|

시장보고서

상품코드

2062122

나일론 6 필라멘트사 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Nylon 6 Filament Yarn - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

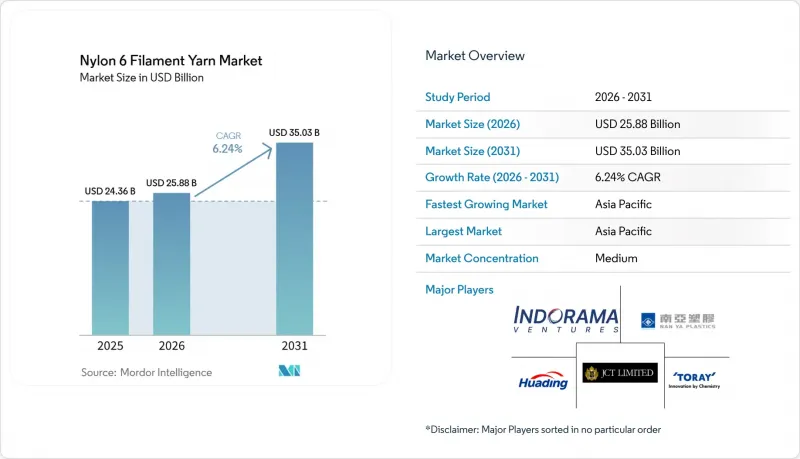

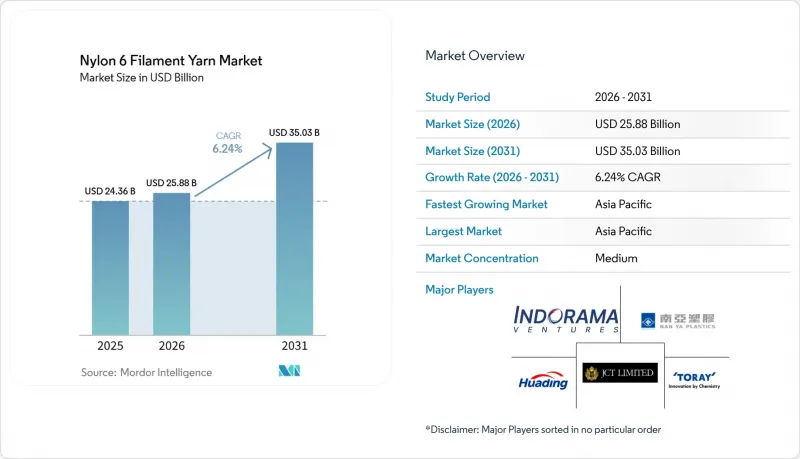

Mordor Intelligence에 의하면, 나일론 6 필라멘트사 시장 규모는 2025년에 243억 6,000만 달러로 평가되었습니다. 2026년 258억 8,000만 달러에서 2031년까지 350억 3,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 6.24%를 나타낼 전망입니다.

본 보고서는 원사 유형(POY, FDY, 기타), 용도(원단, 스포츠 의류, 기타), 유통 채널(섬유 무역사·도매업체, 기타), 최종 사용자 산업(의류 및 패션, 산업용·기술용 섬유, 기타), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 나일론 6 필라멘트사 시장 동향 및 인사이트

산업용 섬유의 확대

자동차 제조업체들은 특정 에어백용 원단의 경우, 나일론 6보다 강도가 높은 나일론 6 필라멘트를 선정하고 있습니다. 이 결정은 강도가 약간 저하되는 대신, 중합 주기를 단축하고 재료 비용을 절감하는 이점을 동시에 확보해야 할 필요성에서 비롯된 것입니다. 태국에서는 도요보와 인드라마가 운영하는 연간 1만 1,000톤 규모의 에어백용 원사 생산 시설이 동남아시아 전역의 OEM 업체들에 대한 리드타임을 단축하고 있습니다. AdvanSix의 저용융점도 수지는 엔진룸 내부 부품의 사출 성형 주기를 최대 40% 단축하여, 전기차의 경량화 요건을 충족하고 있습니다. 내마모성이 뛰어난 나일론 6 모노필라멘트는 반복되는 역세척 주기를 견딜 수 있는 산업용 여과재로 채택되어 있으며, ISO 11057 규격에 부합합니다. 또한, OSHA 1926의 개정에 따라 안전망에는 자외선 안정화 처리된 나일론 6의 사용이 권장되게 되었습니다. 성장은 미국, 독일, 중국의 자동차 산업 거점을 중심으로 이루어지고 있습니다. 이 지역들에서는 엔지니어링 센터와의 근접성이 사양 중심의 도입을 촉진하고 있습니다.

아시아의 도시형 자전거 공유 서비스와 전동 킥보드용 가방의 급성장

중국, 인도, 동남아시아 전역에서 지방자치단체의 마이크로모빌리티 프로그램에 경량 210-420 데니어 원단이 점점 더 많이 채택되고 있습니다. 500회 이상의 세탁을 견딜 수 있는 이 원단에는 주로 용액 염색 나일론 6 필라멘트가 사용됩니다. 메이투안(Meituan)이나 Hello 등의 업체들은 브랜딩 목적의 디지털 인쇄와의 호환성을 확보하기 위해 자외선 차단 등급 제품에 대한 수요를 주도하고 있습니다. 이에 대응하여 중국 양쯔강 삼각주 지역의 변환기 제조업체들은 전용 직기 라인을 설치했습니다. 인도에서는 인도표준협회(BIS)의 규격 IS 15061에 따라, 특히 배터리 수납 케이스용으로 난연성 혼합 재료의 사용이 권장되고 있습니다. 또한, 일반적으로 12-18개월간공급 계약을 통해 중데니어 POY 제조업체는 안정적인 공급량을 유지하고 있습니다.

비용 경쟁이 치열한 폴리에스터와 폴리프로필렌을 대체

현재, 흡습·발산성 면에서 나일론 6에 필적하는 폴리에스터는 그 성능을 15-20% 더 낮은 비용으로 실현하고 있습니다. 이러한 비용 차이로 인해 중저가 액티브웨어 시장에서 나일론이 시장 점유율을 유지하는 것이 과제가 되고 있습니다. 인도에서는 2024년 나일론 모노필라멘트 수입량이 전년 대비 18% 감소했으며, 이는 폴리프로필렌과의 경쟁이 심화되고 있음을 보여줍니다. 폴리프로필렌은 밀도가 낮기 때문에 지오텍스타일이나 브러시 털 등의 용도에서 점차 나일론 6을 대체하고 있습니다. 또한, 재생 폴리에스터는 비재생 제품과 동등한 원가를 실현하고 있는 반면, 재생 나일론 6은 30-50% 더 비싸기 때문에 큰 제약 요인으로 작용하고 있습니다. 이러한 가격 차이로 인해, 이 제품의 채택은 주로 프리미엄 시장 부문으로 한정되어 있습니다.

부문별 분석

2025년 기준으로, 부분 신장사는 나일론 6 필라멘트사 시장의 31.11%를 차지했으며, 이는 다운스트림 공정에서 텍스처링의 유연성이라는 장점에 힘입은 결과입니다. 양말이나 신축성 원단의 경우, 부피 증가나 뒤틀림을 제어해야 하기 때문에 이 부문은 연평균 성장률(CAGR) 6.31%로 확대될 것으로 예측됩니다. 풀드로우 원사(FDY)는 에어젯 직기를 가동하는 중국의 통합형 방적 공장에서 보급이 확대되고 있으며, POY(부분 신장 원사)의 텍스처링 공정에 비해 에너지 사용량을 12-18% 절감하고 있습니다. 고강도 등급은 8.5 g/데니어 이상의 강도가 필수로 요구되는 타이어 코드나 에어백용 원단에 사용됩니다.

중국의 생산자들은 증가하는 테크니컬 텍스타일 수요를 충족하기 위해 FDY 및 고강도 제품 라인에 새로운 생산 능력을 배정하고 있는 반면, 대만의 방적 공장들은 고급 아웃도어 브랜드용 10데니어 이하의 마이크로필라멘트 생산을 전문으로 하고 있습니다. 자동화 및 인더스트리 4.0을 기반으로 한 제어 기술 덕분에 성장률과 수축률을 실시간으로 모니터링할 수 있게 되어, 규격 외 폐기물이 5-7% 감소했습니다. 그러나 POY(폴리에스터 오리엔티드 원사)의 나일론 6 필라멘트사 시장 규모는 여전히 다른 원사들을 압도하고 있으며, 이는 아시아 전역에 뿌리 깊은 독립 텍스처링 업체들의 인프라를 반영하고 있습니다.

2025년에는 원단 용도가 시장 점유율의 38.89%를 차지했습니다. 그러나 폴리에스테르로의 대체가 진행되고 있어 그 성장세는 제한적입니다. 스포츠 어드벤처 용품 부문은 연평균 성장률(CAGR) 6.45%를 나타낼 것으로 전망됩니다. 이러한 성장은 나일론의 내마모성에 기인하며, 초경량 텐트, 배낭, 하네스 등의 용도에서 폴리에스터보다 25-40% 높은 가격 책정이 정당화되고 있습니다. 규제가 엄격한 틈새 시장인 어망 부문에서는 유럽연합(EU)과 일본이 정한 지속가능성 요건을 준수하기 위해 재활용 소재의 사용이 점차 의무화되고 있습니다.

프리미엄 브랜드의 발주에 따른 7-15 데니어 원단에 대한 수요는 이러한 원단이 ASTM D5034의 인열 강도 기준(40 N 이상)을 충족함에 따라 증가하고 있습니다. 이러한 추세에 따라 풀드로우 가공 및 UV 안정화 처리를 거친 원사에 대한 수요가 증가하고 있습니다. 이와 동시에, 여행용 액세서리 부문에서는 용액 염색 처리된 420-840 데니어 필라멘트가 사용되고 있습니다. 이러한 필라멘트는 대량 맞춤형 디지털 프린팅을 가능하게 하며, 리드 타임을 30-40% 단축합니다. 스포츠 및 어드벤처 장비와 관련된 나일론 6 필라멘트사 시장 규모는 여전히 비교적 작지만, 성장을 이어가고 있습니다. 또한, 이 부문은 일반 원단에 비해 높은 이익률을 기록하고 있습니다.

지역별 분석

2025년에는 아시아태평양이 전 세계 시장의 51.12%를 차지하며, 연평균 성장률(CAGR) 6.36%를 나타냈습니다. 중국 장쑤성과 저장성에 위치한 통합 허브에서는 다른 지역에 비해 15-20% 낮은 가공 비용을 실현하고 있습니다. 또한, 베트남과 태국은 서유럽 타이어 시장에 관세 없이 진출하고자 하는 중국 기업들에게 주요 거점으로 부상하고 있습니다. 인도에서는 수라트와 티르푸르의 방적 클러스터 현대화를 위한 노력이 진행되고 있지만, 인도는 특수 원사 수요를 충족하기 위해 여전히 수입에 의존하고 있습니다.

북미에서는 BASF와 Fibrant의 공장 폐쇄 이후 발생한 카프로락탐 공급 부족으로 인해 어려움을 겪고 있습니다. 이로 인해 해당 지역의 수입 의존도가 높아지고 있습니다. 에어백 및 방위용도에 필수적인 고강도 섬유의 국내 생산은 국제무기거래규정(ITAR)의 제한으로 인해 안정적으로 이루어지고 있습니다. 그러나 패션용 필라멘트의 조달처는 미국·멕시코·캐나다 협정(USMCA)의 규정에 따라 운영되는 캐나다와 멕시코의 가공업체들에 의해 촉진되면서 아시아로 점차 이동하고 있습니다. 유럽에서는 시장이 아쿠아필(Aquafil)사의 ‘에코닐(ECONYL)’과 같은 고급 원편사 부문과, 배출권 거래 제도(ETS) 비용으로 인해 위축되고 있는 범용 제품 생산 부문으로 양극화가 진행되고 있습니다. 게다가 튀르키예의 세이프가드 관세가 아시아 지역 수출처 변경에 영향을 미치고 있습니다.

남미에서는 주로 브라질의 자동차 산업과 액티브웨어에 대한 수요 증가에 힘입어 시장이 완만한 성장세를 보이고 있습니다. 그러나 이 지역은 특수 필라멘트 공급에 있어 여전히 아시아 공급업체에 의존하고 있습니다. 중동 및 아프리카에서는 사우디아라비아의 초기 단계 프로젝트가 저비용 가스 원료 공급을 활용하고 있습니다. 이러한 장점에도 불구하고, 해당 지역은 숙련된 인력 부족이나 공급망의 비효율성 같은 과제에 직면해 있으며, 이러한 요인들이 프로젝트의 확장성을 제한하고 있습니다. 그 결과, 나일론 6 필라멘트사 시장은 여전히 아시아에 집중되어 있는 반면, 유럽과 북미에서는 지속가능성과 추적성을 중시하는 틈새 시장 개발에 주력하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the nylon 6 filament yarn market size was valued at USD 24.36 billion in 2025 and is estimated to grow from USD 25.88 billion in 2026 to reach USD 35.03 billion by 2031, at a CAGR of 6.24% during the forecast period (2026-2031).

This report is Segmented by Yarn Type (POY, FDY, and More), Application (Fabric, Sports Apparel, and More), Distribution Channel (Textile Traders/Distributors, and More), End-User Industry (Apparel & Fashion, Industrial and Technical Textiles, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle-East and Africa). Market Forecasts are Provided in Terms of Value (USD).

Global Nylon 6 Filament Yarn Market Trends and Insights

Expansion of Technical Textiles

Automakers are choosing high-tenacity Nylon 6 filaments over Nylon 6,6 in certain airbag fabrics. This decision is driven by the need to balance slightly lower strength with faster polymerization cycles and reduced material costs. In Thailand, Toyobo and Indorama's facility, producing 11,000 tons per year of airbag yarn, is reducing lead times for OEMs across Southeast Asia. AdvanSix's resins, with low melt viscosity, are reducing injection-molding cycles by up to 40% for under-hood components, aligning with the lightweighting requirements of electric vehicles. Nylon 6 monofilament, valued for its abrasion resistance, is being specified for industrial filtration media during repeated back-wash cycles, meeting ISO 11057 standards. Additionally, updates from OSHA 1926 now recommend UV-stabilized Nylon 6 for safety netting. Growth is focused around automotive hubs in the U.S., Germany, and China, where proximity to engineering centers supports specification-driven adoption.

Rapid Growth in Asian Urban Bike-Sharing and E-Scooter Bags

Across China, India, and Southeast Asia, municipal micro-mobility programs are increasingly adopting lightweight 210-420 denier fabrics. These fabrics, which can withstand over 500 wash cycles, are primarily using solution-dyed Nylon 6 filament. Operators such as Meituan and Hello are driving demand for UV-resistant grades to ensure compatibility with digital printing for branding purposes. In response, converters in China's Yangtze River Delta have set up dedicated weaving lines. In India, the Bureau of Indian Standards IS 15061 is encouraging the use of flame-retardant blends, particularly for battery enclosures. Furthermore, supply contracts, typically lasting 12-18 months, are enabling mid-denier POY producers to maintain a steady off-take.

Cost-Competitive Polyester and Polypropylene Substitutions

Polyester, which now matches Nylon 6 in moisture-wicking capabilities, achieves this at a cost that is 15 to 20 percent lower. This cost difference is creating challenges for Nylon in retaining its share within the mid-tier activewear market. In India, a year-on-year decline of 18 percent in Nylon monofilament imports in 2024 indicates increasing competition from Polypropylene. Due to its lower density, Polypropylene is gradually replacing Nylon 6 in applications such as geotextiles and brush bristles. Additionally, while recycled polyester has achieved cost parity with its non-recycled counterpart, the higher cost of recycled Nylon 6, which is 30 to 50 percent more expensive, acts as a significant restraint. This price disparity is limiting its adoption primarily to premium market segments.

Other drivers and restraints analyzed in the detailed report include:

- Fishing and Aquaculture Net Modernization Programs

- Low-Denier Micro-Filament Adoption in Premium Outdoor Gear

- Carbon-Pricing and Decarbonization CAPEX

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Partially oriented yarn accounted for 31.11% of the Nylon 6 filament yarn market in 2025, benefiting from flexibility in downstream texturing. The segment is expected to rise at a 6.31% CAGR as hosiery and stretch fabrics demand controlled bulk and crimp. Fully drawn yarn is gaining traction in integrated Chinese mills feeding air-jet looms, trimming energy use 12-18% versus POY-texturing routes. High-tenacity grades serve tire cord and airbag fabrics where greater than 8.5 g/denier strength is mandatory.

Chinese producers are allocating fresh capacity toward FDY and high-tenacity lines to capture rising technical-textile demand, while Taiwanese mills specialize in sub-10 denier micro-filament for premium outdoor brands. Automation and Industry 4.0 controls now allow real-time monitoring of draw ratio and shrinkage, reducing off-grade waste by 5-7%. However, the Nylon 6 filament yarn market size for POY still dwarfs other yarns, reflecting the entrenched infrastructure of independent texturizers across Asia.

In 2025, fabric applications accounted for 38.89% of the market share. However, their growth has been limited due to the increasing substitution of polyester. The sports and adventure equipment segment is anticipated to grow at a compound annual growth rate (CAGR) of 6.45%. This growth is attributed to the abrasion resistance of nylon, which justifies a price premium of 25-40% over polyester in applications such as ultralight tents, backpacks, and harnesses. The fishing nets segment, which operates within a regulated niche, is progressively specifying recycled content to comply with sustainability mandates established by the European Union and Japan.

The demand for 7-15 denier fabrics, commissioned by premium brands, is increasing as these fabrics meet the ASTM D5034≥40 N tear strength standard. This trend is driving the need for fully drawn and UV-stabilized yarns. In parallel, the travel accessories segment is adopting solution-dyed 420-840 denier filaments. These filaments enable mass-customized digital prints and reduce lead times by 30-40%. The market size for Nylon 6 filament yarn associated with sports and adventure gear remains relatively small but is experiencing growth. Additionally, this segment offers higher margins compared to commodity fabrics.

Geography Analysis

In 2025, Asia-Pacific accounted for 51.12% of the global volume and is projected to grow at a compound annual growth rate (CAGR) of 6.36%. China's integrated hubs in Jiangsu and Zhejiang offer conversion costs that are 15-20% lower compared to other regions. Additionally, Vietnam and Thailand are emerging as key destinations for Chinese firms seeking tariff-free access to Western tire markets. In India, efforts are underway to upgrade the Surat and Tirupur spinning clusters; however, the country continues to rely on imports to meet its demand for specialty yarns.

North America faces challenges due to a caprolactam deficit, which arose after the closures of BASF and Fibrant facilities. This has increased the region's dependence on imports. Domestic production of high-tenacity yarns, which are essential for airbags and defense applications, remains stable due to International Traffic in Arms Regulations (ITAR) restrictions. However, the sourcing of fashion-grade filaments is shifting toward Asia, facilitated by Canadian and Mexican converters operating under the United States-Mexico-Canada Agreement (USMCA) rules. In Europe, the market is divided between premium circular yarns, such as Aquafil's ECONYL, and a declining commodity production segment that is burdened by Emissions Trading System (ETS) costs. Furthermore, Turkey's safeguard duties are influencing the redirection of Asian exports.

In South America, the market is experiencing modest growth, primarily driven by Brazil's automotive sector and an increasing demand for activewear. However, the region remains dependent on Asian suppliers for specialty filaments. In the Middle East and Africa, early-stage projects in Saudi Arabia are leveraging the availability of low-cost gas feedstocks. Despite this advantage, the region faces obstacles such as a shortage of skilled labor and inefficiencies in the supply chain, which are limiting the scalability of these projects. Consequently, the Nylon 6 filament yarn market continues to be concentrated in Asia, while Europe and North America focus on developing niches that emphasize sustainability and traceability.

- Aquafil S.p.A.

- Anand Rayons Ltd.

- Changzhou Yida Chemical Fiber

- East Asia Textile Technology

- Indorama Ventures PCL

- JCT Ltd.

- NanYa Plastics Corp.

- Prutex Nylon Co., Ltd.

- Salud Industry (Dongguan) Co., Ltd.

- Singhal Industries Pvt.

- Toray Industries Inc.

- Universal Fibers, Inc.

- Yiwu Huading Nylon

- Zhejiang Century ChenXing Fiber Technology

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of technical textiles (safety, filtration, airbags)

- 4.2.2 Rapid growth in Asian urban bike-sharing and e-scooter bags

- 4.2.3 Fishing and aquaculture net modernization programs

- 4.2.4 Low-denier micro-filament adoption in premium outdoor gear

- 4.2.5 Corporate circularity targets driving recycled Nylon 6 procurement

- 4.3 Market Restraints

- 4.3.1 Cost-competitive polyester and polypropylene substitutions

- 4.3.2 Carbon-pricing and decarbonisation CAPEX for high-temperature polymerisation

- 4.3.3 Equipment bottlenecks for chemical recycling feedstock

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of Substitution

- 4.5.4 Threat of New Entrants

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Yarn Type

- 5.1.1 Partially Oriented Yarn (POY)

- 5.1.2 Fully Drawn Yarn (FDY)

- 5.1.3 High-Tenacity Industrial Yarn

- 5.1.4 Textured Yarn

- 5.2 By Application

- 5.2.1 Fabric

- 5.2.2 Sports Apparel

- 5.2.3 Sports and Adventure Equipment

- 5.2.4 Travel Accessories

- 5.2.5 Fishing Nets

- 5.3 By Distribution Channel

- 5.3.1 Textile Traders / Distributors

- 5.3.2 Direct Sales (Spinners)

- 5.3.3 E-commerce Platforms

- 5.4 By End-user Industry

- 5.4.1 Apparel and Fashion

- 5.4.2 Industrial and Technical Textiles

- 5.4.3 Automotive Components

- 5.4.4 Consumer Goods

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Vietnam

- 5.5.1.6 Malaysia

- 5.5.1.7 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Nordic Countries

- 5.5.3.7 Russia

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Aquafil S.p.A.

- 6.4.2 Anand Rayons Ltd.

- 6.4.3 Changzhou Yida Chemical Fiber

- 6.4.4 East Asia Textile Technology

- 6.4.5 Indorama Ventures PCL

- 6.4.6 JCT Ltd.

- 6.4.7 NanYa Plastics Corp.

- 6.4.8 Prutex Nylon Co., Ltd.

- 6.4.9 Salud Industry (Dongguan) Co., Ltd.

- 6.4.10 Singhal Industries Pvt.

- 6.4.11 Toray Industries Inc.

- 6.4.12 Universal Fibers, Inc.

- 6.4.13 Yiwu Huading Nylon

- 6.4.14 Zhejiang Century ChenXing Fiber Technology

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment