|

시장보고서

상품코드

2035022

ASEAN의 클라우드 컴퓨팅 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)ASEAN Cloud Computing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

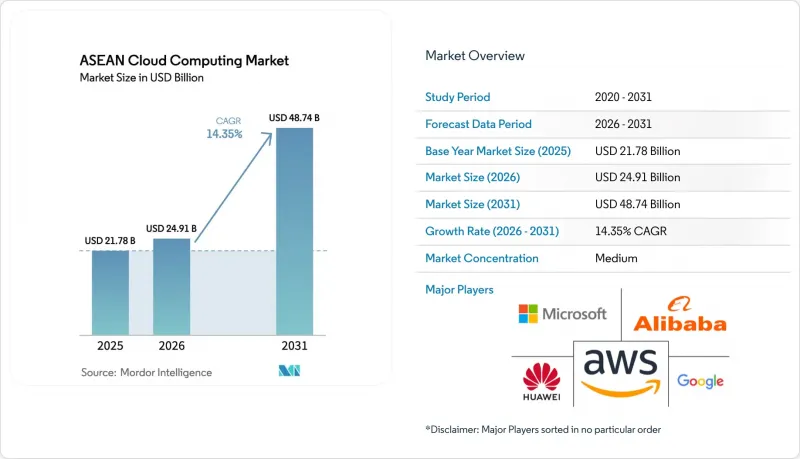

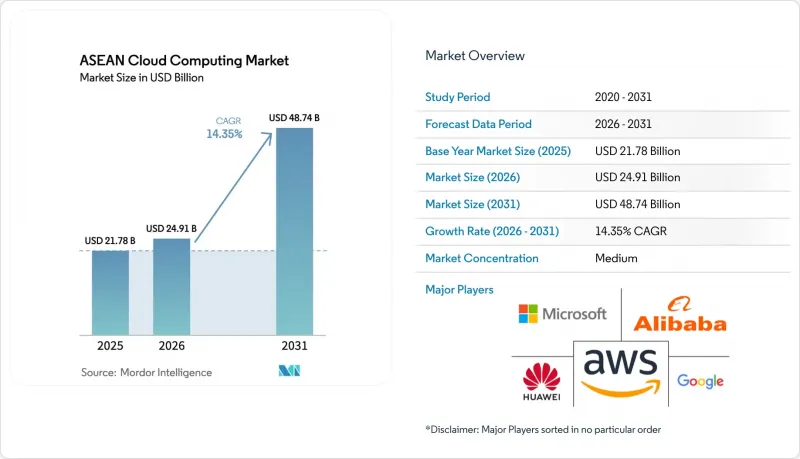

ASEAN의 클라우드 컴퓨팅 시장 규모는 2025년에 217억 8,000만 달러로 평가되었고 2026년 249억 1,000만 달러에서 2031년까지 487억 4,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 14.35%를 나타낼 전망입니다.

싱가포르가 지역 수요를 주도하고, 베트남이 가장 빠른 성장을 기록했으며, 2024-2025년 사이 250억 달러 이상의 하이퍼스케일 투자가 이루어지면서 전체 용량 파이프라인이 강화되었습니다. 정부의 디지털 경제 마스터플랜에 따라 공공기관의 클라우드 전환이 계속 의무화되는 한편, 기업의 현대화로 인해 멀티 클라우드 및 하이브리드 전략이 추진되고 있습니다. 중국 하이퍼스케일러의 가격 경쟁 심화와 현지화된 용량 제공으로 인도네시아, 말레이시아, 태국에서의 인프라 구축이 가속화되고 있습니다. 아세안 클라우드 컴퓨팅 시장은 5G를 활용한 엣지 구축, 재생에너지를 활용한 데이터센터 구축, 중소기업의 확장 가능한 IT에 대한 수요 증가로 인해 더욱 큰 수혜를 받고 있습니다.

아세안 클라우드 컴퓨팅 시장 동향과 인사이트

5G의 빠른 확산으로 엣지-클라우드의 융합이 가능해집니다.

캄보디아의 전국적인 5G 라이선스 부여와 태국의 고밀도 네트워크로의 업그레이드는 근접한 클라우드 노드에 의존하는 밀리초 단위의 지연이 필요한 용도를 가능하게 하고 있습니다. 태국의 수도권 전력공사(Metropolitan Electricity Authority)와 같은 유틸리티 사업자는 이미 5G 네트워크를 클라우드 분석과 연계하여 정전 예측 관리를 하고 있습니다. 엣지 노드와 퍼블릭 클라우드의 시너지 효과로 서비스 내결함성이 향상되고, 사물인터넷(IoT) 워크로드의 적용 범위가 넓어지고 있습니다. 현재 지역 통신사들은 백홀 혼잡을 최소화하기 위해 5G 기지국 내에 미니 데이터센터를 설치하여 운영하고 있습니다. 이러한 융합을 통해 기업이 지연시간에 민감한 트래픽을 엣지 노드로 분할하고 나머지는 중앙의 하이퍼스케일 영역으로 스케일 아웃하는 하이브리드 환경의 도입이 더욱 가속화될 것으로 예측됩니다.

중국 업체들의 아세안 지역 하이퍼스케일 데이터센터 투자 급증세

텐센트는 인도네시아 데이터센터 건설에 5억 달러를 투자하고, 현지 주요 전자상거래 기업과의 제휴를 강화해 북미 플랫폼에 대항할 수 있는 비용 경쟁력을 확보했습니다. 알리바바 클라우드의 AI 공동 프로그램도 말레이시아와 태국에서 서비스 범위를 확장하고 있습니다. 중국계 공급자의 용량 유입은 로컬 데이터 레지던시를 우선시하는 규제 산업에 유리하게 작용하여 기존 벤더에게 가격 및 지연 시간 측면에서 압박을 가하고 있습니다. 조호르와 싱가포르에 위치한 중국계 시설 간의 단거리 국경 간 상호 연결로 인해 다지역 복제에서 2밀리초 미만의 지연 시간이 제공되기 시작했습니다. 이러한 투자 물결은 아세안 클라우드 컴퓨팅 시장 전체공급을 크게 증가시켜 중소기업과 스타트업의 진입장벽을 낮추고 있습니다.

데이터 거주지 및 주권 관련 규정

말레이시아의 '2025년 국경 간 데이터 이전 가이드라인'은 기업에게 이전 영향 평가 실시 및 외국의 개인정보 보호 기준과의 동등성 증명을 의무화하고 있습니다. 베트남의 2025년 7월 시행되는 데이터법에 따라 '핵심 데이터'가 분류되어 기밀성이 높은 데이터 세트에 대해서는 국내 처리가 의무화되어 있습니다. 이러한 규제는 인프라 계획의 분절화를 초래하고, 공급자는 중복된 시설을 설치해야 하며, 자본 비용이 증가하고, 각 관할권마다 서비스 카탈로그를 조정해야 합니다. 기업들은 지역 간 재해복구 체계를 구축할 때 법적 복잡성과 총소유비용(TCO) 증가에 직면하고 있습니다. 컴플라이언스 컨설팅 회사가 지식의 격차를 메울 수 있지만, 국가마다 다른 규제는 단기적으로 아세안 클라우드 컴퓨팅 시장의 성장에 여전히 큰 걸림돌이 되고 있습니다.

부문 분석

퍼블릭 클라우드는 탄력적인 가격 설정과 풍부한 지역 가용성 영역에 힘입어 2025년 아세안 클라우드 컴퓨팅 시장에서 67.05%의 점유율을 유지했습니다. 하이브리드 클라우드는 2026년부터 2031년까지 연평균 복합 성장률(CAGR) 15.85%를 나타낼 것으로 예측되며, 2026년부터 2031년까지 아세안 클라우드 컴퓨팅 시장 규모 확대에서 가장 큰 증가분을 차지할 것으로 전망됩니다. AIS와 같은 통신사업자들은 국내 자본에 의한 하이퍼스케일 플랫폼을 출범시킴으로써 지역 주권과 세계 서비스를 융합하고 있습니다. 규제 대상인 은행과 병원에서는 프라이빗 클라우드 도입이 계속되고 있지만, 보안 체계가 성숙해짐에 따라 점유율을 양보할 것으로 예측됩니다.

하이브리드 클라우드의 성장은 멀티 클라우드 거버넌스 도구, 컨테이너의 이식성, 그리고 성숙해가는 제로 트러스트 프레임워크에 기인합니다. 현재 기업들은 지연 시간이 중요한 분석 처리를 로컬 노드에 할당하고, 버스트 워크로드를 퍼블릭 존으로 라우팅하여 비용과 컴플라이언스를 동시에 최적화하고 있습니다. 이러한 접근 방식은 아세안의 다양한 데이터 규제 환경에서 하이브리드 환경을 연결해줄 수 있는 오케스트레이션 벤더와 매니지드 서비스 제공업체에게 새로운 비즈니스 기회를 열어줄 수 있습니다.

2025년에는 SaaS(Software as a Service)가 매출의 55.65%를 차지하여 여전히 시장에서 가장 성숙한 제공 형태가 됐습니다. 한편, PaaS(Platform as a Service)는 CAGR 16.3%로 서버리스 런타임과 통합된 DevSecOps 파이프라인에 대한 개발자들 수요 증가를 반영하고 있습니다. PaaS의 급격한 성장은 개발자 중심의 도구에서 아세안 클라우드 컴퓨팅 시장 규모를 확대하고 있으며, VNPT는 플랫폼 서비스를 배경으로 클라우드 관련 수익으로 113억 달러를 목표로 하고 있습니다.

마이크로서비스, AI 모델 호스팅, IoT 이벤트 스트림은 인프라를 추상화하면서도 유연성을 유지하는 관리형 미들웨어가 필요하며, 이를 통해 PaaS는 빠른 제품 주기에 필수적인 계층으로 자리매김하고 있습니다. SaaS 도입은 HR, CRM, ERP 워크로드에서 지속적으로 강세를 보이고 있으며, 특히 턴키 솔루션을 원하는 중견기업에서 두드러지게 나타나고 있습니다. IaaS의 성장은 계속되고 있지만, 추상화 계층이 밸류체인의 상층부로 이동함에 따라 그 속도는 느려지고 있습니다.

아세안 클라우드 컴퓨팅 시장은 도입 모델(퍼블릭 클라우드, 프라이빗 클라우드, 하이브리드 클라우드), 서비스 모델(Infrastructure As A Service, Platform As A Service, Software As A Service), 조직 규모(중소기업, 대기업), 최종 사용자 산업(제조, 교육, 소매 등), 국가별로 분류됩니다. 시장 예측은 금액(USD) 기준으로 제공됩니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 동향

JHS 26.05.20The ASEAN Cloud Computing Market size was valued at USD 21.78 billion in 2025 and estimated to grow from USD 24.91 billion in 2026 to reach USD 48.74 billion by 2031, at a CAGR of 14.35% during the forecast period (2026-2031).

Singapore anchors regional demand, Vietnam registers the fastest growth, and hyperscale investments exceeding USD 25 billion in 2024-2025 have strengthened the overall capacity pipeline. Government digital-economy master plans continue to mandate cloud migration across public agencies, while enterprise modernization pushes multi-cloud and hybrid strategies. Chinese hyperscalers have added significant price competition and localized capacity, accelerating infrastructure build-out across Indonesia, Malaysia, and Thailand. The ASEAN cloud computing market benefits further from 5G-enabled edge deployments, renewable-energy data-center initiatives, and rising demand for scalable IT among SMEs.

ASEAN Cloud Computing Market Trends and Insights

Accelerated 5G roll-outs enabling edge-cloud convergence

Nationwide 5G licenses in Cambodia and dense network upgrades in Thailand are enabling millisecond-latency applications that depend on proximate cloud nodes. Utilities such as Thailand's Metropolitan Electricity Authority have already tied 5G grids to cloud analytics for predictive outage management. The synergy between edge nodes and public clouds improves service resilience and widens the addressable base for Internet-of-Things (IoT) workloads. Regional telcos now co-locate mini-data centers inside 5G base stations to minimize backhaul congestion. This convergence is expected to deepen hybrid adoption as enterprises partition latency-sensitive traffic to edge nodes while scaling the remainder on central hyperscale regions.

Surge in ASEAN hyperscale data-center investments by Chinese providers

Tencent allocated USD 500 million for Indonesian builds and formed deeper partnerships with local e-commerce leaders, delivering cost-competitive alternatives to North American platforms. Alibaba Cloud's collaborative AI programs have also widened service breadth across Malaysia and Thailand. The influx of Chinese capacity favors regulated industries that prioritize local data residency, thereby pressuring incumbent vendors on price and latency. Short-haul cross-border interconnects between Chinese-backed facilities in Johor and Singapore have begun to offer sub-2 ms latency for multi-region replication. This investment wave materially boosts the ASEAN cloud computing market's overall supply, lowering entry barriers for SMEs and start-ups.

Data residency and sovereignty regulations

Malaysia's 2025 Cross-Border Transfer Guidelines oblige firms to run Transfer Impact Assessments and prove the equivalence of foreign privacy standards. Vietnam's July 2025 Data Law classifies "core data" and enforces domestic processing for sensitive sets. Such rules fragment infrastructure planning, forcing providers to duplicate facilities, raise capital costs, and adapt service catalogs per jurisdiction. Enterprises face legal complexity and higher total cost of ownership when architecting cross-region disaster recovery. Although compliance consultancies can bridge knowledge gaps, divergent national rules remain a notable drag on ASEAN cloud computing market growth during the near term.

Other drivers and restraints analyzed in the detailed report include:

- Government digital-economy masterplans boosting cloud adoption

- Rising enterprise demand for scalable IT infrastructure

- Shortage of cloud-skilled workforce in Tier-2 markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Public Cloud retained a 67.05% share of the ASEAN cloud computing market in 2025, backed by elastic pricing and abundant regional availability zones. Hybrid Cloud is forecast to post a 15.85% CAGR, generating the largest incremental addition to the ASEAN cloud computing market size between 2026-2031. Telecom operators such as AIS are blending local sovereignty with global services by launching domestically owned hyperscale platforms. Private Cloud installations continue among regulated banks and hospitals but are expected to cede share as security postures mature.

Hybrid growth springs from multi-cloud governance tooling, container portability, and maturing zero-trust frameworks. Enterprises now segment latency-critical analytics to local nodes while routing burst workloads to public zones, optimizing cost and compliance simultaneously. The approach unlocks new addressable opportunities for orchestration vendors and managed-service providers that can bridge hybrid estates across ASEAN's diverse data-regulation landscape.

Software as a Service contributed 55.65% revenue in 2025 and remains the market's most mature delivery mode. Platform as a Service, however, is on track for a 16.3% CAGR, reflecting rising developer demand for serverless runtimes and integrated DevSecOps pipelines. The PaaS surge enlarges the ASEAN cloud computing market size for developer-centric tooling, with VNPT targeting USD 11.3 billion cloud-related revenue on the back of platform services.

Micro-services, AI model hosting, and IoT event streams require managed middleware that abstracts infrastructure yet preserves flexibility, positioning PaaS as the essential layer for rapid product cycles. SaaS uptake remains strong among HR, CRM, and ERP workloads, especially for mid-market firms seeking turnkey solutions. IaaS growth continues but at a tempered pace as abstraction layers climb the value chain.

ASEAN Cloud Computing Market is Segmented by Deployment Model (Public Cloud, Private Cloud, and Hybrid Cloud), Service Model (Infrastructure As A Service, Platform As A Service, and Software As A Service), Organization Size (Small and Medium Enterprises and Large Enterprises), End-User Industry (Manufacturing, Education, Retail, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Amazon Web Services, Inc.

- Microsoft Corporation

- Google LLC (Alphabet Inc.)

- Alibaba Cloud (Alibaba Group Holding Limited)

- Huawei Technologies Co., Ltd.

- Tencent Holdings Ltd.

- IBM Corporation

- Oracle Corporation

- Salesforce, Inc.

- SAP SE

- DigitalOcean Holdings, Inc.

- Rackspace Technology, Inc.

- VMware, Inc.

- Equinix, Inc.

- OVH Groupe SAS (OVHcloud)

- Cloudflare, Inc.

- Snowflake Inc.

- NetApp, Inc.

- Nutanix, Inc.

- Red Hat, Inc. (IBM)

- Fastly, Inc.

- Akamai Technologies, Inc.

- Workday, Inc.

- ServiceNow, Inc.

- Databricks Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated 5G roll-outs enabling edge-cloud convergence

- 4.2.2 Surge in ASEAN hyperscale data-center investments by Chinese providers

- 4.2.3 Government digital-economy masterplans boosting cloud adoption

- 4.2.4 Rising enterprise demand for scalable IT infrastructure

- 4.2.5 Cloud-native fintech growth in Indonesia and Vietnam

- 4.2.6 Sustainability incentives for renewable-powered cloud facilities

- 4.3 Market Restraints

- 4.3.1 Data residency and sovereignty regulations

- 4.3.2 Shortage of cloud-skilled workforce in Tier-2 markets

- 4.3.3 Cross-border connectivity and latency challenges

- 4.3.4 High total cost of private and hybrid deployments for SMEs

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Pricing Model Analysis

- 4.8 Assessment of Macro-Economic Trends

- 4.8.1 Ongoing Digitalization in SMEs

- 4.8.2 Economic Growth in ASEAN Countries

- 4.9 Number of Data Centres Across ASEAN

- 4.10 Industry Attractiveness - Porter's Five Forces Analysis

- 4.10.1 Bargaining Power of Suppliers

- 4.10.2 Bargaining Power of Buyers

- 4.10.3 Threat of New Entrants

- 4.10.4 Threat of Substitutes

- 4.10.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Deployment Model

- 5.1.1 Public Cloud

- 5.1.2 Private Cloud

- 5.1.3 Hybrid Cloud

- 5.2 By Service Model

- 5.2.1 Infrastructure as a Service (IaaS)

- 5.2.2 Platform as a Service (PaaS)

- 5.2.3 Software as a Service (SaaS)

- 5.3 By Organization Size

- 5.3.1 Small and Medium Enterprises (SMEs)

- 5.3.2 Large Enterprises

- 5.4 By End-user Industry

- 5.4.1 Manufacturing

- 5.4.2 Education

- 5.4.3 Retail

- 5.4.4 Transportation and Logistics

- 5.4.5 Healthcare

- 5.4.6 BFSI

- 5.4.7 Telecom and IT

- 5.4.8 Government and Public Sector

- 5.4.9 Utilities

- 5.4.10 Other End-user Industries

- 5.5 By Country

- 5.5.1 Singapore

- 5.5.2 Thailand

- 5.5.3 Malaysia

- 5.5.4 Indonesia

- 5.5.5 Vietnam

- 5.5.6 Philippines

- 5.5.7 Others

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amazon Web Services, Inc.

- 6.4.2 Microsoft Corporation

- 6.4.3 Google LLC (Alphabet Inc.)

- 6.4.4 Alibaba Cloud (Alibaba Group Holding Limited)

- 6.4.5 Huawei Technologies Co., Ltd.

- 6.4.6 Tencent Holdings Ltd.

- 6.4.7 IBM Corporation

- 6.4.8 Oracle Corporation

- 6.4.9 Salesforce, Inc.

- 6.4.10 SAP SE

- 6.4.11 DigitalOcean Holdings, Inc.

- 6.4.12 Rackspace Technology, Inc.

- 6.4.13 VMware, Inc.

- 6.4.14 Equinix, Inc.

- 6.4.15 OVH Groupe SAS (OVHcloud)

- 6.4.16 Cloudflare, Inc.

- 6.4.17 Snowflake Inc.

- 6.4.18 NetApp, Inc.

- 6.4.19 Nutanix, Inc.

- 6.4.20 Red Hat, Inc. (IBM)

- 6.4.21 Fastly, Inc.

- 6.4.22 Akamai Technologies, Inc.

- 6.4.23 Workday, Inc.

- 6.4.24 ServiceNow, Inc.

- 6.4.25 Databricks Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 White-Space and Unmet-Need Assessment