|

시장보고서

상품코드

2061618

미국의 의료 BPO : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United States Healthcare BPO - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

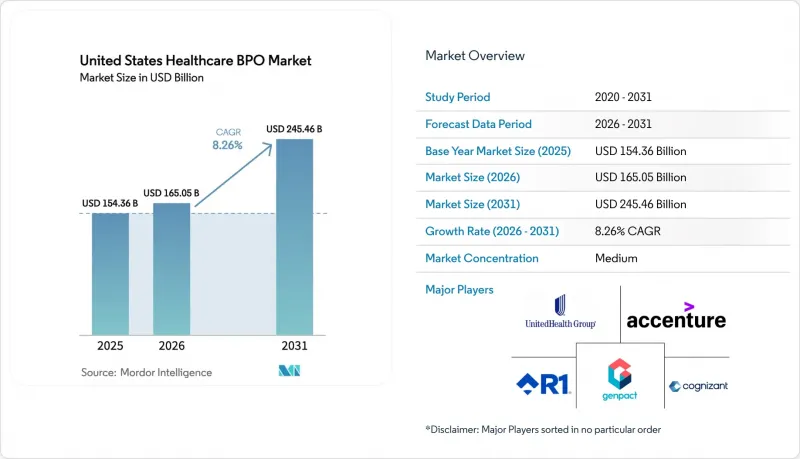

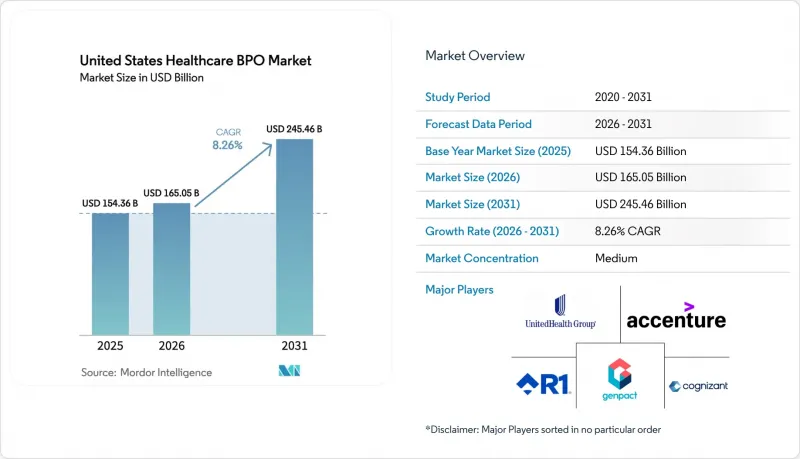

Mordor Intelligence에 의하면, 미국의 의료 BPO 시장 규모는 2025년 1,543억 6,000만 달러로 평가되었습니다. 2026년에는 1,650억 5,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR은 8.26%를 나타내, 2031년에는 2,454억 6,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 서비스 유형(지불자 대상 서비스(청구 관리 등), 제공업체 대상 서비스(환자 관리 서비스 등), 기타), 제공 모델(온쇼어, 니어쇼어, 오프쇼어), 서비스 제공 형태(캡티브, 써드파티, 하이브리드), 최종 고객(지불자, 제공업체, 제약·바이오기술 기업, 정부 기관)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국의 의료 BPO 시장 동향과 인사이트

지불자 및 의료 제공업체에 대한 관리 비용 부담 증가

병원들은 청구 기각에 대한 이의 제기에 매년 197억 달러를 지출하고 있으며, 2025년의 기각률은 11.8%에서 19% 사이가 되었습니다. 이에 따라 CFO는 고정 인건비를 절감하고 현금 회수율을 개선할 수 있는 성과급형 파트너에게 수익 사이클 관련 업무를 아웃소싱해야 하는 상황에 직면해 있습니다. 2023년 국내 의료비는 4조 9,000억 달러에 달했으며, 2033년까지 연평균 5.8%의 성장률을 보일 것으로 전망됨에 따라, 수급 자격 확인, 사전 승인 및 청구 심사와 관련된 업무 부담이 증가하고 있습니다. 민간 보험의 보상액 증가율은 의료비 인플레이션율을 150-200베이시스포인트 밑도는 추세를 이어가고 있어, 의료 제공업체의 이익률을 압박하고 있으며, 이로 인해 비임상 업무의 아웃소싱을 피할 수 없게 만들고 있습니다. 2023년부터 2024년에 걸쳐 지방 병원의 거의 절반이 영업 손실을 기록했으며, 600개 이상의 의료 기관이 여전히 높은 재무적 위험에 노출되어 있는 상황에서 수익 사이클 BPO는 환자 서비스를 유지하기 위한 생명줄이 되고 있습니다. 의료 손실률이 규제 상한선 근처에서 유지되고 있어, 보험사들도 비슷한 압박에 직면해 있습니다. 미국 상위 10대 건강보험사 중 9곳은 이미 청구 및 가입자 관리 업무에서 콘듀언트에 의존하고 있습니다.

첨단 기술(AI, RPA, 애널리틱스) 도입을 통한 규모의 경제 실현

생성형 AI는 사전 승인, 이의 제기, 이용 관리 등 각 워크플로우에서 심사 소요 시간과 직원들의 업무량을 대폭 단축하고 있습니다. HCLTech는 자사의 생성형 AI 솔루션을 통해 특정 지역의 블루크로스 보험 플랜에서 임상 심사 시간을 3시간에서 20분으로 단축하고, 비용을 30% 절감할 수 있음을 입증했습니다. 가입자 수 100만 명 규모의 보험사는 일반적으로 임상 심사 인건비로 5,000만-7,000만 달러를 지출하며, 간호사 200-300명 규모의 인력을 유지하고 있습니다. 생성형 AI를 활용한 정보 추출 및 요약 덕분에 간호사는 서류 수집이 아닌 결정 내용의 검증에 전념할 수 있게 되었으며, 이에 따라 인력 수요가 감소하고 있습니다. 2024년 4월에 도입된 Optum Real은 보험 적용 여부를 즉시 확인할 수 있게 해주었으며, Allina Health에서 실시한 초기 시범 운영을 통해 행정 처리 오류가 감소하고 환자 경험이 개선된 것으로 확인되었습니다. 코그니전트의 BPaaS 플랫폼은 RPA와 머신러닝을 결합하여 총 소유 비용을 25-50% 절감합니다. 한편, 엠블럼 헬스는 시스템 도입 후 청구 처리의 첫 번째 통과율(first-pass yield)이 99% 향상되었다고 보고했습니다. IBM 컨설팅에 따르면, 바이오의약품 업계의 고객사들은 컨텐츠 양이 많은 워크플로우에 생성형 AI를 활용함으로써 규제 관련 문서 작성 주기를 50-75% 단축할 수 있게 되었다고 합니다.

침해 발생 후의 사이버 보안 및 데이터 개인정보 보호에 대한 우려

체인지 헬스케어에 대한 랜섬웨어 공격은 수천 곳의 의료 기관의 보험 청구 업무를 마비시키고 약 2억 건의 기록이 유출되는 사태를 초래했으며, 이에 따라 공급업체들은 사이버 위험 대응 프로토콜을 재검토하게 되었습니다. 2024년 JAMA의 조사에 따르면, 1억 7,000만 건의 기록에 영향을 미친 566건의 침해 사례가 확인되었으며, 침해된 데이터의 69%는 랜섬웨어에 의한 것이었습니다. 미국 보건복지부(HHS)의 시민권국은 2024년 한 해 동안만 총 87만 5,000달러의 HIPAA 합의금을 부과하며 규제 집행 강화의 움직임을 분명히 보여주었습니다. 현재 보험 지급 기관은 공급업체에 대해 SOC 2 Type II 인증, 독립적인 침투 테스트, 그리고 고액 보상 한도의 사이버 보험 가입을 의무화하고 있으며, 이로 인해 소규모 해외 공급업체의 진입 장벽이 높아지고 있습니다. 2025년 1월에 발생한 Conduent의 보안 사고는 우려를 증폭시켰으며, 투명한 사고 대응 절차서의 필요성을 여실히 드러냈습니다. 일부 주에서는 의료 BPO 업체에 대한 최소 사이버 보안 기준을 의무화하는 법안을 검토하고 있으며, 이로 인해 성숙한 보안 운영 체계를 갖춘 대형 공급업체들이 더욱 유리한 입지를 차지하게 될 것입니다.

부문별 분석

2025년, 미국의 의료 BPO 시장 점유율의 58.62%를 제약 서비스가 차지했습니다. 이는 각 후원사가 의약품 개발 일정을 앞당기는 가운데, 임상시험 관리, 규제 관련 문서 작성, 제조 품질 보증이 주도한 결과입니다. IQVIA는 2024년에 154억 달러의 매출을 기록했으며, 320억 달러 규모의 미수주 물량을 보유하고 있어 계약 연구 역량에 대한 끊임없는 수요를 입증하고 있습니다. 2024년 9월에 발표된 분산형 임상시험에 관한 FDA 지침은 아웃소싱의 적용 범위를 원격 모니터링 및 재택치료 분야까지 확대함으로써 새로운 활용 사례를 촉진하고 있습니다. 한편, 의료기관 대상 서비스는 병원들의 청구 거절률이 최대 19%에 달하고 회수 비용이 증가함에 따라, 종합적인 수익 사이클 파트너를 찾는 움직임이 강화될 것으로 예상에 따라, 2026년부터 2031년까지 연평균 성장률(CAGR) 12.73%로 가장 빠르게 성장할 것으로 전망됩니다. 의료 시스템이 청구, 코딩 및 환자 비용 부담과 관련된 종합적인 솔루션을 요구함에 따라, 의료 서비스 제공업체 대상 계약 분야의 미국의 의료 BPO 시장 규모는 급격히 확대될 전망입니다.

제약 아웃소싱은 임상 연구를 넘어 공급망 및 물류, 배치 기록 검토, 옴니채널 판매 지원 등으로 지속적으로 다각화되고 있으며, 21 CFR Part 11에 기반한 데이터 무결성에 관한 더욱 엄격한 규제에 대응하고 있습니다. 제조 지원 BPO는 검증된 품질 보증 시스템을 갖추지 못한 중소 바이오기술 기업에게 특히 매력적인 분야입니다. 한편, 페이어 서비스는 전국 규모의 보험사와 플랫폼 중심 벤더 사이에 구축된 견고한 관계가 고객 이탈을 억제하고 있기 때문에 안정적인 중견 시장 내의 틈새 분야로 자리 잡고 있습니다. 코그니전트의 TriZetto만 해도 650여 개의 보험 플랜에 대해 수십억 건의 거래를 처리하고 있으며, 심도 있는 시스템 통합을 통해 고객 유지율을 높이고 있습니다. 전반적으로, 미국의 헬스케어 BPO 시장에서는 단순한 인력 차익 거래가 아닌, 전문 지식과 확장성이 뛰어난 기술을 융합한 업체들이 계속해서 우위를 점하고 있습니다.

오프쇼어 서비스는 2025년 지출의 81.35%를 차지했으며, 이는 인도와 필리핀 전역의 HIPAA 준수 센터에 대한 20년에 걸친 공급업체의 투자를 반영한 것입니다. 그러나 인건비 격차 축소와 관세로 인한 하드웨어 가격 급등으로 인해 성장은 니어쇼어 거점으로 이동하고 있으며, 미국의 의료 BPO 시장 규모는 급속히 확대될 전망입니다. 니어쇼어 거점에서는 동일한 시간대 내에서 당일 지원이 가능하여, 보험사, 의료 제공업체 및 BPO 팀 간의 협업 지연을 줄여줍니다. 2024년 2월의 정보 유출 사건을 계기로 해외 거점의 사이버 보안 대책에 대한 감시가 강화되었으며, 보험사들은 현재 감사의 용이성과 실시간 사고 대응을 중시하여 지리적 근접성을 우선시하고 있습니다.

면허를 소지한 간호사나 의료 제공업체와의 직접적인 소통이 필요한 고도로 복잡한 임상 서비스의 경우, 국내에서의 제공이 여전히 필수적입니다. 옵텀은 온쇼어에서의 임상 감독과 오프쇼어에서의 거래 처리를 결합하여 품질과 비용의 균형을 맞추고 있습니다. 코그니전트나 젠팩트와 같은 대형 오프쇼어 기업들은 니어쇼어 거점 설립을 서두르고 있지만, 멕시코와 콜롬비아에 대한 설비 투자로 인해 단기적으로는 이익률이 압박받을 것으로 보입니다. 온쇼어에서의 감독, 니어쇼어에서의 실행, 오프쇼어에서의 대량 처리를 통합하는 하이브리드형 제공 모델이 표준으로 자리 잡아가고 있으며, 벤더들은 플랫폼 통합 및 실시간 워크플로 관리에 대한 투자를 서두르고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.19According to Mordor Intelligence, the united states healthcare bPO market size is expected to grow from USD 154.36 billion in 2025 to USD 165.05 billion in 2026 and is forecast to reach USD 245.46 billion by 2031 at 8.26% CAGR over 2026-2031.

This report is Segmented by Service Type (Payer Service [Claims Management and More], Provider Service [Patient Care Service and More] and More), Delivery Model (Onshore, Nearshore, Offshore), Service Delivery Mode (Captive, Third-Party, Hybrid), and End Customer (Payers, Providers, Pharmaceutical & Biotech, Government Agencies). The Market Forecasts are Provided in Terms of Value (USD).

United States Healthcare BPO Market Trends and Insights

Escalating Administrative-Cost Pressure on Payers & Providers

Hospitals spend USD 19.7 billion each year disputing denied claims, with 2025 denial rates ranging from 11.8% to 19%, pushing CFOs to outsource revenue-cycle tasks to variable-fee partners that can cut fixed labor and improve cash collections. National health expenditure reached USD 4.9 trillion in 2023 and is projected to rise at 5.8% annually through 2033, magnifying workloads related to eligibility verification, prior authorization, and claims adjudication. Commercial reimbursement growth continues to lag medical-cost inflation by 150-200 basis points, squeezing provider margins and making non-clinical outsourcing unavoidable. Nearly half of rural hospitals posted operating losses in 2023-2024, and more than 600 facilities remain at high financial risk, so revenue-cycle BPO is becoming a lifeline for sustaining patient services. Payers face similar pressure as medical loss ratios hover near regulatory ceilings; nine of the 10 largest U.S. health plans already rely on Conduent for claims and member operations.

Advanced Tech Adoption (AI, RPA, Analytics) Unlocking Scale Efficiencies

Generative-AI is collapsing review cycle times and staff hours across prior authorization, appeals, and utilization-management workflows. HCLTech showed that its GenAI solution can cut clinical-review time from three hours to 20 minutes and reduce costs by 30% for a regional Blue Cross plan. A 1-million-member insurer typically spends USD 50-70 million on clinical-review labor and maintains 200-300 nurse FTEs; GenAI-powered extraction and summarization now let nurses validate decisions instead of gathering documents, shrinking staffing needs. Optum Real, rolled out in April 2024, enables instant coverage validation, and early pilots at Allina Health recorded lower administrative errors and better patient experience. Cognizant's BPaaS platform blends RPA and machine learning to deliver 25-50% reductions in total cost of ownership, while EmblemHealth reported a 99% improvement in claims-first-pass yield after deployment. IBM Consulting says biopharma clients now close regulatory documentation cycles 50-75% faster by using generative AI for content-heavy workflows.

Cyber-Security & Data-Privacy Concerns Post-Breach

The Change Healthcare ransomware attack disrupted claims for thousands of providers, exposed nearly 200 million records, and triggered a reassessment of vendor cyber-risk protocols. A 2024 JAMA study counted 566 breaches affecting 170 million records, with ransomware responsible for 69% of compromised data. HHS's Office for Civil Rights issued HIPAA settlements totaling USD 875,000 in 2024 alone, underscoring rising enforcement. Payers now require vendors to hold SOC 2 Type II attestations, independent penetration tests, and high-limit cyber-insurance, raising the cost of entry for small offshore suppliers. Conduent's January 2025 security incident heightened concerns and spotlighted the need for transparent incident-response playbooks. Several states are considering legislation mandating minimum cybersecurity standards for healthcare BPO vendors, which would further favor large providers with mature security operations.

Other drivers and restraints analyzed in the detailed report include:

- Heightening Regulatory Complexity

- Surge in BPaaS Adoption by Small & Mid-Size Payers

- Shrinking Offshore Cost Arbitrage Amid Tariffs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Pharmaceutical Services accounted for 58.62% of United States healthcare BPO market share in 2025, anchored by clinical-trial management, regulatory documentation, and manufacturing quality assurance as sponsors accelerate drug-development timelines. IQVIA logged USD 15.4 billion in 2024 revenue and carried a USD 32 billion backlog, illustrating unrelenting demand for contract-research capacity. FDA guidance on decentralized clinical trials released in September 2024 expands the outsourcing remit to remote monitoring and home-health components, driving new use cases. Provider Services, however, are projected to grow fastest at a 12.73% CAGR between 2026-2031 as hospitals battle denial rates of up to 19% and rising cost-to-collect, pushing them toward full-service revenue-cycle partners. The United States healthcare BPO market size for provider-oriented deals is set to accelerate sharply as health systems seek end-to-end claims, coding, and patient-financial-engagement solutions.

Pharma outsourcing continues to diversify beyond clinical research into supply-chain logistics, batch-record reviews, and omnichannel sales enablement, responding to stricter 21 CFR Part 11 data-integrity enforcement. Manufacturing-support BPO is particularly attractive for small biotech firms that lack validated quality-assurance systems. Conversely, Payer Services remain a stable mid-market niche where entrenched relationships between national insurers and platform-centric vendors constrain churn. Cognizant's TriZetto alone handles billions of transactions for 650 plans, reinforcing stickiness through deep system integration. Overall, the United States healthcare BPO market continues to reward vendors that marry domain expertise with scalable technology rather than pure labor arbitrage.

Offshore Delivery commanded 81.35% of 2025 spending, reflecting two decades of vendor investment in HIPAA-ready centers across India and the Philippines. Yet erosion in labor-cost differentials and tariff-driven hardware inflation are tilting growth toward nearshore locations, where the United States healthcare BPO market size is poised to expand swiftly. Nearshore centers offer same-day time-zone support, lowering hand-off latency between payers, providers, and BPO teams. The February 2024 breach intensified scrutiny of offshore cybersecurity controls, and payers now favor proximity for easier audits and real-time incident response.

Onshore Delivery remains essential for high-complexity clinical services that require licensed nurses and direct provider interaction. Optum blends onshore clinical oversight with offshore transaction processing to balance quality and cost. Offshore majors like Cognizant and Genpact are racing to establish nearshore hubs, yet capital investments in Mexico and Colombia will dampen margins in the short term. Hybrid delivery models that orchestrate onshore oversight, nearshore execution, and offshore bulk processing are becoming the norm, forcing vendors to invest in platform orchestration and real-time workflow management.

List of Companies Covered in this Report:

- Accenture

- Capgemini

- Cognizant

- Conduent

- EXL Service Holdings

- Firstsource Solutions

- GeBBs Healthcare Solutions

- Genpact

- HCL Technologies

- Hinduja Global Solutions (HGS)

- IBM

- IQVIA

- Omega Healthcare

- OutsourceRCM

- Parexel International

- R1 RCM

- Sutherland Healthcare Solutions

- Tata Consultancy Services (TCS)

- United Health Group

- Wipro

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating Administrative-Cost Pressure on Payers & Providers

- 4.2.2 Advanced Tech Adoption (AI, RPA, Analytics) Unlocking Scale Efficiencies

- 4.2.3 Heightening Regulatory Complexity

- 4.2.4 Surge In BPaaS Adoption by Small & Mid-Size Regional Payers

- 4.2.5 Medicaid Redetermination Backlog Driving Eligibility-Processing Demand

- 4.2.6 Generative-AI Prior-Auth & Coding Accelerating Revenue-Cycle Outsourcing

- 4.3 Market Restraints

- 4.3.1 Cyber-Security & Data-Privacy Concerns Post High-Profile Breaches

- 4.3.2 Shrinking Offshore Cost Arbitrage Amid Rising On-Shore Labor Costs

- 4.3.3 U.S. Tariffs Inflating Imported It Hardware for Offshore Delivery Centers

- 4.3.4 Vendor Consolidation Increasing Lock-In Risk for Mid-Tier Clients

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value - USD)

- 5.1 By Service Type

- 5.1.1 Payer Service

- 5.1.1.1 Human Resource Management

- 5.1.1.2 Claims Management

- 5.1.1.3 Customer Relationship Management (CRM)

- 5.1.1.4 Operational / Administrative Management

- 5.1.1.5 Care Management

- 5.1.1.6 Provider Management

- 5.1.1.7 Other Payer Services

- 5.1.2 Provider Service

- 5.1.2.1 Patient Enrollment & Strategic Planning

- 5.1.2.2 Patient Care Service

- 5.1.2.3 Revenue Cycle Management (RCM)

- 5.1.3 Pharmaceutical Service

- 5.1.3.1 Research & Development Support

- 5.1.3.2 Manufacturing Support

- 5.1.3.3 Non-clinical Services

- 5.1.3.3.1 Supply Chain & Logistics

- 5.1.3.3.2 Sales & Marketing Support

- 5.1.3.3.3 Other Non-clinical Services

- 5.1.1 Payer Service

- 5.2 By Delivery Model

- 5.2.1 Onshore Delivery

- 5.2.2 Nearshore Delivery

- 5.2.3 Offshore Delivery

- 5.3 By Service Delivery Mode

- 5.3.1 Captive (In-house) Centers

- 5.3.2 Third-Party Outsourcing

- 5.3.3 Hybrid / Co-sourcing

- 5.4 By End Customer

- 5.4.1 Healthcare Payers (Insurers & PBMs)

- 5.4.2 Healthcare Providers (Hospitals, Physician Groups)

- 5.4.3 Pharmaceutical & Biotech Companies

- 5.4.4 Government Agencies

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1 Accenture PLC

- 6.3.2 Capgemini

- 6.3.3 Cognizant

- 6.3.4 Conduent

- 6.3.5 EXL Service Holdings

- 6.3.6 Firstsource Solutions

- 6.3.7 GeBBS Healthcare Solutions

- 6.3.8 Genpact Limited

- 6.3.9 HCL Technologies

- 6.3.10 Hinduja Global Solutions (HGS)

- 6.3.11 IBM Corporation

- 6.3.12 IQVIA

- 6.3.13 Omega Healthcare

- 6.3.14 OutsourceRCM

- 6.3.15 Parexel International

- 6.3.16 R1 RCM

- 6.3.17 Sutherland Healthcare Solutions

- 6.3.18 Tata Consultancy Services (TCS)

- 6.3.19 UnitedHealth Group

- 6.3.20 Wipro

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment