|

시장보고서

상품코드

2062154

사출성형 폴리아미드 6 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Injection Molding Polyamide 6 - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

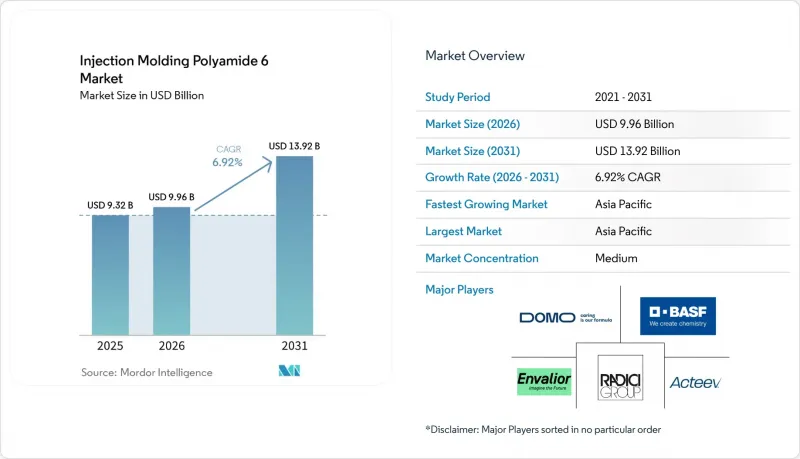

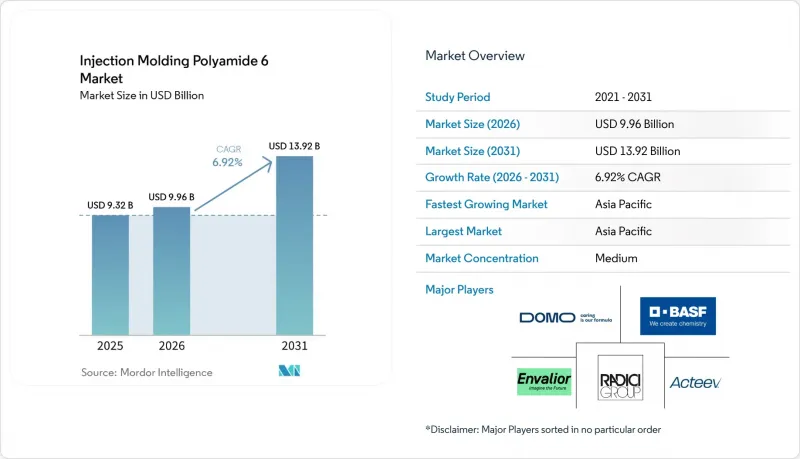

Mordor Intelligence에 의하면, 사출성형 폴리아미드 6시장 규모는 2025년 93억 2,000만 달러로 평가되었습니다. 2026년 99억 6,000만 달러로 확대되어 2031년까지 139억 2,000만 달러에 이를 것으로 예상되며 2026-2031년에 걸쳐 CAGR은 6.92%를 나타낼 전망입니다.

본 보고서는 유형(무충진 PA6, 광물 충진 PA6, 기타), 가공 방법(표준 사출 성형, 가스 어시스트 사출 성형, 기타), 용도(자동차 부품, 전기 및 전자 기기, 기타), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 사출성형 폴리아미드 6 시장 동향 및 인사이트

전기 및 전자 부문에서 소형 부품의 성장

800V 고전압 차량 플랫폼이 확대됨에 따라, 1g 미만의 커넥터 및 센서에 대한 수요가 증가하고 있습니다. 이러한 부품에는 UL 94 V-0(언더라이터스 래버러토리즈 94 수직 연소 시험)의 난연성 평가와 600V 이하의 CTI(비교 트래킹 지수)가 요구됩니다. 유리섬유 강화 PA6 등급은 이러한 기준을 항상 충족합니다. BASF의 특수 폴리아미드 ‘Ultramid Advanced N’은 2025년에 KOSTAL Automotive와 계약을 체결하여 액정 폴리머의 대체재로 채택되었습니다. 이는 특수 폴리아미드가 0.03mm라는 정밀한 공차 범위를 충족하면서도 수지 비용을 약 15% 절감할 수 있는 능력을 입증한 것입니다. 또한, 마이크로 사출 성형기에서 폐쇄 루프 방식의 사출 중량 제어 기술이 발전함에 따라, 현재는 0.5%의 재현성을 달성하여 치수 공차의 변동을 최소화하고, 수작업에 의한 보정 필요성을 줄이고 있습니다.

PA6의 뛰어난 기계적·열적 특성

비충진 폴리아미드 6(PA6)의 인장 강도는 약 85MPa입니다. 유리 섬유를 30% 배합하면 이 강도는 170MPa까지 향상되며, 무하중 브래킷의 경우 알루미늄 다이캐스팅을 대체할 수 있는 경량 소재가 될 가능성을 지니고 있습니다. Toray Industries Inc.의 NANOALLOY 개질 등급은 얇은 두께 성형에 필요한 용융 유동성을 유지하면서 인장 탄성률을 25% 더 향상시킵니다. 또한, PA6의 진동 감쇠 성능 덕분에 유리섬유 강화 폴리프로필렌에 비해 차내 소음을 최대 5데시벨(dB)까지 줄일 수 있습니다. 이 특성은 계기판의 크로스카 빔에 활용되고 있습니다.

화석 유래 폴리머에 대한 규제 압력

2025년 11월부터 시행된 유럽연합(EU)의 펠릿 손실 규제에 따르면, 환경에 미치는 영향을 최소화하기 위해 배출 제로화를 위한 설비 교체가 의무화됩니다. 이 규제로 인해 중소 컴파운더의 이자·세금·감가상각 전 이익(EBITDA) 마진은 최대 150베이시스포인트 하락할 것으로 예측됩니다. 또한, 프랑스와 독일의 확대 생산자 책임(EPR) 제도에 따른 부과금은 바이오 폴리아미드 6(PA6)과 화학적 재활용 폴리아미드 6(PA6) 간의 비용 경쟁을 심화시켜, 해당 소재의 채택을 촉진하고 있습니다.

부문별 분석

2025년, 유리섬유 강화 PA6가 사출성형 폴리아미드 6 시장을 독점하며 48.11%의 점유율을 차지했습니다. 이러한 급증은 엔진 커버, 시트 프레임, 배터리 팩 브래킷 등의 용도에서 30%-50%의 유리섬유 강화 시스템이 채택된 데 따른 것으로, 이들 모두 8,000 MPa 이하의 탄성 계수를 필요로 합니다. 한편, 광물 충전 및 내충격성 개선 유형은 전체 시장의 4분의 1을 차지하며, 강성보다는 낮은 뒤틀림이나 저온 인성을 우선시하는 용도에서 선호되고 있습니다. 사출성형 폴리아미드 6 시장의 ‘기타’ 부문(탄소섬유, 바이오, 화학적 재활용 수지 포함)은 각 OEM 업체들이 스코프 3 배출량 감축을 적극적으로 추진하고 있는 만큼, 연평균 성장률(CAGR) 7.88%라는 견조한 성장이 예상됩니다.

BASF의 ‘루프아미드’, 라디치 그룹의 ‘BIONSIDE PA610’, UBE의 ISCC PLUS 인증을 획득한 바이오카프로락탐에서 볼 수 있듯이, 원료의 혁신을 통해 기존에는 화석 유래 벤젠에 의존하던 공급망이 재구축되고 있습니다. 동시에, 엔바리오사의 ‘듀레탄 FLX-RTM’은 회전 성형된 압력 용기 부문에서 틈새 시장을 개척하고 있습니다. 이러한 동향은 시장의 세분화를 여실히 보여주고 있으며, 가치가 범용 비충진 등급에서 내구성과 지속가능성 기준을 충족하는 특수한 엔지니어링 솔루션으로 명확하게 이동하고 있음을 시사합니다. 이 모든 것은 기존 재인증 절차로 인한 지연 없이 실현되고 있습니다.

지역별 분석

아시아태평양은 2025년 시장 규모의 50.11%를 차지했으며, 2031년까지 연평균 성장률(CAGR) 7.78%를 나타낼 것으로 전망됩니다. 2025년 하반기에는 중국이 연간 922킬로톤의 생산 능력을 갖춘 신규 공장을 가동하여, 주로 30-50% 함량의 유리섬유 강화 컴파운드 수출에 주력할 것으로 보입니다. 한편, 인도에서는 파노리(Panori)와 타네(Thane) 지역의 생산 능력 확대가 하이브리드차 및 전기차의 신속한 보급·제조(FAME) 제도에 따른 인센티브에 힘입어, 국내 전기차(EV) 관련 노력을 뒷받침하고 있습니다. 일본과 한국은 모두 프리미엄 나노 개질 및 바이오 순환형 제품을 상용화하고 있습니다. 이 제품들은 20-30%의 가격 프리미엄이 붙지만, OEM 업체들이 점점 더 엄격해지고 있는 탄소 발자국 규정에 대응하는 데에도 기여하고 있습니다.

북미에서는 ‘인플레이션 감축법(IRA)’에 힘입어 배터리 부품 성형 공정의 국내 복귀가 두드러지고 있으며, 어센드(Ascend)사가 앨라배마주에서 ReDefyne의 기계적 재활용 역량을 확대하고 있는 것이 그 한 예입니다. 미국의 생산 라인 가동률이 85%를 넘어섬에 따라, 세라니즈사는 2026년 2월부터 1Kg당 0.25달러의 추가 요금을 부과하기로 했습니다. 한편, 미국·멕시코·캐나다 협정(USMCA)에 따른 캐나다의 자동차 부품 무역은 폴리아미드 6(PA6)으로 제작된 흡기 매니폴드 및 냉각수 저장탱크의 미국에 대한 안정적인 공급을 확보함으로써 양국 간 공급망을 더욱 공고히 하고 있습니다.

유럽에서는 펠릿 손실 및 확장된 생산자 책임(EPR) 과세로 인한 비용을 관리하는 한편, 소재 개발 분야에서 주도권을 유지하고 있습니다. 그 대표적인 사례가 BASF가 알사시미(Alsachimie) 합작회사를 완전히 인수한 것으로, 이를 통해 유럽 내에서 아디핀산과 헥사메틸렌디아민(HMD)의 전구체를 확보할 수 있게 되었습니다. 독일의 각 OEM 기업들은 2028년까지 ‘지속 가능한 제품을 위한 에코디자인 규정(ESPR)’이 정한 25% 기준을 충족하는 것을 목표로, 재생 소재의 사용을 주도하고 있습니다. 반면, 영국에서는 기준이 다르기 때문에 적합성 심사 주기가 길어지고 있습니다. 라틴아메리카에서는 엔진 커버에 중점을 두고, 브라질의 에탄올 내성 배합을 활용하고 있습니다. 한편, 중동 및 아프리카 수요는 아직 초기 단계이긴 하지만, 사우디아라비아의 전기차 조립 및 남아프리카공화국의 광산기계 수요로 인해 증가하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the injection molding polyamide 6 market size is expected to increase from USD 9.32 billion in 2025 to USD 9.96 billion in 2026 and reach USD 13.92 billion by 2031, growing at a CAGR of 6.92% over 2026-2031.

This report is Segmented by Type (Unfilled PA6, Mineral-Filled PA6, and More), Processing Method (Standard Injection Molding, Gas-Assisted Injection Molding, and More), Application (Automotive Components, Electrical and Electronics, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Injection Molding Polyamide 6 Market Trends and Insights

Growth in E&E Miniaturized Components

As high-voltage 800-V vehicle platforms expand, the demand for sub-gram connectors and sensors is increasing. These components require a UL 94 V-0 (Underwriters Laboratories 94 Vertical Burning Test) flame rating and a CTI (Comparative Tracking Index) of less than or equal to 600 V. Glass-fiber-reinforced PA6 grades consistently meet these standards. BASF's Ultramid Advanced N, a specialty polyamide, secured contracts in 2025 with KOSTAL Automotive, replacing liquid-crystal polymer. This demonstrates the ability of specialty polyamides to meet precise 0.03 mm tolerance windows while reducing resin costs by approximately 15%. Additionally, advancements in closed-loop shot-weight control within micro-injection presses now achieve 0.5% repeatability, minimizing dimensional drift and reducing the need for manual rework.

Excellent Mechanical and Thermal Profile of PA6

Unfilled Polyamide 6 (PA6) has a tensile strength of approximately 85 MPa. With a 30% glass loading, this strength increases to 170 MPa, making it a potential lightweight alternative to aluminum die-castings in non-load-bearing brackets. Toray's NANOALLOY-modified grades enhance the tensile modulus by an additional 25%, while maintaining the melt flow required for thin-wall molding. Additionally, PA6's vibration-damping capability reduces interior noise by up to 5 decibels (dB) compared to glass-filled polypropylene. This feature is utilized in instrument-panel cross-car beams.

Regulatory Pressure on Fossil-Based Polymers

Effective November 2025, the European Union's (EU) pellet-loss rule requires zero-discharge upgrades, aimed at minimizing environmental impact. This regulation is projected to reduce Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA) margins for smaller compounders by up to 150 basis points. Furthermore, Extended Producer Responsibility (EPR) fees in France and Germany are driving the adoption of bio-based and chemically recycled polyamide 6 (PA6) by making it more cost-competitive.

Other drivers and restraints analyzed in the detailed report include:

- Capacity Expansions in Asia for Glass-Filled Grades

- Adoption in EV Battery Enclosures and E-Axle Housings

- Scrap-Rate Sensitivity in Micro-Injection Molding

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, glass-fiber-reinforced PA6 dominated the injection molding polyamide 6 market, seizing a 48.11% share. This surge was driven by the adoption of 30%-50% glass systems in applications like engine covers, seat frames, and battery-pack brackets, all demanding a modulus of less than or equal to 8,000 MPa. Meanwhile, mineral-filled and impact-modified variants carved out a combined quarter of the market, favored in applications prioritizing low warpage or cold-temperature toughness over stiffness. The other types segment of the injection molding polyamide 6 market, encompassing carbon-fiber, bio-based, and chemically recycled resins, is set to grow at a robust 7.88% CAGR, as OEMs aggressively pursue Scope-3 emission reductions.

Innovations in feedstock are reshaping supply chains, previously tethered to fossil benzene, as seen with BASF's loopamid, RadiciGroup's BIONSIDE PA610, and UBE's ISCC PLUS-certified bio-caprolactam. Concurrently, Envalior's Durethan FLX-RTM is carving out niches in rotational-molded pressure vessels. This trend underscores a market fragmentation, with a clear shift in value from generic unfilled grades to specialized engineered solutions that meet durability and sustainability benchmarks, all without the typical requalification holdups.

Geography Analysis

Asia-Pacific, accounting for 50.11% of the 2025 volume, is projected to grow at a 7.78% compound annual growth rate (CAGR) through 2031. In late 2025, China will activate new plants with a capacity of 922 kilotons per year, primarily focusing on exporting 30-50% glass compounds. Meanwhile, India's capacity expansions in Panoli and Thane are supporting domestic electric vehicle (EV) initiatives, driven by incentives from the Faster Adoption and Manufacturing of Hybrid and Electric Vehicles (FAME) scheme. Both Japan and South Korea are commercializing premium nano-modified and bio-circular variants, which, while commanding a 20-30% price uplift, also address the tightening carbon footprints of original equipment manufacturers (OEMs).

In North America, the reshoring of battery-component molding, spurred by the Inflation Reduction Act (IRA), is evident with Ascend's expansion of the ReDefyne mechanical-recycling capacity in Alabama. U.S. production lines are operating at over 85% utilization, leading Celanese to impose a USD 0.25 per kilogram surcharge in February 2026. Meanwhile, Canada's auto-parts trade, aligned with the United States-Mexico-Canada Agreement (USMCA), ensures a steady flow of polyamide 6 (PA6) intake manifolds and coolant reservoirs to the U.S., solidifying binational supply chains.

Europe, while managing costs from pellet-loss and extended producer responsibility (EPR) levies, maintains its leadership in material development. This is exemplified by BASF's complete acquisition of the Alsachimie joint venture, securing adipic acid and hexamethylenediamine (HMD) precursors within the bloc. German OEMs are leading the adoption of recycled content, aiming to meet the Ecodesign for Sustainable Products Regulation (ESPR)'s 25% threshold by 2028. In contrast, the UK's differing standards are extending qualification cycles. Latin America, with a focus on engine covers, is leveraging Brazil's ethanol-resistant formulations. Meanwhile, demand in the Middle East and Africa, though still in its early stages, is increasing with Saudi Arabia's EV assembly and South Africa's mining equipment.

- Arkema

- Asahi Kasei Corporation

- Ascend Performance Materials

- BASF

- Celanese Corporation

- Domo Chemicals

- EMS-CHEMIE HOLDING AG

- Ensinger

- Envalior

- Evonik Industries AG

- Kingfa Sci.&Tech. Co.,Ltd.

- LG Chem

- Mitsui Chemicals, Inc.

- Radici Partecipazioni SpA

- RTP Company

- SABIC

- Solvay

- Toray Industries, Inc.

- UBE Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth in E&E miniaturised components

- 4.2.2 Excellent mechanical and thermal profile of PA6

- 4.2.3 Capacity expansions in Asia for glass-filled grades

- 4.2.4 Adoption in EV battery enclosures and e-axle housings

- 4.2.5 Rapid-heating thin-wall molding technologies boosting PA6 penetration

- 4.3 Market Restraints

- 4.3.1 Regulatory pressure on fossil-based polymers

- 4.3.2 Scrap-rate sensitivity in micro-injection molding

- 4.3.3 Low thermal margin vs PA66 for >150 °C under-hood parts

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Unfilled PA6

- 5.1.2 Glass-fiber-reinforced PA6

- 5.1.3 Mineral-filled PA6

- 5.1.4 Impact-modified PA6

- 5.1.5 Other Types (carbon-fiber, bio-based, recycled)

- 5.2 By Processing Method

- 5.2.1 Standard injection molding

- 5.2.2 Gas-assisted injection molding

- 5.2.3 Micro-injection molding

- 5.2.4 Other Processing Methods (water-assist, metal-insert)

- 5.3 By Application

- 5.3.1 Automotive Components

- 5.3.2 Electrical and Electronics

- 5.3.3 Industrial Machinery and Equipment

- 5.3.4 Consumer Goods (power tools, appliances)

- 5.3.5 Other Applications (Packaging, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Arkema

- 6.4.2 Asahi Kasei Corporation

- 6.4.3 Ascend Performance Materials

- 6.4.4 BASF

- 6.4.5 Celanese Corporation

- 6.4.6 Domo Chemicals

- 6.4.7 EMS-CHEMIE HOLDING AG

- 6.4.8 Ensinger

- 6.4.9 Envalior

- 6.4.10 Evonik Industries AG

- 6.4.11 Kingfa Sci.&Tech. Co.,Ltd.

- 6.4.12 LG Chem

- 6.4.13 Mitsui Chemicals, Inc.

- 6.4.14 Radici Partecipazioni SpA

- 6.4.15 RTP Company

- 6.4.16 SABIC

- 6.4.17 Solvay

- 6.4.18 Toray Industries, Inc.

- 6.4.19 UBE Corp.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment