|

시장보고서

상품코드

2044064

중국의 데이터센터 랙 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)China Data Center Rack - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

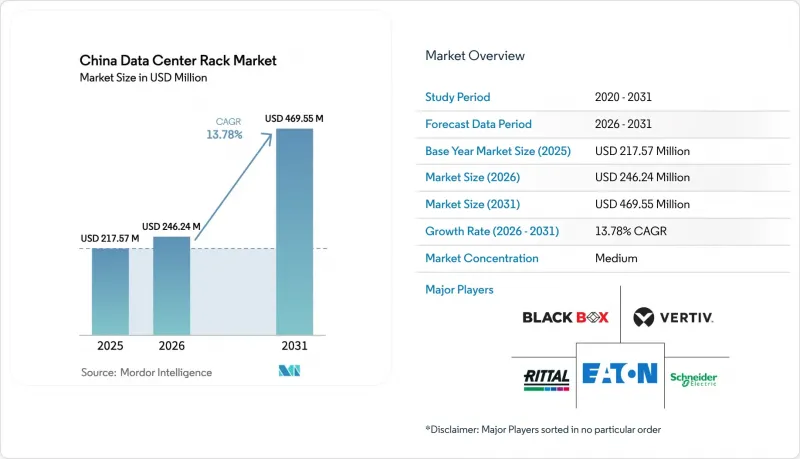

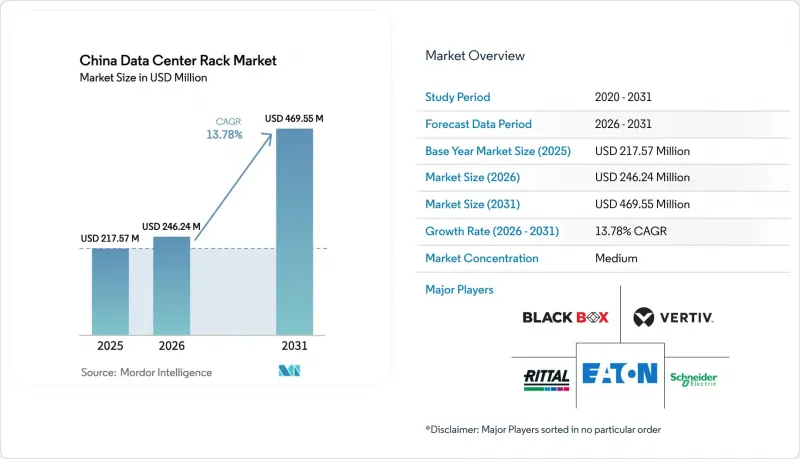

중국의 데이터센터 랙 시장 규모는 2025년 2억 1,757만 달러로 평가되었습니다. 2026년 2억 4,624만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 13.78%를 나타내, 2031년에는 4억 6,955만 달러에 이를 것으로 예측됩니다.

'동부 데이터, 서부 컴퓨팅' 정책으로 인해 하이퍼스케일 워크로드가 저렴한 재생에너지와 자연 냉각에 적합한 기후를 갖춘 내륙의 허브로 이동함에 따라 수요가 가속화되고 있습니다. 한때 틈새 시장이었던 액체 냉각 캐비닛은 인공지능(AI) 클러스터의 랙 전력 밀도가 30kW를 넘어서면서 이제는 주류로 채택되고 있습니다. 국유 통신 사업자는 버스웨이 배전 및 공장 출하 컨테이너를 갖춘 전체 높이 캐비닛을 표준화하여 설치 시간을 단축하고 지역 간 통일성을 높였습니다. 반면, 중견기업과 5G 사업자들은 설치 공간이 제한적인 엣지 노드를 위해 컴팩트한 하프하이트(Half-Height) 형태를 선호하고 있습니다. 이러한 배경에서 파워, 텔레메트리, 냉각 루프를 통합한 사전 시운전된 랙 행을 출하할 수 있는 벤더는 하이퍼스케일러와 코로케이션 제공업체 모두로부터 점점 더 많은 지지를 받고 있습니다.

중국의 데이터센터 랙 시장 동향 및 인사이트

클라우드 및 AI 워크로드 급증으로 고밀도 랙에 대한 수요 증가 주도

인공지능(AI) 클러스터의 전력 소비량은 현재 랙당 30kW를 넘어섰기 때문에 사업자들은 8-12kW용으로 설계된 액체 냉각 매니폴드를 갖춘 구형 캐비닛을 개조할 수밖에 없습니다. 화웨이의 'CloudMatrix 384' 테스트베드에서 서버 1대당 8개의 H100급 가속기를 호스팅하기 위해서는 전력 공급 용량을 50kW까지 확장해야 하는 것으로 나타났습니다. 국내 AI 관련 매출은 2025년 410억 달러를 넘어 2028년까지 960억 달러에 달할 것으로 예측됩니다. 금융, 의료 등 기밀성이 높은 분야는 서버 수요의 5%에 불과하지만, 부정 조작 감지 기능을 갖춘 On-Premise형 캐비닛을 강력하게 요구하고 있으며, 이를 위해 랙에 능동형 냉각 및 보안 기능을 탑재할 것을 요구하고 있습니다. Dell'&Oro Group의 보고서에 따르면, 2026년 1분기 직접 액체 냉각 매출은 2배 이상 증가했으며, 이는 600kW급 랙 열에 필요한 버스웨이 파워레일에 대한 수요가 40% 급증한 것을 반영하고 있습니다. 이러한 요인들이 결합되어 중국의 데이터센터 랙 시장은 더 높은 전력 용량, 더 높은 수준의 원격 측정 및 공장 통합 냉각 루프를 향해 나아가고 있습니다.

하이퍼스케일 및 코로케이션 시설 도입 확대

GDS 홀딩스는 2024년 3분기에 8만 8,000평방미터의 신규 화이트스페이스를 확보했고, 브로드넷은 2025년 중반까지 7만 2,000개의 캐비닛을 운영했으며, 추가로 23만 개의 캐비닛을 계획하고 있습니다. 코로케이션 업계의 주요 기업들은 버스바, PDU 및 컨테이너를 표준으로 장착한 Scorpio 프레임을 채택하여 현장 작업 인력을 60% 절감하고 있습니다. 간쑤성 국가전신망 클라우드 노드는 3,000개 랙에 1억 3,700만 달러를 투자하여 턴키 방식의 랙 그룹의 자본 집약성을 강조하고 있습니다. 하이퍼스케일러 업체들은 현재 유통업체를 거치지 않고 제조업체와 직접 다년 계약을 맺고 랙을 조달하고 있으며, 이 관행은 공동 설계 능력이 없는 소규모 벤더에게는 불리한 상황입니다. VNET Group의 2024년 3분기 매출은 견조한 코로케이션 수요로 인해 전년 동기 대비 14.3% 증가했으며, 분기당 수천 개의 동일한 캐비닛을 공급할 수 있는 사업자에게 축적되는 규모의 경제가 부각되었습니다.

블레이드 및 컨버지드 시스템을 통해 기존 랙의 수를 줄일 수 있습니다.

하이퍼컨버지드 어플라이언스는 컴퓨팅, 스토리지, 네트워크 기능을 단일 섀시에 통합하여 BFSI(은행, 금융, 보험) 산업 및 지점 거점의 랙 설치 면적을 줄여줍니다. 출하량은 감소하는 반면, 컨버지드 캐비닛은 더 견고한 프레임, 듀얼 버스바, 강화 캐스터가 필요하기 때문에 평균 판매가격이 상승하고 있습니다. 3계층 네트워크로 개조하는 기업들은 42U에서 48U 포맷으로 업사이징하는 경우가 많으며, 이로 인해 출하량 감소가 일부 완화되고 있습니다. 따라서 공급업체는 미묘한 위협에 직면하고 있습니다. 즉, 캐비닛 수는 감소하는 반면, 대당 탑재 용량은 증가하고 있는 것입니다. 경쟁 우위는 공기 흐름에 영향을 주지 않고 1,500kg의 정적 하중을 견딜 수 있는 강화 케이스를 공급할 수 있느냐에 달려 있습니다.

부문 분석

하프 랙은 마이크로 엣지 사이트와 5G 무선 노드가 컴팩트하고 견고한 포맷을 필요로 하기 때문에 CAGR 14.54%로 중국 전체 데이터센터 랙 시장보다 더 높은 성장세를 보일 것으로 예측됩니다. 통신사업자들이 도로변 기지국 근처의 먼지와 습기를 견딜 수 있는 IP65 규격의 캐비닛을 도입함에 따라 중국의 데이터센터 랙 시장에서 하프 랙의 규모가 확대되고 있습니다. 에지 배포의 전력 소비는 3-4 kW를 초과하는 경우는 드물지만, 그럼에도 불구하고 파괴 행위를 방지하기 위해 생체 인식 잠금 장치와 원격 원격 측정이 요구되고 있습니다. 반면, 풀랙은 42U 및 48U Scorpio 프레임을 표준으로 하는 하이퍼스케일 계약 덕분에 2025년 71.32%의 점유율을 확보했습니다. 이러한 대형 인클로저는 공기 흐름과 케이블 경로를 간소화하고, 조립 시간을 단축하며, 여러 캠퍼스 간 일관성을 높입니다.

풀하이트 형식은 하이퍼스케일 시설 내 핵심 설비로 계속 자리 잡을 것입니다. 이는 사업자가 컨테이너 단위로 대량 구매를 하기 때문에 수익률이 압축되고, 공장의 생산량을 예측할 수 있기 때문입니다. 쿼터 랙과 벽걸이형 마이크로 인클로저는 밀도보다 미적 감각을 중시하는 소매 체인이나 지점 사무실에서 계속 채택되고 있습니다. Inspur의 사막 대응 "Desert Ship" 시리즈는 광범위한 온도 환경에 대응하고 방진 필터를 갖춘 캐비닛으로의 전환을 상징하며, 현재 중국 서부 풍력 발전 벨트 지역에 재도입이 진행되고 있습니다. 사전 배선이 완료된 상태로 배송되는 신속한 배치 설계는 설치 시간을 최대 40%까지 단축시켜 새로운 홀의 운영을 서둘러야 하는 코로케이션 제공업체에게 생산성 측면에서 큰 이점을 제공합니다.

2025년에는 밀폐형 캐비닛이 75.33%의 점유율을 차지했습니다. 이는 변조 감지, EMI 차폐, 내진 고정에 대한 BFSI(은행, 금융, 보험) 부문의 엄격한 규제를 반영한 것입니다. 이 부문은 사이버 리스크 규제 강화에 따라 CAGR 14.76%로 성장하여 중국 전체 데이터센터 랙 시장보다 더 빠른 속도로 성장할 것으로 예측됩니다. 오픈 프레임 랙은 이미 접근이 제한되어 있고, 기류 효율이 최우선인 하이퍼스케일러에 여전히 선호되고 있습니다. 그럼에도 불구하고 하이퍼스케일러 사업자들은 메쉬도어 삽입과 사각지대 카메라 도입을 늘리고 있어 비용 격차는 줄어들고 있습니다.

벽걸이형과 마이크로 엣지형은 IoT 게이트웨이, 소매점 계산대 허브, 스마트팩토리 셀 등으로 보급이 확산되고 있습니다. 따라서 기업들은 초기 비용 절감보다 물리적 컴플라이언스 기능을 우선시하기 때문에 중국의 데이터센터 랙 시장에서 인클로저형 캐비닛의 점유율은 여전히 압도적입니다. 슈나이더일렉트릭과 버티브는 각각의 EcoStruxure 및 Vertiv Life 플랫폼에 원활하게 통합되는 모듈형 액세서리(수직 PDU, 브러시 스트립이 있는 침입 패널, 환경 프로브 등)를 통해 직접 경쟁하고 있습니다. 운영자는 전력 및 열 데이터를 중앙에서 관리할 수 있는 대시보드를 사용할 수 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTH 26.05.29The China data center rack market size is expected to grow from USD 217.57 million in 2025 to USD 246.24 million in 2026 and is forecast to reach USD 469.55 million by 2031 at a 13.78% CAGR over 2026-2031.

Demand is accelerating as the Eastern Data, Western Computing policy moves hyperscale workloads toward inland hubs that offer inexpensive renewable energy and free-cooling climates. Liquid-cooling cabinets, once niche, now command mainstream adoption because rack power densities have climbed past 30 kilowatts in artificial-intelligence clusters. State-owned carriers are standardizing on full-height cabinets with busway distribution and factory-installed containment, thereby reducing installation time and improving consistency across regions. Mid-sized enterprises and 5G operators, meanwhile, favor compact half-height formats for edge nodes where floor space is constrained. Against this backdrop, vendors able to ship pre-commissioned rows with integrated power, telemetry, and coolant loops capture growing preference from both hyperscalers and colocation providers.

China Data Center Rack Market Trends and Insights

Surge in Cloud and AI Workloads Driving High-Density Rack Demand

Artificial-intelligence clusters now exceed 30 kilowatts per rack, forcing operators to retrofit old cabinets with liquid manifolds designed for only 8-12 kilowatts. Huawei's CloudMatrix 384 testbed showed that power delivery must scale to 50 kilowatts to host eight H100-class accelerators per server. Domestic AI revenues surpassed USD 41 billion in 2025 and could top USD 96 billion by 2028. Sensitive sectors such as finance and healthcare account for only 5% of server demand but insist on on-prem cabinets with tamper detection, nudging racks toward active cooling and security functions. Dell'Oro Group reported that direct liquid-cooling revenue more than doubled in Q1 2026, mirroring a 40% surge in busway power rails needed for 600-kilowatt rows. Together, these forces propel the China data center rack market toward higher wattages, richer telemetry, and factory-integrated coolant loops.

Increasing Deployment of Hyperscale and Colocation Facilities

GDS Holdings committed 88,000 square meters of new white space in Q3 2024, while BroadNet operated 72,000 cabinets by mid-2025 with another 230,000 in pipeline. Colocation leaders standardize on Scorpio frames that arrive with busbars, PDUs, and containment, cutting on-site labor by 60%. Gansu State Grid's cloud node invested USD 137 million for 3,000 racks, underscoring the capital intensity of turnkey rows. Hyperscalers now bypass distributors, locking multi-year rack contracts directly with manufacturers, a practice that disadvantages small vendors lacking co-engineering capacity. VNET Group's Q3 2024 revenue climbed 14.3% year-over-year on persistent colocation demand, spotlighting the scale dividends accruing to players that can deliver thousands of identical cabinets each quarter.

Blade and Converged Systems Reducing Traditional Rack Counts

Hyper-converged appliances pack compute, storage, and networking into a single chassis, trimming rack footprints for BFSI and branch sites. Although unit shipments decline, average selling prices rise because converged cabinets need heavier frames, dual busbars, and reinforced casters. Enterprises retrofitting three-tier networks often upsize from 42U to 48U formats, partially cushioning unit erosion. Vendors therefore face a nuanced threat; fewer cabinets but richer content per cabinet. Competitive positioning hinges on supplying reinforced enclosures that can handle 1,500-kilogram static loads without sacrificing airflow.

Other drivers and restraints analyzed in the detailed report include:

- Government Eastern Data, Western Computing Initiative Accelerating Build-Outs

- Carbon-Neutral Mandates Fostering Liquid-Cooling-Ready Rack Adoption

- Land and Power Quota Caps in Tier-1 Cities Tightening Data-Center Approvals

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Half racks will outpace the broader China data center rack market with a 14.54% CAGR because micro edge sites and 5G radio nodes need compact, rugged formats. The China data center rack market size for half racks is expanding as operators install cabinets rated IP65 to handle dust and moisture near street-level base stations. Edge deployments seldom exceed 3-4 kilowatts, yet still demand biometric locks and remote telemetry to deter vandalism. In contrast, full racks secured 71.32% of share in 2025 thanks to hyperscale contracts that standardize on 42U and 48U Scorpio frames. These larger enclosures streamline airflow and cable routes, lowering assembly hours and boosting consistency across multiple campuses.

Full-height formats will remain the backbone inside hyperscale halls because operators buy them in container-load volumes, compressing margins but creating predictable factory throughput. Quarter racks and wall-mount micro enclosures persist in retail chains and branch offices where aesthetics trump density. Inspur's desert-rated "Desert Ship" family highlights the march toward wide-temperature, dust-filtered cabinets that are now repatriating to western China wind belts. Rapid-deploy designs that arrive pre-cabled slash installation times by up to 40%, a productivity edge valued by colocation providers racing to bring new halls online.

Enclosed cabinets held 75.33% share in 2025, reflecting strict BFSI rules for tamper detection, EMI shielding, and seismic anchoring. The segment will grow faster than the overall China data center rack market, advancing 14.76% CAGR as cyber-risk regulations tighten. Open-frame racks remain favored by hyperscalers where access is already restricted and airflow efficiency is paramount. Even so, hyperscale operators increasingly add mesh-door inserts and blind-spot cameras, narrowing the cost gap.

Wall-mount and micro-edge styles gain traction in IoT gateways, retail checkout hubs, and smart-factory cells. The China data center rack market share for enclosed cabinets therefore remains dominant because enterprises continue to prioritize physical compliance features over initial cost savings. Schneider Electric and Vertiv compete head-to-head with modular accessories vertical PDUs, brush strip ingress panels, and environmental probes that integrate seamlessly into their respective EcoStruxure and Vertiv Life platforms, giving operators unified dashboards for power and thermal data.

The China Data Center Rack Market Report is Segmented by Rack Size (Quarter Rack, Half Rack, and Full Rack), Rack Type (Enclosed Cabinet, Open-Frame, and Wall-Mount and Micro-Edge Enclosure), Tier Type (Tier 1 and 2, Tier 3, and Tier 4), Data Center Size (Small, Medium, Large, and Hyperscale), Data Center Type (Colocation, Hyperscalers/CSPs, and Enterprise and Edge). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Eaton Corporation

- Black Box Corporation

- Rittal GmbH and Co. KG

- Schneider Electric SE

- Vertiv Group Corp.

- Dell Technologies Inc.

- nVent Electric PLC

- Hewlett Packard Enterprise

- Legrand SA

- Fujitsu Corporation

- Huawei Technologies Co. Ltd.

- Inspur Group

- Sugon Information Industry

- ZTE Corporation

- GreatIoT (Shenzhen) Technology

- Tripp Lite by Eaton

- Panduit Corp.

- Belden Inc.

- CyberPower Systems

- StarTech.com

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Deployment of Hyperscale and Colocation Facilities

- 4.2.2 Surge in Cloud and AI Workloads Driving High-Density Rack Demand

- 4.2.3 Government "Eastern Data, Western Computing" Initiative Accelerating Build-Outs

- 4.2.4 Carbon-Neutral Mandates Fostering Liquid-Cooling-Ready Rack Adoption

- 4.2.5 5G Edge Build-Outs Requiring Compact Micro-Racks in Base Stations

- 4.2.6 Rising BFSI Digital-Core Upgrades Requiring Secure On-Prem Racks

- 4.3 Market Restraints

- 4.3.1 Blade and Converged Systems Reducing Traditional Rack Counts

- 4.3.2 Land and Power Quota Caps in Tier-1 Cities Tightening Data-Center Approvals

- 4.3.3 U.S. Export-Control Limits on High-End Chips Slowing Ultra-Dense Rack Roll-Outs

- 4.3.4 Skilled-Labor Shortages for Advanced Rack Integration and Maintenance

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Rack Size

- 5.1.1 Quarter Rack (More than 11U)

- 5.1.2 Half Rack (12-22U)

- 5.1.3 Full Rack (More than Equal to 42U)

- 5.2 By Rack Type

- 5.2.1 Enclosed Cabinet

- 5.2.2 Open-Frame

- 5.2.3 Wall-Mount and Micro-Edge Enclosure

- 5.3 By Tier Type

- 5.3.1 Tier 1 and 2

- 5.3.2 Tier 3

- 5.3.3 Tier 4

- 5.4 By Data Center Size

- 5.4.1 Small Data Center

- 5.4.2 Medium Data Center

- 5.4.3 Large Data Center

- 5.4.4 Hyperscale Data Center

- 5.5 By Data Center Type

- 5.5.1 Colocation Data Center

- 5.5.2 Hyperscalers Data Center/CSPs

- 5.5.3 Enterprise and Edge Data Center

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 Eaton Corporation

- 6.4.2 Black Box Corporation

- 6.4.3 Rittal GmbH and Co. KG

- 6.4.4 Schneider Electric SE

- 6.4.5 Vertiv Group Corp.

- 6.4.6 Dell Technologies Inc.

- 6.4.7 nVent Electric PLC

- 6.4.8 Hewlett Packard Enterprise

- 6.4.9 Legrand SA

- 6.4.10 Fujitsu Corporation

- 6.4.11 Huawei Technologies Co. Ltd.

- 6.4.12 Inspur Group

- 6.4.13 Sugon Information Industry

- 6.4.14 ZTE Corporation

- 6.4.15 GreatIoT (Shenzhen) Technology

- 6.4.16 Tripp Lite by Eaton

- 6.4.17 Panduit Corp.

- 6.4.18 Belden Inc.

- 6.4.19 CyberPower Systems

- 6.4.20 StarTech.com

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment