|

시장보고서

상품코드

2044071

미국의 판유리 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United States Flat Glass - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

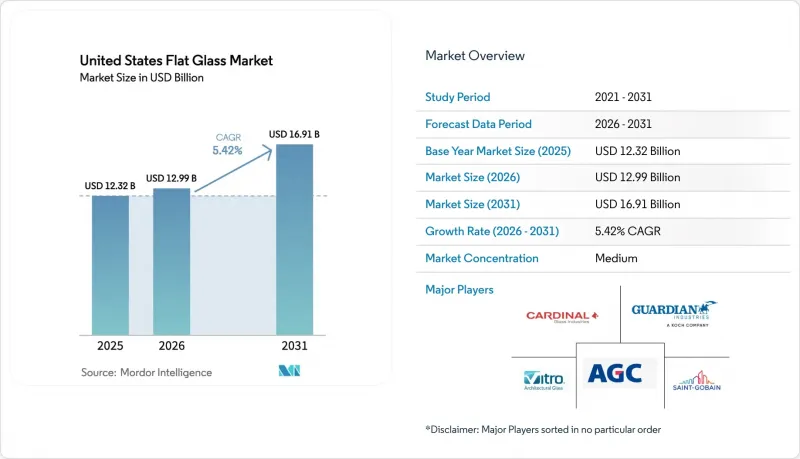

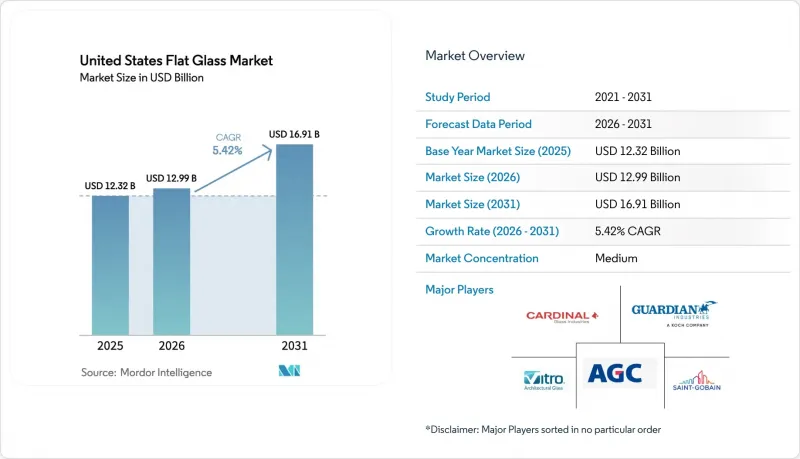

미국의 판유리 시장 규모는 2025년 123억 2,000만 달러로 평가되었습니다. 2026년 129억 9,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 5.42%를 나타내, 2031년까지 169억 1,000만 달러에 이를 것으로 예측됩니다.

태양광 발전 설비 설치 장려책, 에너지 절약형 개보수 의무화, 전기자동차용 유리 수요로 인해 조달 전략이 재편되면서 수요가 범용 플로트 유리에서 수익성이 높은 코팅 및 가공 제품으로 이동하고 있습니다. 미국의 판유리 시장은 숙련된 인력 부족과 탄소 규제 강화로 인한 운영 비용 증가에 직면해 있으며, 이에 따라 생산자들은 가격 결정력을 통해 규제 준수 비용을 상쇄할 수 있는 고부가가치 분야로 전환하고 있습니다. 수직 통합형 태양광 유리 생산업체는 이미 지속 가능한 수익률을 확보한 반면, 전통적인 건축용 유리 공급업체는 최근 반덤핑 조치 이후에도 수입 경쟁의 격화에 직면해 있습니다. 국내 7개 플로트 유리 제조업체 간의 통합이 진행되는 한편, 하류 가공업체 기반은 활기를 띠고 있으며, 공급망에 따라 고객의 협상력이 크게 달라지고 있습니다. 전반적으로 미국의 판유리 시장에서는 현재 단순한 생산량뿐만 아니라 다층 라미네이트, 다이나믹 틴팅 또는 초저방사율 스퍼터링 기술을 제공할 수 있는 기업이 평가받고 있습니다.

미국의 판유리 시장 동향과 인사이트

IRA 우대 조치로 국내 태양광 패널 제조 확대

연방세법 제45X조에 근거한 세액공제는 태양광 유리 1평방미터당 12달러를 지급하여 수십억 달러 규모의 그린필드 프로젝트를 지원하고 있습니다. 이로 인해 수직통합형 생산라인은 일반용 플로트 유리의 가격 변동에 영향을 덜 받습니다. 퍼스트솔라는 2025년 루이지애나주와 앨라배마주에 3.5GW의 생산라인을 증설하여 미국 내 생산능력은 14GW에 달했습니다. 필킨턴은 오하이오 주 로스포드에 위치한 플로트 공장을 투명 전도성 산화물(TCO) 공급기지로 전환했습니다. 이는 미국의 판유리 시장에서 독자적인 비용 요인을 가진 병렬 태양전지 기판 공급망이 생겨나고 있음을 보여줍니다. 대출 프로그램 사무실의 지침은 자금 조달 장벽을 더욱 낮추고 신규 진출기업이 건축용 플로트 유리 대신 태양전지용 유리를 목표로 삼도록 장려하고 있습니다.

에너지 절약형 건축물의 건설 및 개보수 활동의 활성화

IRA(인플레이션 억제법)에 의한 연방 조달청(GSA)의 조달 요건은 현재 최상급 판유리에 대해 톤당 1,331kg CO2e(이산화탄소 환산)의 저탄소 함량 제한을 규정하고 있으며, 이로 인해 칼렛 비율이 높은 용광로와 전기 보조 가열을 채용한 용광로에 대한 수요가 증가하고 있습니다. 로에 대한 수요가 전환되고 있습니다. 버클리 연구소의 조사에 따르면 저방사선(Low-E) 코팅은 이미 미국 주택의 80%에 적용되고 있으며, U값이 0.20 미만인 삼중 유리 유닛이 다음 개조 표준으로 부상하고 있습니다. 이러한 추세에 따라 미국 평면유리 시장은 호황을 누리고 있습니다. 이는 가공업체가 스페이서 바 및 에지 씰링 라인의 자동화를 통해 평방 피트당 가치 상승을 포착할 수 있기 때문입니다.

플로트로에 대한 미국의 탄소 배출 규제 강화

EPA Subpart N의 보고 의무와 더불어 Subpart CC에 따른 미립자 물질 및 SOx 배출 제한으로 인해 고가의 배출 저감 개조가 의무화되어 있습니다. 가디언사가 2024년 캘리포니아 주 킹스버그의 플로트 공장을 폐쇄한 것은 이 지역의 에너지 및 탄소 정책에 대한 취약성을 부각시키고 있습니다. 생산자들은 전기 증압에 대한 투자, 이전, 또는 범용 플로트 사업에서 철수 중 하나를 선택해야 했고, 이로 인해 미국의 판유리 시장은 컴플라이언스 비용을 수익률로 흡수할 수 있는 고부가가치 코팅 분야로 이동하고 있습니다.

부문 분석

어닐링 유리는 2025년 매출의 62.33%를 차지했지만, 허리케인, 폭발 사고, 건축법 강화로 인해 더 많은 용도가 강화 유리와 접합 유리로 전환되고 있어 점유율이 감소하고 있습니다. 가공 유리는 예측 기간(2026-2031년) 동안 CAGR 6.78%로 성장하여 미국 전체 평면 유리 시장을 능가할 것으로 예측됩니다. 미국 내 가공 평면유리 시장 규모는 건축 기준의 확대와 함께 증가했으며, 절단부터 강화, 엣지 실링까지 신속하게 대응할 수 있는 통합형 공장의 혜택을 누리고 있습니다.

강화, 접합, 가스 충전, 품질 검사를 하나의 라인에 통합한 가공업체는 단일 강화유리를 판매하는 동종업계에 비해 평방피트당 수익이 약 30-40% 더 높은 것으로 나타났습니다. Glaston과 Fenzi의 E-Coat 인쇄 플랫폼의 신규 도입은 다운스트림 공정의 자동화를 위한 설비 투자의 변화를 뒷받침하며, 미국의 판유리 시장에서 가공 제품의 선도적 지위를 강화할 수 있는 모멘텀을 강화합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTH 26.05.29The United States Flat Glass Market size is expected to grow from USD 12.32 billion in 2025 to USD 12.99 billion in 2026 and is forecast to reach USD 16.91 billion by 2031 at a 5.42% CAGR over 2026-2031.

Demand is pivoting from commodity float toward higher-margin coated and processed products as solar-manufacturing incentives, energy-efficient retrofit mandates, and electric-vehicle glazing needs reshape procurement strategies. The United States flat glass market is also contending with skilled-labor shortages and tightening carbon rules that raise operating costs, nudging producers toward value-added segments where pricing power offsets compliance outlays. Vertically integrated solar-glass producers are already securing sustainable margins, while traditional architectural suppliers face intensified import competition even after recent anti-dumping actions. Consolidation among the seven domestic float operators co-exists with a vibrant downstream fabricator base, so customer leverage varies sharply along the chain. Overall, the United States flat glass market now rewards firms that can deliver multi-layer lamination, dynamic tinting, or ultra-low-emissivity sputtering rather than raw tonnage alone.

United States Flat Glass Market Trends and Insights

Expansion of Domestic Solar-Panel Manufacturing Under IRA Incentives

Federal Section 45X credits pay USD 12 per m2 of solar glass, underpinning multi-billion-dollar greenfield projects that insulate vertically integrated lines from merchant-float volatility. First Solar added 3.5 GW lines in Louisiana and Alabama in 2025, bringing the United States' capacity to 14 GW. Pilkington converted its Rossford, Ohio float into a transparent-conductive-oxide supply, illustrating how the United States flat glass market is birthing a parallel solar substrate chain with distinct cost drivers. Loan Programs Office guidance further lowers financing barriers, encouraging new entrants to target solar rather than architectural float.

Rising Construction-Retrofit Activity for Energy-Efficient Buildings

IRA-funded General Services Administration procurement now specifies low-embodied-carbon limits of 1,331 kg CO2e (carbon dioxide-equivalent)/ton for top-tier flat glass, shifting demand toward furnaces with high cullet ratios or electric boosting. Berkeley Lab finds Low-E coatings already cover 80% of United States homes, yet triple-pane units with U-factors below 0.20 are emerging as the next retrofit standard. That dynamic elevates the United States flat glass market as fabricators are able to automate spacer-bar and edge-seal lines, capturing rising per-square-foot values.

Tightening US Carbon-Emission Rules on Float Furnaces

EPA Subpart N reporting plus particulate and SOx limits under Subpart CC compel costly abatement retrofits; Guardian's 2024 closure of its Kingsburg, California float underscores vulnerability to regional energy and carbon policies. Producers must decide whether to invest in electric boosting, relocate, or exit commodity float, pushing the United States flat glass market toward high-value coatings where margins can absorb compliance premiums.

Other drivers and restraints analyzed in the detailed report include:

- Automotive Lightweighting and Safety-Glazing Mandates

- Growing Demand for Electronic Displays

- Skilled-Labor Shortages in Advanced Glass Processing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Annealed Glass retained 62.33% of 2025 revenue, yet its share is slipping as hurricanes, blasts, and overhead codes move more applications to tempered or laminated forms. Processed Glass expanded at a 6.78% CAGR during the forecast period (2026-2031), outstripping the overall United States Flat Glass market. The United States flat glass market size for processed offerings rose in tandem with code adoption, rewarding integrated shops able to move quickly from cutting to tempering to edge-sealing.

Fabricators that consolidate tempering, laminating, gas filling, and quality inspection on one line earn roughly 30-40% higher revenue per square foot than peers selling stand-alone annealed sheets. New installs from Glaston and Fenzi's E-Coat printing platform validate the capital shift toward downstream automation, reinforcing the momentum behind processed product leadership inside the United States Flat Glass market.

The United States Flat Glass Market Report is Segmented by Product Type (Annealed Glass (Including Tinted Glass), Coater Glass, Patterned Glass, and More), Coating Type (Low-E (Hard-Coat), Solar-Control (Soft-Coat), and More), End-User Industry (Building and Construction, Automotive, Solar Glass, and Other End-User Industries (Electronics, Aerospace, and More)). The Market Size and Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- AGC Inc.

- CARDINAL GLASS INDUSTRIES, INC

- Central Glass Co., Ltd.

- China CSG Group Co., Ltd.

- Corning Incorporated

- First Solar

- Fuyao Group

- Guardian Industries

- Nippon Sheet Glass Co., Ltd

- Saint-Gobain

- SCHOTT

- Sisecam

- Specialty Glass Products

- Swift Glass

- Vitro

- Xinyi Glass Holdings Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for electronic displays

- 4.2.2 Rising construction-retrofit activity for energy-efficient buildings

- 4.2.3 Expansion of domestic solar-panel manufacturing under IRA incentives

- 4.2.4 Automotive lightweighting and safety-glazing mandates

- 4.2.5 Emergence of dynamic/smart glass in commercial real estate

- 4.3 Market Restraints

- 4.3.1 Tightening US carbon-emission rules on float furnaces

- 4.3.2 Skilled-labor shortages in advanced glass processing

- 4.3.3 Competition from imported low-cost processed glass

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Annealed Glass (Including Tinted Glass)

- 5.1.2 Coater Glass

- 5.1.3 Patterned Glass

- 5.1.4 Processed Glass

- 5.1.5 Mirrors

- 5.2 By Coating Type

- 5.2.1 Low-E (Hard-Coat)

- 5.2.2 Solar-Control (Soft-Coat)

- 5.2.3 Self-Cleaning

- 5.2.4 Anti-Reflective

- 5.2.5 Others

- 5.3 By End-User Industry

- 5.3.1 Building and Construction

- 5.3.2 Automotive

- 5.3.3 Solar Glass

- 5.3.4 Other End-user Industries (Electronics, Aerospace, and more)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 AGC Inc.

- 6.4.2 CARDINAL GLASS INDUSTRIES, INC

- 6.4.3 Central Glass Co., Ltd.

- 6.4.4 China CSG Group Co., Ltd.

- 6.4.5 Corning Incorporated

- 6.4.6 First Solar

- 6.4.7 Fuyao Group

- 6.4.8 Guardian Industries

- 6.4.9 Nippon Sheet Glass Co., Ltd

- 6.4.10 Saint-Gobain

- 6.4.11 SCHOTT

- 6.4.12 Sisecam

- 6.4.13 Specialty Glass Products

- 6.4.14 Swift Glass

- 6.4.15 Vitro

- 6.4.16 Xinyi Glass Holdings Limited

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment