|

시장보고서

상품코드

2061644

전신 홍반성 루푸스 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Systemic Lupus Erythematosus - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

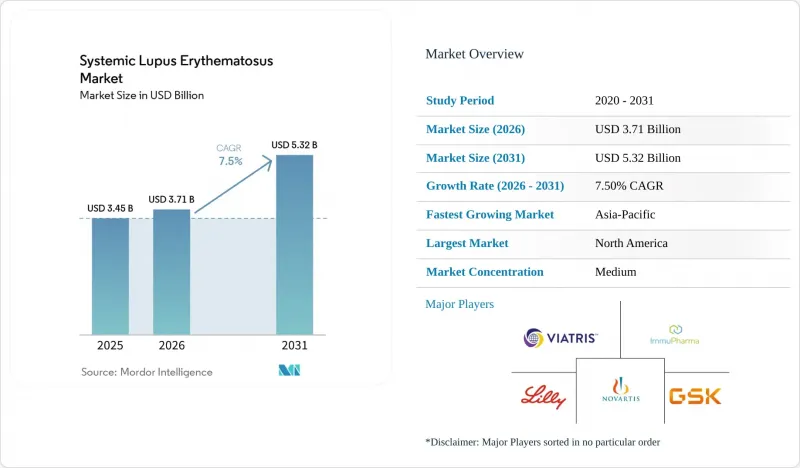

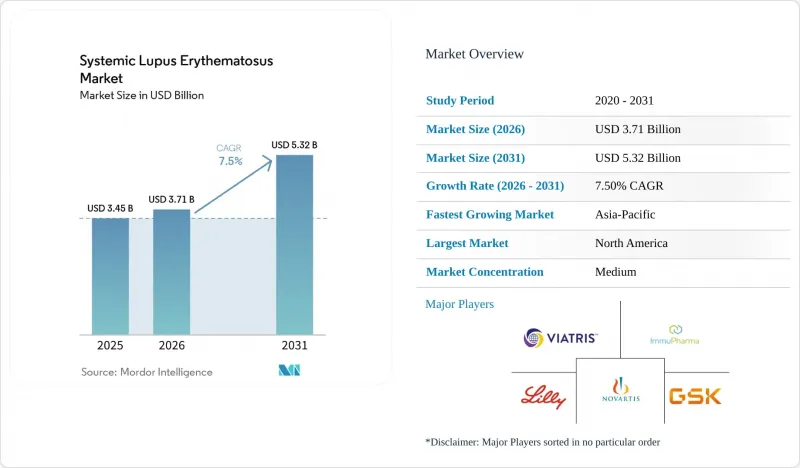

Mordor Intelligence에 의하면, 전신 홍반성 루푸스 시장 규모는 2025년 34억 5,000만 달러로 평가되었습니다. 2026년에는 37억 1,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR은 7.5%를 나타내, 2031년에는 53억 2,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 제품 카테고리(진단약 및 치료제), 투여 경로(경구, 정맥 내, 피하), 최종 사용자(병원, 전문 클리닉 등) 및 지역(북미, 유럽 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 전신 홍반성 루푸스 시장 동향 및 인사이트

SLE 유병률 증가와 조기 진단

최근 데이터에 따르면, 전신 홍반성 루푸스(SLE)의 유병률은 태국에서 10만 명당 85.8명, 카탈루냐에서 10만 명당 92.3명, 스웨덴에서 10만 명당 71.5명인 것으로 나타났습니다. 1차 진료 현장에서 항이중가닥 DNA 및 항스미스 항체 검사의 도입이 증가함에 따라, 전문의에게 의뢰되는 사례가 늘어났고, 증상 발현부터 류마티스과에서의 확정 진단까지 걸리는 시간이 단축되었습니다. 보험사가 1차 선택 생물학적 제제의 승인을 위해 검사를 통한 확정 진단을 요구하고 있기 때문에 검사 건수는 인구 증가율보다 빠른 속도로 증가하고 있습니다. 미국에서는 발병률이 10만 명당 연간 5.1명으로 안정적으로 유지되고 있지만, 고위험 인종 집단의 인구 구성 변화로 인해 절대적인 환자 수가 증가하고 있습니다. 이러한 유병률의 꾸준한 상승은 고도의 치료가 필요한 환자 수를 늘림으로써 SLE 시장을 확대시키고 있습니다.

신규 생물학적 제제의 신속한 승인

2026년 4월, 미국 FDA는 피하 투여형 아니플로맙을 승인하여 1회 투여 비용을 22% 절감하는 동시에 재택 치료를 가능하게 했습니다. 오비누츠주맙에 대한 생물학적 제제 추가 승인 신청에 대해서는 2026년 12월까지 결정을 내리는 것을 목표로 하고 있습니다. 이러한 승인에 더해, 글락소스미스클라인(GSK)이 2024년에 소아용 베리무맙 자동 주사기의 승인을 획득한 것은 규제 당국이 ‘퍼스트 인 클래스’의 혁신성을 우선시하기보다는 약물 전달 방식의 간소화에 중점을 두고 있음을 보여줍니다. 유럽의약품청(EMA)에 동시 신청함으로써 해당 지역에서의 출시 기간이 단축되어, 미국에서의 최초 승인 후 18개월 이내에 SLE 시장에서의 점유율이 더욱 확대될 전망입니다.

바이오의약품의 높은 비용과 제한된 보험 적용

미국에서는 베리뮐맙의 연간 가격이 3만 5,000달러 가까이 책정되어 있으며, 아니플로맙은 4만 달러에 육박하고 있습니다. 이러한 가격 책정은 많은 신흥 시장의 가구 소득 중위값을 상회하고 있습니다. 중국에서는 보험 급여로 인해 본인 부담금이 줄어들었지만, 성별 격차로 인해 농촌 지역에서는 여전히 큰 경제적 부담을 겪고 있습니다. 유럽의 보험사들은 1년 이상의 보장 대상이 되기 위해 지속적인 관해의 증거를 요구하고 있으며, 이로 인해 광범위한 도입이 지연되고 있습니다. 게다가, 많은 약제가 전신 홍반성 루푸스(SLE)에 대해 여전히 적응증 외 사용 상태이기 때문에 바이오시밀러 개발 기업들은 기존 생물학적 제제에 도전하는 것을 주저하고 있으며, 그 결과 오리지널 제품의 독점 기간이 연장되고 있습니다. 이로 인해 코르티코스테로이드와 하이드록시클로로퀸이 주류를 이루는 분절된 치료 환경이 조성되어, SLE 시장에서 신약의 단기적인 수익 창출 가능성이 제한되고 있습니다.

부문별 분석

2025년, 진단 분야는 전신 홍반성 루푸스 시장의 37.66%를 차지했습니다. 이는 참조 검사 기관이 보험자로부터 부여받은 역할을 수행하게 되었기 때문입니다. 보체 활성화 및 인터페론 시그니처를 평가하는 다중 마커 패널은 현재 고가의 생물학적 제제의 적합성을 판단하는 기준으로 자리 잡고 있으며, 2031년까지 연평균 성장률(CAGR) 8.45%를 나타낼 것으로 전망됩니다. 수익은 주로 24시간 이내에 결과를 제공할 수 있게 해주는 자동 분석 장치 덕분에, 효소 결합 플랫폼을 활용한 면역 분석법에 의해 주도되고 있습니다. 이에 이어 보체 분해 산물 검사, 단백뇨 검사, 영상 진단 등의 보조적 검사법이 있으며, 이 모든 검사는 예후를 정밀하게 파악하고 장기 손상을 발견하는 데 기여하고 있습니다.

경제적 인센티브도 높아지고 있습니다. 전문 클리닉에서는 검사와 원격 의료 상담을 패키지로 제공함으로써 추가적인 수익원을 창출하고 있습니다. 한편, 대규모 병원 네트워크는 증가하는 검체량을 처리하기 위해 민간 검사 기관과 합작 사업을 전개하고 있습니다. 의료 시스템이 생물학적 제제에 대한 접근성과 검사를 통해 확인된 재발 위험을 연계함에 따라, 검사 단가가 소폭 상승하는 데 그치더라도 진단 분야가 전신 홍반성 루푸스 시장을 점점 더 주도하고 있습니다.

지역별 분석

2025년, 북미는 전신 홍반성 루푸스 시장의 39.34%라는 큰 점유율을 차지했습니다. 이는 고가의 생물학적 제제에 대한 메디케어의 지원과 바이오마커 요건의 도입이 주된 원동력이 되고 있습니다. 아시아태평양에서는 중국의 지방 차원에서의 보험 급여 확대와 일본의 소아용 의약품 승인으로 인해, 2031년까지 연평균 성장률(CAGR)이 8.25%를 나타낼 것으로 전망됩니다. 인도에서는 루푸스 환자의 가족 중 36.2%가 여전히 막대한 의료비 부담에 직면해 있지만, 민간 보험 가입률 증가와 의료 관광의 확대로 인해 치료 접근성은 점차 개선되고 있습니다.

유럽의 전망은 복잡합니다. 유럽의약품청(EMA)의 일원화된 승인은 제약사에게 절차를 간소화해 주지만, 각국의 의료기술평가(HTA)에 따른 예산상의 제약으로 인해 약제의 보험 적용 시작이 최대 18개월 지연될 가능성이 있습니다. 중동에서는 각국 정부가 수입 의존도를 낮추기 위해 국내 단일클론 항체 생산 시설에 대한 투자를 확대하고 있으며, 아랍에미리트(UAE)는 2027년 가동을 목표로 하는 신규 시설 건설을 계획하고 있습니다. 남미에서는 공적 의료보험 제도로 인한 접근 제한이 지속되는 가운데, 브라질과 아르헨티나가 민간 보험을 통한 보장 확대를 통해 지역 성장을 주도하고 있습니다. 이러한 지역별 동향은 전신 홍반성 루푸스 시장에서 성장이 집중되고 있는 분야를 드러내는 동시에, 여전히 미충족 의료 수요가 남아 있는 지역을 부각시키고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.19According to Mordor Intelligence, the systemic lupus erythematosus market size is expected to grow from USD 3.45 billion in 2025 to USD 3.71 billion in 2026 and is forecast to reach USD 5.32 billion by 2031 at 7.5% CAGR over 2026-2031.

This report is Segmented by Product Category (Diagnostics and Therapeutics), Route of Administration (Oral, Intravenous, Subcutaneous), End User (Hospitals, Specialty Clinics, and More), and Geography (North America, Europe, and More). Market Forecasts are Provided in Terms of Value (USD).

Global Systemic Lupus Erythematosus Market Trends and Insights

Rising Prevalence of SLE & Earlier Diagnosis

Recent data indicates prevalence rates of systemic lupus erythematosus (SLE) at 85.8 per 100,000 in Thailand, 92.3 per 100,000 in Catalonia, and 71.5 per 100,000 in Sweden. Increased adoption of anti-double-stranded DNA and anti-Smith testing in primary care settings has accelerated referrals, reducing delays between symptom onset and rheumatology confirmation. With payers requiring laboratory confirmation for first-line biologic approvals, test volumes are growing faster than population rates. In the United States, while the incidence has stabilized at 5.1 per 100,000 person-years, demographic shifts toward higher-risk ethnic groups are driving an increase in absolute case numbers. This steady rise in prevalence is expanding the SLE market by increasing the number of patients eligible for advanced treatments.

Rapid Approvals of Novel Biologics

In April 2026, the U.S. FDA approved subcutaneous anifrolumab, reducing per-dose administration costs by 22% and enabling home-based care. A supplemental biologics license application for obinutuzumab is targeting a decision by December 2026. These approvals, combined with GlaxoSmithKline's 2024 authorization of a pediatric belimumab autoinjector, highlight a regulatory focus on simplifying drug delivery rather than prioritizing first-in-class innovations. Simultaneous filings with the European Medicines Agency are shortening regional launch timelines, driving broader SLE market penetration within 18 months of initial U.S. approval.

High Costs of Biologics & Limited Reimbursement

In the U.S., belimumab is priced at nearly USD 35,000 annually, while anifrolumab approaches the USD 40,000 mark. Such pricing exceeds median household earnings in many emerging markets. In China, while reimbursements have reduced copayments, disparities across provinces leave rural communities facing significant financial burdens. European insurers require evidence of sustained remission for coverage beyond a year, delaying broader adoption. Additionally, biosimilar developers are hesitant to challenge established biologics, as many agents remain off-label for systemic lupus erythematosus (SLE), extending the exclusivity period for originators. This has resulted in a segmented treatment landscape where corticosteroids and hydroxychloroquine dominate, limiting short-term revenue potential for newer agents in the SLE market.

Other drivers and restraints analyzed in the detailed report include:

- Adoption of Advanced Autoantibody Panels

- Growth in Healthcare Spending in Emerging Markets

- Safety Concerns with Chronic Immunosuppression

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, diagnostics captured 37.66% of the systemic lupus erythematosus market share, as reference labs took on roles mandated by payers. Multi-marker panels, which assess complement activation and interferon signatures, now determine eligibility for premium biologics, forecasting an 8.45% CAGR through 2031. Revenue is predominantly driven by immunoassays utilizing enzyme-linked platforms, thanks to automated analyzers ensuring a 24-hour turnaround. Following closely are adjunct modalities like complement split-product testing, urinalysis for proteinuria, and imaging, all refining prognosis and detecting organ threats.

Financial incentives are on the rise: specialist clinics bundle testing with telehealth consultations, tapping into additional reimbursement streams. Meanwhile, large hospital networks are entering joint ventures with commercial labs to handle elevated sample volumes. As health systems synchronize biologic access with test-verified flare risks, diagnostics increasingly dominate the systemic lupus erythematosus market, even with only modest hikes in per-test prices.

Geography Analysis

In 2025, North America captured a significant 39.34% share of the systemic lupus erythematosus market, driven by Medicare support for high-cost biologics and the implementation of biomarker requirements. In the Asia-Pacific region, an 8.25% CAGR through 2031 is attributed to expanded provincial reimbursements in China and pediatric drug approvals in Japan. Although 36.2% of lupus families in India still face catastrophic healthcare expenses, increasing private insurance adoption and growing medical tourism are gradually improving access to treatments.

Europe presents a mixed outlook: centralized EMA approvals simplify processes for manufacturers, but national health-technology assessments impose budgetary restrictions, delaying drug formulary entries by up to 18 months. In the Middle East, governments are investing in domestic monoclonal-antibody production facilities to reduce import dependency, with the United Arab Emirates planning a new facility set to commence operations in 2027. In South America, Brazil and Argentina drive regional growth through private-sector coverage, even as public healthcare systems continue to ration access. These regional dynamics highlight areas of concentrated growth within the systemic lupus erythematosus market while emphasizing regions where unmet needs persist.

- Abbvie

- Amgen

- AstraZeneca

- Biogen

- Bristol-Myers Squibb

- Eli Lilly and Company

- Euroimmun Medizinische Labordiagnostika GmbH

- Exagen

- Roche

- GlaxoSmithKline

- Johnson & Johnson

- Merck

- Novartis

- PerkinElmer Inc. (Diagnostics)

- Pfizer

- Quest Diagnostics

- Sanofi

- Siemens Healthineers

- Thermo Fisher Scientific

- UCB

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of SLE & Earlier Diagnosis

- 4.2.2 FDA Approvals of Novel Biologics

- 4.2.3 Adoption of Advanced Autoantibody Panels

- 4.2.4 Growth In Healthcare Spending in Emerging Markets

- 4.2.5 AI-Driven Multi-Omics Flare-Prediction Tools

- 4.2.6 Venture-Backed Tolerogenic Cell Therapies

- 4.3 Market Restraints

- 4.3.1 High Cost of Biologics & Limited Reimbursement

- 4.3.2 Safety Concerns Over Chronic Immunosuppression

- 4.3.3 Diagnostic Heterogeneity; Lack of Gold-Standard Test

- 4.3.4 Regulatory Scrutiny on Porcine-Derived Antigens

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Category

- 5.1.1 Diagnostics

- 5.1.1.1 Immunoassays

- 5.1.1.2 Complement Tests

- 5.1.1.3 Urinalysis

- 5.1.1.4 Imaging

- 5.1.1.5 Others

- 5.1.2 Therapeutics

- 5.1.2.1 B-Cell Inhibitors

- 5.1.2.2 T-Cell Inhibitors

- 5.1.2.3 Cytokine Inhibitors

- 5.1.2.4 Immunosuppressants

- 5.1.2.5 Corticosteroids

- 5.1.2.6 Others

- 5.1.1 Diagnostics

- 5.2 By Route of Administration

- 5.2.1 Oral

- 5.2.2 Intravenous

- 5.2.3 Subcutaneous

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Specialty Clinics

- 5.3.3 Diagnostic Laboratories

- 5.3.4 Home-care Settings

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 AbbVie Inc.

- 6.3.2 Amgen Inc.

- 6.3.3 AstraZeneca plc

- 6.3.4 Biogen Inc.

- 6.3.5 Bristol Myers Squibb Company

- 6.3.6 Eli Lilly & Company

- 6.3.7 Euroimmun Medizinische Labordiagnostika GmbH

- 6.3.8 Exagen Inc.

- 6.3.9 F. Hoffmann-La Roche Ltd

- 6.3.10 GSK plc

- 6.3.11 Johnson & Johnson (Janssen)

- 6.3.12 Merck & Co., Inc.

- 6.3.13 Novartis AG

- 6.3.14 PerkinElmer Inc. (Diagnostics)

- 6.3.15 Pfizer Inc.

- 6.3.16 Quest Diagnostics Incorporated

- 6.3.17 Sanofi S.A.

- 6.3.18 Siemens Healthineers AG

- 6.3.19 Thermo Fisher Scientific Inc.

- 6.3.20 UCB S.A.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment