|

시장보고서

상품코드

1940836

특수 비료 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Specialty Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

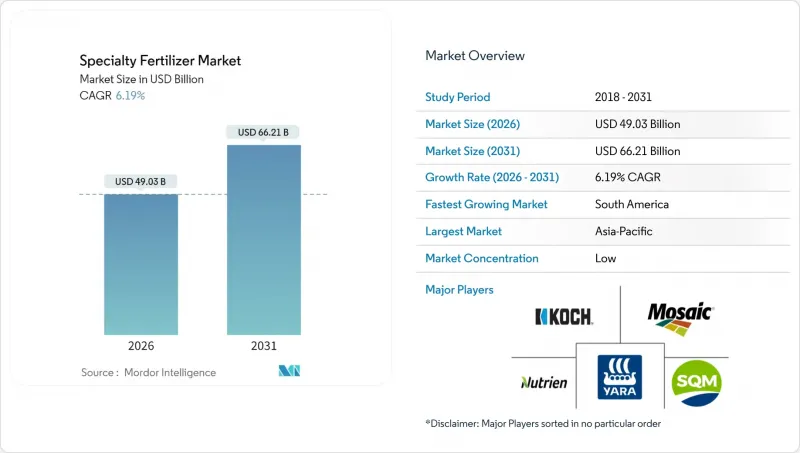

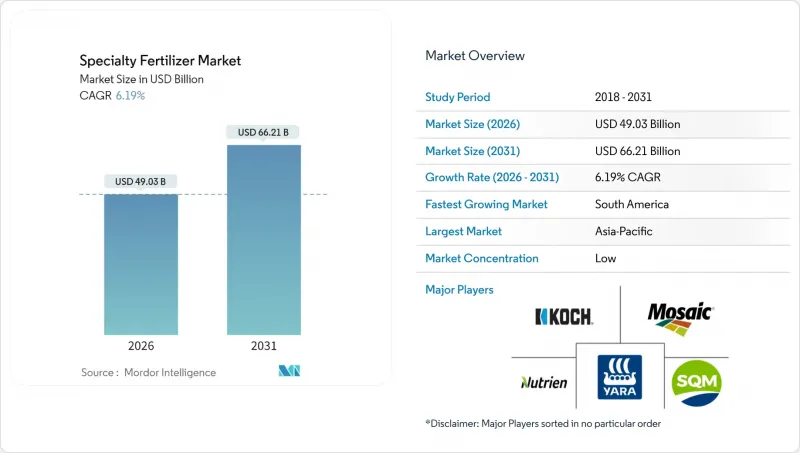

특수 비료 시장은 2025년에 461억 7,000만 달러로 평가되었고, 2026년 490억 3,000만 달러에서 2031년까지 662억 1,000만 달러에 이를 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 6.19%로 예상됩니다.

정밀농업 도구의 도입이 시장 성장을 주도하고 있으며, 이는 효율성 향상형 배합으로의 빠른 전환과 영양 관리를 환경 지표와 연계하는 정책적 지원에 의해 촉진되고 있습니다. 액체 제품이 주류를 차지하는 이유는 완전 용해성이 비료 관개 요구에 부합하기 때문이며, 한편 서방형 코팅 기술의 발전으로 영양분 공급이 작물 수요와 동기화되어 있기 때문입니다. 디지털 농업 플랫폼은 영양분 이용 효율을 높이고, 규제 준수를 촉진하며, 탄소배출권 수익 창출을 가능하게 하는 실시간 현장 데이터를 제공합니다. 보호 재배 확대, 점적 관개 보급률 향상, 질소 이용 효율 향상을 위한 인센티브 제공은 전체 작물 카테고리 수요 회복력을 향상시킬 것입니다. 경쟁의 치열함은 분석, 하드웨어, 맞춤형 영양소 솔루션을 결합한 통합 서비스 모델에 의존하고 있으며, 이는 특수 비료 시장에서 농장의 수익성을 향상시킬 수 있습니다.

세계 특수 비료 시장 동향 및 인사이트

정밀농업 도입

위성영상, 토양센서, GPS 유도 살포기를 통해 양분 투입의 정확도가 향상되고 있습니다. 2024년에는 대다수의 옥수수와 콩 생산자가 가변 비율 비료 시비를 채택하고, 2023년에 비해 전면 살포가 감소함에 따라 에이커당 특수 비료 사용량이 증가합니다. 작물의 생육 단계에 맞추어 주문형 혼합 투입이 가능한 실시간 질소 크레딧을 통해 손실 감소와 수확량 향상을 도모하고 있습니다. 장비 제조업체는 현재 영양제 공급업체와 공동으로 멀티빈 시비기를 설계하고 있으며, 농가는 다운타임 없이 배합을 변경할 수 있습니다. 지원적 보전 프로그램이 하드웨어 비용의 일부를 충당하기 때문에 정밀농업 대응 고효율 제품의 보급이 가속화되고 있습니다.

물 부족과 관개 효율

점적관개와 시비관개 조합은 범람식 관개 시스템에 비해 물 사용량을 줄일 수 있습니다. 이는 농업이 차지하는 담수 자원의 비중이 줄어드는 상황에서 매우 중요한 이점입니다. 2024년에는 전 세계적으로 점적 관개 라인의 설치 면적이 확대되고, 이 네트워크를 통한 특수 비료 사용량은 기존 밭작물 재배 방법의 두 배에 달할 것입니다. 이스라엘과 요르단에서는 10헥타르 이상의 신규 농장에 가압 관개를 의무화하고 있어 완전 수용성 영양소 블렌드에 대한 수요가 고정화되어 있습니다. 온라인 pH 및 전도도 프로브는 막히지 않는 저염도 지수 제품이 요구됩니다. 물 사용 목표와 연동된 보조금 제도는 비료 관개를 촉진하고 특수 비료 시장의 성장을 지원하고 있습니다.

원자재 및 에너지 가격 변동

2024년은 지정학적 긴장으로 인해 천연가스, 칼륨, 인광석 가격이 변동하여 생산자의 수익률을 압박했습니다. CRF 비용의 최대 25%를 차지하는 폴리머 코팅은 유가와 연동되기 때문에 유가 상승은 즉각적인 제품 가격 상승으로 이어집니다. 러시아 벨로루시로부터의 칼륨 공급 차질로 인해 일시적으로 현물 가격이 50% 상승하여 대체 조달이 진행되었습니다. 특수 첨가제 분야에서 단일 공급업체에 대한 의존도는 리스크를 증폭시키고, 환율 변동은 수입에 의존하는 제조업체에게 불확실성을 가중시킵니다. 조달 주기가 짧아 헤지할 여지가 적고, 가격 안정이 어려운 상황입니다.

부문 분석

액체 비료는 2025년 특수 비료 시장 점유율의 53.38%를 차지했습니다. 이 지위는 비료 관개(피겔레이션)와의 탁월한 적합성과 균일한 영양분 분포에 의해 뒷받침됩니다. 빠른 용해성과 혼합의 용이성은 정밀한 균질성을 요구하는 가변 시비장치에 적합합니다. 아시아태평양과 남미에서 대규모 관개 농지의 채택으로 소비량이 높은 수준을 유지하는 반면, 실내 농업은 염분 축적 위험이 낮다는 평가를 받고 있습니다. 또한, 벌크 운송 및 농장 내 혼합을 가능하게 하는 유통 인프라의 확충도 이 부문의 성장에 기여하고 있습니다.

제어 방출형 제품의 특수 비료 시장 규모는 특수 비료 유형 중 가장 빠른 7.81%의 연평균 복합 성장률(CAGR)로 확대될 것으로 예측됩니다. 코팅 기술의 발전으로 작물의 흡수에 따라 예측 가능한 영양분 방출 곡선을 실현하여 유출을 억제하고 노동력을 절감할 수 있습니다. 유황이 부족한 지역에서는 고분자 유황계 제품이 보급되고, 생분해성 필름은 다가올 마이크로 플라스틱 규제에 대응하는 데 기여합니다. 정밀농업 도구는 부가가치를 높이고, 한 번의 시비로 여러 생육단계에 대응할 수 있어 투자수익률 향상에 기여합니다.

특수 비료 시장은 특수 유형별(CRF, 액체 비료, SRF, 수용성), 적용 방법별(관개, 엽면 살포, 토양 살포), 작물 유형별(밭작물, 원예 작물, 잔디 및 관상용 식물), 지역별(아시아태평양, 유럽, 중동/아프리카, 북미, 남미)로 분류됩니다. 시장 예측은 금액(USD) 및 수량(미터톤)으로 제공됩니다.

지역별 분석

2025년 기준 아시아태평양은 전 세계 매출의 65.20%를 차지할 것으로 예상되며, 중국의 토양 검사 보조금과 인도의 소규모 농가를 위한 특수 영양소 장려책이 이를 뒷받침하고 있습니다. 일본과 한국의 집약적 토지 이용은 헥타르당 지출을 더욱 촉진하고, 호주의 가뭄 관리 규정은 액체 혼합 비료를 이용한 시비 관개 시스템의 사용을 촉진하고 있습니다. 동남아시아의 팜유 및 쌀 생산자들은 지속가능성 인증을 위해 고효율 자재를 채택하고 있으며, 이는 추가적인 물량 증가를 가져오고 있습니다.

남미는 2031년까지 연평균 복합 성장률(CAGR) 8.55%로 가장 빠르게 성장하는 지역입니다. 브라질에서는 양분 효율을 높이는 정밀농업 기술에 대한 투자가 시작되었고, 대규모 농장에서는 토양 건강을 보호하기 위해 CRF(제어 방출 비료)의 사용을 무경운 재배와 연계하여 사용하고 있습니다. 아르헨티나는 환경 감시가 강화되는 가운데 수출 경쟁력을 유지하기 위해 콩과 옥수수를 위한 제어 방출 솔루션을 활용하고 있습니다.

남미 특수비료 시장은 대규모 농업경영과 현대적 농업방식의 보급 확대가 특징입니다. 브라질과 아르헨티나를 중심으로 한 이 지역은 광활한 농지와 다양한 작물 포트폴리오를 배경으로 큰 시장 잠재력을 보여주고 있습니다. 브라질은 방대한 농업 경영 규모와 농업 기술 혁신에 대한 강한 집중으로 지역 최대 시장으로 부상하고 있습니다. 아르헨티나는 정밀농업 기술의 보급 확대와 수출 지향형 농업에 집중하면서 가장 빠르게 성장하는 시장으로 자리매김하고 있습니다. 이 지역 시장은 지속 가능한 농업 방식에 대한 인식이 높아지고 농업 기술에 대한 투자가 증가하고 있는 것이 특징입니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 보고서 제공

제3장 주요 요약 및 주요 조사 결과

제4장 주요 산업 동향

제5장 시장 규모와 성장 예측(수량과 금액)

제6장 경쟁 구도

제7장 CEO에 대한 주요 전략적 질문

LSH 26.03.11The specialty fertilizers market was valued at USD 46.17 billion in 2025 and estimated to grow from USD 49.03 billion in 2026 to reach USD 66.21 billion by 2031, at a CAGR of 6.19% during the forecast period (2026-2031).

The adoption of precision farming tools propels market growth, driven by the rapid shift toward enhanced-efficiency formulations and policy support that links nutrient management with environmental metrics. Liquid products dominate because their full solubility matches fertigation needs, while technology improvements in controlled-release coatings keep nutrient availability synchronized with crop demand. Digital agriculture platforms provide real-time field data that enhances nutrient use efficiency, promotes regulatory compliance, and facilitates carbon-credit monetization. Expanding protected cultivation, increasing drip irrigation coverage, and offering incentives for nitrogen use efficiency enhance demand resiliency across crop categories. Competitive intensity hinges on integrated service models that bundle analytics, hardware, and tailored nutrient solutions to raise farm profitability in the specialty fertilizers market.

Global Specialty Fertilizer Market Trends and Insights

Precision-Agriculture Adoption

Satellite imagery, soil sensors, and GPS-guided spreaders are enhancing the accuracy of nutrient placement. In 2024, the majority of corn and soybean growers adopted variable-rate application, compared to 2023, and specialty fertilizer use per acre increased as the broadcast practice declined. Real-time nitrogen crediting triggers on-demand blended inputs that match crop stages, cutting losses and bolstering yields. Equipment firms now co-design multi-bin applicators with nutrient suppliers, letting farmers switch formulations without downtime. Supportive conservation programs cover part of the hardware cost, thereby accelerating the penetration of precision-ready, enhanced-efficiency products.

Water Scarcity and Irrigation Efficiency

Drip irrigation, paired with fertigation, reduces water use compared to flood systems, a critical benefit as agriculture's share of freshwater resources contracts. Global acreage under drip lines reached a higher level in 2024, and specialty fertilizer volumes through these networks doubled those of conventional field methods. Israel and Jordan mandate pressurized irrigation for new farms larger than 10 ha, creating locked-in demand for fully soluble nutrient blends. Online pH and conductivity probes require low-salt index products that remain clog-free. Subsidies linked to water use targets favor fertigation and support the growth of the specialty fertilizers market.

Raw-Material and Energy Price Volatility

Natural gas, potash, and phosphate rock prices fluctuated in 2024 amid geopolitical tensions, compressing producer margins. Polymer coatings, which account for up to 25% of CRF costs, track crude oil, so oil spikes translate quickly into higher finished product prices. Potash supply disruptions from Russia and Belarus led to spot costs increasing by 50% at times, prompting alternative sourcing. Single-supplier dependence for specialty additives magnifies risk, and currency shifts add further uncertainty for import-reliant manufacturers. Short procurement cycles leave little room for hedging, making price stability elusive.

Other drivers and restraints analyzed in the detailed report include:

- Greenhouse and Vertical-Farm Expansion

- Digital Traceability Premiums

- Emerging Micro-Plastic Coating Bans

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Liquid fertilizers accounted for 53.38% of the specialty fertilizers market share in 2025, a position built on their unmatched compatibility with fertigation and uniform nutrient distribution. Their rapid dissolution and ease of blending suit variable-rate rigs that demand precise homogeneity. Adoption of large irrigated acreage across the Asia Pacific and South America keeps volumes high, while indoor farming values its low salt risk. The segment also benefits from an expanded distribution infrastructure that supports bulk shipments and on-farm blending.

The specialty fertilizers market size for controlled-release products is projected to expand at a 7.81% CAGR, the fastest among specialty types. Coating advances offer predictable nutrient release curves that align with crop uptake, thereby curbing leaching and reducing labor requirements. Polymer-sulfur variants gain traction in sulfur-deficient regions, and biodegradable films help satisfy looming microplastic laws. Precision agriculture tools amplify value, as one application now feeds a crop across multiple growth stages, improving return on investment.

The Specialty Fertilizer Market is Segmented by Specialty Type (CRF, Liquid Fertilizer, SRF, Water Soluble), by Application Mode (Fertigation, Foliar, Soil), by Crop Type (Field Crops, Horticultural Crops, Turf and Ornamental), and by Region (Asia-Pacific, Europe, Middle East and Africa, North America, and South America). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Geography Analysis

Asia Pacific commanded 65.20% of global revenue in 2025, supported by China's soil testing subsidies and India's specialty nutrient incentives for smallholders. Intensive land use in Japan and South Korea further propels per-hectare spending, while Australia's drought management rules promote the use of fertigation systems with liquid blends. Southeast Asian palm and rice producers adopt enhanced-efficiency inputs to comply with sustainability certifications, adding incremental volume.

South America represents the fastest-growing region with an 8.55% CAGR to 2031. Brazil has initiated investments in precision agriculture technologies that enhance nutrient efficiency, and large farms are aligning CRF usage with no-till practices to safeguard soil health. Argentina mirrors this trajectory, utilizing controlled-release solutions for soy and corn to maintain export competitiveness amid growing environmental scrutiny.

The South American specialty fertilizer market is characterized by large-scale agricultural operations and growing adoption of modern farming practices. The region, primarily represented by Brazil and Argentina, shows significant market potential driven by extensive agricultural lands and diverse crop portfolios. Brazil emerges as the largest market in the region, supported by its vast agricultural operations and strong focus on technological advancement in farming. Argentina stands as the fastest-growing market, driven by increasing adoption of precision farming techniques and a focus on export-oriented agriculture. The region's market is characterized by growing awareness about sustainable farming practices and increasing investments in agricultural technology.

- Coromandel International Limited

- EuroChem Group AG

- COMPO EXPERT GmbH

- Haifa Group

- Kingenta Ecological Engineering Group Co., Ltd.

- Koch Fertilizer LLC

- Nutrien Ltd.

- Sociedad Quimica y Minera de Chile S.A.

- The Mosaic Company

- Yara International ASA

- ICL Group Ltd.

- K+S Aktiengesellschaft

- Indian Farmers Fertiliser Cooperative Ltd.

- Omex Agriculture Ltd.

- Agro-Culture Liquid Fertilizers LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY AND KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Acreage of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Micronutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.2 Primary Nutrients

- 4.2.2.1 Field Crops

- 4.2.2.2 Horticultural Crops

- 4.2.3 Secondary Macronutrients

- 4.2.3.1 Field Crops

- 4.2.3.2 Horticultural Crops

- 4.2.1 Micronutrients

- 4.3 Agricultural Land Equipped for Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain and Distribution Channel Analysis

- 4.6 Market Drivers

- 4.6.1 Precision-agriculture adoption

- 4.6.2 Water scarcity and irrigation efficiency

- 4.6.3 Greenhouse and vertical-farm expansion

- 4.6.4 Carbon-credit incentives for NUE inputs

- 4.6.5 CRISPR-enabled nutrient-dense crops

- 4.6.6 Digital traceability premiums

- 4.7 Market Restraints

- 4.7.1 Raw-material and energy price volatility

- 4.7.2 High capex of fertigation hardware

- 4.7.3 Emerging micro-plastic coating bans

- 4.7.4 Data-standard gaps for carbon accounting

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Specialty Type

- 5.1.1 Controlled-Release Fertilizer (CRF)

- 5.1.1.1 Polymer Coated

- 5.1.1.2 Polymer-Sulfur Coated

- 5.1.1.3 Others

- 5.1.2 Liquid Fertilizer

- 5.1.3 Slow-Release Fertilizer (SRF)

- 5.1.4 Water-Soluble

- 5.1.1 Controlled-Release Fertilizer (CRF)

- 5.2 Application Mode

- 5.2.1 Fertigation

- 5.2.2 Foliar

- 5.2.3 Soil

- 5.3 Crop Type

- 5.3.1 Field Crops

- 5.3.2 Horticultural Crops

- 5.3.3 Turf and Ornamental

- 5.4 Region

- 5.4.1 Asia-Pacific

- 5.4.1.1 Australia

- 5.4.1.2 Bangladesh

- 5.4.1.3 China

- 5.4.1.4 India

- 5.4.1.5 Indonesia

- 5.4.1.6 Japan

- 5.4.1.7 Pakistan

- 5.4.1.8 Philippines

- 5.4.1.9 Thailand

- 5.4.1.10 Vietnam

- 5.4.1.11 Rest of Asia-Pacific

- 5.4.2 Europe

- 5.4.2.1 France

- 5.4.2.2 Germany

- 5.4.2.3 Italy

- 5.4.2.4 Netherlands

- 5.4.2.5 Russia

- 5.4.2.6 Spain

- 5.4.2.7 Ukraine

- 5.4.2.8 United Kingdom

- 5.4.2.9 Rest of Europe

- 5.4.3 Middle East and Africa

- 5.4.3.1 Nigeria

- 5.4.3.2 Saudi Arabia

- 5.4.3.3 South Africa

- 5.4.3.4 Turkey

- 5.4.3.5 Rest of Middle East and Africa

- 5.4.4 North America

- 5.4.4.1 Canada

- 5.4.4.2 Mexico

- 5.4.4.3 United States

- 5.4.4.4 Rest of North America

- 5.4.5 South America

- 5.4.5.1 Argentina

- 5.4.5.2 Brazil

- 5.4.5.3 Rest of South America

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Coromandel International Limited

- 6.4.2 EuroChem Group AG

- 6.4.3 COMPO EXPERT GmbH

- 6.4.4 Haifa Group

- 6.4.5 Kingenta Ecological Engineering Group Co., Ltd.

- 6.4.6 Koch Fertilizer LLC

- 6.4.7 Nutrien Ltd.

- 6.4.8 Sociedad Quimica y Minera de Chile S.A.

- 6.4.9 The Mosaic Company

- 6.4.10 Yara International ASA

- 6.4.11 ICL Group Ltd.

- 6.4.12 K+S Aktiengesellschaft

- 6.4.13 Indian Farmers Fertiliser Cooperative Ltd.

- 6.4.14 Omex Agriculture Ltd.

- 6.4.15 Agro-Culture Liquid Fertilizers LLC