|

시장보고서

상품코드

2061516

인도의 상처 관리 기기 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)India Wound Care Management Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

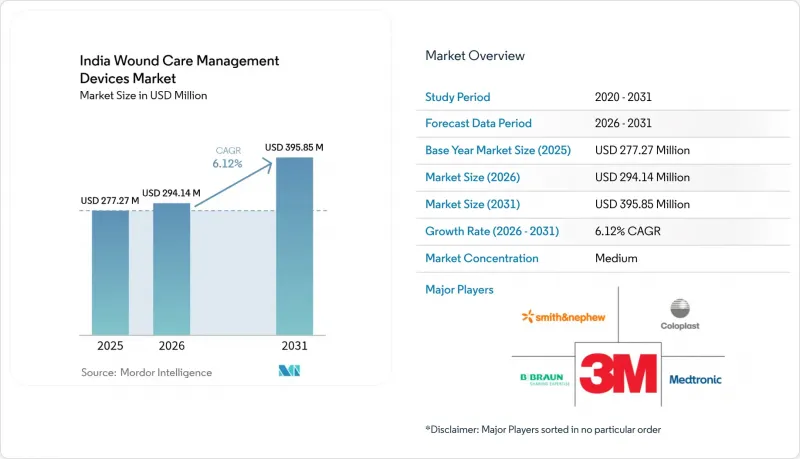

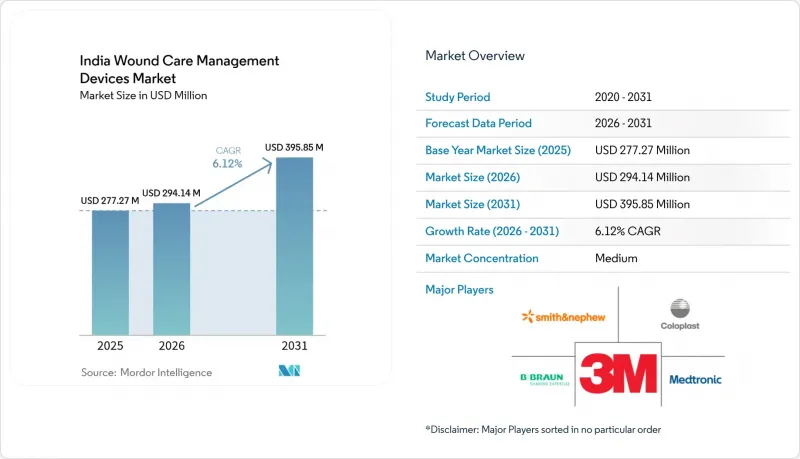

인도의 상처 관리 기기 시장 규모는 2025년에 2억 7,727만 달러로 평가되었고, 2026년에 2억 9,414만 달러로 추정되고, 2031년까지 3억 9,585만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 6.12%로 성장할 전망입니다.

본 보고서는 제품별(드레싱, 붕대, 상처 봉합 장치 등), 상처 유형별(만성 상처 및 급성 상처), 최종 사용자별(병원 및 클리닉, 외래수술센터(ASC), 재택치료, 기타)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

인도의 상처 관리 기기 시장 동향 및 인사이트

당뇨병과 관련된 당뇨병성 족부 궤양의 부담 증가

인도에는 1억 100만 명 이상의 당뇨병 환자와 1억 3,600만 명의 당뇨병 전단계 환자가 있으며, 이는 당뇨병성 족부 궤양의 유병률이 6.2%임을 의미합니다. 하지 절단 수술은 연간 10만 건을 넘어, 고성능 드레싱 재료, 하중 분산 장치 및 음압상처치료(NPWT)에 대한 지속적인 수요를 창출하고 있습니다. Bohler나 Mandakini 등의 설계를 바탕으로 한 현지산 하중 분산 대체품은 전접촉 석고(total-contact casting)와 동등한 치료 효과를 보이고 있으나, 여전히 소수의 3차 의료기관으로 한정되어 있습니다. 제조업체는 합리적인 가격과 효능의 균형을 맞추어야 하므로, 일회용 매트릭스보다 모듈식 키트가 더 선호됩니다.

인도 전역의 수술 건수 증가

2025년 수술 건수는 인구 10만 명당 1,385건으로, 인도는 여전히 WHO 기준을 밑돌고 있어 병원 확충의 여지가 남아 있습니다. 지역 의료시설의 수술 후 감염률이 9%인 반면, 인증 시설에서는 2-3%에 불과하기 때문에 상처 열개를 줄이기 위해 항균 드레싱이나 NPWT의 도입이 확대되고 있습니다. 2024년 3월 휴대용 캐니스터식 NPWT 및 헤모글로빈 스프레이 입찰은 공공 기관들이 첨단 상처 봉합 기술을 도입하기 위해 준비를 진행하고 있음을 보여줍니다. 코비디엔사의 봉합사 60% 할인과 같은 가격 인하 움직임은 가격에 민감한 환경에서 물량 주도 전략이 얼마나 효과적인지를 보여주고 있습니다.

1차 진료에서 고도의 상처 관리에 대한 인식 부족

1차 의료 센터에서는 여전히 거즈나 포비돈요드에 의존하고 있으며, 많은 임상의들이 NPWT나 하이드로콜로이드에 대한 교육을 받지 못하고 있습니다. 국가 보건 미션의 교육 과정에는 상처 관리 역량이 포함되어 있지 않아, 그 결과 환자를 전문 의료기관으로 의뢰하는 데 시간이 오래 걸리고 합병증이 증가하고 있습니다. 재고 부족이나 콜드체인의 미비로 인해, 대도시권 이외의 지역에서는 첨단 제품의 사용이 더욱 제한되고 있습니다. 지방에서는 더 큰 장벽에 직면해 있습니다. 공급망의 취약성으로 인해 첨단 드레싱 재료가 자주 품절되고 있으며, 신뢰할 수 있는 냉장 시설이 없는 시설에서는 생체 매트릭스에 대한 콜드체인 요건이 여전히 충족되지 않고 있습니다.

부문별 분석

2025년 매출에서 드레싱이 46.06%를 차지한 반면, 붕대는 거즈보다 점착성이 높은 형태를 선호하는 스포츠 의학 프로토콜 덕분에 연평균 성장률(CAGR) 9.22%의 성장 궤도에 올라 있습니다. 병원에서는 당뇨성 궤양용 드레싱이 표준화되어 판매량의 기반을 이루고 있으며, 붕대 제조업체들은 의료기관 입찰과 소매 약국을 통한 이중 유통 경로를 활용하고 있습니다. 인도의 상처 관리 기기 시장에서 드레싱은 계속해서 다른 카테고리를 앞지르는 성장세를 보이는 반면, 붕대는 '조기 활동 재개'라는 효과를 전면에 내세워 프리미엄 틈새 시장을 개척하고 있습니다. 검증 단계에 접어든 센서 탑재 드레싱은 이 카테고리를 일반 상품과 스마트 플랫폼 부문으로 분화시켜 가격대의 재편을 가져올 가능성이 있습니다.

봉합사가 주류를 이루는 상처 봉합 기기 분야는 에시콘(Ethicon)과 코비디엔(Covidien)이 주도하며, 병원 처방집에 포함된 고정 계약의 혜택을 누리고 있습니다. 음압상처치료(NPWT), 지혈제 및 생체 매트릭스는 비용 및 보험 급여와 관련된 불확실성으로 인해 시장 확대가 제한되고 있어, 여전히 틈새 시장으로 남아 있습니다. 아유슈만 바라트(Ayushman Bharat)의 적용 범위가 확대되면, 이러한 고수익 부문은 인도 상처 관리 기기 시장에서 뒤처진 부분을 만회할 수 있는 성장을 이룰 준비가 되어 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the india wound care management devices market size is projected to be USD 277.27 million in 2025, USD 294.14 million in 2026, and reach USD 395.85 million by 2031, growing at a CAGR of 6.12% from 2026 to 2031.

This report is Segmented by Product (Dressings, Bandages, Wound Closure Devices, and More), Wound Type (Chronic Wound and Acute Wound), and End-User (Hospitals & Clinics, Ambulatory Surgical Centers, Home Healthcare, and Others). The Market Forecasts are Provided in Terms of Value (USD).

India Wound Care Management Devices Market Trends and Insights

Rising Diabetes-Linked Diabetic Foot Ulcer Burden

India hosts more than 101 million people with diabetes and 136 million with pre-diabetes, translating into 6.2% diabetic foot ulcer prevalence. Lower-limb amputations exceed 100,000 annually, creating sustained demand for advanced dressings, offloading devices, and NPWT. Indigenous offloading alternatives, such as the Bohler and Mandakini designs, match total-contact casting outcomes yet remain confined to a few tertiary centers. Manufacturers must balance affordability with efficacy, which favors modular kits over single-use matrices.

Increasing Surgical Volumes Across India

At 1,385 surgeries per 100,000 population in 2025, India still trails the WHO benchmark, leaving headroom for hospital expansion. Surgical-site infection rates of 9% in community facilities versus 2-3% in accredited centers are driving adoption of antimicrobial dressings and NPWT to reduce dehiscence. March 2024 tenders for portable canistered NPWT and hemoglobin spray show public institutions are gearing up for advanced wound closure. Price-cutting moves such as Covidien's 60% suture discount illustrate how volume-led strategies work in price-sensitive settings.

Limited Awareness of Advanced Wound Care in Primary Care

Primary-health centers still rely on gauze and povidone-iodine, and many clinicians lack training in NPWT or hydrocolloids. National Health Mission curricula omit wound-care competencies, prolonging referrals and escalating complications. Stock-outs and cold-chain gaps further limit advanced product use outside metros. Rural areas face additional barriers: supply-chain fragility means advanced dressings frequently stock out, and cold-chain requirements for biological matrices remain unmet in facilities without reliable refrigeration.

Other drivers and restraints analyzed in the detailed report include:

- Product & Technology Innovation in Dressings & NPWT

- Indigenous Low-Cost NPWT & Smart Dressings Adoption

- High Treatment Cost of Advanced Products

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Dressings captured 46.06% of 2025 revenue, while bandages are on track for a 9.22% CAGR thanks to sports-medicine protocols favoring adhesive formats over gauze. Hospitals standardize dressings for diabetic ulcers, anchoring volumes, and bandage makers exploit dual distribution through institutional tenders and retail pharmacies. The India wound care management devices market for dressings will continue to outpace other categories, while bandages are carving a premium niche by positioning around rapid return-to-activity outcomes. Sensor-enabled dressings entering validation could bifurcate the category into commodity and smart-platform segments, reshaping pricing tiers.

The suture-dominated wound-closure device cluster benefits from locked-in hospital formulary contracts led by Ethicon and Covidien. NPWT, hemostats, and biological matrices remain niche as cost and reimbursement uncertainties limit scale. Once Ayushman Bharat broadens coverage, these high-margin segments are poised for catch-up growth within the India wound care management devices market.

List of Companies Covered in this Report:

- 3M

- Axio Biosolutions Private Limited

- B. Braun

- Cardinal Health

- Centaur Pharmaceuticals Private Limited

- Coloplast

- ConvaTec Group plc

- Datt Mediproducts Private Limited

- Dolphin Sutures

- Healthium Medtech Ltd

- Integra LifeSciences

- Johnson & Johnson

- Lotus Surgicals

- Medtronic

- Meril Life Science

- Molnlycke Health Care AB.

- Hartmann Group

- Rapidcure Healthcare Private Limited

- Smiths Group

- Stryker

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising DiabetesLinked Diabetic-Foot-Ulcer Burden

- 4.2.2 Increasing Surgical Volumes Across India

- 4.2.3 Product & Technology Innovation in Dressings & NPWT

- 4.2.4 Indigenous Low-Cost NPWT & Smart Dressings Adoption

- 4.2.5 Government PLI Scheme for Local Device Manufacturing

- 4.2.6 Growing Sports & Fitness Injuries

- 4.3 Market Restraints

- 4.3.1 Limited Awareness of Advanced Wound Care in Primary Care

- 4.3.2 High Treatment Cost of Advanced Products

- 4.3.3 Reimbursement Gaps Under Ayushman Bharat

- 4.3.4 NPPA Price-Control Risk for Imported Devices

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Dressings

- 5.1.2 Bandages

- 5.1.3 Wound Closure Devices

- 5.1.4 Other Wound Care Products

- 5.2 By Wound Type

- 5.2.1 Chronic Wounds

- 5.2.1.1 Diabetic Foot Ulcer

- 5.2.1.2 Pressure Ulcer

- 5.2.1.3 Other Chronic Wounds

- 5.2.2 Acute Wounds

- 5.2.2.1 Surgical Wounds

- 5.2.2.2 Burns

- 5.2.2.3 Other Acute Wounds

- 5.2.1 Chronic Wounds

- 5.3 By End User

- 5.3.1 Hospitals & Clinics

- 5.3.2 Ambulatory Surgical Centers

- 5.3.3 Home Healthcare

- 5.3.4 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 3M Company

- 6.3.2 Axio Biosolutions Private Limited

- 6.3.3 B. Braun SE

- 6.3.4 Cardinal Health, Inc.

- 6.3.5 Centaur Pharmaceuticals Private Limited

- 6.3.6 Coloplast A/S

- 6.3.7 ConvaTec Group plc

- 6.3.8 Datt Mediproducts Private Limited

- 6.3.9 Dolphin Sutures

- 6.3.10 Healthium Medtech Ltd

- 6.3.11 Integra LifeSciences Holdings Corporation

- 6.3.12 Johnson & Johnson (Ethicon)

- 6.3.13 Lotus Surgicals

- 6.3.14 Medtronic plc

- 6.3.15 Meril Life Sciences Private Limited

- 6.3.16 Molnlycke Health Care AB.

- 6.3.17 Paul Hartmann AG

- 6.3.18 Rapidcure Healthcare Private Limited

- 6.3.19 Smith & Nephew plc

- 6.3.20 Stryker Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment