|

시장보고서

상품코드

2044192

인쇄 장비 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Print Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

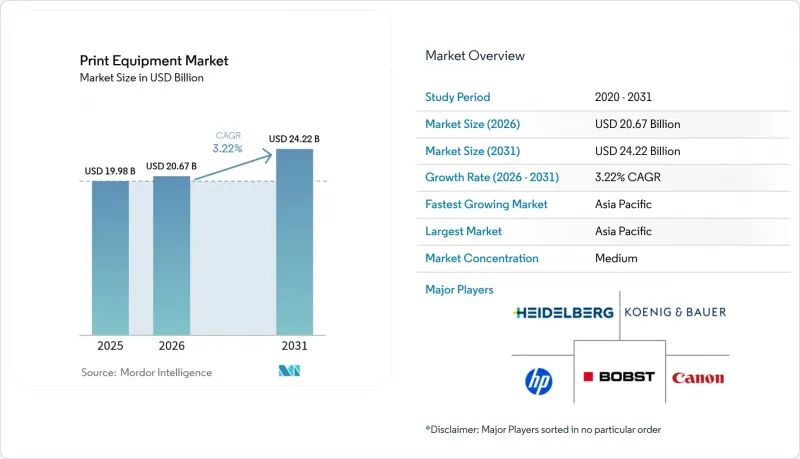

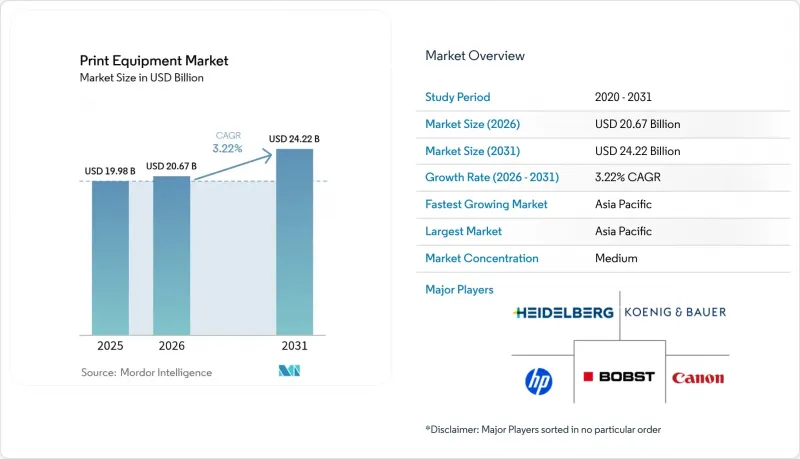

인쇄 장비 시장 규모는 2025년 199억 8,000만 달러, 2026년 206억 7,000만 달러에서 2031년까지 242억 2,000만 달러로 확대될 것으로 예측되고 있으며 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 3.22%를 나타낼 전망입니다.

컨버터 업체들이 빠른 전환, 최소 설정 시간, 가변 데이터 인쇄 기능을 추구함에 따라, 수요는 오프셋 인쇄에서 디지털 및 하이브리드 인쇄기로 이동하고 있습니다. 유럽연합(EU)과 미국의 식품 및 의약품 라벨 표시 규제로 인해 시리얼라이제이션 및 알레르겐 표시에 대응하는 인쇄기에 대한 투자가 촉진되고 있습니다. EC 풀필먼트 센터에서는 당일 배송 상자를 인쇄하기 위해 좁은 웹 디지털 장비를 도입하고 있으며, 브랜드 소유자는 마이크로 부문에 대응하기 위해 SKU 수를 늘리고 있습니다. 소프트웨어 중심의 신규 시장 진출기업들의 경쟁 압력으로 인해 기존 인쇄기 제조업체들은 클라우드 연결형 워크플로우 플랫폼과 구독형 플랜을 추가할 수밖에 없는 상황에 처해 있습니다. 이러한 전환은 자금 조달의 필요성을 증가시키지만, 높은 정착성 서비스 수익을 가져다 줄 것으로 기대됩니다.

세계 인쇄 장비 시장 동향과 인사이트

식품 및 의약품 디지털 라벨에 대한 규제적 측면의 추동력

EU와 미국의 표시 규정에 따라 디지털 워터마크, 가변 알레르기 유발 물질 표시, 로트 단위의 추적성이 의무화됨에 따라 컨버터 업체들은 잉크젯으로 전환하거나 새로운 디지털 인쇄기를 도입해야 하는 상황에 처해 있습니다. 인도에서는 2025년 4월부터 수출 의약품에 QR코드를 통한 시리얼라이제이션이 추가되어 이러한 세계적인 흐름에 더욱 박차를 가하고 있습니다. 브랜드 소유자는 ISO 12647 준수에 따라 공급업체를 사전 심사하기 때문에 인쇄기 공급업체는 고객의 감사를 통과하기 위해 매 판매 시마다 분광광도계와 폐쇄 루프 교정을 세트로 판매합니다. 또한, 디지털 인쇄기는 식품을 잘못 표시한 경우 EU 규제 당국이 전 세계 매출액의 최대 4%까지 부과할 수 있는 벌금을 피할 수 있도록 도와줍니다. 이러한 위험으로 인해 아날로그 방식의 전환 실수는 더 이상 용납할 수 없는 상황이 되었습니다. 향후 규제 변화에 대비하기 위해 제약 패키지 제조업체들은 현재 수성 잉크와 UV 경화형 잉크 모두에 대응할 수 있는 인쇄기를 지정하여 PFAS 규제가 강화될 경우 저전이성 배합에 대응할 수 있는 여지를 확보하고 있습니다. 그 결과, 디지털 직렬화는 단순한 규제 요건이 아닌 이사회 차원의 설비투자(CAPEX)를 결정하는 요인이 되고 있습니다.

주문형 도서 및 패키지 인쇄가 설비 투자를 주도하고 있습니다.

2024년 이후, 단납기 생산의 경제성은 완전히 바뀌었습니다. 토너와 잉크젯 기술이 제판 비용과 준비 과정의 낭비를 제거한 결과, 상업용 인쇄 업체의 62%가 500부 미만의 주문을 수락하여 2020년의 41%에서 크게 증가했습니다. 이커머스 허브는 현재 골판지 상자를 현지에서 인쇄하여 재고 비용을 절감하고 계절별 프로모션을 당일에 진행할 수 있도록 하고 있습니다. Cimpress는 생산의 현지화와 주문에서 출하까지의 주기를 72시간에서 24시간으로 단축하기 위해 HP Indigo 장비에 1억 달러 이상을 투자했습니다. Springer Nature와 같은 출판사는 백리스트 타이틀의 78%를 주문형 인쇄로 전환하여 판매되지 않은 재고를 파쇄할 필요성을 없앴습니다. 오프셋 인쇄기 업체들은 아날로그 방식의 속도가 여전히 중요한 1,000-10,000부 규모의 물량을 확보하기 위해 롤지 인쇄 라인에 잉크젯 바를 추가하는 경쟁을 벌이고 있습니다. 이러한 하이브리드형 프로토타입의 신뢰성이 입증됨에 따라 금융기관들은 서비스 및 소모품이 포함된 기종별 리스 플랜을 제공하기 시작했으며, 중견 인쇄업체들의 도입 장벽이 낮아지고 있습니다.

그래픽 용지 가격 변동으로 수익률 압박

2025년 초 북유럽과 브라질의 펄프 가격 급등으로 코팅지 가격이 18% 상승하여 인쇄업체들의 EBITDA를 압박하고 인쇄기 갱신을 지연시키고 있습니다. EU의 순환 경제 규칙은 재생 섬유의 사용을 장려하고 있지만, 종이의 품질이 다양하기 때문에 작업자는 인쇄기를 자주 재조정해야 하며, 이로 인해 가동 중단 시간과 잉크 부착량이 증가합니다. 8-12% 정도의 낮은 이윤으로 운영되는 컨버터 업체들은 이러한 가격 상승분을 다년 계약 고객에게 전가하는 데 어려움을 겪고 있으며, 이로 인해 신규 라인에 대한 설비투자(CAPEX)의 우선순위를 낮출 수밖에 없는 상황입니다. 일부 오프셋 인쇄업체들은 선물 계약을 통해 펄프 가격의 위험을 헤지하고 있지만, 2025년에는 헤지 수수료가 22% 상승하여 그 혜택이 상쇄되었습니다. 디지털 장비 업체들은 폐기물 감소를 내세우지만, 고커버리지 잉크젯 인쇄는 고가의 잉크와 드럼을 대량으로 소비하기 때문에 비용 절감 효과는 미미합니다. 그 결과, 투자 트렌드가 양극화되고 있습니다. 대형 그룹은 다년 계약으로 용지 조달을 확보하고 고속 잉크젯을 도입하는 반면, 소규모 인쇄업체는 설비 갱신을 미루고 현물 시장의 변동에 몸을 맡기는 경향이 있습니다.

부문 분석

2025년 디지털 인쇄기는 인쇄 장비 시장의 41.32%를 차지하며 연평균 4.02% 성장했습니다. 잉크젯 및 토너 제품 라인은 판값 없이 가변 그래픽을 필요로 하는 컨버터가 선호하고 있으며, 그 가치는 느린 기본 속도를 상쇄하고 있습니다. 출판사가 주문형 인쇄로 전환함에 따라 디지털 인쇄기 시장 규모는 크게 확대될 것으로 예측됩니다. 오프셋은 장판 인쇄를 유지하고 있지만, 그 점유율은 해마다 줄어들고 있습니다. 플 렉소 인쇄기는 여전히 불투명도가 높은 플렉서블 필름에 필수적이며, 그라비아 인쇄는 초장축 장식 인쇄를 담당하고 있습니다. 스크린 인쇄기는 섬유 및 전자장비용 틈새 시장에 머물러 있습니다. 컨버터는 플 렉소 웹에 잉크젯 바를 장착하는 하이브리드 장비를 점점 더 많이 선택하고 있으며, 인쇄 부수와 개인화의 균형을 맞추고 있습니다.

캐논과 하이델베르크는 2024년 B2 사이즈의 전자 사진 엔진으로 제휴하여 하이브리드형 중형 양산 모델의 기반을 구축하는 것을 목표로 하고 있습니다. 리코의 생산용 잉크젯 로드맵은 판을 없애고 싶어하는 라벨 컨버터를 타겟으로 하고 있습니다. 수성 잉크젯의 발전으로 비코팅 용지에 대한 접착력은 향상되었지만, 내마모성에 대해서는 여전히 용제계 시스템에 미치지 못하는 상황입니다.

2025년 전체 생산량에서 인쇄기 하드웨어가 차지하는 비중은 37.32%였으나, 공장의 다이 커팅, 폴딩, 검사 자동화가 진행되면서 포스트 프레스 장비는 CAGR 3.84%로 가장 빠르게 성장하는 부문으로 나타났습니다. 인력 부족으로 인해 로봇에 의한 블랭크 분리 및 비전 검사가 더욱 매력적이 되면서 마무리 라인 인쇄 장비 시장 점유율이 확대되고 있습니다. 하이델베르크의 'Cartonmaster'는 이러한 공정을 통합하여 턴키 셀이 어떻게 바닥 면적과 사이클 시간을 단축할 수 있는지를 보여줍니다. 프리프레스 시스템은 클라우드 워크플로우 아래에서 상품화가 진행되고 있지만, 컬러 관리에는 여전히 필수적인 요소입니다. 슬리터, 라미네이터 등의 주변장비는 컨버터가 한 교대마다 여러 기판을 취급하는 연포장 분야에서 수요를 뒷받침하고 있습니다.

Bobst는 2024년, 다이 커터 '마스터컷'의 주문이 28% 증가했습니다. 이는 다운타임을 줄이고자 하는 절실한 요구를 반영하고 있습니다. 시트지 인쇄기는 그 포맷의 유연성 덕분에 여전히 상업 인쇄를 지배하고 있지만, 롤지 인쇄 라인은 잡지 용량의 감소에 따라 축소되고 있습니다. 형식별로 보면, B1과 B2 클래스는 중간 로트 인쇄를 보장하고, B3는 퀵 프린터에 대응합니다. 독자적인 주변장비 번들은 전환 비용을 높이고, EU와 미국에서 반독점법 심사를 받고 있습니다.

지역별 분석

아시아태평양은 2025년 세계 시장의 41.43%를 차지했으며, 2031년까지 연평균 4.12% 성장할 것으로 전망됩니다. 중국에서는 80억 위안(11억 달러)의 보조금으로 중소도시의 디지털 인쇄기 도입이 진행되어 물류 거리 단축이 이루어지고 있습니다. 인도의 의약품 수출업체들은 EU의 시리얼라이제이션 규제에 대응하기 위해 생산라인을 개조하고 있어 잉크젯 수요가 증가하고 있습니다. 일본 대기업들은 단납기 패키징을 위해 하이브리드 인쇄기를 채택하고 있지만, 호주에서는 신규 설비에 대한 수입 관세가 걸림돌이 되고 있습니다. 국내에서는 반도체 패키징용 스크린 시스템이 성장하고 있습니다.

유럽과 북미를 합치면 2025년 전체 물량의 약 45%를 차지할 것으로 예상되지만, 성장은 완만합니다. EU의 추적성 규제로 인해 컨버터는 디지털 직렬화를 지향하고 있지만, 소규모 사업자에게는 부담이 되고 있습니다. 독일에서는 2024년 총 설치 대수가 4% 감소한 반면, 기업들이 폐기물 감축을 추진하면서 디지털 장비 주문은 12% 증가했습니다. 미국에서는 양극화가 진행되고 있습니다. 대형 패키징 기업들은 고속 잉크젯에 막대한 자금을 투자하는 반면, 많은 상업용 인쇄업체들은 기존의 오프셋 설비를 유지하는데 어려움을 겪고 있습니다. 캐나다에서는 중견 인쇄업체들의 파산과 합병이 진행되면서 업계의 구조조정이 진행되고 있습니다.

기타 지역은 남미, 중동 및 아프리카가 차지하고 있습니다. 브라질은 식품 포장을 위해 플 렉소 인쇄에 투자하고 있지만, 수입 비용의 변동으로 어려움을 겪고 있습니다. 사우디는 '비전 2030'에 따라 인쇄기에 대한 우대 대출을 통해 국내 인쇄 산업을 지원하고 있습니다. 아랍에미리트는 걸프 지역과 아프리카를 위한 프리존 인쇄 허브를 추진하고 있습니다. 남아공은 에너지 비용으로 어려움을 겪고 있지만, 의약품 카톤용 잉크젯 인쇄기를 선별적으로 도입하고 있으며, 케냐는 지역 소비자 수요를 충족시키기 위해 포장 라인을 확장하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.02The Print Equipment Market size is projected to expand from USD 19.98 billion in 2025 and USD 20.67 billion in 2026 to USD 24.22 billion by 2031, registering a CAGR of 3.22% between 2026 to 2031.

Demand is shifting from offset-dominated lines toward digital and hybrid presses as converters chase fast changeovers, minimal makeready, and variable-data features. Food and pharmaceutical labeling rules in the European Union and the United States are pulling capital toward presses that support serialization and allergen declarations. E-commerce fulfillment centers are buying narrow-web digital equipment to print shipping boxes on the day of dispatch, while brand owners widen SKU counts to serve micro-segments. Competitive pressure from software-centric entrants is forcing incumbent press makers to add cloud-connected workflow platforms and subscription plans, a pivot that raises refinancing needs but promises sticky service revenue.

Global Print Equipment Market Trends and Insights

Regulatory Tailwinds For Food And Pharma Digital Labels

EU and U.S. labeling mandates now require digital watermarks, variable allergen labeling, and batch-level traceability, pushing converters toward inkjet retrofits and greenfield digital press purchases. India added QR serialization for export drugs in April 2025, reinforcing this global convergence. Brand owners are prequalifying suppliers based on ISO 12647 compliance, so press vendors bundle spectrophotometers and closed-loop calibration with every sale to pass customer audits. Digital presses also help converters avoid penalties that EU regulators can levy at up to 4% of global turnover for mislabeled food products, a risk that makes analog changeover errors untenable. To hedge against future rule changes, pharmaceutical packagers now specify presses that accept both water-based and UV-curable inks, ensuring headroom for low-migration formulations once PFAS restrictions tighten. The net effect is that digital serialization has become a board-level CAPEX trigger rather than a mere regulatory checkbox.

On-Demand Book And Packaging Runs Driving CAPEX

Short-run economics flipped after 2024, when 62% of commercial printers accepted jobs below 500 units, up from 41% in 2020, thanks to toner and inkjet lines that erase plate cost and makeready waste. E-commerce hubs now print corrugated boxes on-site, reducing inventory costs and enabling same-day seasonal promotions. Cimpress committed more than USD 100 million for HP Indigo units to localize production and cut order-to-ship cycles from 72 to 24 hours. Publishers such as Springer Nature moved 78% of backlist titles to print-on-demand, eliminating the need to pulp unsold stock. Offset press makers are racing to bolt inkjet bars onto web lines so they can chase jobs that fall in the 1,000-10,000 range, where analog speed still matters. As these hybrid prototypes prove reliable, lenders are starting to offer structure-specific leasing packages that bundle service and consumables, lowering the hurdle rate for mid-size shops.

Volatile Graphic-Paper Prices Squeeze Margins

Nordic and Brazilian pulp spikes in early 2025 lifted coated-sheet prices 18%, squeezing printer EBITDA and delaying press upgrades. EU circular-economy rules encourage recycled fiber, but variable sheet quality forces operators to recalibrate presses more often, increasing downtime and ink lay-down. Converters with thin 8-12% margins struggle to pass these hikes through multi-year customer contracts, so CAPEX for new lines slips down the priority list. Some offset printers hedge pulp risk with futures contracts, yet hedging fees rose 22% in 2025, eroding the benefit. Digital vendors pitch reduced waste, but high-coverage inkjet jobs consume expensive ink and drums, muting savings. As a result, investment bifurcates: large groups lock multi-year paper deals and adopt high-speed inkjet, while small shops defer upgrades and ride spot-market volatility.

Other drivers and restraints analyzed in the detailed report include:

- Brand-Owner Push For SKU Proliferation

- Hybrid Press Adoption Cuts Total Cost Of Ownership

- Skilled Press-Operator Shortage

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Digital captured 41.32% of the print equipment market in 2025 and rose at 4.02% annually. Inkjet and toner lines appeal to converters who need variable graphics without plate costs, a value that offsets slower raw speed. The print equipment market size for digital presses is forecast to expand significantly as publishers pivot to print-on-demand. Offset retains long runs, yet its slice narrows each year. Flexographic units stay vital for high-opacity flexible films, while gravure holds ultra-long decorative work. Screen equipment remains a niche for textiles and electronics. Converters increasingly choose hybrid rigs that bolt inkjet bars onto flexo webs, balancing run length and personalization.

Canon and Heidelberg joined forces in 2024 on a B2 electrophotographic engine, aiming to anchor hybrid mid-volume models. Ricoh's production inkjet roadmap targets label converters craving plate elimination. Advances in aqueous inkjet have improved adhesion on uncoated stock, yet rub resistance still trails solvent systems.

Press hardware held 37.32% of 2025 tonnage, but post-press equipment is the fastest-growing segment, with a 3.84% CAGR, as plants automate die-cutting, folding, and inspection. The print equipment market share for finishing lines is growing as labor shortages make robotic blank separation and vision QC more attractive. Heidelberg's Cartonmaster integrates these steps, showing how turnkey cells compress floor space and cycle time. Pre-press systems commoditize under cloud workflows, yet remain essential for color control. Ancillary gear, such as slitters and laminators, sustains demand in flexible packaging, where converters juggle multiple substrates each shift.

Bobst logged a 28% order rise for Mastercut die-cutters in 2024, reflecting the urgency to cut downtime. Sheet-fed presses still dominate commercial work thanks to their format agility, whereas roll-fed lines shrink as magazine volume declines. Format-wise, B1 and B2 classes secure mid-runs, while B3 serves quick printers. Proprietary ancillary bundles raise switching costs and draw antitrust scrutiny in the EU and the United States.

The Print Equipment Market Report is Segmented by Technology (Web-Offset Lithographic, Flexographic, Gravure, Screen Printing, and Digital), Equipment Type (Pre-Press Systems, Press, and More), Application (Books and Publishing, Advertising and Signage, and More), End-User Industry (Packaging Converters, Commercial Printers, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific accounted for 41.43% of global volume in 2025 and is projected to grow at 4.12% through 2031. China's CNY 8 billion (USD 1.1 billion) subsidy funds digital press rollouts in smaller cities, shrinking logistics miles. India's drug exporters are retrofitting lines for EU serialization, boosting inkjet demand. Japan's majors embrace hybrid presses for short-run packaging, while Australia faces import-duty drag on new equipment. South Korea grows in screen systems for semiconductor packaging.

Europe and North America together account for about 45% of the 2025 tons, but growth is slow. EU traceability rules push converters toward digital serialization, straining small operators. Germany saw 4% fewer overall installs in 2024, yet digital orders rose 12% as firms pursued waste-cutting initiatives. The United States splits: large packaging houses pour money into high-speed inkjet, while many commercial shops sweat legacy offset assets. Canada consolidates as mid-sized printers fold or merge.

South America, the Middle East, and Africa hold the rest. Brazil invests in flexo for food packaging but fights import-cost volatility. Saudi Arabia backs local printing under Vision 2030 with soft loans for presses. The United Arab Emirates markets free-zone print hubs to serve Gulf and Africa. South Africa grapples with energy costs but sees selective inkjet buys for pharma cartons, while Kenya scales packaging lines for regional consumer demand.

- Heidelberger Druckmaschinen AG

- Koenig and Bauer AG

- Bobst Group SA

- HP Inc.

- Canon Inc.

- Seiko Epson Corporation

- Fujifilm Holdings Corporation

- Ricoh Company Ltd.

- Electronics for Imaging, Inc.

- Durst Phototechnik AG

- Mark Andy Inc.

- Nilpeter A/S

- Gallus Ferd. Ruesch AG (Heidelberg)

- OMET S.r.l.

- MPS Systems B.V.

- Uteco Converting SpA

- Manroland Goss Web Systems GmbH

- Agfa-Gevaert Group NV

- Brother Industries Ltd.

- AB Graphic International Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Market Drivers

- 4.3.1 Regulatory Tailwinds for Food and Pharma Digital Labels

- 4.3.2 On-Demand Book and Packaging Runs Driving CAPEX

- 4.3.3 Brand-Owner Push for SKU Proliferation

- 4.3.4 Hybrid Press Adoption Cuts Total Cost of Ownership

- 4.3.5 AI-Based Predictive Maintenance Reduces Press Downtime

- 4.3.6 Rise of Decentralised Micro-Factories Near End Users

- 4.4 Market Restraints

- 4.4.1 Volatile Graphic-Paper Prices Squeeze Margins

- 4.4.2 Skilled Press-Operator Shortage

- 4.4.3 Escalating Cyber-Security Risks in Cloud-Connected Presses

- 4.4.4 PFAS Regulations Limiting Certain Ink Chemistries

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 Web-offset Lithographic

- 5.1.2 Flexographic

- 5.1.3 Gravure

- 5.1.4 Screen Printing

- 5.1.5 Digital

- 5.2 By Equipment Type

- 5.2.1 Pre-press Systems

- 5.2.2 Press(Sheet-fed, Roll-fed)

- 5.2.3 Post-press and Finishing

- 5.2.4 Ancillary and Inline Converting

- 5.3 By Application

- 5.3.1 Books and Publishing

- 5.3.2 Advertising and Signage

- 5.3.3 Security and Transactional

- 5.3.4 Packaging

- 5.3.5 Other Applications

- 5.4 By End-User Industry

- 5.4.1 Packaging Converters

- 5.4.2 Commercial Printers

- 5.4.3 In-plant/Corporate

- 5.4.4 Quick Print and Copy Shops

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Kenya

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Heidelberger Druckmaschinen AG

- 6.4.2 Koenig and Bauer AG

- 6.4.3 Bobst Group SA

- 6.4.4 HP Inc.

- 6.4.5 Canon Inc.

- 6.4.6 Seiko Epson Corporation

- 6.4.7 Fujifilm Holdings Corporation

- 6.4.8 Ricoh Company Ltd.

- 6.4.9 Electronics for Imaging, Inc.

- 6.4.10 Durst Phototechnik AG

- 6.4.11 Mark Andy Inc.

- 6.4.12 Nilpeter A/S

- 6.4.13 Gallus Ferd. Ruesch AG (Heidelberg)

- 6.4.14 OMET S.r.l.

- 6.4.15 MPS Systems B.V.

- 6.4.16 Uteco Converting SpA

- 6.4.17 Manroland Goss Web Systems GmbH

- 6.4.18 Agfa-Gevaert Group NV

- 6.4.19 Brother Industries Ltd.

- 6.4.20 AB Graphic International Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment