|

시장보고서

상품코드

2061755

북미의 IT 디바이스 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)North America IT Device - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

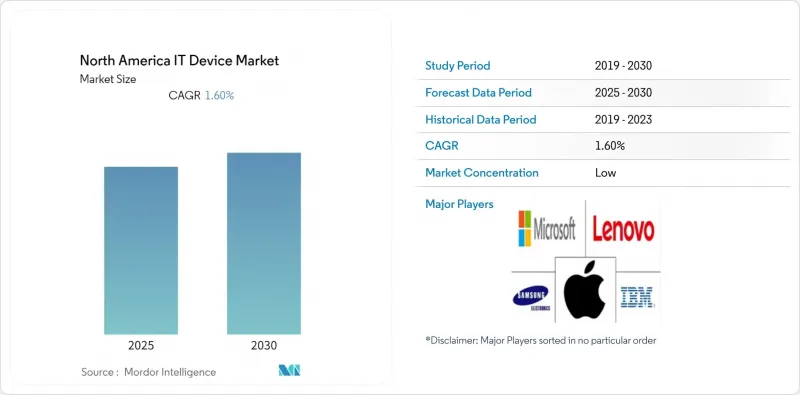

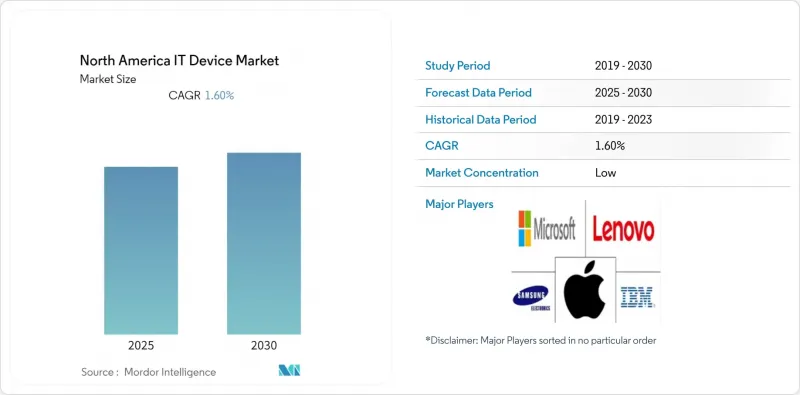

Mordor Intelligence에 의하면, 북미의 IT 디바이스 시장 규모는 2026년 8,018억 5,000만 달러에서 2031년까지 1조 1,141억 7,000만 달러에 이를 것으로 예측됩니다. 2026년부터 2031년에 걸쳐 CAGR은 6.8%를 나타낼 전망입니다.

본 보고서는 기기 유형(데스크톱 PC, 노트북, 태블릿 등), 최종 사용자 산업(일반 소비자, 중소기업, 대기업, 교육 기관 등), 연결 방식(유선 기기, 무선 기기), 유통 채널(온라인 소매, 오프라인 소매, B2B 직접 판매 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

북미의 IT 디바이스 시장 동향과 인사이트

하이브리드 근무용 하드웨어에 대한 수요 급증

하이브리드 근무 방식이 정착되면서, 팬데믹 당시의 급증기를 지나 노트북, 모니터, 웹캠 구매가 지속적으로 증가하고 있습니다. 베스트바이(Best Buy)는 2026 회계연도 3분기 보고서에서 컴퓨팅 및 모바일 제품이 국내 매출의 49%를 차지했으며, 전년 동기 대비 비교 가능 매출이 7.6% 증가했다고 밝혔습니다. 델 테크놀로지스와 HP는 모두 기업용 PC의 미결제 주문 잔고가 증가하고 있음을 강조하고 있으며, 기업들이 PC 교체 주기를 5년에서 3년으로 단축하고 있는 것을 배경으로, 교체 주기의 단축이 두드러지고 있습니다. 수요가 가장 높은 곳은 미국과 캐나다로, 지식 근로자의 재택근무 보급률은 40%를 넘습니다. 반면, 멕시코는 인프라의 제약으로 인해 뒤처지고 있습니다. 그 결과, 신경망 처리 장치(NPU)를 탑재한 프리미엄 노트북의 판매량이 증가하고 있으며, 로컬에서의 AI 추론 및 데이터 주권 관련 규정을 준수하고 있습니다. 그 결과, 북미의 IT 디바이스 시장에서는 기업용 SKU의 평균 판매 가격 상승이 기여하여, 보급형 소비자용 PC의 부진을 일부 상쇄하고 있습니다.

Windows 10 지원 종료에 따른 전사적 기기 교체

마이크로소프트는 2025년 10월 14일에 Windows 10에 대한 지원을 종료했으며, 이는 Windows 7 지원 종료 이후 최대 규모의 기업용 PC 교체 주기를 촉발했습니다. HP 및 Dell의 볼륨 라이선싱 계약에 따라, 현재 Qualcomm Snapdragon X Elite 또는 Intel Core Ultra 프로세서를 탑재하고 각각 전용 AI 엔진을 내장한 Copilot+PC에 Windows 11 Pro가 번들로 제공됩니다. 레노버의 ThinkPad X1 Carbon Gen 13은 이러한 추세를 상징하는 제품으로, 인텔 칩과 CES 2025에서 발표된 기기 내 음성 인식 에이전트를 결합하고 있습니다. 미국, 캐나다 각 주 및 멕시코 자회사의 공공 부문 조달에서 사이버 보안 규정 준수를 위해 보류되었던 예산이 집행되고 있으며, 그 영향은 2026년부터 2027년에 걸쳐 집중될 전망입니다. 그 결과, 북미의 IT 디바이스 시장에서는 수요가 앞당겨지면서 단기적인 수익은 증가하겠지만, 향후 경기 사이클이 장기화될 가능성이 있습니다.

반도체 공급 불균형이 지속되고 있습니다.

표면적인 공급 제약은 완화되었지만, 고대역폭 메모리나 첨단 로직 노드 분야에서는 구조적인 부족 현상이 계속되고 있습니다. 삼성은 AI 서버 수요 증가로 인한 공급 부족을 이유로, 2025년 1분기 DDR5 가격을 최대 60% 인상할 것이라고 발표했습니다. 마이크론도 메모리 부족 현상이 2027년까지 지속될 것이라는 견해를 밝히며, 이에 따라 소비자용 PC용 생산 능력을 다른 용도로 전환할 것이라고 밝혔습니다. 2024년 12월 및 2025년 1월에 미국 산업안보국(BIS)이 발표한 수출 규제로 인해, 중국 반도체 공장에 대한 제조 장비 공급이 더욱 제한되면서 전 세계 웨이퍼 생산 능력 확대가 정체되고 있습니다. 그 결과 발생하는 리드타임의 변동은 북미 전역의 기기 제조업체들의 생산 계획을 복잡하게 만들고, 북미의 IT 디바이스 시장의 예상 성장률을 끌어내리고 있습니다.

부문별 분석

웨어러블 기기는 2025년에는 미미한 시장 점유율에 그쳤으나, 2031년까지 높은 연평균 성장률(CAGR)을 기록하며 성장할 것으로 예상되며, 모든 IT 디바이스 부문 중 가장 빠르게 성장하는 카테고리가 될 전망입니다. 2026년 초에 발표된 최신 FDA 지침에 따라, 저위험 건강 추적 기기에 대한 규제 장벽이 완화되어 보급 가속화의 길이 열렸습니다. 심전도(ECG) 및 혈중 산소 포화도(SpO2) 센서 등 첨단 기능을 탑재한 가민(Garmin)의 ‘Fenix 8’은 운동선수와 구급대원 모두를 대상으로 하여, 틈새 시장이면서도 매우 중요한 시장의 요구를 충족시키고 있습니다. 또한, 애보트, 메드트로닉, 덱스콤 등의 기업이 제공하는 지속형 혈당 모니터는 스마트폰 연동 기능을 통합하여, 더욱 긴밀하게 상호 연결된 데이터 생태계를 구축하고 있습니다. 이러한 발전은 혁신과 규제 측면의 지원에 힘입어, 더 광범위한 IT 디바이스 시장에서 웨어러블 기기의 중요성이 커지고 있음을 여실히 보여주고 있습니다.

스마트폰은 북미의 IT 디바이스 시장에서 여전히 가장 큰 비중을 차지하고 있지만, 시장 침투율이 포화 상태에 이르러 성장세가 둔화되고 있습니다. 반면, 노트북과 데스크톱 PC는 기능성과 매력을 높여주는 엣지 AI 업그레이드의 힘입어 점진적인 성장을 이루고 있습니다. 서버와 스토리지 장치는 시게이트의 대용량 30TB ‘Exos M’ 드라이브가 보여주듯이, AI 워크로드 수요에 부응하기 위해 저장 밀도를 높이고 있습니다. 주변 기기는 하이브리드 근무 환경으로 인한 지속적인 수요의 혜택을 계속 누리고 있는 반면, POS 단말기와 산업용 핸드헬드 기기는 ‘기타 기기’ 카테고리에서 여전히 중요한 구성 요소로 자리 잡고 있습니다. 이러한 변화들은 전반적으로 기업과 소비자 양측의 진화하는 요구를 반영하며, 지속적인 분석 서비스를 뒷받침하는 데이터 생성형 하드웨어로의 광범위한 시장 전환을 여실히 보여주고 있습니다.

의료 분야는 2026년부터 2031년까지 연평균 성장률(CAGR) 10.6%를 나타낼 것으로 예측되며, 여전히 가장 큰 비중을 차지하는 소비자 부문을 웃돌 것으로 전망됩니다. 병원에서는 병상 옆에서 차트를 작성하기 위한 내구성이 뛰어난 태블릿과 원격 환자 모니터링을 위한 웨어러블 모니터를 도입하는 움직임이 가속화되고 있으며, HIPAA의 보호 조치 하에 전자의무기록과의 원활한 통합이 보장되고 있습니다. 미국과 캐나다의 고령화 및 만성 질환 유병률 증가가 지속적인 모니터링 솔루션에 대한 수요를 이끌고 있습니다. 또한, 중소기업은 비용 효율이 높은 노트북을 선택하는 반면, 대기업은 업무 효율과 데이터 보안을 강화하기 위해 제로 트러스트 보안 콘솔을 통해 관리되는 AI 지원 PC의 표준화를 추진하고 있습니다.

교육 분야에서는 캐나다 각 주에서 제공하는 디지털 학습 지원금을 바탕으로 크롬북과 아이패드에 대한 수요가 계속해서 견조한 모습을 보이고 있습니다. 미국 정부 기관들은 다년 계약인 GSA 스케줄을 활용하고 있으며, 캐나다에서도 유사한 계약을 통해 IT 디바이스의 교체가 진행되고 있습니다. BFSI(은행 및 금융 및 보험) 부문에서는 규정 준수 및 업무 민첩성을 확보하기 위해, 실시간 부정 분석에 대응할 수 있도록 워크스테이션 교체 작업이 진행되고 있습니다. 한편, 제조업 및 에너지 업계에서는 가혹한 환경에 맞추어 설계된 견고한 PC가 도입되어 특정 업무 요구 사항을 충족하고 있습니다. 이러한 동향은 전반적으로 업계 고유의 요건과 기술 발전에 힘입어 북미의 IT 디바이스 시장 수요 추세가 변화하고 있음을 여실히 보여주고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.19According to Mordor Intelligence, the north america iT device market size is expected to increase from USD 801.85 billion in 2026 to reach USD 1,114.17 billion by 2031, growing at a CAGR of 6.8% over 2026-2031.

This report is Segmented by Device Category (Desktop PCs, Laptop PCs, Tablets, and More), End User Industry (Consumer, Small and Medium Enterprises, Large Enterprises, Education Sector, and More), Connectivity (Wired Devices, and Wireless Devices), Distribution Channel (Online Retail, Offline Retail, Direct B2B Sales, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America IT Device Market Trends and Insights

Surging Demand for Hybrid Work Hardware

Hybrid work remains entrenched, propelling sustained purchases of laptops, monitors, and webcams beyond the pandemic spike. Best Buy disclosed that computing and mobile products generated 49% of domestic revenue in its third fiscal-quarter 2026 report, with comparable sales up 7.6% year-on-year. Dell Technologies and HP both emphasized growing commercial PC pipelines, underscoring condensed refresh cycles as enterprises step down from five-year to three-year replacement intervals. Demand is strongest in the United States and Canada, where remote work penetration tops 40% of knowledge workers, while Mexico lags because of infrastructure limits. The resulting uplift accelerates unit volumes across premium notebooks equipped with neural processing units, ensuring local AI inference and compliance with data-sovereignty mandates. Consequently, the North America IT device market benefits from higher average selling prices on commercial SKUs, partially offsetting softness in entry-level consumer PCs.

Enterprise-Wide Device Refresh Post-Windows 10 End-of-Life

Microsoft withdrew Windows 10 support on 14 October 2025, triggering the largest enterprise PC replacement cycle since the Windows 7 sunset. Volume-licensing agreements from HP and Dell now bundle Windows 11 Pro with Copilot+ PCs based on Qualcomm Snapdragon X Elite or Intel Core Ultra processors, each embedding dedicated AI engines. Lenovo's ThinkPad X1 Carbon Gen 13 exemplifies the trend, pairing Intel silicon with on-device transcription agents unveiled at CES 2025. Public-sector procurement in the United States, Canadian provinces, and Mexican subsidiaries is releasing deferred budgets to ensure cybersecurity compliance, concentrating the impact in 2026-2027. As a result, the North America IT device market is experiencing front-loaded demand that lifts near-term revenues but may elongate future cycles.

Persistent Semiconductor Supply Imbalances

Structural shortages persist in high-bandwidth memory and advanced logic nodes despite easing headline constraints. Samsung announced DDR5 price hikes of up to 60% for 1Q 2025, citing tight supply linked to AI server demand. Micron echoed that memory scarcity will extend through 2027, diverting capacity away from consumer PCs. Export-control rules issued by the U.S. Bureau of Industry and Security in December 2024 and January 2025 further limit equipment access for Chinese fabs, stalling global wafer additions. Resulting lead-time volatility complicates production planning for device makers across North America, trimming projected growth in the North America IT device market.

Other drivers and restraints analyzed in the detailed report include:

- Accelerated 5G Roll-Outs Fueling Smartphone Upgrades

- Edge-AI Integration into Laptops and PCs

- Inflation-Driven Price Sensitivity Among Consumers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Wearables contributed a modest share in 2025 yet are projected to expand at a strong compound annual growth rate through 2031, making it the fastest-growing category among all IT device segments. Recent FDA guidance issued in early 2026 has eased regulatory barriers for low-risk health trackers, paving the way for accelerated adoption. Garmin's Fenix 8, equipped with advanced features like ECG and SpO2 sensors, caters to both athletes and first responders, addressing niche yet critical market needs. Additionally, continuous glucose monitors from companies such as Abbott, Medtronic, and Dexcom are integrating smartphone connectivity, creating deeper and more interconnected data ecosystems. These advancements highlight the growing importance of wearables in the broader IT device market, driven by innovation and regulatory support.

Smartphones, while remaining the largest segment of the North America IT device market, are experiencing a slowdown in growth as market penetration reaches saturation. In contrast, laptops and desktops are seeing incremental growth fueled by edge-AI upgrades, which enhance their functionality and appeal. Servers and storage devices are scaling up in density to meet the demands of AI workloads, as demonstrated by Seagate's high-capacity 30-TB Exos M drives. Peripherals continue to benefit from sustained demand driven by hybrid work environments, while point-of-sale terminals and industrial handheld devices remain critical components of the "other devices" category. Collectively, these shifts underscore a broader market pivot toward data-generating hardware that supports recurring analytics services, reflecting the evolving needs of businesses and consumers alike.

Healthcare is forecast to post a 10.6% CAGR between 2026 and 2031, outstripping the consumer segment that nevertheless retains the largest share. Hospitals are increasingly deploying rugged tablets for bedside charting and wearable monitors for remote patient surveillance, ensuring seamless integration with electronic health records under HIPAA safeguards. The aging population and rising prevalence of chronic diseases in the United States and Canada are driving the demand for continuous monitoring solutions. Additionally, small and medium enterprises are opting for cost-effective laptops, while large enterprises are standardizing AI-ready PCs managed through zero-trust security consoles to enhance operational efficiency and data security.

Education continues to see steady demand for Chromebooks and iPads, supported by digital-learning grants from Canadian provinces. Government agencies in the United States leverage multi-year GSA schedules, while similar contracts in Canada are enabling the modernization of IT device fleets. The BFSI sector is refreshing workstations to support real-time fraud analytics, ensuring compliance and operational agility. Meanwhile, manufacturing and energy verticals are adopting ruggedized PCs designed for harsh environments, addressing specific operational needs. These trends collectively highlight the evolving demand dynamics within the North America IT device market, driven by sector-specific requirements and technological advancements.

List of Companies Covered in this Report:

- Apple Inc.

- Samsung Electronics Co., Ltd.

- Dell Technologies Inc.

- HP Inc.

- Lenovo Group Limited

- ASUSTeK Computer Inc.

- Acer Inc.

- Microsoft Corporation

- Huawei Technologies Co., Ltd.

- Xiaomi Corporation

- LG Electronics Inc.

- Sony Group Corporation

- Panasonic Holdings Corporation

- Garmin Ltd.

- Zebra Technologies Corporation

- Fujitsu Limited

- Seagate Technology Holdings plc

- Western Digital Corporation

- Toshiba Electronic Devices and Storage Corporation

- Hisense Visual Technology Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Demand for Hybrid Work Hardware

- 4.2.2 Enterprise-wide Device Refresh Cycles Post-Windows 10 End-of-Life

- 4.2.3 Accelerated 5G Roll-outs Fueling Smartphone Upgrades

- 4.2.4 Tax Incentives on Domestic Semiconductor Assembly in Mexico

- 4.2.5 Growing Adoption of XR-Ready Wearables for Training

- 4.2.6 Edge-AI Integration into Laptops and PCs

- 4.3 Market Restraints

- 4.3.1 Persistent Semiconductor Supply Imbalances

- 4.3.2 Inflation-Driven Price Sensitivity Among Consumers

- 4.3.3 Tightened U.S.-China Export Controls on Advanced Chips

- 4.3.4 Escalating E-waste Regulatory Compliance Costs

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Device Category

- 5.1.1 Desktop PCs

- 5.1.2 Laptop PCs

- 5.1.3 Tablets

- 5.1.4 Smartphones

- 5.1.5 Servers and Storage Systems

- 5.1.6 Wearable Devices

- 5.1.7 Peripheral Devices (Keyboards, Mice)

- 5.1.8 Other Device Categories

- 5.2 By End User Industry

- 5.2.1 Consumer

- 5.2.2 Small and Medium Enterprises

- 5.2.3 Large Enterprises

- 5.2.4 Education Sector

- 5.2.5 Government and Public Sector

- 5.2.6 Healthcare Sector

- 5.2.7 Retail and E-Commerce

- 5.2.8 BFSI

- 5.2.9 Other End User Industries

- 5.3 By Connectivity

- 5.3.1 Wired Devices

- 5.3.2 Wireless Devices

- 5.4 By Distribution Channel

- 5.4.1 Online Retail

- 5.4.2 Offline Retail

- 5.4.3 Direct B2B Sales

- 5.4.4 Value-Added Resellers

- 5.4.5 Telecom Carrier Stores

- 5.5 By Country

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Apple Inc.

- 6.4.2 Samsung Electronics Co., Ltd.

- 6.4.3 Dell Technologies Inc.

- 6.4.4 HP Inc.

- 6.4.5 Lenovo Group Limited

- 6.4.6 ASUSTeK Computer Inc.

- 6.4.7 Acer Inc.

- 6.4.8 Microsoft Corporation

- 6.4.9 Huawei Technologies Co., Ltd.

- 6.4.10 Xiaomi Corporation

- 6.4.11 LG Electronics Inc.

- 6.4.12 Sony Group Corporation

- 6.4.13 Panasonic Holdings Corporation

- 6.4.14 Garmin Ltd.

- 6.4.15 Zebra Technologies Corporation

- 6.4.16 Fujitsu Limited

- 6.4.17 Seagate Technology Holdings plc

- 6.4.18 Western Digital Corporation

- 6.4.19 Toshiba Electronic Devices and Storage Corporation

- 6.4.20 Hisense Visual Technology Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment