above 90%, and technology-enabled dispatching are now baseline expectations rather than differentiators in the United States Full-Truck-Load market.

United States Full-Truck-Load (FTL) Market Trends and Insights

Explosive E-commerce Parcelization

Amazon's fast-growing fulfillment estate and the wider omnichannel pivot keep full-truck-load lanes busy between upstream distribution centers and last-mile cross-dock sites. Predictable replenishment schedules enable carriers to lock in dedicated routing contracts, with drop-and-hook models now exceeding 95% of FreightPower platform shipments. Higher return volumes also create reverse-logistics demand, supporting balanced backhauls and superior asset turns. These dynamics underpin service reliability expectations that favor asset-based fleets in the United States Full-Truck-Load market.

Manufacturing Reshoring and Near-shore Trends

The USD 52 billion CHIPS and Science Act catalyzes semiconductor plant construction across the Southeast and Southwest, spawning continuous inbound flows of high-value equipment and construction inputs. Near-shore automotive production in Mexico feeds cross-border corridors where intermodal options now link Monterrey, Laredo, and Atlanta. Shorter yet more frequent hauls lift trip counts, stimulate specialized trailer demand, and lift overall volumes in the United States Full-Truck-Load market.

Driver Shortage and Escalating Labor Costs

Owner-operator exits trimmed Schneider's independent fleet by 12% year-over-year in Q3 2024, mirroring an industry-wide contraction in entrepreneurial capacity. Credit stress resembles 2008 levels as equipment repossessions rise, shifting volume to costlier company drivers. Insurance premiums surge amid nuclear verdict exposure, adding USD 10 million to annual overhead at large carriers. AI-based recruiting and wellness tools show a 49% return on investment, yet the labor gap still depresses long-haul capacity in the United States Full-Truck-Load market.

Other drivers and restraints analyzed in the detailed report include:

- Infrastructure Investment and Jobs Act Freight Stimulus

- Growth in Dedicated Contract Carriage

- Diesel-Price Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Manufacturing held 31.55% of the United States Full-Truck-Load market share in 2025 and is pacing for a 4.03% CAGR between 2026-2031, cementing its status as both volume anchor and growth engine. Semiconductor plant construction, automotive reshoring, and machinery upgrades widen lane density across the Midwest and Southeast. The United States Full-Truck-Load market size tied to manufacturing is anticipated to add more than USD 30.5 billion over the forecast horizon, supported by predictable raw-material inflows and finished-goods outflows. Dedicated flatbed and temperature-controlled equipment gains prominence for sensitive components, a niche where carriers command premium rates. Competitive differentiation hinges on real-time visibility and just-in-time reliability, prompting investment in AI route-planning and sensor-equipped trailers. The United States Full-Truck-Load industry, therefore, witnesses asset mixtures tilting toward specialized rigs that lift yields and bolster carrier.

Outside manufacturing, construction sustains elevated volume on the back of federal infrastructure projects and robust residential demand. Wholesale & retail trade leverages cross-dock networks for e-commerce order pooling, while oil, gas, and mining lanes stay stable on equipment repositioning rhythms. Agriculture's seasonal output supports flexible capacity models, and emerging cannabis logistics further diversifies load mixes with high-margin, compliance-heavy freight.

The United States Full-Truck-Load (FTL) Market Report is Segmented by End User Industry (Agriculture, Fishing, and Forestry, Construction, Manufacturing, Oil and Gas, Mining and Quarrying, Wholesale and Retail Trade, and Others), and Destination (Domestic and International). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- ArcBest

- C.H. Robinson

- Covenant Logistics Group Inc.

- CR England Inc.

- DHL Group

- Hirschbach Motor Lines Inc.

- J.B. Hunt Transport, Inc.

- Knight-Swift Transportation Holdings Inc.

- Landstar System Inc.

- Marten Transport Ltd.

- P.A.M. Transport Inc.

- Penske Logistics

- Prime Inc.

- R+L Carriers

- Ryder System, Inc.

- Schneider National Inc.

- TFI International Inc.

- TransAm Truck Lines Inc.

- United Parcel Service of America, Inc. (UPS)

- Werner Enterprises Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 GDP Distribution by Economic Activity

- 4.3 GDP Growth by Economic Activity

- 4.4 Economic Performance and Profile

- 4.4.1 Trends in E-Commerce Industry

- 4.4.2 Trends in Manufacturing Industry

- 4.5 Transport and Storage Sector GDP

- 4.6 Logistics Performance

- 4.7 Length of Roads

- 4.8 Export Trends

- 4.9 Import Trends

- 4.10 Fuel Pricing Trends

- 4.11 Trucking Operational Costs

- 4.12 Trucking Fleet Size by Type

- 4.13 Major Truck Suppliers

- 4.14 Road Freight Tonnage Trends

- 4.15 Road Freight Pricing Trends

- 4.16 Modal Share

- 4.17 Inflation

- 4.18 Regulatory Framework

- 4.19 Value Chain and Distribution Channel Analysis

- 4.20 Market Drivers

- 4.20.1 Explosive E-Commerce Parcelization

- 4.20.2 Manufacturing Reshoring and Near-Shore Trends

- 4.20.3 Infrastructure Investment and Jobs Act Freight Stimulus

- 4.20.4 Growth in Dedicated Contract Carriage

- 4.20.5 Cannabis-Supply Legalization Wave

- 4.20.6 Cold-Chain Pharma Expansion

- 4.21 Market Restraints

- 4.21.1 Driver Shortage and Escalating Labor Costs

- 4.21.2 Diesel-Price Volatility

- 4.21.3 Urban Congestion-Pricing Zones

- 4.21.4 Limited Public EV-Truck Charging Corridors

- 4.22 Technology Innovations in the Market

- 4.23 Porter's Five Forces Analysis

- 4.23.1 Threat of New Entrants

- 4.23.2 Bargaining Power of Buyers

- 4.23.3 Bargaining Power of Suppliers

- 4.23.4 Threat of Substitutes

- 4.23.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 End User Industry

- 5.1.1 Agriculture, Fishing, and Forestry

- 5.1.2 Construction

- 5.1.3 Manufacturing

- 5.1.4 Oil and Gas, Mining and Quarrying

- 5.1.5 Wholesale and Retail Trade

- 5.1.6 Others

- 5.2 Destination

- 5.2.1 Domestic

- 5.2.2 International

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 ArcBest

- 6.4.2 C.H. Robinson

- 6.4.3 Covenant Logistics Group Inc.

- 6.4.4 CR England Inc.

- 6.4.5 DHL Group

- 6.4.6 Hirschbach Motor Lines Inc.

- 6.4.7 J.B. Hunt Transport, Inc.

- 6.4.8 Knight-Swift Transportation Holdings Inc.

- 6.4.9 Landstar System Inc.

- 6.4.10 Marten Transport Ltd.

- 6.4.11 P.A.M. Transport Inc.

- 6.4.12 Penske Logistics

- 6.4.13 Prime Inc.

- 6.4.14 R+L Carriers

- 6.4.15 Ryder System, Inc.

- 6.4.16 Schneider National Inc.

- 6.4.17 TFI International Inc.

- 6.4.18 TransAm Truck Lines Inc.

- 6.4.19 United Parcel Service of America, Inc. (UPS)

- 6.4.20 Werner Enterprises Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment