|

시장보고서

상품코드

2061553

영국의 전력 EPC 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United Kingdom Power EPC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

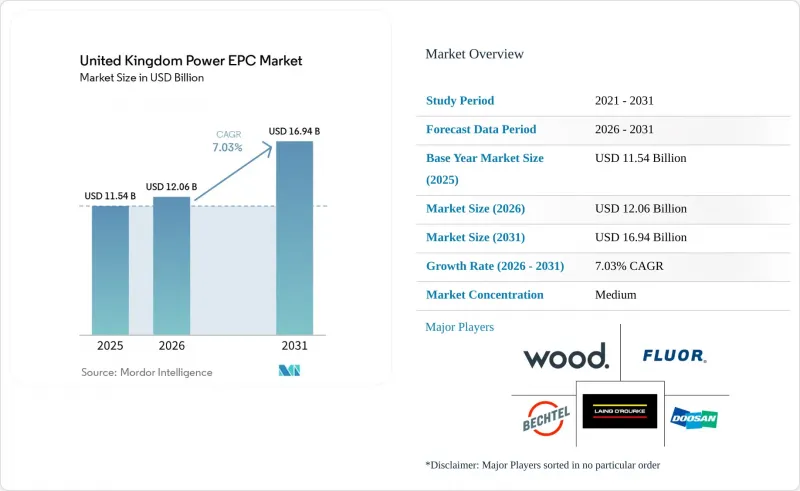

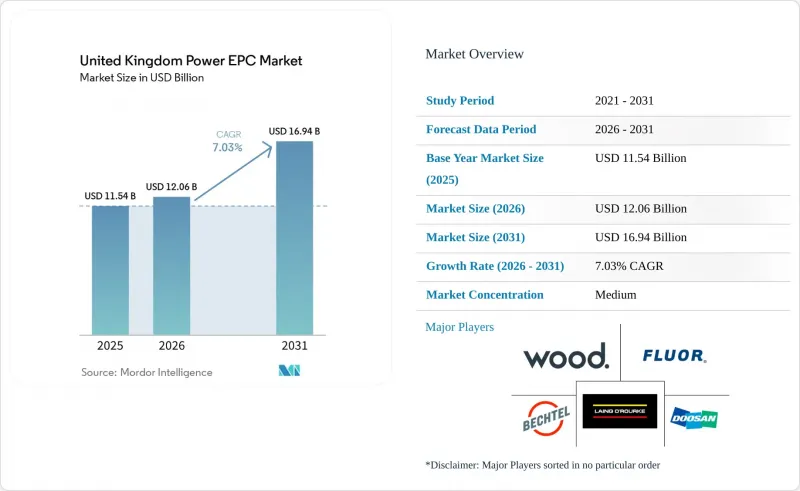

Mordor Intelligence에 의하면, 영국의 전력 EPC 시장 규모는 2026년에 120억 6,000만 달러로 추정되고, 예측 기간(2026-2031년) CAGR 7.03%로 성장을 지속할 것으로 예측되며, 2031년까지 169억 4,000만 달러에 이를 전망입니다.

본 보고서는 전력 EPC : 기술별(화력, 원자력, 재생에너지), 용량대별(100MW 이하, 100-499MW, 500MW 이상), 최종 사용자별(규제 대상 유틸리티자, 독립발전 사업자, 산업용 자가발전, 공공 부문 및 국영 기업), 그리고 송배전(T&D) EPC로 구분되어 있습니다. 시장 규모 및 전망은 금액(달러) 기준으로 제시되어 있습니다.

영국의 전력 EPC 시장 동향과 인사이트

영국의 해상 풍력 메가 프로젝트 추진 계획

ScotWind를 통해 부여된 해저 권익은 총 약 30기가와트에 달하는 17개 프로젝트를 포괄하는 반면, 크라운 에스테이트(Crown Estate)의 제5차 라운드에서는 켈트해에 최대 4.5기가와트의 부유식 발전 용량이 추가될 예정입니다. 이러한 수주 규모는 이미 가동 중인 14기가와트를 훨씬 웃도는 수준이며, 이로 인해 생산 일정이 단축되고 터빈 기초 및 송전 케이블에 대한 수요가 증가하고 있습니다. Orsted사의 2.9기가와트 규모인 Hornsea 3와 같은 프로젝트에서는 200기 이상의 터빈과 100킬로미터가 넘는 해저 케이블이 필요하며, 이는 프로젝트 규모가 확대되고 있음을 보여줍니다. 부유식 풍력 발전의 시제품은 동적 케이블 및 계류와 관련된 과제를 야기하고 있으며, 이는 심해 석유 및 가스전 분야의 경험을 보유한 계약업체들에게 유리하게 작용하고 있습니다. '클린 파워 2030 행동 계획'에 따른 송전망 개혁으로 대기 기간이 2.5년 미만으로 절반으로 줄어들면서, EPC 계약 체결이 가속화되고 있습니다. 이러한 요인들이 복합적으로 작용하여, 재생에너지 EPC 시장의 연평균 성장률(CAGR)이 12.8%를 나타낼 것으로 전망됩니다.

사이즈웰 C의 최종 투자 결정(FID) 이후 원자력 신규 건설의 재개

2025년 7월, 사이즈웰 C에 381억 달러를 투자하기로 결정했습니다. 이는 2016년 이후 처음으로 이루어진 대규모 원자력 발전소의 최종 투자 결정(FID)입니다. 규제자산기준(RAB) 모델을 통해 건설 리스크가 소비자에게 전가됨에 따라 자본 비용이 절감되고, 토목 공사, 원자로 건물 제작, 터빈 홀 통합을 포함한 EPC 업무의 범위가 확대됩니다. 주요 후보 업체로는 두산 바브콕(Doosan Babcock)과 안살도 뉴클리어(Ansaldo Nuclear)가 거론되고 있습니다. 정부가 제시한 24기가와트의 원자력 발전 목표는 6-8기의 추가 원자로 또는 소형 모듈형 원자로(SMR)의 도입을 의미하며, 이를 통해 수십 년에 걸친 EPC 사업이 지속될 것입니다. 10-12년에 이르는 장기적인 건설 주기로 인해 수익 인식은 2030년대까지 지속될 전망이며, 원자력규제청의 감독을 적절히 관리할 수 있는 시공사에게는 막대한 이익이 돌아갈 것으로 보입니다.

인플레이션으로 인한 EPC 비용 초과

2024년 건축자재 가격은 전년 대비 5.6% 상승했으며, 숙련 노동자의 인건비는 6.2% 상승했습니다. 2022-2023년 체결된 고정가격 해상 풍력 발전 계약은 철강 가격과 선박 운임이 지수 연동 조항을 상회함에 따라, 현재 이익률 압박에 직면해 있습니다. 힌클리 포인트 C의 예산은 최종 투자 결정(FID) 당시 330억 달러에서 2025년까지 445억 달러로 늘어났습니다. 도급업체들은 원가상환형 모델로 전환하고 있으며, 이로 인해 실행 위험은 줄어들고 있지만 경쟁력은 약화되고 있습니다.

부문별 분석

재생에너지는 2025년 전력 EPC 시장 규모의 76.3%를 차지했으며, 주로 해상 풍력발전에 힘입어 2031년까지 연평균 성장률(CAGR) 12.8%로 성장할 것으로 전망됩니다. 스콧윈드(ScotWind) 및 켈틱 씨(Celtic Sea) 프로젝트에는 400억 파운드(508억 달러)가 넘는 EPC 투자가 필요합니다. 제6회 차액결제계약(CfD) 입찰에서는 사상 최저의 행사 가격으로 9.6기가와트가 배정되어 비용 경쟁력이 강화되었습니다. 2016년 이후 정체되었던 원자력 EPC 매출은 Sizewell C의 최종 투자 결정(FID)에 힘입어 회복되었으며, 이로 인해 3.2기가와트의 용량이 추가될 예정입니다. 석탄 화력 발전소 폐쇄와 가스 프로젝트가 용량 시장 평가 하락에 직면하면서 화력 EPC 시장은 축소되는 추세이지만, 200억 파운드 규모의 CCUS 프로그램을 통해 자금을 지원받은 탄소 포집 및 저장(CCUS) 개조 사업이 좁은 틈새 시장을 유지하고 있습니다.

500메가와트를 초과하는 프로젝트는 2025년 EPC 총액의 63.6%를 차지했으며, 혼시 3, 혼시 4 및 도거뱅크 복합 시설이 이를 주도하고 있습니다. 기가와트 규모의 해상 풍력 발전 단지들은 터빈 조달에 있어 규모의 경제와 최적화된 해상 물류를 활용하고 있지만, 8-10년에 달하는 개발 주기로 인해 규제 리스크가 높아지고 있습니다. 100-499메가와트 규모는 토지 제약으로 인해 육상 풍력 및 태양광 발전 부지가 제한되는 가운데 완만하게 성장하고 있습니다.

100메가와트 이하 규모의 설비는 기업들이 계량기 뒤편에 태양광 발전 및 에너지 저장 시스템을 도입하거나 항만 기반의 마이크로그리드를 구축함에 따라 9.1%라는 가장 높은 연평균 성장률(CAGR)을 보일 것으로 전망됩니다. 티즈사이드 프리봇의 '넷 제로 클러스터'는 100메가와트 미만의 부지 내에 수소, 탄소 포집 및 열병합 발전 기술을 통합한 모듈형 에너지 파크 모델을 실증하고 있습니다. Ofgem의 지역 유연성 시장은 분산형 자원에 보상을 지급하므로, 1,000만 파운드 규모의 지역 에너지 기금으로 지원되는 지역 에너지 계획의 프로젝트의 경제성이 향상됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the united kingdom power ePC market size is estimated at USD 12.06 billion in 2026, and is expected to reach USD 16.94 billion by 2031, at a CAGR of 7.03% during the forecast period (2026-2031).

This report is Segmented by Power Generation EPC [Technology (Thermal, Nuclear, and Renewables), Capacity Band (Up To 100 MW, 100 To 499 MW, and Above 500 MW), and End-User (Regulated Utilities, Independent Power Producers, Industrial Captive Power, and Public Sector and SOE)], and Power Transmission and Distribution (T&D) EPC. The Market Sizes and Forecasts are Provided in Terms of Value (USD).

United Kingdom Power EPC Market Trends and Insights

UK Offshore-Wind Megaproject Pipeline

Seabed rights awarded under ScotWind cover 17 projects totaling about 30 gigawatts, while Crown Estate Round 5 adds up to 4.5 gigawatts of floating capacity in the Celtic Sea. These allocations dwarf the 14 gigawatts already operating, compressing fabrication schedules and boosting demand for turbine foundations and export cables. Projects such as Orsted's 2.9-gigawatt Hornsea 3 require more than 200 turbines and over 100 kilometers of subsea cable, illustrating the scale shift. Floating-wind prototypes introduce dynamic-cable and mooring challenges that favor contractors with deepwater oil-and-gas experience. Grid reforms under the Clean Power 2030 Action Plan halve queue times to under 2.5 years, accelerating EPC contract awards. Together, these forces underpin the 12.8% CAGR forecast for renewables EPC.

Nuclear New-Build Revival Post-Sizewell C FID

July 2025 marked the USD 38.1 billion commitment to Sizewell C, the first large-scale nuclear FID since 2016. The Regulated Asset Base model transfers construction risk to consumers, cutting the cost of capital and unlocking EPC scopes covering civil works, reactor-island fabrication, and turbine-hall integration. Doosan Babcock and Ansaldo Nuclear are shortlisted for major packages. The government's 24-gigawatt nuclear target implies six to eight additional reactors or an SMR fleet, sustaining multidecade EPC workloads. Extended construction cycles of 10-12 years mean revenue recognition will carry well into the 2030s, rewarding contractors that navigate Office for Nuclear Regulation oversight.

Inflation-Driven EPC Cost Overruns

Construction input prices rose 5.6% year-over-year in 2024, while skilled labor costs climbed 6.2%. Fixed-price offshore-wind contracts signed in 2022-2023 now face margin compression as steel and marine-vessel rates exceed indexed clauses. Hinkley Point C's budget climbed from USD 33 billion at FID to USD 44.5 billion by 2025. Contractors are shifting toward cost-reimbursable models, easing execution risk but eroding bid competitiveness.

Other drivers and restraints analyzed in the detailed report include:

- Fast-Track Grid-Reinforcement Funding (RIIO-T3)

- PPAs Tied to Corporate Net-Zero Pledges

- Supply-Chain Bottlenecks in High-Voltage Equipment Imports

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Renewables captured 76.3% of 2025 generation EPC value and are projected to grow at a 12.8% CAGR through 2031, driven chiefly by offshore wind. ScotWind and Celtic Sea concessions require EPC outlays above GBP 40 billion (USD 50.8 billion). The sixth Contracts for Difference (CfD) round awarded 9.6 gigawatts at record-low strike prices, reinforcing cost competitiveness. Nuclear EPC revenue, dormant since 2016, resurged with the Sizewell C FID, which alone adds 3.2 gigawatts of capacity. Thermal EPC shrinks as coal retires and gas projects face capacity-market de-rating, though carbon-capture retrofits preserve a narrow niche funded by the GBP 20 billion CCUS program.

Projects exceeding 500 megawatts held 63.6% of the 2025 EPC value, dominated by Hornsea 3, Hornsea 4, and the Dogger Bank complex. Gigawatt-scale offshore arrays leverage turbine-procurement scale and optimized marine logistics yet endure 8-10-year development cycles that heighten regulatory risk. The 100-to-499-megawatt band grows moderately as land constraints cap onshore wind and solar acreage.

Installations up to 100 megawatts will post the fastest 9.1% CAGR as corporates deploy behind-the-meter solar-plus-storage and port-based microgrids. Teesside Freeport's Net Zero cluster demonstrates a modular energy-park model integrating hydrogen, carbon capture, and combined-heat-and-power within a sub-100-megawatt footprint. Ofgem's local flexibility markets compensate distributed resources, improving project economics for community-energy schemes backed by the GBP 10 million Community Energy Fund.

List of Companies Covered in this Report:

- Fluor Ltd

- Wood plc

- Bechtel Corp

- Doosan Babcock Ltd

- Ramboll UK Ltd

- Laing O'Rourke

- Orsted A/S

- Balfour Beatty

- General Electric Co.

- Siemens Energy AG

- ABB Ltd

- Hitachi Energy Ltd

- Prysmian Group

- Ansaldo Nuclear Ltd

- Mott MacDonald Ltd

- Kier Infrastructure

- Bouygues Energies & Services

- Vinci Energies UK

- Skanska UK

- Engie Solutions UK

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Installed Capacity Outlook

- 4.3 Primary-Energy Consumption Snapshot

- 4.4 Market Drivers

- 4.4.1 UK offshore-wind megaproject pipeline

- 4.4.2 Nuclear new-build revival post-Sizewell C FID

- 4.4.3 Ageing thermal fleet repowering mandates

- 4.4.4 Fast-track grid-reinforcement funding (RIIO-T3)

- 4.4.5 PPAs tied to corporate net-zero pledges

- 4.4.6 Modular "energy-park" concepts adopted by UK ports

- 4.5 Market Restraints

- 4.5.1 Inflation-driven EPC cost overruns

- 4.5.2 Supply-chain bottlenecks in HV equipment imports

- 4.5.3 Public opposition to on-shore transmission corridors

- 4.6 Supply-Chain Analysis

- 4.7 Regulatory Landscape

- 4.8 Technological Outlook

- 4.9 Porter's Five Forces

- 4.9.1 Threat of New Entrants

- 4.9.2 Bargaining Power of Suppliers

- 4.9.3 Bargaining Power of Buyers

- 4.9.4 Threat of Substitutes

- 4.9.5 Competitive Rivalry

- 4.10 PESTLE Analysis

5 Market Size & Growth Forecasts

- 5.1 Power Generation EPC

- 5.1.1 By Technology

- 5.1.1.1 Thermal

- 5.1.1.2 Nuclear

- 5.1.1.3 Renewables

- 5.1.2 By Capacity Band

- 5.1.2.1 Up to 100 MW (DER, micro-grid)

- 5.1.2.2 100 to 499 MW

- 5.1.2.3 Above 500 MW

- 5.1.3 By End-User

- 5.1.3.1 Regulated Utilities

- 5.1.3.2 Independent Power Producers

- 5.1.3.3 Industrial Captive Power

- 5.1.3.4 Public Sector and SOE

- 5.1.1 By Technology

- 5.2 Power Transmission and Distribution (T&D) EPC

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Fluor Ltd

- 6.4.2 Wood plc

- 6.4.3 Bechtel Corp

- 6.4.4 Doosan Babcock Ltd

- 6.4.5 Ramboll UK Ltd

- 6.4.6 Laing O'Rourke

- 6.4.7 Orsted A/S

- 6.4.8 Balfour Beatty

- 6.4.9 General Electric Co.

- 6.4.10 Siemens Energy AG

- 6.4.11 ABB Ltd

- 6.4.12 Hitachi Energy Ltd

- 6.4.13 Prysmian Group

- 6.4.14 Ansaldo Nuclear Ltd

- 6.4.15 Mott MacDonald Ltd

- 6.4.16 Kier Infrastructure

- 6.4.17 Bouygues Energies & Services

- 6.4.18 Vinci Energies UK

- 6.4.19 Skanska UK

- 6.4.20 Engie Solutions UK

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment