|

시장보고서

상품코드

2062027

나노 산화 아연 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Nano Zinc Oxide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

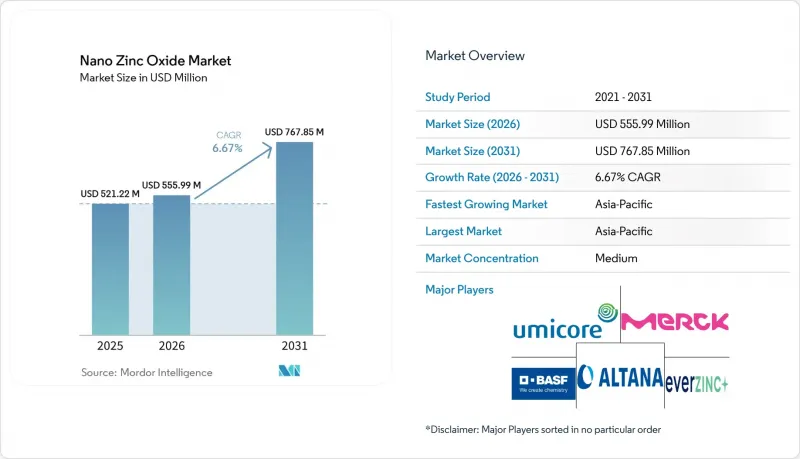

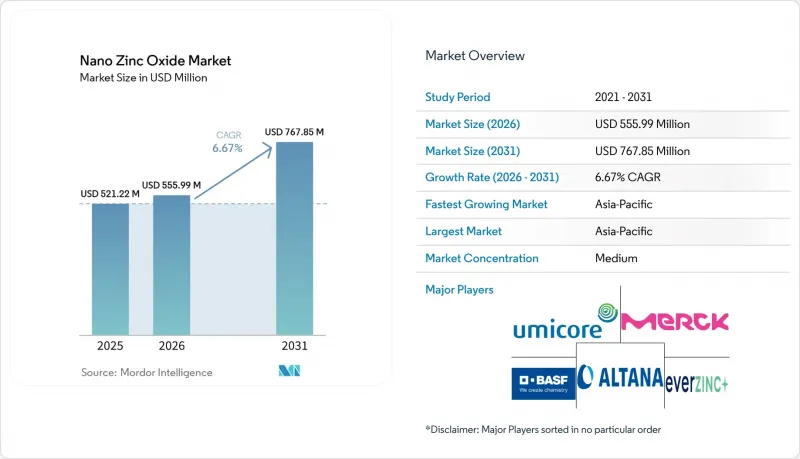

Mordor Intelligence에 의하면, 나노 산화 아연 시장 규모는 2025년 5억 2,122만 달러로 평가되었고, 2026년 5억 5,599만 달러로 추정되고, 2031년까지 7억 6,785만 달러로 확대될 전망이며, 2026-2031년 CAGR 6.67%를 나타낼 것으로 예측됩니다.

본 보고서는 유형별(코팅 나노 산화아연 및 비코팅 나노 산화아연), 형태별(분말 및 분산액, 슬러리), 용도별(퍼스널케어 및 화장품, 페인트 및 코팅, 전자, 섬유, 고무 및 플라스틱, 의약품, 기타), 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 나노 산화 아연 시장 동향 및 분석

자외선 차단제에서 비나노 TiO2 대체재에 대한 규제 동향

이산화티타늄에 대한 모니터링이 강화됨에 따라, 자외선 차단제 혁신의 방향성이 바뀌었습니다. 소비자안전과학위원회(SCCS)는 2024년에 나노 TiO₂에 대한 심사를 강화했으며, 이에 따라 제제 개발자들은 100nm 기준을 약간 상회하는 산화 아연을 우선적으로 선택하게 되었습니다. 이를 통해 투명성을 유지하면서도 나노 표기를 피할 수 있게 되었습니다. 동시에, 미국 식품의약국(FDA)의 미해결 모노그래프로 인해 12가지 유형의 유기 필터가 불확실한 상태에 놓여 있는 반면, 산화 아연은 카테고리 I 지위를 유지하고 있어 안전항(safe harbor)으로서의 우위가 강화되고 있습니다. Solesence 등 공급업체들은 알루미늄 산화물 및 오르가노실란 쉘을 적용함으로써 백탁 현상을 최소화하면서도 높은 SPF를 구현하고 있으며, 이러한 성능은 호주 TGA의 현지 승인을 통해 입증되었습니다. 2025년 5월 SCCS가 4-메틸벤질리덴캄퍼의 사용 금지를 결정한 이후, 시장의 문의가 급증하면서 산화 아연은 전 세계적으로 조화를 이룬 몇 안 되는 자외선 차단제 중 하나로 그 입지를 확고히 다졌습니다. 이러한 규제 동향에 따라, 선진국 시장에서 프리미엄 자외선 차단제 출시와 관련하여 광물성 유효 성분이 계속해서 최전선에 위치할 것으로 예측됩니다.

Mini-LED/마이크로 LED 백플레인의 전자기기 분야에서의 활용 확대

디스플레이 제조업체들은 비용 효율이 뛰어난 투명 전도체로 알루미늄 또는 갈륨을 도핑한 산화아연으로의 전환을 추진하고 있습니다. 2024년 발표된 동료 심사 논문에 따르면, 원자층 증착법(ALD)으로 형성된 AZO 박막은 10Ω/sq 미만의 표면 저항과 85%를 초과하는 가시광 투과율을 달성하여, 4K 및 8K 패널의 사양을 충족합니다. 일본과 한국에서는 이러한 필름을 고급 TV에 적용하여, 2025년에는 200만 대 이상을 출하했습니다. 중국 내 미니 LED 백라이트 생산 능력의 급속한 확대는 지역 내 수요를 더욱 부추기고 있습니다. 산화아연은 저온에서 용액 공정이 가능하기 때문에 연성 웨어러블 전자 기기에도 적합하며, 마이크로 LED 아키텍처가 상업적으로 보급됨에 따라 나노 산화아연 시장은 지속적인 성장이 예상됩니다.

기상염 분사 합성 방식의 높은 설비 투자 비용(CAPEX)과 운영 비용(OPEX)

연간 1만 톤의 생산 능력을 갖춘 프레임 스프레이 공장을 건설하려면 반응기, 집진 장치, 공해 방지 설비에 400만-700만 달러가 필요합니다. 천연가스 연소 및 배기가스 정화에 따른 톤당 800-1,200달러의 운영 비용은 특히 2025년에 EU 탄소배출권 가격이 톤당 80유로(약 93.20달러)를 넘어설 것으로 예상되는 상황에서 유럽 및 미국 기업들의 이익률을 압박하고 있습니다. 시범 규모의 수열 프로젝트는 비용 경쟁력을 확보했으나, 핵생성 반응 속도의 문제로 인해 규모 확대에 어려움을 겪고 있습니다. 연속 수열 처리 기술이 성숙기에 도달하기 전까지는 공공요금이 저렴한 중국 생산자들이 구조적인 비용 우위를 유지함으로써 나노 산화아연 시장 전체의 가격 형성을 억제하게 될 것입니다.

부문별 분석

코팅 처리된 제품은 광촉매 작용을 저감하고 자외선 차단제에서 눈에 띄지 않는 마감을 구현하는 표면 처리 기술을 통해, 2025년에는 나노 산화 아연 시장 점유율의 62.21%를 차지했습니다. 1kg당 2-5달러의 추가 비용은 소비자의 미적 감각과 산호초의 안전성을 중시하는 퍼스널케어 브랜드들이 부담하고 있습니다. 코팅되지 않은 제품 시장 점유율은 작지만, 약물 전달 기술 개발자들이 최적의 세포 내 취인을 위해 무결한 표면을 필요로 하기 때문에 연평균 성장률(CAGR) 6.88%로 시장을 주도할 것으로 전망됩니다. 2024년에 발표된 의약품 검사 결과에 따르면, 코팅되지 않은 나노입자의 생체이용률은 60%인 반면, 코팅된 제품은 35-40%에 그치는 것으로 나타났습니다. 규제상의 미묘한 차이가 매우 중요합니다. 코팅된 등급의 경우, 대개 별도의 EU REACH(화학물질의 등록, 평가, 허가 및 제한) 관련 서류가 필요하기 때문에 신규 시장 진출기업에게는 진입 장벽이 됩니다. Advance ZincTek은 REACH 및 TGA(치료용 의약품국) 규정 준수를 위해 초기 단계부터 투자해 왔으며, 유럽의 4-MBC 금지 조치 이후 급증할 수요에 대비해 체제를 갖추고 있습니다.

부수적인 영향으로는 코팅 관련 지적재산권(IP) 포트폴리오를 보유한 기업에 대한 경쟁적 보호가 있습니다. Solesence는 10건의 미국 특허와 100건 이상의 해외 출원을 보유하고 있으며, 이러한 독점권을 바탕으로 BASF와 장기 공급 계약을 협상하고 있습니다. 소비자 브랜드들이 투명성을 추구하며 공급망을 통합하는 가운데, 코팅 제품 부문은 나노 산화아연 시장의 가격 기준이 될 것으로 보이며, 반면 코팅되지 않은 제품의 성장은 수익성이 높은 의약품 유통 채널을 개척하는 계기가 될 것입니다.

지역별 분석

아시아태평양은 2025년 매출의 48.11%를 차지했으며, 예측 기간(2026-2031년) 동안 연평균 성장률(CAGR) 7.74%를 나타낼 것으로 전망됩니다. 이는 중국의 저비용 프레임 스프레이 공장과 일본의 전자제품 수요에 힘입은 결과입니다. Huzheng이나 SAT NANO와 같은 중국 공급업체들은 범용 분말을 1.50-2.13달러/kg에 판매하고 있으며, 이는 유럽 및 미국의 가격보다 최대 40% 낮은 수준입니다. 품질 편차로 인해 고부가가치 의약품 등급 시장으로의 진출이 제한되고 있어, 일본과 호주의 기업들이 프리미엄 틈새 시장을 공략하고 있습니다. PLI 제도 하에서 인도에서 일어나고 있는 화장품 붐과 루바민(Rubamin)을 통한 연간 5만 톤의 생산 능력 확대는 나노 산화아연 시장의 역학에 대한 남아시아의 부상하는 영향력을 강화하고 있습니다.

2025년 북미 시장 점유율은 클린 뷰티에 대한 선호도와 전기차 인프라에 대한 투자에 힘입어 상승했습니다. 솔레센스(Soresense)는 2024년에 5,230만 달러의 매출을 기록했으며, 이 중 85%가 완성된 소비자용 제품이 차지하여 브랜드 최전선에서 창출되는 가치를 입증하고 있습니다. 2025년 12월에 체결된 미국-한국 Zinc의 테네시주 내 67억-74억 달러 규모 제련소 건설 계약은 2029년까지 국내 슈퍼 스페셜 하이그레이드(SHG) 아연 공급을 확보하고, 지역 내 나노 산화아연 시장에 진출하는 기업들의 원료 리스크를 경감시킬 것입니다.

유럽에서는 REACH 신청 서류 비용과 SCCS(유럽 화학 안전 위원회)의 모니터링 체계로 인해 규정 준수 장벽이 높아, BASF나 Merck KGaA와 같은 기존 기업들이 유리한 입지를 점하고 있습니다. 2025년 5월의 4-MBC 금지 조치는 광물성 자외선 차단제 수요를 촉진했으나, 어드밴스 징크테크의 분기 보고서에 따르면 유럽에서의 매출액은 41만 호주달러로 정체된 상태이며, 이는 배합 승인까지의 긴 주기를 보여주고 있습니다. 순도 99.99% 이상의 아연 공급 부족 현상이 지속되고 있는 가운데, EU 제조업체들은 카자흐스탄 및 노르웨이의 제련소와 공급 계약을 체결하여 조달처를 다각화하려 하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the nano zinc oxide market size is projected to expand from USD 521.22 million in 2025 and USD 555.99 million in 2026 to USD 767.85 million by 2031, registering a CAGR of 6.67% between 2026 and 2031.

This report is Segmented by Type (Coated Nano Zinc Oxide and Uncoated Nano Zinc Oxide), Form (Powder and Dispersion/Slurry), Application (Personal Care and Cosmetics, Paints and Coatings, Electronics, Textiles, Rubber and Plastics, Pharmaceuticals, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Nano Zinc Oxide Market Trends and Insights

Regulatory Shift Toward Non-Nano TiO2 Alternatives in Sunscreens

Expanded scrutiny of titanium dioxide has redirected sunscreen innovation. The Scientific Committee on Consumer Safety (SCCS) intensified its review of nano-TiO2 during 2024, prompting formulators to prioritize zinc oxide that stays just above the 100-nm threshold, thereby avoiding nano labeling while preserving transparency. Concurrently, the US Food and Drug Administration (FDA)'s unresolved monograph leaves 12 organic filters in limbo, whereas zinc oxide retains Category I status, reinforcing its safe-harbor advantage. Suppliers such as Solesence apply aluminum-oxide and organosilane shells that deliver high SPF with minimal whitening, a capability validated by its Australian TGA site clearance. Market inquiries rose sharply after the May 2025 SCCS ban on 4-methylbenzylidene camphor, consolidating zinc oxide's position as one of the few globally harmonized UV filters. These converging regulations are forecast to keep mineral actives at the forefront of premium sun-care launches across developed economies.

Rising Use in Mini-LED/µ-LED Backplane Electronics

Display manufacturers are transitioning to aluminum- or gallium-doped zinc oxide as a cost-efficient transparent conductor. Peer-reviewed 2024 studies showed atomic-layer-deposited AZO films achieving sheet resistance below 10 Ω/sq with over 85% visible-light transmittance, meeting 4K and 8K panel specifications. Japan and South Korea integrated these films into premium televisions that shipped in excess of 2 million units in 2025. China's rapid capacity build-out for mini-LED backlights further elevates regional demand. Because zinc oxide can be solution-processed at low temperatures, the material also aligns with flexible and wearable electronics, positioning the nano zinc oxide market for continued expansion as micro-LED architectures scale commercially.

High CAPEX/OPEX for Vapor-Phase Flame-Spray Synthesis Routes

Building a 10,000 tons per year flame-spray plant requires USD 4-7 million for reactors, precipitators, and pollution controls. Operating costs of USD 800-1,200 per ton, driven by natural-gas flames and exhaust scrubbing, squeeze Western margins, especially with EU carbon allowances exceeding EUR 80 (~USD 93.20) per ton in 2025. Pilot hydrothermal projects achieved cost parity but face scalability challenges due to nucleation kinetics. Until continuous hydrothermal processing matures, Chinese producers with lower utility tariffs retain a structural cost edge, restraining price realization across the nano zinc oxide market.

Other drivers and restraints analyzed in the detailed report include:

- Antibacterial Surface Coatings for High-Touch Public Assets

- EU Micro-Plastics Ban Spurring Bio-Degradable UV-Packaging Inks

- Stricter Occupational Exposure Limits for Nano-Metals

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Coated variants secured 62.21% nano zinc oxide market share in 2025, owing to surface treatments that reduce photocatalysis and deliver an invisible finish in sunscreens. The premium added cost of USD 2-5/kg is absorbed by personal-care brands that prioritize consumer aesthetics and reef safety. Uncoated grades, though smaller, are predicted to outpace with a 6.88% CAGR as drug-delivery developers need pristine surfaces for optimal cell uptake. Pharmaceutical trials published in 2024 showed 60% bioavailability for uncoated nanoparticles versus 35-40% for coated ones. Regulatory nuance is pivotal: coated grades often require separate EU REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals) dossiers, posing a hurdle for new entrants. Advance ZincTek invested early in REACH and TGA (Therapeutic Goods Administration) compliance, positioning itself for post-4-MBC demand spikes in Europe.

Second-order effects include competitive protection for firms holding coating IP portfolios. Solesence lists 10 US patents and over 100 foreign filings, leveraging exclusivity to negotiate long-term supply agreements with BASF. As consumer brands consolidate suppliers for transparency, the coated segment will remain the pricing anchor of the nano zinc oxide market, while uncoated growth taps higher-margin pharmaceutical channels.

Geography Analysis

Asia-Pacific held 48.11% of 2025 revenue, with a forecast of 7.74% CAGR during the forecast period (2026-2031), led by China's low-cost flame-spray plants and Japan's electronics demand. Chinese suppliers such as Huzheng and SAT NANO sell commodity powder at USD 1.50-2.13/kg, undercutting Western prices by up to 40%. Quality variability limits penetration in high-value pharma grades, allowing Japanese and Australian players to serve premium niches. India's cosmetics boom under the PLI scheme and Rubamin's 50,000 tons per year capacity extension reinforce South Asia's emerging influence over nano zinc oxide market dynamics.

North America's 2025 market share was buoyed by clean-beauty preferences and EV infrastructure investment. Solesence booked USD 52.3 million revenue in 2024, with finished consumer products representing 85% of sales, demonstrating value capture closer to the brand front line. The December 2025 U.S.-Korea Zinc deal to build a USD 6.7-7.4 billion smelter in Tennessee secures domestic Super Special High Grade (SHG) zinc supply by 2029, mitigating feedstock risk for regional nano zinc oxide market participants.

In Europe, REACH dossier costs and SCCS vigilance create high compliance barriers, favoring incumbents such as BASF and Merck KGaA. The May 2025 4-MBC ban catalyzed mineral UV filter demand, yet Advance ZincTek's interim report showed flat European sales at AUD 0.41 million, illustrating long formulary qualification cycles. Supply tightness persists for more than or equal to 99.99% purity zinc, prompting EU manufacturers to diversify sourcing via off-take agreements with Kazakhstan and Norway smelters.

- Advanced NanoTech Lab

- ALTANA

- American Elements

- BASF

- EverZinc

- Inframat Advanced Materials LLC

- Intelligent Materials Private Limited

- Merck KGaA

- Nanoshel LLC

- Reade

- SkySpring Nanomaterials, Inc.

- Umicore

- US Research Nanomaterials, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory shift toward non-nano TiO2 alternatives in sunscreens

- 4.2.2 Rising use in mini-LED/µ-LED backplane electronics

- 4.2.3 Antibacterial surface coatings for high-touch public assets

- 4.2.4 EU micro-plastics ban spurring bio-degradable UV-packaging inks

- 4.2.5 ZnO varistor ceramics for EV fast-charging surge protection

- 4.3 Market Restraints

- 4.3.1 High CAPEX/OPEX for vapor-phase flame-spray synthesis routes

- 4.3.2 Stricter occupational exposure limits for nano-metals

- 4.3.3 Volatile availability-pricing of more than or equal to 99.9% purity Zn feedstock

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Coated Nano Zinc Oxide

- 5.1.2 Uncoated Nano Zinc Oxide

- 5.2 By Form

- 5.2.1 Powder

- 5.2.2 Dispersion/Slurry

- 5.3 By Application

- 5.3.1 Personal Care and Cosmetics

- 5.3.2 Paints and Coatings

- 5.3.3 Electronics

- 5.3.4 Textiles

- 5.3.5 Rubber and Plastics

- 5.3.6 Pharmaceuticals

- 5.3.7 Other Applications (Textiles, Rubber, and More)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 Advanced NanoTech Lab

- 6.4.2 ALTANA

- 6.4.3 American Elements

- 6.4.4 BASF

- 6.4.5 EverZinc

- 6.4.6 Inframat Advanced Materials LLC

- 6.4.7 Intelligent Materials Private Limited

- 6.4.8 Merck KGaA

- 6.4.9 Nanoshel LLC

- 6.4.10 Reade

- 6.4.11 SkySpring Nanomaterials, Inc.

- 6.4.12 Umicore

- 6.4.13 US Research Nanomaterials, Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment