|

시장보고서

상품코드

2061846

베이커리 가공 장비 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Bakery Processing Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

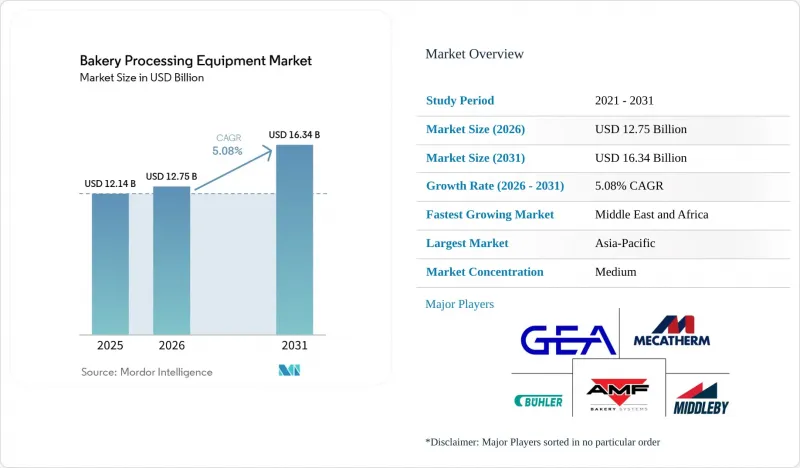

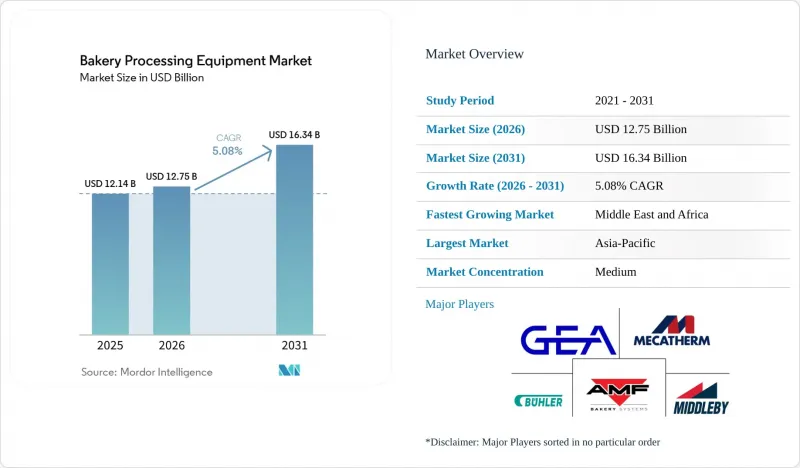

Mordor Intelligence에 의하면, 베이커리 가공 장비 시장 규모는 2025년 121억 4,000만 달러로 평가되었습니다. 2026년에는 127억 5,000만 달러로 확대되어 2031년까지 163억 4,000만 달러에 이를 것으로 예측됩니다. 2026년부터 2031년에 걸쳐 CAGR은 5.08%를 나타낼 전망입니다.

본 보고서는 장비 유형(믹서 및 블렌더, 분할·둥글리기 기계, 성형·시트 기계, 오븐 및 발효기, 기타), 용도(빵, 케이크 및 페이스트리, 쿠키 및 비스킷, 피자 크러스트, 기타), 지역(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 베이커리 가공 장비 시장 동향과 인사이트

세계적으로 장인 정신이 깃든 특제 베이커리 제품에 대한 수요가 증가하고 있습니다.

독립적인 구역 제어 기능을 갖춘 데크 오븐이나 반죽을 부드럽게 다루는 성형기가 현재 설계 요건의 최전선에 서 있습니다. 이를 통해 수분 함량이 높고 발효 시간이 긴 반죽에서도 기포 구조를 유지할 수 있게 되며, 이는 장인의 손으로 빵을 굽는 과정에서 바람직한 식감과 풍미를 구현하는 데 필수적입니다. 또한, 소비자의 6%가 집이나 매장에서 빵류 제품을 구매하는 것을 선호함에 따라, 적응성이 높고 효율적인 가공 장비에 대한 수요가 점점 더 두드러지고 있습니다. 오븐 및 발효기 시장공급업체들은 금형을 교체할 필요 없이 차바타에서 포카차로 생산을 전환할 수 있는 유연한 생산 라인에 대한 수요가 급증하고 있음을 목격하고 있습니다. 이를 통해 업무 효율이 향상되고 가동 중단 시간이 줄어듭니다. 2025년 IBIE 조사에 따르면, 북미 제빵사의 64%가 향후 24개월 이내에 특화 생산 라인에 대한 예산을 편성할 계획이라고 답했으며, 특히 고대 곡물에 대한 소비자의 관심과 그 건강 효과에 대한 기대를 배경으로, 스펠트 밀과 엔콘 밀의 가공 능력에 중점을 두고 있습니다. 비용에 민감한 아시아태평양에서는 이러한 추세가 다소 완만하지만, 상하이와 뭄바이의 부티크 체인들은 건강 지향적 및 프리미엄 지향적 소비자로 구성된 확대되는 틈새 시장에 점차 대응해 나가면서, 약 5년 정도의 시차는 있지만 이미 유럽과 미국 수요 패턴에 발맞추고 있습니다.

자동화의 발전과 위생 설계 기준

FSMA, NSF/ANSI 169, EHEDG 등의 규정에서는 식품 가공 및 제조 과정에서 엄격한 위생 및 안전 기준을 준수하기 위해 위생적인 외장, 공구 없이 분해 가능한 구조, CIP 회로의 설치를 의무화하고 있습니다. 미들비(Middleby)나 VMI와 같은 공급업체들은 세척 시간을 40% 단축하고 위생 관리 주기를 디지털로 기록하는 믹서나 오븐을 적극 홍보하고 있으며, 이를 통해 감사 부담이 줄어들고 업무 효율이 향상됩니다. 내장형 센서와 스마트 HMI를 통해 운영자는 인건비를 60% 절감할 수 있으며, 12-18개월 이내에 투자 비용을 회수할 수 있습니다. 임금 상승률이 자금 조달 비용을 상회하는 현 상황에서 이는 특히 매력적이며, 자동화가 비용 대비 효과가 높은 해결책이 되고 있습니다. 한편, 소규모 사업자들은 자금 부족을 극복하기 위해 계절별로 상환이 가능한 리스 계약을 채택하고 있어, 막대한 초기 투자 없이도 첨단 설비를 도입할 수 있게 되었습니다.

첨단 생산 라인에 대한 대규모 설비 투자

턴키 방식의 베이커리를 설립하려면 현재 200만-500만 달러의 투자가 필요합니다. 이 과제는 9-12개월에 달하는 리드타임과 2024년 이전 평균보다 200-300베이시스포인트 높은 자금 조달 비용으로 인해 더욱 심각해지고 있습니다. 이러한 비용 상승과 기간 연장은 시장에 새로 진입하려는 기업들에게 큰 장벽이 되고 있습니다. 예산이 빠듯한 상황에서 신규 진출기업들은 유럽산 중고 기계에 관심을 기울이고 있으며, 최대 70% 할인된 가격에 구입하고 있습니다. 이러한 접근 방식은 초기 설비 투자를 줄일 수 있지만, 많은 경우 업무 효율 저하를 초래하고 있습니다. 게다가 재생 기기에 대한 의존은 사업의 확장성을 제한하고 있으며, 이로 인해 이들 기업이 기존 시장 선도 기업들과 경쟁하는 데 어려움을 겪고 있습니다. 이러한 선택으로 인해 자동화의 전면적인 도입이 미뤄지고 있으며, 이러한 추세는 특히 라틴아메리카와 동남아시아에서 두드러지게 나타나고 있습니다. 자동화 도입의 지연은 해당 지역의 생산성과 증가하는 소비자 수요에 대응하는 능력에 더욱 부정적인 영향을 미치고 있습니다.

부문별 분석

2025년에는 오븐 및 발효기가 열처리 장비 시장 전체 매출에서 32.56%라는 압도적인 점유율을 차지했습니다. 이러한 경쟁력은 데크식, 랙식, 터널식, 스파이럴식, 하이브리드 연료 시스템 등 각각 다른 처리 능력과 배합 요구 사항에 맞추어 설계된 다양한 제품 라인업에 의해 뒷받침되고 있습니다. 이러한 시스템은 제빵 생산에 필수적이며, 이 부문의 견조한 수요를 뒷받침하고 있습니다. 또한 하이브리드 연료식 터널, 열회수 모듈, 신속한 벨트 교체 시스템과 같은 혁신 기술은 업무 효율을 높일 뿐만 아니라 비용 절감에도 기여하여, 설비의 업그레이드 주기를 지속시키고 있습니다. 중국의 OEM 제조업체들이 가하는 가격 압박이 있는 반면, 안목이 높은 프리미엄층 구매자들은 수명 주기 비용, 신뢰성, 사후 서비스를 중시하며 확고한 태도를 유지하고 있습니다.

성형기 및 시트 성형기는 급속히 성장하고 있으며, 2031년까지 14%의 시장 점유율을 차지할 것으로 전망됩니다. 이러한 급속한 성장은 크루아상이나 페이스트리 등 층이 있는 제과류의 산업 규모 생산 확대에 힘입은 바가 큽니다. 2031년까지의 연평균 성장률(CAGR)은 5.08%로 예측되며, 이 부문의 성장은 대량 생산을 하는 제빵 업계에서 해당 기술이 널리 도입되고 있음을 보여줍니다. 특히 대규모 시설이나 수출 지향적인 시설에서 원단 처리 과정의 자동화 및 균일화를 위한 노력이 이러한 확장을 주도하고 있습니다. 또한, 정밀 성형 기술의 발전과 연속 생산 라인과의 원활한 통합이 도입을 가속화하고 있습니다. 제빵 기기 제조업체들이 층상 제품의 라인업을 확대함에 따라, 최첨단 성형 및 시트 성형 설비에 대한 투자 열기는 더욱 고조될 전망입니다.

지역별 분석

2025년에는 중국, 인도 및 다양한 아세안(ASEAN) 국가들의 신규 생산 능력 확대에 힘입어 아시아태평양이 매출 점유율의 39.53%를 차지하며 선두 자리를 유지했습니다. 국내 OEM 제조업체는 가격 면에서 우위를 점하고 있어, 지역 제빵업체들이 더 신속하게 투자 회수를 실현할 수 있도록 지원하고 있지만, 레시피의 정확성이나 가동 시간이 매우 중요한 경우에는 여전히 고가의 수입 제품이 선호되고 있습니다. 도시화의 진전과 포장된 제빵 제품에 대한 수요 증가가 2·3선 도시의 설비 투자를 견인하고 있습니다. 또한, 식품 가공 인프라를 지원하는 정부의 인센티브 덕분에 첨단 제빵 기술의 도입이 가속화되고 있습니다. 지역 기업들도 제품의 균일성을 높이고 숙련된 노동자에 대한 의존도를 낮추기 위해 자동화를 점점 더 많이 도입하고 있습니다.

중동 및 아프리카에서는 연평균 성장률(CAGR) 7.02%라는 견실한 성장이 예상됩니다. 사우디아라비아에서는 정부계 펀드의 투자를 통해 주 식량인 빵의 현지 생산에 주력하고 있는 반면, 이집트의 생산자들은 북아프리카 슈퍼마켓 수요를 충족시키기 위해 생산량을 5배로 늘리고 있습니다. 소매 체인의 확대와 현대적인 판매 형태의 보급으로 인해, 표준화된 대량 생산형 제빵 솔루션에 대한 수요가 증가하고 있습니다. 만안 국가들의 식량 안보 프로그램에 대한 투자는 현지 생산 능력을 더욱 강화하고 있습니다. 또한, 유럽의 장비 공급업체와의 제휴를 통해 지역 제조업체들은 기술력을 향상시킬 수 있게 되었습니다. 인구 증가와 도시 지역의 소비 패턴 변화는 장기적인 시장 성장을 지속적으로 뒷받침하고 있습니다.

또한 시장 점유율이 높은 유럽과 북미에서는 생산 능력 확대에서 설비 갱신 투자로 초점을 전환하고 있습니다. 이러한 변화는 주로 엄격한 위생 및 에너지 규제에 의해 주도되고 있습니다. 각 제조업체는 엄격한 배기가스 규제 및 식품 안전 기준을 충족하기 위해 설비 업그레이드를 최우선으로 하고 있습니다. IoT 기반 감시 시스템을 포함한 디지털화 도입은 설비 조달 시 의사결정의 중요한 요소로 자리 잡고 있습니다. 기존 생산 라인에 에너지 절약 부품을 도입함으로써, 제과점은 운영 비용을 효율적으로 관리할 수 있게 되었습니다. 게다가 인력 부족으로 인해 자동화 및 원격 진단 도입이 가속화되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.19According to Mordor Intelligence, the bakery processing equipment market size is expected to increase from USD 12.14 billion in 2025 to USD 12.75 billion in 2026 and reach USD 16.34 billion by 2031, growing at a 5.08% CAGR over 2026-2031.

This report is Segmented by Equipment Type (Mixers and Blenders, Dividers and Rounders, Molders and Sheeters, Ovens and Proofers, Others), Application (Bread, Cakes and Pastries, Cookies and Biscuits, Pizza Crusts, Others), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). Market Forecasts are Provided in Terms of Value (USD).

Global Bakery Processing Equipment Market Trends and Insights

Rising global demand for artisanal and specialty bakery products

Independent zone-control deck ovens and gentle-handling molders are now at the forefront of design briefs, allowing for high-hydration, long-fermentation doughs that maintain their gas-cell structure, which is critical for achieving desired texture and flavor profiles in artisanal baking. Moreover, as 6% of consumers shift their preferences towards bakery purchases, whether at home or in-store, the demand for adaptable and efficient processing equipment becomes increasingly evident. Suppliers in the ovens and proofers market are witnessing a surge in demand for flexible lines, capable of transitioning from ciabatta to focaccia without the need for tooling swaps, thereby enhancing operational efficiency and reducing downtime. An IBIE survey from 2025 highlighted that 64% of North American bakers are allocating budgets for specialty lines within the next 24 months, with a particular focus on spelt and einkorn capabilities, driven by consumer interest in ancient grains and their perceived health benefits. While this trend is muted in the cost-sensitive Asia-Pacific region, boutique chains in Shanghai and Mumbai are already aligning with Western demand patterns, albeit with a five-year delay, as they gradually cater to a growing niche of health-conscious and premium-seeking consumers.

Increased automation and hygienic-design standards

Protocols like FSMA, NSF/ANSI 169, and EHEDG mandate sanitary enclosures, tool-free disassembly, and CIP circuits to ensure compliance with stringent hygiene and safety standards in food processing and manufacturing. Vendors, including Middleby and VMI, tout mixers and ovens that slash cleaning time by 40% and digitally log sanitation cycles, lightening the audit load and improving operational efficiency. With embedded sensors and smart HMIs, operators enjoy a 60% reduction in labor costs and a return on investment within 12 to 18 months. This is especially appealing as wage inflation surpasses financing expenses, making automation a cost-effective solution. Meanwhile, smaller operators are turning to leasing structures with seasonal repayments to navigate the capital gap, enabling them to adopt advanced equipment without significant upfront investment.

High capital expenditure for advanced equipment lines

Turnkey bakeries now demand an investment of USD 2-5 million. This challenge is intensified by lead times stretching 9-12 months and financing costs that are 200-300 basis points higher than averages seen before 2024. These higher costs and extended timelines have created significant barriers for new players in the market. With tighter budgets, new entrants are leaning towards refurbished European machinery, snagging them at discounts of up to 70%. This approach allows them to reduce initial capital expenditure but often comes at the expense of operational efficiency. Additionally, the reliance on refurbished equipment limits the scalability of operations, making it harder for these players to compete with established market leaders. This choice has led to a postponement in fully adopting automation, a trend particularly evident in Latin America and Southeast Asia. The delayed automation adoption further impacts productivity and the ability to meet growing consumer demand in these regions.

Other drivers and restraints analyzed in the detailed report include:

- Energy-efficient equipment adoption amid sustainability mandates

- Expansion of industrial-scale bakeries in emerging asia-pacific markets

- Skilled-labor shortage and steep learning curve

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, ovens and proofers are set to command a dominant 32.56% share of the thermal-processing equipment market's total revenue. Their supremacy is bolstered by a diverse product lineup, featuring deck, rack, tunnel, spiral, and hybrid fuel systems, each tailored for distinct throughput and formulation needs. These systems are indispensable in bakery production, underscoring the segment's robust demand. Furthermore, innovations like hybrid-fuel tunnels, heat-recovery modules, and rapid belt-change systems not only boost operational efficiency but also curtail costs, perpetuating a cycle of equipment upgrades. While Chinese OEMs exert pricing pressures, discerning premium buyers remain steadfast, emphasizing lifecycle costs, reliability, and after-sales service.

Molders and sheeters are on a rapid ascent, eyeing a 14% market share by 2031. This surge is fueled by the rising industrial-scale production of laminated delicacies like croissants and pastries. Anticipating a CAGR of 5.08% until 2031, the segment's growth is a testament to its adoption in high-volume bakery operations. The push for automation and uniformity in dough handling, especially in large-scale and export-focused facilities, drives this expansion. Moreover, advancements in precision forming and seamless integration with continuous production lines are hastening the adoption. As bakery producers broaden their laminated offerings, the momentum for investing in cutting-edge molding and sheeting equipment is poised to escalate.

Geography Analysis

In 2025, the Asia-Pacific region is projected to hold a leading 39.53% revenue share, driven by the development of greenfield capacities in China, India, and various ASEAN nations. Domestic OEMs offer price advantages that enable local bakers to achieve faster returns on investment, although premium imports remain preferred in scenarios where recipe precision and uptime are critical. The rise in urbanization and increasing demand for packaged bakery products are driving equipment investments in tier-2 and tier-3 cities. Additionally, government incentives supporting food processing infrastructure are accelerating the adoption of advanced baking technologies. Regional players are also increasingly adopting automation to enhance consistency and reduce reliance on skilled labor.

The Middle East and Africa are expected to record a strong 7.02% CAGR. In Saudi Arabia, sovereign wealth investments are focused on localizing staple bread production, while Egyptian producers are increasing output fivefold to meet the needs of North African supermarkets. Expanding retail chains and modern trade formats are boosting demand for standardized, high-volume baking solutions. Investments in food security programs across Gulf nations are further strengthening local production capabilities. Partnerships with European equipment suppliers are also enabling regional manufacturers to upgrade their technological capabilities. Population growth and evolving urban consumption patterns continue to support long-term market growth.

Europe and North America, which together account for a significant market share, are shifting their focus from capacity expansion to replacement spending. This shift is primarily driven by stringent hygiene and energy regulations. Manufacturers are prioritizing equipment upgrades to meet strict emissions and food safety standards. The adoption of digitalization, including IoT-enabled monitoring systems, is becoming a key factor in equipment procurement decisions. Retrofitting existing production lines with energy-efficient components is helping bakeries manage operational costs. Furthermore, labor shortages are accelerating the adoption of automation and remote diagnostics.

- GEA Group Aktiengesellschaft

- Buhler Holding AG

- John Bean Technologies Corporation

- The Middleby Corporation (Baker Perkins)

- Ali Group S.r.l. (Rondo)

- AMF Bakery Systems (a Markel Food Group Company)

- Mecatherm S.A.

- Rademaker B.V.

- WP Bakery Group GmbH

- Koenig Maschinen GmbH

- European Pastry & Bakery Machinery (EBAK)

- Reading Bakery Systems (a Markel Food Group Company)

- Revent International AB

- Shaffer Mixing

- Zeppelin Systems GmbH

- Oshikiri Machinery Ltd.

- VMI SA (VMI Group)

- Sigma S.r.l.

- Rheon Automatic Machinery Co., Ltd.

- Gemini Bakery Equipment Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising global demand for artisanal and specialty bakery products

- 4.2.2 Increased automation and hygienic-design standards

- 4.2.3 Energy-efficient equipment adoption amid sustainability mandates

- 4.2.4 Expansion of industrial-scale bakeries in emerging Asia-Pacific markets

- 4.2.5 IoT-enabled predictive maintenance reducing unplanned downtime

- 4.2.6 Specialized equipment for gluten-free and alt-grain formulations

- 4.3 Market Restraints

- 4.3.1 High capital expenditure for advanced equipment lines

- 4.3.2 Skilled-labor shortage and steep learning curve

- 4.3.3 Electronic-component supply-chain fragility

- 4.3.4 Prospective carbon-border taxes inflating lifecycle costs

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Equipment Type

- 5.1.1 Mixers and Blenders

- 5.1.2 Dividers and Rounder

- 5.1.3 Molders and Sheeters

- 5.1.4 Ovens and Proofers

- 5.1.5 Others

- 5.2 By Application

- 5.2.1 Bread

- 5.2.2 Cakes and Pastries

- 5.2.3 Cookies and Biscuits

- 5.2.4 Pizza Crusts

- 5.2.5 Others

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 Italy

- 5.3.2.4 France

- 5.3.2.5 Spain

- 5.3.2.6 Netherlands

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 South Africa

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 United Arab Emirates

- 5.3.5.4 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 GEA Group Aktiengesellschaft

- 6.4.2 Buhler Holding AG

- 6.4.3 John Bean Technologies Corporation

- 6.4.4 The Middleby Corporation (Baker Perkins)

- 6.4.5 Ali Group S.r.l. (Rondo)

- 6.4.6 AMF Bakery Systems (a Markel Food Group Company)

- 6.4.7 Mecatherm S.A.

- 6.4.8 Rademaker B.V.

- 6.4.9 WP Bakery Group GmbH

- 6.4.10 Koenig Maschinen GmbH

- 6.4.11 European Pastry & Bakery Machinery (EBAK)

- 6.4.12 Reading Bakery Systems (a Markel Food Group Company)

- 6.4.13 Revent International AB

- 6.4.14 Shaffer Mixing

- 6.4.15 Zeppelin Systems GmbH

- 6.4.16 Oshikiri Machinery Ltd.

- 6.4.17 VMI SA (VMI Group)

- 6.4.18 Sigma S.r.l.

- 6.4.19 Rheon Automatic Machinery Co., Ltd.

- 6.4.20 Gemini Bakery Equipment Company