|

시장보고서

상품코드

2044044

중국의 LED 에피택시 MOCVD 장비 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)China LED Epitaxy MOCVD Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

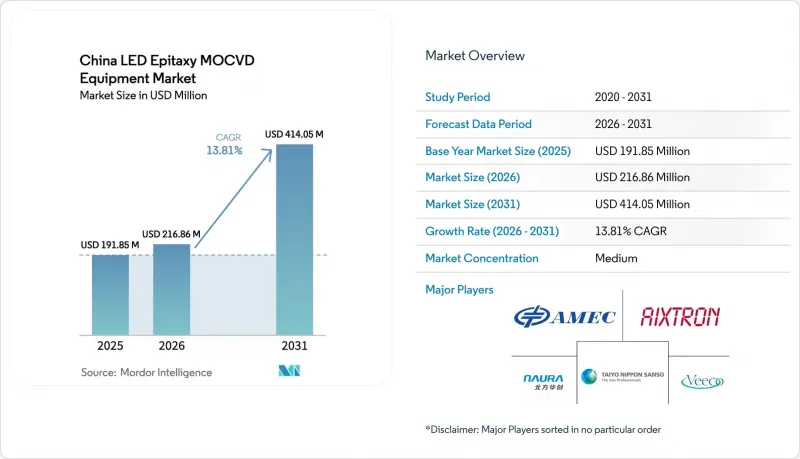

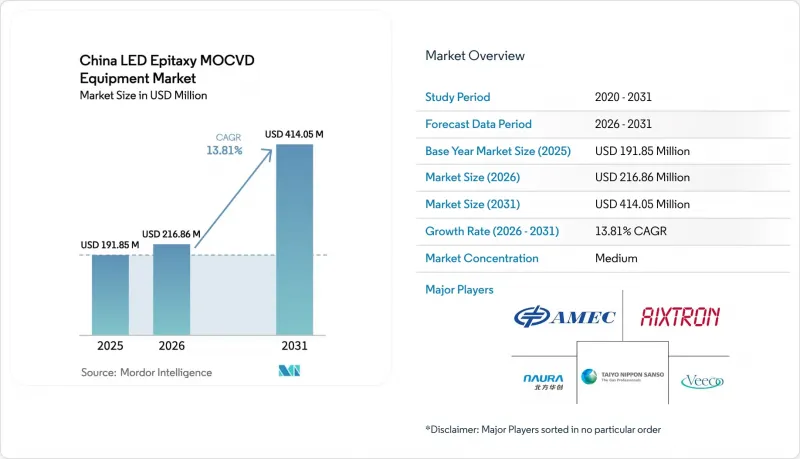

중국의 LED 에피택시 MOCVD 장비 시장 규모는 2025년에 1억 9,185만 달러로 평가되었습니다. 2026년 2억 1,686만 달러에서 2031년까지 4억 1,405만 달러에 이를 것으로 예측되며, 2026년부터 2031년에 걸쳐 CAGR 13.81%를 나타낼 전망입니다.

탄탄한 정책적 지원, 수직계열화된 장치 제조업체들의 빠른 생산능력 확대, 그리고 첨단 디스플레이 및 자동차 용도으로의 꾸준한 전환이 국내 리액터에 대한 투자를 촉진하고 있습니다. 정부의 인센티브를 현지 장비 구매로 연결시키는 강력한 현지 조달 규칙으로 인해 중국 공급업체는 신규 라인의 기본 선택이 되고 있습니다. 한편, 200mm 웨이퍼로의 전환이 임박했다는 것은 일반 조명 수요가 정체되어도 단위당 경제성을 매력적으로 유지할 수 있는 구조적인 비용 재설정을 약속합니다. 주요 스마트폰 및 패널 제조업체들은 현재 파일럿 규모의 마이크로 LED 생산 라인에 투자하고 있으며, 균일성에 대한 사양을 강화하여 밀착형 샤워헤드 구조에 유리하게 작용하고 있습니다. 한편, 갈륨 및 알루미늄 전구체를 둘러싼 공급 리스크가 지속됨에 따라 국내 화학물질 공급원을 확보하기 위한 다년 계약이 가속화되고 있습니다. 이러한 요인들이 복합적으로 작용하여 범용 디바이스 시장의 주기적인 침체에도 불구하고 중국의 LED 에피택시 MOCVD 장비 시장은 견고한 전망을 유지하고 있습니다.

중국의 LED 에피택시 MOCVD 장비 시장 동향과 인사이트

자동차 조명의 고휘도 GaN 기반 LED에 대한 수요 증가

자동차 제조업체들은 할로겐 램프와 HID 램프에서 최대 200루멘/와트까지 구현하는 적응형 GaN 어레이로 전환하고 있으며, 이를 통해 전력 소비를 줄이고 전기자동차의 항속거리를 연장하고 있습니다. Sanan Optoelectronics의 루미레드(Lumileds) 인수는 2025년 루미레드(Lumileds)의 방대한 특허 포트폴리오와 자동차용 인증된 GaN 제조 공정을 확보함으로써, 현지 Tier 1 공급업체가 고부가가치 모듈 시장을 선점할 수 있는 기반을 마련했습니다. 고부가가치 모듈 시장을 선점할 수 있게 되었습니다. 중국 공업정보화부(MIIT)가 발표한 새로운 헤드램프 규정은 눈부심 없는 하이빔 패턴을 의무화하고 있으며, 이로 인해 픽셀 주소 지정이 가능한 GaN은 사실상 적합 기술로 자리 잡게 될 것입니다. 2025년 이후 원자재 비용의 상승도 이러한 고효율 다이를 더욱 유리하게 만들고 있습니다. 왜냐하면 필요한 밝기를 달성하기 위해 필요한 칩 수가 감소했기 때문입니다. 이러한 요인들이 결합되어 헤드램프 제조업체들이 전체 생산라인을 고출력 GaN으로 전환함에 따라 장비 수요가 증가하고 있습니다.

보조금 개혁으로 국내 MOCVD 도입 가속화

2025년 12월의 지침은 국가 보조금 지급 조건으로 국산 장비 채택률 50%를 의무화하여, 공적 자금에 의존하는 팹은 중국산 원자로를 채택하지 않으면 810억 위안(114억 달러)의 지원을 받을 수 없는 상황으로 내몰렸습니다. 이에 반해 Advanced Micro-Fabrication Equipment Inc. China는 현지 조달율 80% 이상의 최신형 6장 및 8장 웨이퍼용 장비 양산 로트를 출하하여 미국 수출 규제에 따른 라이선싱 리스크를 줄였습니다. 초기 도입 기업들은 50회 웨이퍼 처리에서 파장 균일성이 2% 미만이라는 보고가 있으며, 이는 과거에는 고급 수입품에서만 달성할 수 있었던 수준으로, 전환을 가속화하고 있습니다.

일반 조명용 LED 수요 둔화 및 포화 상태

2024년까지 도시 가구의 LED 보급률이 75%를 넘어섰고, 교체 주기가 3년에서 약 7년으로 연장되었습니다. 여기에 부동산 착공 둔화까지 겹치면서 2025년에는 범용 GaN 웨이퍼 가격이 8% 하락하고, 제조업체의 가동률이 70%대 후반까지 떨어질 것으로 예측됩니다. 공급업체들은 자동차, 원예, UVC 분야로 자본을 재분배하고 있지만, 이 과도기는 기존 150mm 장비에 대한 단기적인 주문에 집중되어 있습니다.

부문 분석

2025년 중국의 LED 에피택시 MOCVD 장비 시장에서 GaN 플랫폼은 67.19%의 점유율을 차지했습니다. 이는 자동차 전조등, 원예용 램프 및 파일럿 단계의 마이크로 디스플레이 생산 라인에서의 채택이 주도했습니다. AlGaN 자외선용 장비는 14.53%의 연평균 복합 성장률(CAGR)로 확대될 것으로 예측됩니다. 이는 지자체 수도사업자나 의료사업자들이 화학적 부산물을 발생시키지 않고 소독 기준을 충족하는 무수은 265-275나노미터 파장의 발광소자를 선호하기 때문입니다. 이러한 성장은 질화 알루미늄 웨이퍼의 기술 발전이 뒷받침하고 있습니다. 질화 알루미늄 웨이퍼는 사파이어에 비해 높은 전류 밀도를 실현하고, 램프 당 다이 수를 줄이며, 픽스처 비용을 절감할 수 있습니다.

GaN 제조업체들은 일반 조명 수요의 부진에 대응하기 위해 잉여 생산능력을 고휘도 자동차용 어레이와 초기 단계의 마이크로 디스플레이 인증 시험 생산으로 전환하고 있습니다. 이러한 용도는 엄격한 비닝이 필요하지만, 가격 프리미엄을 얻을 수 있기 때문에 전체적으로 건전한 가동률이 보장됩니다. UV 분야의 지속적인 모멘텀은 기판 기술의 발전에 의존하고 있으며, 질화 알루미늄 웨이퍼는 성능과 비용 효율성 향상에 중요한 역할을 하고 있습니다.

2025년 기준, 중국의 LED 에피택시 MOCVD 장비 시장 규모의 45.24%는 기존 150mm 리액터가 차지했습니다. 200mm 이상의 시스템에 대한 수요는 2031년까지 연평균 14.14% 성장할 것으로 예측됩니다. 이러한 성장은 처리량 증가와 기판 활용률 향상으로 팹이 다이당 비용을 35-40% 절감할 수 있게 된 데 기인합니다.

ALLOS와 Ennostar의 200mm 실리콘 기판 상 GaN 프로그램 등 공동 개발 프로젝트의 급증은 이러한 전환 추세를 뒷받침합니다. 리액터 OEM 업체들은 플레이트 직경을 확대하는 동시에 가스 유량을 미세 조정하여 더 큰 웨이퍼 전체에서 파장 변동이 2% 미만으로 유지되도록 하고 있으며, 이는 고품질 마이크로 디스플레이의 필수 조건입니다. 이러한 파라미터를 조기에 습득한 장비 제조업체는 결정 성장 제조업체가 현재의 리드타임 병목현상을 해소하는 시점에 다음 수주의 물결을 포착할 수 있을 것입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTHThe China LED epitaxy MOCVD equipment market size is projected to be USD 191.85 million in 2025, USD 216.86 million in 2026, and reach USD 414.05 million by 2031, growing at a CAGR of 13.81% from 2026 to 2031.

Solid policy support, rapid capacity expansion by vertically integrated device makers, and a steady pivot toward advanced display and automotive applications are steering capital toward domestic reactors. Strong localization rules that tie government incentives to local tool purchases have made Chinese suppliers the default choice for new lines, while a looming switch to 200 millimeter wafers promises a structural cost reset that keeps unit economics attractive even as general lighting demand plateaus. Large smart phone and panel makers are now underwriting pilot micro LED lines, tightening uniformity specifications that favor close coupled showerhead architectures. Meanwhile, persistent supply risk around gallium and aluminum precursors accelerates multi-year procurement contracts that lock in domestic chemical streams. Together, these factors sustain a robust outlook for the China LED epitaxy MOCVD equipment market despite cyclical softness in commodity devices.

China LED Epitaxy MOCVD Equipment Market Trends and Insights

Rising Demand for High Brightness GaN Based LEDs in Automotive Lighting

Automakers are shifting from halogen or HID lamps to adaptive GaN arrays that deliver up to 200 lumens per watt, cutting power draw and boosting electric-vehicle range. Sanan Optoelectronics' 2025 purchase of Lumileds secured a sizeable patent library and automotive-qualified GaN recipes, positioning local tier-one suppliers to capture higher value modules. New headlamp rules issued by MIIT mandate glare-free high beam patterns, effectively locking in pixel-addressable GaN as the compliant technology. Higher raw material costs since 2025 further favor these efficient dies, because fewer chips now achieve the required brightness. Collectively, these forces lift equipment demand as headlamp makers convert entire production lines to high-power GaN.

Subsidy Reforms Accelerating Domestic MOCVD Adoption

A December 2025 directive links state subsidies to a 50% domestic tool quota, forcing fabs that rely on public funding to qualify Chinese reactors or lose access to RMB 81 billion (USD 11.4 billion) in aid. Advanced Micro-Fabrication Equipment Inc. China responded by shipping production batches of its newest six and eight-wafer tools with over 80% local content, easing licensing risk under United States export controls. Early adopters report wavelength uniformity under 2% across 50 wafer runs, a level once attainable only on premium imports, supporting accelerated switch overs.

Slowdown In General Lighting LED Demand Saturation

Urban households surpassed 75% LED penetration by 2024, elongating replacement cycles from three to roughly seven years. Combined with slower real estate starts, this dynamic reduced commodity GaN wafer pricing by 8 % in 2025 and cut merchant utilization into the high seventies. Suppliers are reallocating capital toward automotive, horticultural, and UVC segments, but the transition period weighs on near term orders for legacy 150 millimeter tools.

Other drivers and restraints analyzed in the detailed report include:

- Capacity Expansion of Chinese IDM LED Manufacturers Post-2026

- Localization Initiatives for Semiconductor Equipment Supply Chains

- High Capital Intensity and Long Payback Periods for New Reactors

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

GaN platforms accounted for 67.19% of the China LED epitaxy MOCVD equipment market share in 2025, driven by their use in automotive headlamps, horticultural lamps, and pilot micro display lines. AlGaN ultraviolet tools are expected to grow at a 14.53% CAGR as municipal water and healthcare operators prefer mercury-free 265-275 nanometer emitters that meet disinfection standards without chemical byproducts. This growth is supported by advancements in aluminum nitride wafers, which enable higher current density compared to sapphire, reducing die counts per lamp and lowering fixture costs.

GaN producers are addressing flat general lighting demand by redirecting surplus capacity into high-brightness automotive arrays and early micro display qualification runs. These applications require tight binning but offer price premiums, ensuring healthy overall utilization. Sustained UV momentum relies on substrate breakthroughs, with aluminum nitride wafers playing a critical role in enhancing performance and cost efficiency.

Legacy 150 millimeter reactors accounted for 45.24% of the China LED epitaxy MOCVD equipment market size in 2025. The demand for 200 millimeter and larger systems is expected to grow at a rate of 14.14% through 2031. This growth is driven by fabs achieving 35-40% per die cost savings through higher throughput and improved substrate utilization.

A surge of joint development projects, such as the 200 millimeter GaN on silicon program between ALLOS and Ennostar, underlines the migration. Reactor OEMs are enlarging platen diameters while refining gas flow to hold sub-2% wavelength variation across larger wafers, prerequisites for premium micro displays. Tool makers that master these parameters early will capture next wave orders once crystal growers clear current lead time bottlenecks.

The China LED Epitaxy MOCVD Equipment Market Report is Segmented by LED Material System (GaN-Based LED Epitaxy Systems, and More), Wafer Size Capability (Up To 100mm, 150mm, and 200mm and Above), Reactor Configuration (Planetary Reactors, and Showerhead Reactors), End User (Integrated LED Manufacturers, and Epitaxy Foundries and Merchant Epi Suppliers). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Advanced Micro-Fabrication Equipment Inc. China

- Veeco Instruments Inc.

- Aixtron SE

- NAURA Technology Group Co., Ltd.

- Jiangsu Advanced Power Semiconductor Co., Ltd.

- Taiyo Nippon Sanso Corporation

- Jusung Engineering Co., Ltd.

- Wuhan HC Semitek Corporation

- Silan Azure Co., Ltd.

- San'an Optoelectronics Co., Ltd.

- HC SemiTek Corp.

- Optigon Technologies (Shanghai) Co., Ltd.

- EpiWorld International Co., Ltd.

- Tsinghua Tongfang Co., Ltd.

- Tianjin Zhonghuan Semiconductor Co., Ltd.

- Chongqing Silan Azure Tech Co., Ltd.

- ProLight Opto Technology Inc.

- Epileds Technologies Inc.

- Changelight Co., Ltd.

- MOCVD Semiconductor Equipment Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for High Brightness GaN-Based LEDs in Automotive Lighting

- 4.2.2 Subsidy Reforms Accelerating Domestic MOCVD Adoption

- 4.2.3 Capacity Expansion of Chinese IDM LED Manufacturers Post-2026

- 4.2.4 Localization Initiatives for Semiconductor Equipment Supply Chains

- 4.2.5 Shift to 200 mm Sapphire Wafers Reducing Per-Device Cost

- 4.2.6 Emerging Micro-LED Display Projects Backed by Smartphone OEMs

- 4.3 Market Restraints

- 4.3.1 Slowdown in General Lighting LED Demand Saturation

- 4.3.2 High Capital Intensity and Long Payback Periods for New Reactors

- 4.3.3 Supply Chain Volatility in High Purity Source Materials

- 4.3.4 Stringent Environmental Compliance Costs for Epitaxy Facilities

- 4.4 Industry Supply Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By LED Material System

- 5.1.1 GaN-based LED Epitaxy Systems

- 5.1.2 AlGaN UV LED Epitaxy Systems

- 5.1.3 AlInGaP LED Epitaxy Systems

- 5.2 By Wafer Size Capability

- 5.2.1 Upto 100 mm

- 5.2.2 150 mm

- 5.2.3 200 mm and Above

- 5.3 By Reactor Configuration

- 5.3.1 Planetary Reactors

- 5.3.2 Showerhead Reactors

- 5.4 By End User

- 5.4.1 Integrated LED Manufacturers (IDMs)

- 5.4.2 Epitaxy Foundries and Merchant Epi Suppliers

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 Advanced Micro-Fabrication Equipment Inc. China

- 6.4.2 Veeco Instruments Inc.

- 6.4.3 Aixtron SE

- 6.4.4 NAURA Technology Group Co., Ltd.

- 6.4.5 Jiangsu Advanced Power Semiconductor Co., Ltd.

- 6.4.6 Taiyo Nippon Sanso Corporation

- 6.4.7 Jusung Engineering Co., Ltd.

- 6.4.8 Wuhan HC Semitek Corporation

- 6.4.9 Silan Azure Co., Ltd.

- 6.4.10 San'an Optoelectronics Co., Ltd.

- 6.4.11 HC SemiTek Corp.

- 6.4.12 Optigon Technologies (Shanghai) Co., Ltd.

- 6.4.13 EpiWorld International Co., Ltd.

- 6.4.14 Tsinghua Tongfang Co., Ltd.

- 6.4.15 Tianjin Zhonghuan Semiconductor Co., Ltd.

- 6.4.16 Chongqing Silan Azure Tech Co., Ltd.

- 6.4.17 ProLight Opto Technology Inc.

- 6.4.18 Epileds Technologies Inc.

- 6.4.19 Changelight Co., Ltd.

- 6.4.20 MOCVD Semiconductor Equipment Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment