|

시장보고서

상품코드

2044211

프린트, 부착 라벨링 및 라벨링 기기 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Print And Apply Labeling And Labeling Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

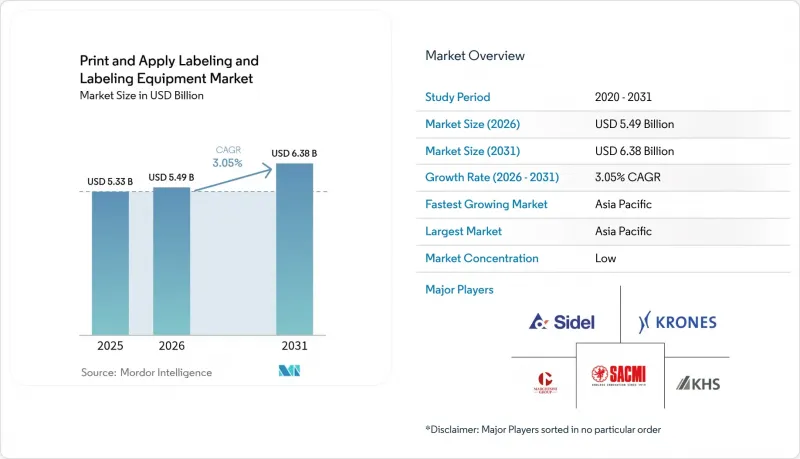

프린트, 부착 라벨링 및 라벨링 기기 시장 규모는 2025년에 53억 3,000만 달러, 2026년에 54억 9,000만 달러가 되어, 2031년까지 63억 8,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 복합 성장률(CAGR) 3.05%를 나타낼 것으로 예측됩니다.

수요는 주문형 가변 데이터 인쇄를 선호하는 고속 식음료 포장, 의약품 직렬화 프로그램 및 전자상거래 주문 처리 워크플로우에 의해 뒷받침되고 있습니다. 엣지 AI를 통한 결함 감지 기능으로 전환 시간을 단축하는 한편, 디지털 잉크젯 모듈은 '로트 사이즈 1'의 경제성을 실현하여 브랜드 소유자가 몇 주 분량의 사전 인쇄된 재고를 보유하지 않고도 단기간의 프로모션 캠페인을 진행할 수 있도록 지원합니다. 아시아태평양은 중국의 소포 처리량과 인도의 RFID 투자가 공장 현장 자동화 예산으로 이어지면서 양적 성장의 원동력이 되고 있습니다. 한편, 북미와 유럽에서는 통합형 비전 검사 기능을 갖춘 전자동 시스템을 평가하는 지속가능성 및 추적성 관련 규제에 대한 대응이 계속 강조되고 있습니다. 경쟁 기업 간의 적대적 관계는 완만한 상황입니다. 세계 OEM 5사가 여전히 세계 설치 용량의 거의 절반을 점유하고 있지만, 가격 경쟁력을 갖춘 중국 통합업체들이 모듈형 셀을 확장하고 있고, 유럽과 미국 제조업체의 정가보다 최대 40% 낮은 가격을 책정하고 있기 때문에 기존 제조업체들은 수익률을 지키기 위해 IoT 지원 서비스 계약에 의존할 수밖에 없는 상황입니다.

세계 프린트, 부착 라벨 및 라벨링 장비 시장 동향과 인사이트

디지털 인쇄 및 전자동 부착기의 진화

디지털 잉크젯 및 UV-LED 모듈은 현재 속도면에서 플 렉소 인쇄에 필적할 뿐만 아니라 플레이트가 필요하지 않아 음료 OEM 제조업체가 라벨 재고를 12주에서 3일로 단축하여 운전 자본을 절약할 수 있도록 돕고 있습니다. 2025년 11월에 출시된 도미노의 레이저 코더 'Dx1060i'는 골판지 및 냉동 수산물 상자에 분당 200m 속도로 인쇄하면서 에너지 소비를 40% 절감할 수 있습니다. 코니카미놀타의 'AccurioLabel 400'은 인라인 분광광도계 기능을 탑재하여 수백 개의 SKU를 취급하는 브랜드에서도 Delta-E 0.5 이내로 색상 편차를 억제합니다. 비전 시스템을 탑재한 서보 제어식 어플리케이터는 골판지의 위치 오차를 보정하여 불량률을 0.05% 미만으로 낮춥니다. 이 수치는 2026년 1월 Erdinger Weissbrau사가 AI 지원 인쇄 엔진을 도입했을 때 입증된 수치입니다. 고해상도 프린트 헤드와 클로즈드 루프 로봇 공학의 결합으로 프린트, 부착링 장비 시장은 무인 생산과 '로트 사이즈 1'의 개인화를 향해 나아가고 있습니다.

엄격한 추적성 및 직렬화 규정 준수

미국 의약품 공급망 보안법은 2024년 11월까지 단위 단위의 2차원 데이터 매트릭스 코딩을 의무화하고 있으며, 이에 따라 프린트 및 부착은 단순한 인쇄 후 부가기능이 아닌 컴플라이언스 대응 자산으로 전환되고 있습니다. 유럽에서는 위조 의약품 지침의 규정과 함께 변조 방지 씰이 도입됨에 따라 이미 수축 슬리브와 잉크젯 직렬화 모듈을 결합한 솔루션으로 조달이 전환되고 있습니다. ForgeStop이 2026년 1월에 출시할 예정인 NFC 지원 라벨은 일련번호와 온도 추적 기능을 통합하여 연간 350억 달러에 달하는 콜드체인 폐기 문제를 해결할 수 있습니다. 브라질과 사우디아라비아도 비슷한 규제를 도입하고 있어 신흥 지역 전체에서 대응 가능한 수요를 확대되고 있습니다. 이러한 요구사항은 시리얼라이제이션 지원 플랫폼이 높은 가격대임에도 불구하고 프린트, 부착 라벨 및 라벨링 장비 시장에서 기존 반자동 라인의 성장률을 능가하는 이유를 설명해줍니다.

고속 인쇄 및 적용 시스템의 설비투자(Cap-Ex) 강도

양면 코딩, 비전 검사, 데이터베이스 직렬화를 통합한 차세대 라인의 비용은 25만-50만 달러에 달하고, 중소기업의 투자 회수 기간을 허용 가능한 수준 이상으로 끌어올렸습니다. 2025년 북미 조사에 따르면, 계약 포장업체의 62%가 자동화를 미루고 대신 기존 설비로 교대 근무를 늘리는 방식으로 대응하고 있다고 합니다. 유럽에서는 리스 옵션이 등장하고 있지만, 남미와 아프리카에서는 이자율이 두 자릿수에 달하기 때문에 이용률이 낮은 임베디드니다. 2023년부터 2025년까지 프린트 헤드의 해상도가 두 배로 증가함에 따라 급속한 노후화로 인한 리스크가 더욱 커지고 있습니다. '서비스로서의 장비(EaaS)' 모델이 전 세계적으로 확산되지 않는 한, 높은 자본 집약도는 프린트, 부착 및 라벨링 장비 시장의 성장률을 계속 낮출 것입니다.

부문 분석

2025년 기준, 전자동 플랫폼은 프린트, 부착 라벨 및 라벨링 장비 시장에서 89.51%의 점유율을 차지해, 2031년까지 연평균 복합 성장률(CAGR) 4.51%로 확대될 것으로 예측됩니다. 이러한 시스템은 작업자의 개입을 폐쇄형 로봇으로 대체하여 단위당 인건비를 최대 70%까지 절감할 수 있습니다. Erdinger Weissbrau는 2026년 1월 리노베이션 후 AI 제어 인쇄 엔진으로 불량률이 0.05% 미만으로 떨어졌습니다. 반자동 장비는 SKU 전환이 빈번한 공동 포장 현장에 여전히 적합하지만, 수동 스테이션은 장인적인 식품 생산 및 임상시험용 라벨 부착 현장에 남아있습니다.

IoT 연결에 대한 관심이 높아지면서 그 격차는 더욱 벌어지고 있습니다. SATO는 2025년 7월 태국에서의 사업 확장에 있어 다수의 센서를 탑재하고 클라우드에서 모니터링되는 전용 라인을 추가했습니다. 이 라인은 다운타임이 발생하기 전에 프린트 헤드의 마모를 감지합니다. 반자동 장치에는 현재 터치스크린 방식의 설정 마법사가 탑재되어 있어 기술자가 부족한 상황에서도 쉽게 교육을 받을 수 있습니다. 미화 3만 달러 미만의 모듈식 저비용 "인쇄 및 적용" 셀이 인쇄 및 적용 라벨 및 라벨링 장비 시장에 진입함에 따라 수동 도구는 꾸준히 감소하고 있습니다. 이를 통해 소규모 양조장이나 틈새 화장품 브랜드에서도 자동화에 대한 접근이 확대되고 있습니다.

지역별 분석

아시아태평양은 2025년 매출의 37.89%를 차지하며, 2024년 중국의 소포 처리량 1,750억 개와 인도의 RFID 용량 확대에 힘입어 CAGR 4.92%를 나타낼 것으로 예측됩니다. 에이버리데니슨의 푸네 인레이 공장(투자금액 3,000만 달러)은 2025년 4월부터 가동에 들어가 연간 50억 개의 태그를 생산할 수 있어 급증하는 옴니채널 소매 수요를 충족시킬 수 있습니다. 오므론의 방갈로르 자동화 센터는 도입의 병목현상이 될 수 있는 기술자 부족 문제를 더욱 해소할 수 있습니다.

북미와 유럽의 성장률은 세계 평균인 3.05%에 근접한 수준이지만, 직렬화 및 지속가능성 관련 법규를 준수하고 수익성이 높은 전자동 시스템에 중점을 두고 있습니다. 유럽연합 집행위원회의 '포장 및 포장 폐기물 규제'는 2030년까지 포장재를 15% 감축하는 목표를 설정하고 있으며, 이로 인해 라이너리스 기술과 디지털 인쇄에 대한 관심이 높아지고 있습니다. 미국에서는 FDA의 추적성 규제로 인해 2027년까지 식품 생산 라인의 40%가 업그레이드가 필요하기 때문에 기존 설비의 개보수 수요가 증가하고 있습니다.

남미에서는 브라질이 2027년까지 의약품 직렬화를 단계적으로 도입하고, 자동화 분야에 대한 외국인 직접투자가 유입되면서 시장이 활기를 띠고 있습니다. 2025년 4월에 발표된 Dyfuku의 텔랑가나 주에 2,400만 달러 규모의 시설은 이 지역의 물류 허브에 대한 관심을 입증하는 것입니다. 중동 및 아프리카는 여전히 개발 중인 지역이지만, 사우디아라비아의 2024년 일련화 규정과 아랍에미리트의 항공화물용 RFID 프로젝트는 향후 5년간 프린트, 부착 라벨 및 라벨링 장비 시장의 성장을 예고하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.02The print and apply labeling and labeling equipment market size is projected to be USD 5.33 billion in 2025, USD 5.49 billion in 2026, and reach USD 6.38 billion by 2031, growing at a CAGR of 3.05% from 2026 to 2031.

Demand is anchored in high-speed food and beverage packaging, pharmaceutical serialization programs, and e-commerce fulfillment workflows that favor on-demand variable data printing. Edge-AI defect detection is shortening changeover windows while digital inkjet modules deliver lot-size-of-one economics, encouraging brand owners to run short promotional campaigns without holding weeks of pre-printed inventory. Asia-Pacific remains the volume growth engine as China's parcel throughput and India's RFID investments translate into factory-floor automation budgets, whereas North America and Europe continue to target sustainability and traceability mandates that reward fully automatic systems with integrated vision inspection. Competitive rivalry is moderate: five global OEMs still control nearly half of installed capacity, yet price-aggressive Chinese integrators are scaling modular cells that undercut Western list prices by up to 40%, forcing incumbents to lean on IoT-enabled service contracts for margin defense.

Global Print And Apply Labeling And Labeling Equipment Market Trends and Insights

Evolution Of Digital Printing And Fully Automatic Applicators

Digital inkjet and UV-LED modules now rival flexography on speed while eliminating plates, enabling beverage co-packers to slash label inventory from twelve weeks to three days and unlock working-capital savings. Domino's Dx1060i laser coder, released in November 2025, prints 200 meters per minute on corrugated and frozen seafood cartons while cutting energy use by 40%. Konica Minolta's AccurioLabel 400 adds inline spectrophotometry, keeping color drift within 0.5 Delta-E for brands juggling hundreds of SKUs. Servo-guided applicators equipped with vision systems compensate for carton misalignment and drive defect rates below 0.05%, a metric validated by Erdinger Weissbrau's January 2026 installation of AI-enabled print engines. Together, high-resolution printheads and closed-loop robotics move the print and apply labeling and labeling equipment market toward lights-out production and lot-size-of-one personalization.

Stringent Trace And Trace And Serialization Mandates

The U.S. Drug Supply Chain Security Act requires unit-level 2D DataMatrix coding by November 2024, converting print-and-apply stations into compliance assets rather than post-printing niceties. In Europe, Falsified Medicines Directive rules plus tamper-evident seals have already shifted procurement toward combination shrink-sleeve and inkjet serialization modules. ForgeStop's January 2026 NFC-enabled label merges serialization with temperature tracking to combat USD 35 billion of annual cold-chain spoilage. Brazil and Saudi Arabia are phasing in parallel mandates that extend addressable demand across emerging regions. These requirements explain why serialization-ready platforms command premium pricing yet still outgrow legacy semi-automatic lines in the print and apply labeling and labeling equipment market.

Cap-Ex Intensity Of High-Speed Print-And-Apply Systems

Next-generation lines integrating dual-sided coding, vision inspection, and database serialization cost USD 250,000-500,000, pushing payback horizons beyond the comfort level of small and medium enterprises. North American surveys in 2025 showed 62% of contract packagers delaying automation, instead adding shifts to legacy gear. Leasing options have emerged in Europe, yet double-digit interest rates in South America and Africa keep utilization low. Rapid obsolescence compounds the risk, as printhead resolution doubled between 2023 and 2025. Unless equipment-as-a-service models proliferate globally, capital intensity will continue to shave growth points from the print and apply labeling and labeling equipment market.

Other drivers and restraints analyzed in the detailed report include:

- Automation Demand In Food And Beverage High-Speed Packaging Lines

- E-Commerce Cold-Chain Dual-Temperature Label Needs

- Shortage Of Integration And Maintenance Technicians

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fully automatic platforms captured 89.51% share of the print and apply labeling and labeling equipment market in 2025 and are projected to advance at a 4.51% CAGR to 2031. These systems replace operator intervention with closed-loop robotics, trimming labor cost per unit by up to 70%. At Erdinger Weissbrau, AI-guided print engines pushed defect rates below 0.05% after a January 2026 retrofit. Semi-automatic equipment still fits co-packing sites handling frequent SKU swaps, while manual stations linger in artisanal food production and clinical trial labeling.

Interest in IoT connectivity widens the gulf. SATO's July 2025 Thailand expansion added a line dedicated to sensor-rich, cloud-monitored machines that flag printhead wear before downtime occurs. Semi-automatic units now ship with touchscreen setup wizards, making training accessible during the technician shortage. Manual tools decline steadily as modular low-cost print-and-apply cells often below USD 30,000 enter the print and apply labeling and labeling equipment market, broadening automation access for micro-breweries and niche cosmetic brands.

The Print and Apply Labeling and Labeling Equipment Market Report is Segmented by Technology (Fully Automatic, Semi-Automatic, and Manual), Label Type (Pressure-Sensitive, Shrink-Sleeve, Glue-Based, In-Mold, Linerless, and Smart-Label RFID and QR), End-User Vertical (Food and Beverage, Pharmaceutical, Personal Care and Household, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 37.89% of 2025 revenue and is expected to expand at a 4.92% CAGR, underpinned by China's 175 billion parcel throughput in 2024 and India's RFID capacity build-outs. Avery Dennison's USD 30 million Pune inlay plant, inaugurated in April 2025, can output 5 billion tags per year to satisfy surging omnichannel retail demand. OMRON's Bengaluru Automation Center further addresses technician shortages that might otherwise bottleneck adoption.

North America and Europe grow near the global average of 3.05% yet focus on higher-margin fully automatic systems that comply with serialization and sustainability statutes. The European Commission's Packaging and Packaging Waste Regulation sets a 15% packaging-reduction target by 2030, boosting linerless and digital print interest. In the United States, FDA traceability rules mean 40% of food lines require upgrades by 2027, feeding retrofit demand.

South America gains traction as Brazil phases pharmaceutical serialization in by 2027 and as foreign direct investment pours into automation. Daifuku's USD 24 million Telangana facility, announced April 2025, underscores interest in the region's logistics hubs. The Middle East and Africa remain nascent, yet Saudi Arabia's 2024 serialization rules and United Arab Emirates air-cargo RFID projects foreshadow a lift in the print and apply labeling and labeling equipment market over the next five years.

- Avery Dennison Corporation

- Axon LLC

- BW Packaging (Barry-Wehmiller Group, Inc)

- Domino Printing Sciences PLC

- Videojet Technologies

- Fuji Seal International, Inc.

- Heuft Systemtechnik GmbH

- HERMA GmbH

- ID Technology, LLC

- KHS GmbH

- Krones AG

- Shenzhen Shuangcheng Automation Co., Ltd

- Marchesini Group S.p.A.

- MARKEM-IMAJE (DOVER CORPORATION)

- Novexx Solutions GmbH

- PDC International Corp.

- Quadrel Labeling Systems

- FoxJet

- SATO Holdings Corporation

- SIDEL (Tetra Laval)

- Weber Marking Systems GmbH

- ProMach

- Wuxi Sici Auto Co, Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Evolution of Digital Printing and Fully-Automatic Applicators

- 4.2.2 Stringent Trace-and-Trace and Serialization Mandates

- 4.2.3 Automation Demand in Food and Beverage High-Speed Packaging Lines

- 4.2.4 E-Commerce Cold-Chain Dual-Temperature Label Needs

- 4.2.5 Sustainability Push Toward Liner-Less Label Formats

- 4.2.6 IoT-Edge Predictive Maintenance for Labeling Lines

- 4.3 Market Restraints

- 4.3.1 Cap-Ex Intensity of High-Speed Print-and-Apply Systems

- 4.3.2 Durability Issues in Extreme Humidity / Freezer Tunnels

- 4.3.3 Shortage of Integration and Maintenance Technicians

- 4.3.4 RFID Inlay Supply Volatility Inflating Raw-Material Cost

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 Fully Automatic

- 5.1.2 Semi-Automatic

- 5.1.3 Manual

- 5.2 By Label Type

- 5.2.1 Pressure-Sensitive / Self-Adhesive

- 5.2.2 Shrink-Sleeve

- 5.2.3 Glue-Based

- 5.2.4 In-Mold

- 5.2.5 Liner less Label Applicators

- 5.2.6 Smart-Label (RFID / QR) Systems

- 5.3 By End-User Vertical

- 5.3.1 Food and Beverage

- 5.3.2 Pharmaceutical

- 5.3.3 Personal Care and Household

- 5.3.4 Industrial and Logistics

- 5.3.5 Others End-User Verticals

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Chile

- 5.4.2.4 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South Korea

- 5.4.4.5 Australia

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 Saudi Arabia

- 5.4.5.1.2 United Arab Emirates

- 5.4.5.1.3 Turkey

- 5.4.5.1.4 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Nigeria

- 5.4.5.2.3 Rest of Africa

- 5.4.5.1 Middle East

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 Avery Dennison Corporation

- 6.4.2 Axon LLC

- 6.4.3 BW Packaging (Barry-Wehmiller Group, Inc)

- 6.4.4 Domino Printing Sciences PLC

- 6.4.5 Videojet Technologies

- 6.4.6 Fuji Seal International, Inc.

- 6.4.7 Heuft Systemtechnik GmbH

- 6.4.8 HERMA GmbH

- 6.4.9 ID Technology, LLC

- 6.4.10 KHS GmbH

- 6.4.11 Krones AG

- 6.4.12 Shenzhen Shuangcheng Automation Co., Ltd

- 6.4.13 Marchesini Group S.p.A.

- 6.4.14 MARKEM-IMAJE (DOVER CORPORATION)

- 6.4.15 Novexx Solutions GmbH

- 6.4.16 PDC International Corp.

- 6.4.17 Quadrel Labeling Systems

- 6.4.18 FoxJet

- 6.4.19 SATO Holdings Corporation

- 6.4.20 SIDEL (Tetra Laval)

- 6.4.21 Weber Marking Systems GmbH

- 6.4.22 ProMach

- 6.4.23 Wuxi Sici Auto Co, Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment