|

시장보고서

상품코드

2043973

남미의 플라스틱 뚜껑 및 마개 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)South America Plastic Caps And Closures - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

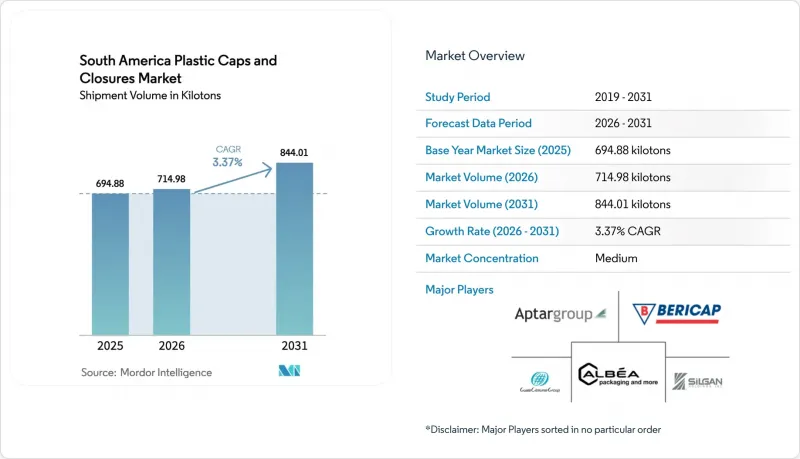

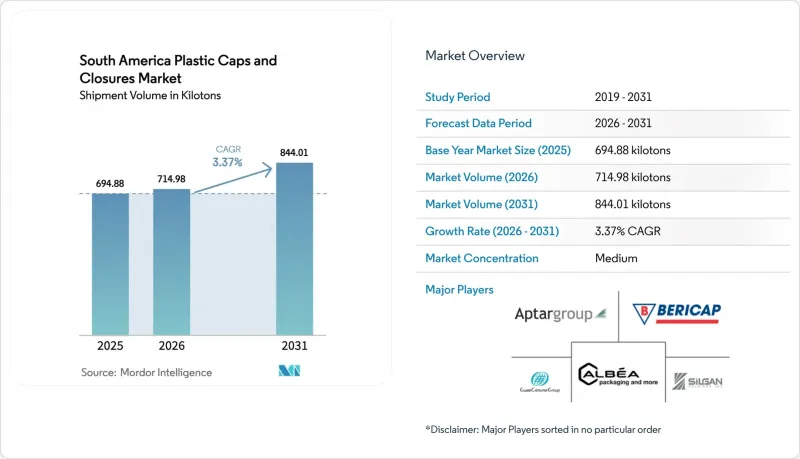

남미의 플라스틱 뚜껑 및 마개 시장 규모는 2025년에 694.88 킬로톤으로 평가되었습니다. 2026년 714.98 킬로톤에서 2031년까지 844.01 킬로톤에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 3.37%를 나타낼 전망입니다.

재활용 재료 함유량에 대한 유리한 규제, 전자상거래 이행의 급속한 확대, 유럽 연합(EU)의 테더 캡 규제에 대한 수출 업체의 대응으로 제품 사양 및 조달 전략이 재검토되고 있습니다. 지역 수지 제조업체인 브라스켐(Braskem)은 기계적 및 화학적 재생 등급으로의 전환을 가속화하고 있으며, 고급 퍼스널케어 브랜드와 주류 브랜드는 소비 시점에 정품임을 확인할 수 있는 스마트 캡을 도입하고 있습니다. 버진 수지와 사용 수지의 혼합, 변조 방지 기능의 통합, 프로모션 캠페인용 소량 생산에 대응할 수 있는 컨버터가 신규 계약을 체결하고 있습니다. 동시에 브랜드 소유자가 탄소 감축 목표를 추구하고 변동이 심한 폴리프로필렌 가격의 영향을 줄이기 위해 노력하는 가운데, 캡의 경량화는 진입 비용에 대한 요구 사항이 되고 있습니다.

남미의 플라스틱 뚜껑 및 마개 시장 동향 및 인사이트

급증하는 이동 중 음료 소비

도시 통근자들은 이동 중에도 마실 수 있는 1회용 페트병을 선호하고 있으며, 이로 인해 브랜드는 탄산을 유지하고, 누출을 방지하고, 부드럽게 열리는 캡을 지정해야 합니다. 소매 데이터에 따르면 브라질과 콜롬비아에서 청량음료와 에너지 음료의 수량이 증가하고 있으며, 스포츠 음료 라인은 한 손으로 조작할 수 있는 플립탑이나 푸시풀식 디자인을 채택하고 있습니다. 각 컨버터 업체들은 변조 방지 밴드, 압력 방출 밸브, 더 견고한 힌지 설계 등으로 이에 대응하고 있으며, 이는 단가를 최대 8%까지 상승시키면서도 소매업체의 재고 감소를 억제합니다. 멀티캐비티 압축 금형에 대한 투자가 물량 증가를 뒷받침하는 한편, 경량화로 인해 추가 기능 비용의 일부가 상쇄되고 있습니다. 그 결과, 부가가치가 높은 캡에 대한 분석이 호전되고, 평균 판매가격이 상승하는 선순환이 일어나고 있습니다.

PET 병에 담긴 우유 음료의 보급 확대

브라질과 아르헨티나의 유제품 제조업체들은 종이팩에서 냉장용 PET 병으로 전환하고 있으며, 풍미를 보호하고 프리미엄 포지셔닝을 나타내는 캡에 대한 수요를 주도하고 있습니다. 테트라팩이 도입한 사탕수수 유래 테더캡은 바이오 유래 소재가 지속가능성 목표와 성능적 요구를 모두 충족시킬 수 있다는 것을 입증하고 있습니다. 포일 라이너와 탬퍼링을 결합한 이중 밀봉 설계가 주목을 받고 있지만, 공동 사출 금형의 요구 사항으로 인해 생산은 대규모 컨버터로 제한됩니다. 페루와 콜롬비아의 콜드체인 확대는 인프라가 구축되면 더 많은 수요를 창출할 것으로 예상되며, PET 유음료는 장기적으로 중요한 성장 분야로 자리매김할 것으로 보입니다. 다양한 수지의 공동성형이 가능하고, 소량 컬러 생산이 가능한 캡 제조업체는 전략적 우위를 점할 수 있습니다.

가정용 세제에서 스탠드업 파우치로의 전환

브라질과 칠레에서는 세제 및 유연제 매장에서 현재 부드러운 리필용 파우치가 주류를 이루고 있으며, 딱딱한 병마개에 대한 수요는 감소하고 있습니다. Unilever의 남미 매출은 2024년 6.0% 증가했는데, 이는 무게가 70% 가볍고 1회당 사용 비용이 낮은 파우치 형태가 기여한 것으로 분석됩니다. 캡 공급업체들은 플립 탑이 달린 주둥이가 있는 파우치를 모색하고 있지만, 이 하위 형태는 여전히 전체 연질 포장의 5% 미만에 불과합니다. 농축형 포드의 보급으로 컨버터 업체들이 리필 스테이션용 디스펜서 헤드로 전환하거나 필름 라미네이트와 호환되는 재밀봉 가능한 주둥이를 설계하지 않는 한, 캡의 중요성은 더욱 감소할 수 있습니다.

부문 분석

기타 소재(주로 재생 PET, 바이오 폴리에틸렌, 첨단 바이오플라스틱)는 2026년부터 브라질에서 PET 포장재에 22% 재생 소재 함유가 의무화됨에 따라 CAGR 4.33%로 남미 전체 플라스틱 뚜껑 및 마개 시장보다 더 높은 성장률을 나타낼 것으로 예측됩니다. 폴리프로필렌은 2025년 44.20%의 물량 점유율을 유지했지만, 톤당 840달러의 불안정한 공급가격으로 인해 컨버터 업체들은 20-30%의 포스트컨슈머 수지를 혼합하여 고객의 지속가능성에 대한 약속을 지키면서 수익성을 확보할 수 있게 되었습니다. 수익성을 확보할 수 있습니다.

브라스켐이 2025년 6월에 출시한 FDA 인증 PCR PP는 식품 접촉용 캡에 재생 PP를 사용하는 데 있어 마지막 기술적 장벽을 제거했습니다. 한편, 바이오 유래 사탕수수 유래 PE는 Bonsucro 인증 요건을 충족하며, 수명주기 동안 탄소배출량을 70% 감소시킵니다. 그러나 페루와 콜롬비아의 식품용 rPET 생산 능력이 제한적이기 때문에 PET 캡 시장의 성장은 제한적입니다. 이 지역 전체에서 컨버터 업체들은 현재 버진 수지, 기계적 재생 수지, 화학적 재생 수지, 바이오 수지, 바이오 수지의 네 가지 수지 스트림을 인증하고 있으며, 재고 비용은 상승하지만 공급의 탄력성이 확보되어 있습니다.

2025년에는 Ambev 양조장과 Coca-Cola FEMSA의 병입 기지 덕분에 음료용 캡이 총 출하량의 49.32%를 차지했습니다. 그럼에도 불구하고, 프리미엄 스킨케어 및 헤어케어 제품들이 소프트 스퀴즈 및 에어리스 펌프를 채택하여 용량의 정확성을 향상시킴에 따라 화장품 및 세면도구용 캡은 CAGR 4.52%로 더 빠른 속도로 성장할 것으로 예측됩니다. 남미 화장품 플라스틱 뚜껑 및 마개 시장은 판매량은 적지만 평균 판매가격이 높아 그 영향을 상쇄하고 있습니다.

식품용 뚜껑 및 마개는 1인당 소득 증가와 함께 성장하고 있지만, 가정용 화학제품용 뚜껑 및 마개는 리필용 파우치의 보급으로 인해 어려움을 겪고 있습니다. 제약 헬스케어 부문은 틈새 시장에 머물러 있지만, ANVISA(브라질 국가위생감독청)와 ANMAT(아르헨티나 국가 의약품 및 의료기기 감독청)에서 요구하는 어린이 내성 기능, 건조제 내장 기능 등으로 높은 수익성을 유지하고 있습니다. 품질 규제가 더 엄격한 칠레와 브라질 시장에서는 브랜드 소유주들이 이러한 고급형 캡에 대해 일반 스크류 캡의 3-5배의 가격을 지불하고 있습니다.

"남미의 플라스틱 뚜껑 및 마개 시장 보고서"는 재료(PET, PP, LDPE, LDPE, 기타), 최종 사용자 산업(음료, 식품, 기타), 캡 유형(스크류 캡, 테더 캡, 어린이용 캡, 기타), 제조 기술(사출 성형, 압축 성형, 기타), 지역(브라질, 아르헨티나, 콜롬비아, 멕시코, 페루, 칠레, 콜롬비아) 압축성형, 기타), 지역(브라질, 아르헨티나, 콜롬비아, 콜롬비아, 기타)으로 분류되어 있습니다. 시장 예측은 킬로톤 기준으로 제공됩니다.

기타 혜택

- 엑셀 형태 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTH 26.05.29The South America plastic caps and closures market size was valued at 694.88 kilotons in 2025 and estimated to grow from 714.98 kilotons in 2026 to reach 844.01 kilotons by 2031, at a CAGR of 3.37% during the forecast period (2026-2031).

Favorable recycled-content mandates, the rapid uptick in e-commerce fulfillment, and exporter alignment with the European Union tethered-cap rule are redefining product specifications and sourcing strategies. Regional resin producer Braskem has accelerated the shift toward mechanically and chemically recycled grades, while premium personal-care and spirits brands are installing smart closures that validate authenticity at the point of consumption. Converters able to blend virgin and post-consumer resin, integrate tamper-evident functionality, and offer short print runs for promotional campaigns are winning new contracts. At the same time, closure lightweighting is becoming a cost-of-entry requirement as brand owners pursue carbon-reduction targets and seek relief from volatile polypropylene prices.

South America Plastic Caps And Closures Market Trends and Insights

Surging On-The-Go Beverage Consumption

Urban commuters are favoring single-serve PET bottles that can be consumed on the move, pushing brands to specify closures that maintain carbonation, resist leakage, and open smoothly. Retail data show soft-drink and energy-drink volumes rising in Brazil and Colombia, and sports-drink lines are adopting flip-top and push-pull designs that enable one-handed use. Converters are responding with tamper-evident bands, pressure-relief vents, and stronger hinge designs that add up to 8% to unit cost yet reduce shrinkage for retailers. Investment in high-cavity compression molds supports the volume surge, while lightweighting offsets part of the added feature cost. The net effect is a positive mix shift toward value-added closures that lift average selling prices.

Rising Penetration of PET Bottled Dairy Drinks

Dairy processors in Brazil and Argentina are switching from cartons to chilled PET bottles, driving demand for closures that protect flavor and signal premium positioning. Sugarcane-based tethered caps introduced by Tetra Pak demonstrate that bio-attributed materials can meet both sustainability targets and performance needs. Dual-seal designs combining foil liners with tamper rings are gaining traction, though their co-injection tooling requirements limit production to larger converters. Cold-chain expansion in Peru and Colombia will unlock additional volume once infrastructure matures, making PET dairy drinks a key long-term growth pocket. Closure makers able to co-mold dissimilar resins and manage small color runs hold a strategic edge.

Shift Toward Stand-Up Pouches In Household Cleaners

Flexible refill pouches now dominate detergent and fabric-softener aisles in Brazil and Chile, reducing demand for rigid-bottle closures. Unilever's South America revenue rose 6.0% in 2024, helped by pouch formats that weigh 70% less and sell at a lower cost-per-use. Closure suppliers are exploring spouted pouches with flip-tops, yet the subformat still accounts for less than 5% of flexible-pack volume. As concentrated pods gain traction, closures could lose further relevance unless converters pivot to dispensing heads for refill stations or design resealable spouts compatible with film laminates.

Other drivers and restraints analyzed in the detailed report include:

- Booming E-Commerce Demand For Tamper-Evident Packaging

- Private-Label Expansion Among Regional FMCG Players

- Growing Anti-Plastic Regulations In Pacific Alliance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Other Materials, mainly recycled PET, bio-based polyethylene, and advanced bioplastics, are forecast to outpace the overall South America plastic caps and closures market at a 4.33% CAGR, benefiting from Brazil's 22% mandatory recycled content in PET packaging beginning in 2026. Polypropylene retained 44.20% volume share in 2025, but volatile offer prices at USD 840 per tonne have prompted converters to blend in 20-30% post-consumer resin, safeguarding margins while meeting client sustainability commitments.

Braskem's FDA-compliant PCR PP launched in June 2025 removed the last technical barrier to using recycled PP in food-contact closures. Meanwhile, bio-attributed sugarcane PE qualifies for Bonsucro certification and cuts life-cycle carbon emissions by 70%. Limited food-grade rPET capacity in Peru and Colombia, however, constrains PET closure growth. Across the region, converters now qualify four resin streams, virgin, mechanically recycled, chemically recycled, and bio-based, raising inventory costs yet providing supply resilience..

Beverage closures delivered 49.32% of volume in 2025 thanks to Ambev's breweries and Coca-Cola FEMSA's bottling footprint. Even so, cosmetics and toiletries closures will grow faster at 4.52% CAGR as premium skincare and hair-care lines adopt soft-squeeze and airless pumps that improve dosing precision. The South America plastic caps and closures market size for cosmetics commands higher average selling prices, offsetting lower tonnage.

Food closures advance in lockstep with rising per-capita income, while household-chemical closures suffer from refill pouches. Pharmaceutical and healthcare remain niche but highly profitable because of child-resistant and desiccant-integrated features demanded by ANVISA and ANMAT. Brand owners in Chile and Brazil, markets with stricter quality regulation, already pay 3-5 times the price of commodity screw caps for these advanced formats.

The South America Plastic Caps and Closures Market Report is Segmented by Material (PET, PP, LDPE, and More), End-User Industry (Beverage, Food, and More), Cap Type (Screw Closures, Tethered Caps, Child-Resistant Closures, and More), Manufacturing Technology (Injection Molding, Compression Molding, and More), and Geography (Brazil, Argentina, Colombia, and More). The Market Forecasts are Provided in Terms of Volume (Kilotons).

List of Companies Covered in this Report:

- Silgan Holdings Inc.

- Albea S.A.

- Guala Closures S.p.A.

- Bericap GmbH & Co. KG

- AptarGroup, Inc.

- Amcor plc

- Crown Holdings, Inc.

- Closure Systems International, Inc.

- Plastivaloire SE

- Tecnocap S.p.A.

- Pano Cap (Canada) Limited

- Mold-Tek Packaging Limited

- RPC M&H Plastics Ltd.

- Oben Holding Group S.A.C.

- Universal Closures Ltd.

- Paccor Packaging GmbH

- Weener Plastics Group BV

- Freudenberg Home and Cleaning Solutions GmbH

- Comar, LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging On-The-Go Beverage Consumption

- 4.2.2 Rising Penetration Of Pet Bottled Dairy Drinks

- 4.2.3 Booming E-Commerce Demand For Tamper-Evident Packaging

- 4.2.4 Private-Label Expansion Among Regional Fmcg Players

- 4.2.5 Refill-And-Reuse Pilots By Large Beverage Brands

- 4.2.6 Adoption Of Tethered-Cap Eu Directive By Sa Exporters

- 4.3 Market Restraints

- 4.3.1 Shift Toward Stand-Up Pouches In Household Cleaners

- 4.3.2 Growing Anti-Plastic Regulations In Pacific Alliance

- 4.3.3 Price Volatility Of Virgin Polypropylene

- 4.3.4 Consumer Preference For Metal Crowns In Premium Beer

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 The Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VOLUME)

- 5.1 By Material

- 5.1.1 Polyethylene Terephthalate (PET)

- 5.1.2 Polypropylene (PP)

- 5.1.3 Low Density Polyethylene (LDPE)

- 5.1.4 High-Density Polyethylene (HDPE)

- 5.1.5 Other Materials

- 5.2 By End-user Industry

- 5.2.1 Beverage

- 5.2.2 Food

- 5.2.3 Pharmaceutical and Healthcare

- 5.2.4 Cosmetics and Toiletries

- 5.2.5 Household Chemicals

- 5.2.6 Other End-user Industries

- 5.3 By Cap Type

- 5.3.1 Screw Closures

- 5.3.2 Tethered Caps

- 5.3.3 Flip-top and Snap-on Caps

- 5.3.4 Child-resistant Closures

- 5.3.5 Luxury/Premium Decorative Closures

- 5.3.6 Dispensing Caps

- 5.4 By Manufacturing Technology

- 5.4.1 Injection Molding

- 5.4.2 Compression Molding

- 5.4.3 3-Piece and In-line Assembly

- 5.4.4 Digitally Printed Smart Closures

- 5.5 By Country

- 5.5.1 Brazil

- 5.5.2 Argentina

- 5.5.3 Colombia

- 5.5.4 Chile

- 5.5.5 Peru

- 5.5.6 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Silgan Holdings Inc.

- 6.4.2 Albea S.A.

- 6.4.3 Guala Closures S.p.A.

- 6.4.4 Bericap GmbH & Co. KG

- 6.4.5 AptarGroup, Inc.

- 6.4.6 Amcor plc

- 6.4.7 Crown Holdings, Inc.

- 6.4.8 Closure Systems International, Inc.

- 6.4.9 Plastivaloire SE

- 6.4.10 Tecnocap S.p.A.

- 6.4.11 Pano Cap (Canada) Limited

- 6.4.12 Mold-Tek Packaging Limited

- 6.4.13 RPC M&H Plastics Ltd.

- 6.4.14 Oben Holding Group S.A.C.

- 6.4.15 Universal Closures Ltd.

- 6.4.16 Paccor Packaging GmbH

- 6.4.17 Weener Plastics Group BV

- 6.4.18 Freudenberg Home and Cleaning Solutions GmbH

- 6.4.19 Comar, LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment