|

시장보고서

상품코드

2061585

의료 BPO : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Healthcare BPO - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

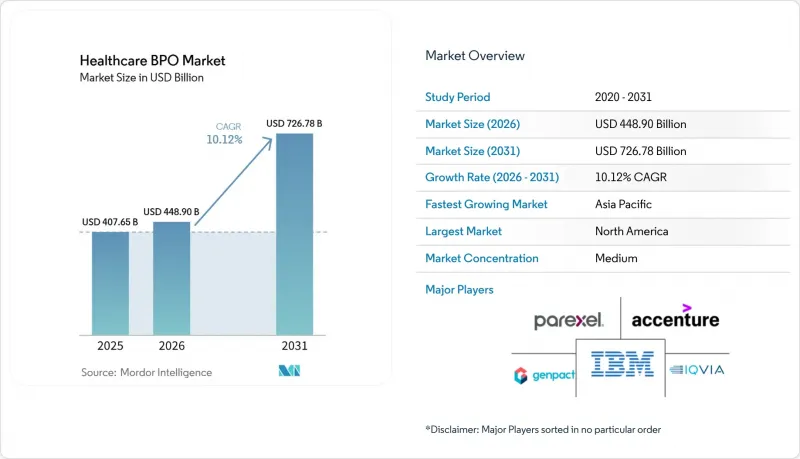

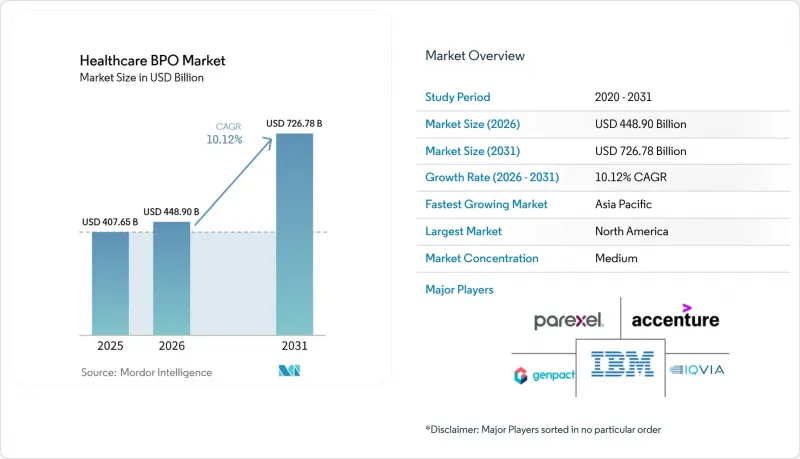

Mordor Intelligence에 의하면, 의료 BPO 시장 규모는 2025년 4,076억 5,000만 달러로 평가되었습니다. 2026년에는 4,489억 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR은 10.12%를 나타내, 2031년에는 7,267억 8,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 서비스 유형(지불자 대상 서비스(청구 관리, 케어 관리 등), 제공업체 대상 서비스(환자 케어 서비스 등), 제약 서비스), 서비스 제공 모델(온쇼어 등), 기술 도입 모델(기존의 리프트 앤 시프트형 BPO 등), 그리고 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 의료 BPO 시장 동향과 인사이트

니어쇼어 아웃소싱은 실시간 협력을 가능하게 합니다.

학술연구에 따르면, 업무를 인근 국가로 이관하는 의료 기관은 국내 제공에 비해 20-30%의 비용 절감을 실현하는 동시에 운영 리스크를 35% 낮출 수 있는 것으로 나타났습니다. 미국, 그 영토 또는 캐나다 내에 전자 건강 기록을 보관하도록 의무화하는 플로리다주의 요건 등, 데이터 소재지에 관한 규제가 강화됨에 따라 원격 허브보다 인근 거점의 매력이 높아지고 있습니다. 멕시코의 니어쇼어 IT 및 비즈니스 서비스 매출이 연간 10.5% 증가한 것은 특히 수익 사이클 및 임상 문서화 계약 분야에서 멕시코가 유리한 입지를 차지하고 있음을 더욱 확고히 하고 있습니다. USMCA(미국·멕시코·캐나다 협정)의 디지털 무역 장은 국경을 넘는 데이터 유통 및 지적 재산권 보호와 관련하여 법적 확실성을 제공하며, 이를 통해 지불 기관과 의료 제공업체는 해당 지역공급업체와 다년 계약을 체결하는 데 자신감을 갖게 되었습니다. 스탠퍼드 대학의 조사 결과에 따르면, 근접성을 중시한 모델은 규정 준수 달성률을 40% 향상시키고, 의사소통상의 실수를 25% 줄이는 것으로 나타났습니다. 이러한 요인들이 복합적으로 작용하여, 특히 수익 주기의 중간 단계에서 의료 BPO 시장에 유리한 지리적 변화가 가속화되고 있습니다.

임상 프로세스 아웃소싱(CPO)의 급속한 확산

5년에 걸친 종단적 조사에 따르면, 외부 파트너를 활용한 의뢰사는 규정 준수 문제를 일으키지 않으면서 임상시험 기간을 18개월 단축할 수 있었습니다고 보고되었습니다. 팬데믹 이후 분산형 임상시험에 대한 관심이 높아짐에 따라, 전문 BPO 기업이 이미 운영 중인 환자 참여 도구 및 데이터 통합 플랫폼에 대한 수요가 증가하고 있습니다. 하버드 의과대학 연구진은 사내 프로그램과 비교했을 때, 외주화된 임상시험에서 피험자 등록 수가 22% 증가했고 데이터 품질 점수가 15% 향상되었음을 확인했습니다. 인공지능(AI) 엔진이 데이터 수집 및 규제 당국에 대한 신청 업무를 자동화함에 따라, 공급업체는 기존의 모니터링 기능에 부가가치가 높은 분석 기능을 더해 제공할 수 있게 됩니다. 또한 아웃소싱을 통해 생명공학 기업 팀은 전 세계 환자 풀과 전문적인 규제 대응 노하우를 활용하면서 핵심 연구 개발에 집중할 수 있게 됩니다. 이러한 시너지 효과 덕분에 CPO는 헬스케어 업무 프로세스 아웃소싱 시장에서 가장 빠르게 성장하고 있는 분야가 되었습니다.

복잡한 다자간 규제

끊임없이 진화하는 HIPAA 조항은 GDPR(EU 개인정보보호규정)과 얽혀 있어, 공급업체는 암호화, 다단계 인증, 그리고 지역별 정보 유출 대응 프로토콜을 모두 준수해야만 합니다. 공급업체는 새로운 국경을 넘는 호스팅 시나리오마다 법적 심사를 받아야 합니다. 플로리다주의 해외 데이터 저장 금지 조치는 여러 주에 걸쳐 운영되는 시스템에서 도입 비용 증가와 지연을 초래하고 있습니다. 소규모 공급업체들은 규정 준수 팀을 병행 운영하기 위한 자금 확보에 어려움을 겪고 있으며, 이로 인해 헬스케어 비즈니스 프로세스 아웃소싱(BPO) 서비스 시장 전체의 신규 고객 확보 성장세가 둔화되고 있습니다.

부문별 분석

의약품 서비스 분야에서 제조 부문은 의료 BPO 시장에서 압도적인 점유율을 차지하고 있습니다. 생물학적 제제의 복잡성이 증가함에 따라, 제조 투자는 고효능 제제 및 세포 치료 시설로 전환되고 있습니다. 이러한 추세에 따라, 기술 이전과 규제 관련 로트 릴리스 서비스를 패키지로 묶은 장기 마스터 서비스 계약이 활성화되고 있습니다. 영업 및 마케팅 아웃소싱은 옴니채널을 통한 의료진과의 협력 및 규제 준수 환자 지원 프로그램에 중점을 두고 있습니다. 한편, 연구개발(R&D) 아웃소싱은 소규모 생명공학 기업이 사내에서 감당하기 어려운 전문적인 생물정보학, 독성학, 동반진단 분석 업무를 담당하고 있습니다. 시리얼화 및 위조 방지 관련 규제가 강화됨에 따라, 비임상 공급망의 통합이 진행되고 있습니다. 디지털 트윈 모델링과 실제 세계 데이터(RWE) 플랫폼은 유해사건의 원인을 거의 실시간으로 파악함으로써 임상시험의 조기 종결을 가능하게 하고 있습니다. 임상 데이터와 상업 데이터의 통합은 제품 출시 속도를 높여주며, 한편 사모펀드가 지원하는 CRO의 통합은 임상시험 기관 모니터링 및 중앙 검사실 서비스를 효율화하여, 의뢰사가 파이프라인 연구에 집중하고 건전한 이익률을 유지할 수 있도록 돕고 있습니다. 통신사 대상 서비스는 2031년까지 연평균 성장률(CAGR)이 14.78%로, 가장 빠르게 성장하고 있는 서비스 분야입니다. 수익 주기 관리 서비스는 진료 기록 및 청구 정보의 수집과 보험사의 편집 과정을 자동화함으로써, 인력 부족 상황에서도 병원의 재정적 안정을 뒷받침하고 유동 자금의 변동을 억제합니다. 환자 관리 서비스는 가상 간호 및 컨택 센터를 통한 분류 시스템을 통합하여 환자 만족도를 높이고, 전략적 기획 서비스는 의뢰 패턴과 보험 가입자 구성을 분석하여 서비스 라인에 대한 투자를 유도합니다. Ensemble Health가 도입한 예측 알고리즘과 같은 첨단 AI는 룰 엔진만으로는 해결할 수 없는 복잡한 청구서만 숙련된 코더에게 배정하므로, 병원은 인력을 비례적으로 늘리지 않고도 순수익을 증대시킬 수 있습니다. 이러한 생산성의 변화에 따라 아웃소싱은 단순한 비용 절감 수단이 아닌 수익 창출의 원동력으로 자리매김하며, 의료 BPO 업계를 강화하고 있습니다.

지역별 분석

2025년, 북미는 전 세계 매출의 48.15%를 차지했습니다. 이는 해당 지역의 복잡한 상환 환경이 광범위한 전문가의 지원을 필요로 했기 때문입니다. 병원은 만성적인 인력 부족을 메우기 위해 업무의 중간 단계를 지속적으로 아웃소싱하고 있습니다. 옵텀(Optum)의 가치 기반 의료로의 경영 방침 전환은 임상 문서 작성과 네트워크 스터링을 통합한 종합적 아웃소싱 계약의 성장을 뒷받침하고 있습니다. 캐나다 전역에서 전자건강기록(EHR)의 상호운용성을 촉진하고, 니스쇼어 거점으로서 멕시코의 부상은 이 지역의 활력을 더욱 높이고 있습니다. 따라서, 의료 BPO 시장은 이 지역에서 단순한 가격 경쟁이 아닌, 플랫폼에 대한 투자와 규제 대응의 심화에 초점을 맞추었습니다.

아시아태평양은 인도, 중국, 동남아시아의 집단건강관리 이니셔티브와 디지털 헬스 분야에 대한 자금 지원에 힘입어 12.62%라는 가장 높은 연평균 성장률(CAGR)을 기록하고 있습니다. 인도의 여러 공급업체들은 데이터 현지화 조항에 대응하기 위해 말레이시아와 UAE에 니어쇼어 거점을 추가로 마련하고 있습니다. 필리핀에서는 환자 참여 센터가 확대되고 있는 반면, 중국의 민간 서비스 제공업체들은 새로운 데이터 보안법 요건을 잘 이해하고 있는 국내 BPO 업체에 의존하고 있습니다. 인력 공급은 여전히 매력적이지만, 개인정보 보호에 대한 기대가 높아짐에 따라 기업들은 고도화된 사이버 방어 시스템에 투자할 수밖에 없는 실정입니다. 그 결과, 의료 BPO 시장은 최종 시장과 가까운 곳에 거점을 분산하고, 다국어 대응이 가능한 컴플라이언스 팀을 배치함으로써 이에 대응하고 있습니다.

GDPR(EU 개인정보보호규정)로 인해 해외로의 데이터 유출이 제한되는 가운데, 유럽에서는 꾸준한 성장이 이어지고 있습니다. 독일과 영국에서는 NHS나 Krankenkasse의 기준을 관리할 수 있는 국내 분석 파트너를 선호합니다. 남유럽 국가들에서는 청구 처리 센터의 현대화가 진행되고 있으며, 솅겐 지역 내 국경을 초월한 상환 제도를 잘 이해하고 있는 지역 통합 업체에 업무를 아웃소싱하고 있습니다. 공급업체들은 EU 클라우드 행동 강령의 원칙을 반영하여 프리미엄 가격 책정 및 장기 계약을 확보하고 있습니다. 의료 BPO 시장은 전자 처방전 감사 및 EU 의약품 전략에 부합하는 성과 측정과 같은 전문적인 서비스를 통해 지속적으로 성숙해 가고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.19According to Mordor Intelligence, the healthcare bPO market size is expected to grow from USD 407.65 billion in 2025 to USD 448.90 billion in 2026 and is forecast to reach USD 726.78 billion by 2031 at 10.12% CAGR over 2026-2031.

This report is Segmented by Service Type (Payer Service (Claims Management, Care Management, and More), Provider Service (Patient Care Service, and More), and Pharmaceutical Service), Service Delivery Model (Onshore and More), Technology Adoption Model (Traditional Lift-And-Shift BPO, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Healthcare BPO Market Trends and Insights

Near-shore outsourcing enables real-time collaboration

Academic research shows that healthcare organizations shifting work to nearby countries reduce operational risk by 35% while still saving 20-30% compared with on-shore delivery. Heightened data-residency laws such as Florida's requirement that electronic health records stay in the United States, its territories, or Canada make proximate sites more attractive than far-shore hubs. Mexico's 10.5% annual rise in near-shore IT and business services revenue further strengthens its position as a preferred location, particularly for revenue cycle and clinical documentation contracts. The USMCA's digital-trade chapter provides legal certainty regarding cross-border data flows and intellectual property protection, giving payers and providers confidence to award multi-year deals to suppliers in the region. Stanford University findings indicate that proximity-based models enhance compliance outcomes by 40% and reduce communication errors by 25%. Together, these factors accelerate a geographic shift that favors the healthcare BPO market, especially for mid-cycle revenue functions.

Rapid uptake of clinical process outsourcing (CPO)

A five-year longitudinal study reported that sponsors using external partners short-ened clinical trials by 18 months without sacrificing compliance. Post-pandemic interest in decentralized studies increases the need for patient-engagement tools and data-integration platforms that specialized BPO firms already operate. Harvard Medical School researchers observed 22% higher enrollment and 15% better data-quality scores in outsourced trials versus in-house programs. As artificial-intelligence engines automate data capture and regulatory-submission tasks, vendors can layer value-added analytics on top of traditional monitoring. Outsourcing also frees biotech teams to focus on core R&D while accessing global patient pools and dedicated regulatory expertise. This combination positions CPO as the fastest-expanding slice of the healthcare business process outsourcing market.

Complex Multi-Jurisdictional Regulations

Ever-evolving HIPAA clauses intersect with GDPR, forcing vendors to juggle encryption, multifactor authentication, and localized breach protocols. Suppliers incur legal reviews for every new cross-border hosting scenario. Florida's prohibition on non-domestic storage increases onboarding cost and delays for multistate systems. Smaller vendors struggle to fund parallel compliance teams, which tempers new-logo growth across the Healthcare Business Process Outsourcing (BPO) Services market.

Other drivers and restraints analyzed in the detailed report include:

- Healthcare reforms propel specialized outsourcing

- Generative-AI automation unlocks mid-cycle revenue deals

- Hidden Total Cost and Vendor Lock-in

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

By pharmaceutical services, manufacturing commands a dominant share in the healthcare business process outsourcing market. Manufacturing investments are shifting toward high-potency and cell-therapy facilities, driven by the growing complexity of biologicals. This trend is fostering long-term master service agreements that bundle technology transfer and regulatory lot-release services. Sales and Marketing outsourcing focuses on omnichannel physician engagement and compliant patient-support programs, while R&D outsourcing addresses specialized bioinformatics, toxicology, and companion-diagnostic analytics that smaller biotech firms cannot scale internally. Tightening serialization and anti-counterfeit mandates are driving the orchestration of non-clinical supply chains. Digital twin modeling and real-world-evidence platforms are expediting trial close-outs by mapping adverse-event triggers in near real time. Consolidating clinical and commercial data lakes enhances product-launch speed, while private equity-backed CRO roll-ups streamline site monitoring and central lab services, enabling sponsors to focus on pipeline science and maintain healthy margins.By provider services is the fastest growing service with a 14.78% CAGR over 2031. Revenue cycle management services support hospital fiscal stability amid labor shortages by automating clinical notes, charge capture, and payer edits, reducing cash-on-hand volatility. Patient Care Services integrates virtual nursing with contact-center triage to enhance experience scores, while Strategic Planning services analyze referral patterns and payer mixes to guide service-line investments. Advanced AI, such as predictive algorithms used by Ensemble Health, routes complex invoices to senior coders only when rules engines cannot resolve them on their own, enabling hospitals to increase net revenue without proportional headcount growth. This productivity shift positions outsourcing as a revenue driver rather than just a cost-cutting tool, reinforcing the healthcare bpo industry.

Geography Analysis

North America contributed 48.15% of global revenue in 2025 as the region's complex reimbursement environment required extensive expert support. Hospitals continue to outsource mid-cycle operations to offset chronic staffing gaps. Optum's leadership reshuffle toward value-based care underscores growth in bundled outsourcing contracts that integrate clinical documentation with network steering. Canada's drive for pan-Canadian EHR interoperability and Mexico's rise as nearshore hub extend regional dynamism. The Healthcare BPO market therefore focuses on platform investments and regulatory depth in this geography rather than price competition alone.

Asia-Pacific records the fastest 12.62% CAGR, buoyed by population-health initiatives and digital-health funding in India, China, and Southeast Asia. Indian vendors add nearshore centers in Malaysia and the UAE to meet data-localization clauses. The Philippines expands patient-engagement centers, while China's private providers lean on domestic BPOs versed in new data-security law requirements. Talent supply remains a draw, yet escalating privacy expectations mean firms must invest in advanced cyber defenses. Consequently, the Healthcare BPO market adapts by distributing centers closer to end-markets and embedding multilingual compliance teams.

Europe maintains steady growth as GDPR limits offshore traffic. Germany and the United Kingdom favor domestic analytics partners able to manage NHS or Krankenkasse standards. Southern European countries modernize claims clearinghouses, outsourcing to regional integrators that understand cross-border reimbursement across the Schengen area. Vendors embed EU Cloud Code of Conduct principles, gaining premium pricing and long-term contracts. The Healthcare BPO market continues to mature through specialized offerings such as e-prescription auditing and outcome measurement aligned with the EU Pharmaceutical Strategy.

- Accenture

- United Health Group

- Cognizant

- Genpact

- Wipro

- Tata Consultancy Services

- IBM

- IQVIA

- Parexel International

- GeBBs Healthcare Solutions

- Sutherland Global Services

- R1 RCM

- Conifer Health Solutions

- Firstsource Solutions

- Omega Healthcare

- WNS Global Services

- NTT DATA

- Capgemini

- Optum

- EXL Service Holdings

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rise of Near-shore Outsourcing & Access to Technology

- 4.2.2 Rapid Increase in Clinical Process Outsourcing (CPO)

- 4.2.3 Healthcare Reforms (PPACA / ICD-11 / Value-based Care) Spur Outsourcing

- 4.2.4 Generative-AI Coding Automation Unlocks Mid-RCM Deals

- 4.2.5 Payvider Convergence Driving Integrated BPaaS Models

- 4.2.6 PE-fuelled Roll-ups Creating Specialist Delivery Centers

- 4.3 Market Restraints

- 4.3.1 Complex Multi-jurisdictional Regulations

- 4.3.2 Hidden Total Cost & Vendor Lock-in

- 4.3.3 Sovereign Data-Residency Laws Fragment Delivery

- 4.3.4 Shortage of Medically-Trained Coders in Tier-2 Hubs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technology Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value-USD)

- 5.1 By Service Type

- 5.1.1 By Payer Service

- 5.1.1.1 Human Resource Management

- 5.1.1.2 Claims Management

- 5.1.1.3 Customer Relationship Management (CRM)

- 5.1.1.4 Operational / Administrative Management

- 5.1.1.5 Care Management

- 5.1.1.6 Provider Management

- 5.1.1.7 Other Payer Services

- 5.1.2 By Provider Service

- 5.1.2.1 Patient Enrollment & Strategic Planning

- 5.1.2.2 Patient Care Service

- 5.1.2.3 Revenue Cycle Management

- 5.1.3 By Pharmaceutical Service

- 5.1.3.1 Research & Development

- 5.1.3.2 Manufacturing

- 5.1.3.3 Non-clinical Service

- 5.1.3.3.1 Supply-Chain Management & Logistics

- 5.1.3.3.2 Sales & Marketing Services

- 5.1.3.3.3 Other Non-clinical Services

- 5.1.1 By Payer Service

- 5.2 By Service Delivery Model

- 5.2.1 Onshore

- 5.2.2 Nearshore

- 5.2.3 Offshore

- 5.2.4 Hybrid / Multishore

- 5.3 By Technology Adoption Model

- 5.3.1 Traditional Lift-and-Shift BPO

- 5.3.2 Platform-based BPaaS

- 5.3.3 Intelligent-Automation-led BPO

- 5.3.4 Generative-AI-embedded BPO

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1 Accenture

- 6.3.2 UnitedHealth Group

- 6.3.3 Cognizant Technology Solutions

- 6.3.4 Genpact

- 6.3.5 Wipro

- 6.3.6 Tata Consultancy Services

- 6.3.7 IBM Corporation

- 6.3.8 IQVIA

- 6.3.9 Parexel International Corporation

- 6.3.10 GeBBS Healthcare Solutions

- 6.3.11 Sutherland Global Services

- 6.3.12 R1 RCM Inc.

- 6.3.13 Conifer Health Solutions

- 6.3.14 Firstsource Solutions

- 6.3.15 Omega Healthcare

- 6.3.16 WNS Global Services

- 6.3.17 NTT DATA

- 6.3.18 Capgemini SE

- 6.3.19 Optum

- 6.3.20 EXL Service Holdings

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment