|

시장보고서

상품코드

2062124

오디오 스트리밍 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Audio Streaming - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

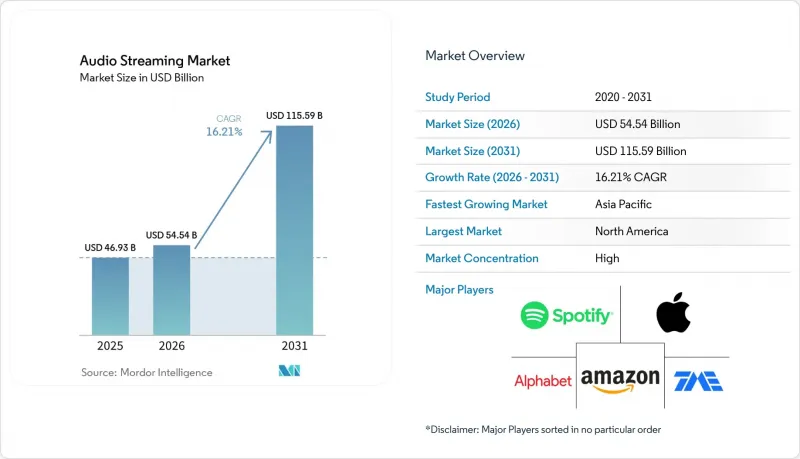

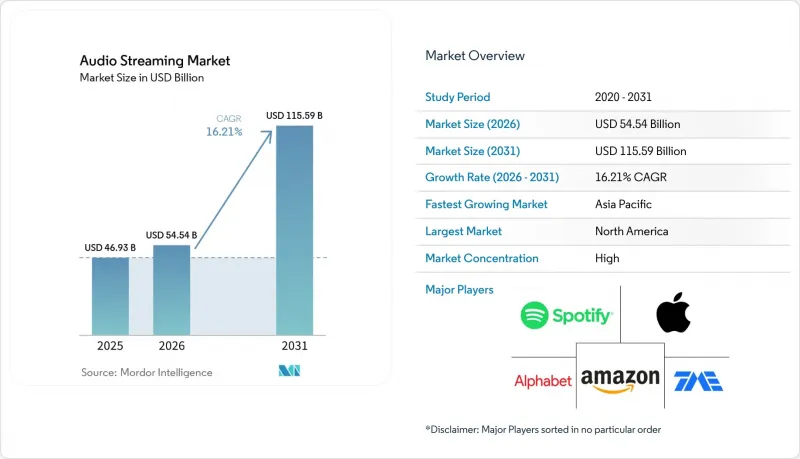

Mordor Intelligence에 의하면, 오디오 스트리밍 시장 규모는 2025년 469억 3,000만 달러에서 2026년에는 545억 4,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 16.21%로 성장을 지속하여, 2031년에는 1,155억 9,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 서비스 유형(온디맨드, 라이브 인터넷 라디오 등), 수익화 모델(구독형, 광고 지원형 등), 플랫폼/기기(스마트폰·태블릿, 데스크톱/노트북 등), 컨텐츠(음악, 팟캐스트 등), 최종 사용자(개인 소비자, 자동차 제조업체(OEM)와의 제휴 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 오디오 스트리밍 시장 동향과 인사이트

신흥국에서의 구독 요금 적정화

저소득층 시장을 대상으로 한 구독 요금 변경은 신규 사용자 유치를 완전히 중단하지 않으면서도 수익 구조를 개선하고 있으며, 오디오 스트리밍 시장에서 단순한 규모 확대 전략 이상의 의미를 지닙니다. 스포티파이는 2025년 8월 인도에서 프리미엄 요금제 가격을 17-28% 인상했지만, 가입자 수는 계속 증가했습니다. 이는 가장 열성적인 청취자층이 많은 소비자 모델이 예상했던 것보다 가격에 덜 민감했음을 시사합니다. 스트리밍이 이미 청취 시장을 장악하고 있는 지역에서는 이러한 경향이 더욱 두드러집니다. IFPI 보고서에 따르면, 중동 및 북아프리카의 음반 매출은 2024년에 전년 대비 22.8% 증가했으며, 총 매출의 99.5%를 스트리밍이 차지하고 있습니다. 이는 가격 책정이 해당 지역의 카테고리 수익 창출에 직접적인 영향을 미치고 있음을 의미합니다(IFPI). 또한 IFPI는 사하라 이남 아프리카가 2025년 가장 급성장한 음악 시장이며, 매출이 처음으로 1억 달러를 돌파했다고 밝혔습니다. 이는 지역별 가격 책정이 단순히 기존 지출을 재배분하는 데 그치지 않고, 새로운 수익원을 개척하고 있다는 관점을 뒷받침하는 것입니다. 오디오 스트리밍 시장에서 이러한 성장 요인은 플랫폼들이 모바일 광대역의 확대에 맞추어 지역별 요금 체계를 지속적으로 조정하고, 국경을 넘는 가격 차이로 인한 영향이 지역별 가격 구조를 약화시키지 않는 한 지속될 것입니다.

통신사(Telco)와 OTT의 번들링이 유료 서비스의 보급을 촉진

통신 사업자의 번들링은 오디오 스트리밍 시장에서 스트리밍 서비스를 별도로 구매하는 대상이 아닌 월정액 통신 요금제에 포함시킴으로써, 구독 서비스 도입의 장벽을 낮추고 있습니다. 디지털 미디어 협회(DMA)의 보고서에 따르면, 2025년 말까지 아시아태평양에서 500건 이상의 OTT 사업자와 통신 사업자 간 제휴가 성사되었으며, 이는 번들링이 더 이상 시험적인 모델이 아니라 표준적인 비즈니스 모델로 자리 잡았음을 보여줍니다. 에어텔(Airtel)은 2025년 2월, 후불 요금제 및 홈 Wi-Fi 요금제에 Apple Music을 추가했습니다. 이를 통해 가격에 가장 민감한 대규모 소비자층 중 하나를 대상으로 통신사 채널을 통해 해당 플랫폼의 도달 범위를 확대했습니다. 앙가미는 중동 및 북아프리카 16개국 내 45개 통신사와의 제휴를 발표했습니다. 이는 현지 전문 업체들도 대규모 세계 서비스에 맞서 자신들의 입지를 지키기 위해 번들링을 활용하고 있음을 보여줍니다. 이 점은 중요합니다. 이는 번들링을 통해 유입된 사용자들이 앱 기반 가입자들에 비해 해지 절차를 더 신중하게 진행하는 경향이 있으며, 그 결과 오디오 스트리밍 시장에서 시간이 지남에 따라 고객 유지율은 향상되고 자발적 해지율은 낮아지는 경향이 있기 때문입니다.

ARPU 증가율을 상회하는 로열티율 상승

로열티 인플레이션은 오디오 스트리밍 시장의 이익 확대에 있어 가장 명백한 구조적 제약 중 하나입니다. 저작권 로열티 위원회(CRB)의 Web VI 결정에 따라, 1회당 기계적 재생 요율은 Web V의 0.0021달러에서 2026년에는 0.0028달러로 인상되며, 2030년까지 0.0032달러로 상승하는 경로가 제시되었습니다. 디지털 미디어 협회(DMA)는 기존 체계 하에서 플랫폼들이 이미 수익의 약 70%를 저작권자에게 지급하고 있다고 밝혔으며, 이는 가격 조정이나 이익률 압박 없이 더 높은 사용료율을 감당할 여지가 제한적임을 의미합니다. 이 문제는 신흥 시장에서 더욱 심각합니다. 현지 가격 책정을 통해 대상 고객층을 확대하는 것은 가능하지만, 사용료 증가 속도를 따라잡을 만큼 신속하게 ARPU를 끌어올리지 못하는 경우가 많기 때문입니다. 또한 IMPALA는 2025년 6월, 스트리밍 개혁안으로 인해 로열티 수입이 카탈로그 작품 중심의 권리자에게 편중될 가능성이 있으며, 롱테일 컨텐츠로 차별화를 꾀하고 있는 플랫폼의 경우 비용 부담이 더욱 커질 우려가 있다고 경고했습니다.

부문별 분석

2025년, 주문형 음악 스트리밍은 오디오 스트리밍 시장 점유율의 78.20%를 차지하며, 해당 부문의 주요 수익원으로서의 입지를 유지했습니다. 이러한 경쟁력은 방대한 컨텐츠 라이브러리, 추천 시스템, 그리고 대규모 구독자 기반 전반에 걸쳐 월간 반복 수익을 뒷받침하는 정기적인 시청 습관에서 비롯됩니다. 또한, 이 서비스는 오랜 기간에 걸친 라이선스 계약, 재생 목록 생태계, 소셜 공유 기능의 혜택을 누리고 있어, 이러한 요소들 때문에 겉보기만큼 쉽게 서비스를 변경하기 어렵게 되었습니다. 오디오 스트리밍 시장은 여전히 예측 가능하고 반복적인 이용 사례에 크게 의존하고 있으며, 주문형 음악은 여전히 일상적인 청취와 가장 밀접하게 연결된 형식이기 때문에 이러한 기능들은 중요합니다. 동시에, 인접한 오디오 컨텐츠 카테고리가 새로운 청취 기회와 광고 공간을 창출하고 있기 때문에 이 부문은 더 이상 참여도 성장의 유일한 원동력이 아닙니다.

팟캐스트 호스팅 및 배포 시장은 광고 수요와, 라이선스 음악에 비해 크리에이터 주도형 컨텐츠 호스팅에 드는 한계 비용이 낮다는 점의 호재를 타고, 2031년까지 연평균 성장률(CAGR) 19.60%로 성장할 것으로 전망됩니다. 2026년에는 전 세계 월간 팟캐스트 청취자 수가 6억 1,900만 명에 달했으며, 같은 기간 미국 팟캐스트 광고 시장은 전년 대비 31% 성장했습니다. 이는 오디오 스트리밍 시장에서 팟캐스트 배포가 전략적 중요성을 더해가고 있는 이유를 보여줍니다. 스포티파이에 따르면, 오디오북 사업을 시작한 지 2년 차에 접어든 현재, 청취자 수는 전년 대비 36% 증가했으며, 14개 시장에서 50만 권이 넘는 도서 목록을 보유하고 있습니다. 이는 오디오북이 단순한 개별 구매 대상이 아니라, 보다 광범위한 구독 서비스 내에서 새로운 참여의 영역으로 자리 잡고 있다는 관점을 뒷받침하는 것입니다. 인터넷 라디오 생방송, ASMR, 명상용 오디오는 여전히 열성적인 청취자층을 유지하고 있으며, 이용 시간은 일반적인 주문형 컨텐츠보다 길고 몰입감이 더 높은 임베디드니다. 이는 온디맨드 음악이 여전히 서비스 모델의 경제성 측면에서 상업적 기준으로 자리 잡고 있음에도 불구하고, 오디오 스트리밍 업계가 점차 다양한 청취 형태에 대응해 나가고 있음을 의미합니다.

2025년 오디오 스트리밍 시장 규모에서 구독형 수익 모델은 63.10%의 점유율을 차지하고 있으며, 이는 주요 플랫폼 전반에 걸쳐 정기적인 유료 이용이 여전히 주요 수익 기반임을 보여줍니다. 이러한 구조는 스포티파이의 2억 9,300만 명에 달하는 프리미엄 구독자를 포함한 방대한 프리미엄 회원 기반과, 애플 뮤직과 같은 서비스가 기기 사용 현황 및 계정 ID와 긴밀하게 연동될 수 있도록 하는 생태계의 이점에 힘입어 여전히 견고하게 유지되고 있습니다. 또한, 구독 수익은 광고 수익보다 예측하기 쉬우므로, 성숙한 시장에서도 각 플랫폼 기업들은 정기적인 가격 인상을 지속적으로 시도하고 있습니다. 이 모델은 탄탄한 기반을 갖추고 있는데, 이는 열성적인 사용자들이 광고 없는 청취, 오프라인 접속, 그리고 방대한 컨텐츠 라이브러리를 핵심 가치 제안의 일부로 여기기 때문입니다. 오디오 스트리밍 시장에서 비록 다음 성장 단계가 신규 구독뿐만 아니라 광고 수익 증대에서도 비롯될지라도, 유료 요금제는 여전히 핵심적인 위치를 차지하고 있습니다.

광고 지원형 모델은 2031년까지 연평균 성장률(CAGR) 17.80%를 나타낼 것으로 예측되며, 오디오 스트리밍 시장에서 가장 빠르게 성장하는 수익 창출 경로가 될 것입니다. IAB와 PwC의 보고서에 따르면, 디지털 오디오 광고 시장은 2025년에 10.2% 성장하여 84억 달러에 달했습니다. 이는 엄청난 청취 시간을 바탕으로 수익 창출이 여전히 확대되고 있음을 보여줍니다. 프로그래매틱 광고 도구는 오디언스 타겟팅, 다이내믹 크리에이티브, 크로스 디바이스 측정 정확도 향상을 통해 플랫폼이 광고 인벤토리를 보다 효과적으로 활용할 수 있도록 지원하며, 이를 통해 이용 시간과 광고 수익 창출 사이에 오랫동안 존재해 온 격차가 줄어들고 있습니다. 하이브리드형 프리미엄 플랜은 저소득 시장에서의 진입 장벽을 낮추고, 시간이 지남에 따라 유료 플랜으로 유도하는 역할을 하므로 여전히 중요한 역할을 수행하고 있습니다. 청취 건당 과금 모델은 여전히 규모는 작지만, 월정액 계약을 원하지 않는 가끔 이용하는 사용자들을 위한 자리를 확보하고 있으며, 이를 통해 오디오 스트리밍 업계의 가격 체계가 다양하게 유지되고 있습니다.

지역별 분석

2025년, 북미는 오디오 스트리밍 시장에서 39.64%의 점유율을 차지하며 지역별로는 가장 큰 기여도를 보였습니다. 미국의 음악 도매 시장은 2025년에 115억 3,500만 달러에 달했으며, 유료 스트리밍 가입자 수는 1억 650만 명으로 증가했습니다. 이는 2022년 이후 가장 높은 연간 순 증가 수치로, 성숙한 환경에서도 성장이 지속되고 있음을 보여줍니다. 또한, 해당 지역은 프로그래매틱 오디오 광고의 기반이 가장 탄탄하며, 주요 플랫폼들은 유료 구독 서비스에 더해 무료 청취 및 팟캐스트의 수익 창출 능력을 더욱 강화하고 있습니다. 캐나다에서는 높은 광대역 보급률이 프리미엄 서비스 이용 확대를 뒷받침하고 있으며, 멕시코에서는 중산층의 확대와 번들 서비스를 통한 무료에서 유료로의 전환이 호재로 작용하고 있습니다. 이와 더불어, 2026년 4월에 발표된 SiriusXM과 YouTube의 오디오 광고 제휴는 팟캐스트 및 라디오 광고 공간이 대규모 광고 판매 인프라에 더욱 긴밀하게 통합되고 있는 시장의 실태를 보여줍니다. 또한, 미국 내 사용료율 결정이 오디오 스트리밍 시장 전체의 라이선싱 및 가격 책정 동향에 영향을 미칠 가능성이 있기 때문에 이 지역에서는 다른 많은 지역보다 사용료 규제가 더욱 중요한 의미를 지닙니다.

아시아태평양은 오디오 스트리밍 시장에서 가장 빠르게 성장하고 있는 지역으로, 2031년까지 연평균 성장률(CAGR)이 17.66%를 나타낼 것으로 전망됩니다. 텐센트 뮤직은 2026년 1분기에 79억 위안(11억 5,000만 달러)의 매출을 기록했으며, 이는 전년 동기 대비 7.3% 증가한 수치입니다. 이는 현지 플랫폼에 대한 투자와 컨텐츠 현지화가 여전히 강력한 성장을 뒷받침하고 있음을 보여줍니다. 인도의 모바일 광대역 가입자 수는 8억 1,200만 명을 넘어섰으며, 가격 정책과 번들 요금제가 소득 수준에 맞추어 지속적으로 조정되고 있는 가운데, 유료 오디오 서비스에 있어 여전히 방대한 잠재 고객층이 남아 있습니다. 일본, 한국, 호주는 여전히 프리미엄 시장이지만, 각국마다 고유한 컨텐츠 선호도가 있어 현지화된 편집 방침과 추천 모델이 요구되고 있습니다. 남미도 성장을 이어가고 있지만, 그 속도는 지역에 따라 차이가 있습니다. 브라질의 인터넷 보급률은 84.3%에 달하며, 가처분 소득이 적은 지역에서는 Claro Musica와 같은 통신사 주도의 스트리밍 모델이 여전히 중요한 역할을 하고 있습니다.

2025년, 유럽은 여전히 큰 점유율을 차지하고 있었지만, 그 성장 추세는 보급률이 높은 서유럽 시장과 이 지역 내 더 빠르게 성장하고 있는 신흥 시장 사이에서 엇갈리고 있습니다. 2024년 독일의 가구당 디지털 음악 지출은 전년 대비 18.7% 증가했으며, 영국의 오디오북 시장은 2억 6,800만 파운드(3억 4,100만 달러)에 달했습니다. 이는 지불 의향이 음악에만 국한되지 않고 오디오 포맷 전반으로 확대되고 있음을 보여줍니다. 개인정보 보호 규제로 인해 유럽에서의 수익 창출 방식이 재편되고 있습니다. 타겟팅 기준이 강화됨에 따라, 광고 지원형 오디오 플랫폼은 컨텍스트 광고 방식으로 전환해야 하는 상황에 놓여 있기 때문입니다. 중동 및 아프리카는 오디오 스트리밍 시장에서 더욱 전략적인 성장 거점으로 부상하고 있으며, 사우디아라비아는 2024년 엔터테인먼트 개발을 위해 48억 사우디 리얄(12억 8,000만 달러)을 배정했습니다. Anghami는 2025 회계연도에 전년 대비 27% 증가한 9,930만 달러의 매출을 기록했으며, Boomplay의 1억 4,500만 곡에 달하는 음원 카탈로그는 서아프리카를 컨텐츠 발신의 거점으로 자리매김하는 데 일조하고 있습니다. 규제, 현지 컨텐츠의 충실도, 그리고 엔터테인먼트 투자 증가가 맞물리면서, 세계 플랫폼이 확대되는 상황에서도 지역 전문 기업들은 여전히 중요한 입지를 유지할 여지가 남아 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19According to Mordor Intelligence, the audio streaming market size is expected to grow from USD 46.93 billion in 2025 to USD 54.54 billion in 2026 and is forecast to reach USD 115.59 billion by 2031 at 16.21% CAGR over 2026-2031.

This report is Segmented by Service Type (On-Demand, Live Internet Radio, and More), Monetization (Subscription-Based, Advertising-Supported, and More), Platform/Device (Smartphones and Tablets, Desktop/Laptop, and More), Content (Music, Podcasts, and More), End-User (Individual Consumers, Automotive OEM Integrations, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Audio Streaming Market Trends and Insights

Subscription Price Rationalization In Emerging Economies

Subscription price changes in lower-income markets are improving revenue mix without fully stopping user additions, which makes them more than a simple volume tactic in the audio streaming market. Spotify raised Premium pricing in India by 17-28% in August 2025, yet subscriber growth continued, which suggests that the most engaged listener groups were less price sensitive than many consumer models assumed. The same pattern matters even more in regions where streaming already dominates the listening economy. IFPI reported that recorded music revenue in the Middle East and North Africa grew 22.8% year over year in 2024, with streaming accounting for 99.5% of total revenue, which means pricing decisions directly shape category monetization in that region IFPI.ORG.IFPI also stated that Sub-Saharan Africa was the fastest-growing music market in 2025 and crossed USD 100 million in revenue for the first time, which supports the view that localized pricing is opening new revenue pools instead of just shifting existing spending. For the audio streaming market, this driver stays durable as long as platforms keep regional tiers aligned with mobile broadband expansion and keep cross-border arbitrage from weakening local price structures.

Telco-OTT Bundling Pushes Paid Uptake

Telco bundling is reducing the friction of subscription adoption by placing streaming inside monthly connectivity plans instead of treating it as a separate purchase in the audio streaming market. The Digital Media Association reported more than 500 OTT-operator partnerships across Asia-Pacific by the end of 2025, which shows that bundling had become a standard commercial route rather than a trial model. Airtel added Apple Music to its postpaid and home Wi-Fi plans in February 2025, which extended the platform's reach through an operator channel in one of the most price-sensitive large consumer bases. Anghami disclosed partnerships with 45 telecom operators across 16 Middle East and North Africa countries, showing that local specialists are also using bundling to defend their position against larger global services. This matters because bundled users usually face a more deliberate cancellation step than app-based sign-ups, and that tends to improve retention and lower voluntary churn over time in the audio streaming market.

Royalty-Rate Inflation Exceeding ARPU Growth

Royalty inflation is one of the clearest structural limits on profit expansion in the audio streaming market. The Copyright Royalty Board's Web VI determination raised the per-performance mechanical rate from USD 0.0021 under Web V to USD 0.0028 in 2026 and set a path to USD 0.0032 by 2030. The Digital Media Association stated that platforms already remit around 70% of revenue to rights holders under existing frameworks, which means there is limited room to absorb higher rates without price action or margin pressure. The problem is sharper in emerging markets, where localized pricing can expand the addressable base but often cannot raise ARPU fast enough to match the speed of royalty increases. IMPALA also warned in June 2025 that streaming reform proposals could steer more royalty flows toward catalog-heavy rights owners, which may deepen cost pressure for platforms that rely on long-tail content to differentiate.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Smart Speaker Install Base Expansion

- OEM-Level In-Car Streaming Integrations

- Content-License Windowing By Major Labels

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

On-demand music streaming held 78.20% of the audio streaming market share in 2025, which kept it as the core revenue engine for the category. That lead came from catalog depth, recommendation systems, and repeat listening habits that support monthly recurring revenue across large subscriber bases. The service also benefits from long-established licensing relationships, playlist ecosystems, and social sharing features that make switching less effortless than it appears at first glance. Those features matter because the audio streaming market still depends heavily on predictable, repeat use cases, and on-demand music remains the format most closely tied to everyday listening. At the same time, the segment is no longer the only driver of engagement growth because adjacent spoken-audio categories are adding new listening occasions and ad inventory.

Podcast hosting and distribution is projected to grow at a 19.60% CAGR through 2031, helped by advertising demand and the lower marginal cost of hosting creator-led content versus licensed music. Global monthly podcast listenership reached 619 million in 2026, and the United States podcast advertising market expanded 31% year over year in the same period, showing why podcast distribution is gaining strategic weight inside the audio streaming market. Spotify said audiobook listeners rose 36% year over year in the service's second year in that category, with a catalog that exceeded 500,000 titles across 14 markets, which supports the view that audiobooks are becoming an added engagement layer inside broader subscriptions rather than a separate purchase decision. Live internet radio, ASMR, and meditation audio still retain dedicated audiences whose sessions are often longer and more ambient than standard on-demand use. That means the audio streaming industry is gradually supporting more listening modes, even though on-demand music still sets the commercial baseline for service type economics.

Subscription-based monetization held 63.10% share of the audio streaming market size in 2025, which shows that recurring paid access remained the main cash foundation across leading platforms. This structure is still supported by large premium bases, including Spotify's 293 million premium subscribers, and by ecosystem advantages that help services like Apple Music stay closely tied to device usage and account identity. Subscription revenue also remains easier to forecast than advertising income, which is why platforms continue testing periodic price increases even in mature markets. The model has resilience because highly engaged users treat ad-free listening, offline access, and broader content libraries as part of the core value proposition. In the audio streaming market, this keeps paid tiers central even as the next phase of growth is coming from improved ad monetization rather than only new subscriptions.

The advertising-supported model is forecast to grow at a 17.80% CAGR through 2031, making it the fastest-growing monetization path in the audio streaming market. IAB and PwC reported that digital audio advertising grew 10.2% to USD 8.4 billion in 2025, which shows that monetization is still rising against a very large base of listening time. Programmatic tools are helping platforms make that inventory more usable through audience targeting, dynamic creative, and better cross-device measurement, which narrows the long-standing gap between time spent and ad spend capture. Hybrid freemium tiers still matter because they reduce entry barriers in lower-income markets and create a funnel into paid plans over time. Pay-per-listen models remain smaller, but they preserve a place for occasional users who want access without a monthly commitment, which keeps pricing architecture broad in the audio streaming industry.

Geography Analysis

North America held 39.64% share of the audio streaming market in 2025, which made it the largest regional contributor. The United States wholesale recorded music market reached USD 11.535 billion in 2025, and paid streaming subscriptions rose to 106.5 million, the strongest net annual intake since 2022, showing that growth continued even in a mature environment. The region also has the deepest programmatic audio advertising base, which gives leading platforms a stronger ability to monetize free listening and podcasts alongside paid subscriptions. Canada supports premium uptake through high broadband penetration, while Mexico is benefiting from middle-class expansion and bundle-led conversion from free to paid listening. In parallel, the SiriusXM and YouTube audio advertising arrangement announced in April 2026 points to a market where podcast and radio inventory is being drawn more tightly into large-scale ad sales infrastructure. Royalty regulation also matters more here than in many other regions because the United States rate decisions can influence broader licensing and pricing behavior across the audio streaming market.

Asia-Pacific is the fastest-growing region in the audio streaming market, with a projected CAGR of 17.66% through 2031. Tencent Music reported revenue of CNY 7.90 billion (USD 1.15 billion), in Q1 2026, up 7.3% year over year, showing that local platform investment and content localization are still supporting strong expansion. India's mobile broadband base exceeded 812 million subscriptions, which leaves a large addressable audience for paid audio as pricing and bundling continue to adapt to income realities. Japan, South Korea, and Australia remain premium markets, but each has distinct content preferences that require localized editorial decisions and recommendation models. South America is growing as well, though unevenly, with Brazil supported by 84.3% internet penetration and operator-led distribution models such as Claro Musica still important where discretionary spending is tighter.

Europe held a significant share in 2025, but its growth profile is split between highly penetrated Western markets and faster-expanding emerging parts of the region. Germany's household digital music spending rose 18.7% year over year in 2024, and the United Kingdom audiobook segment reached GBP 268 million (USD 341 million), which shows that willingness to pay is widening across audio formats rather than staying limited to music. Privacy rules are reshaping monetization in Europe because tighter targeting standards are pushing platforms toward contextual advertising methods for ad-supported audio. Middle East and Africa is becoming a more strategic growth pocket in the audio streaming market, with Saudi Arabia allocating SAR 4.8 billion (USD 1.28 billion), toward entertainment development in 2024, Anghami reporting FY2025 revenue of USD 99.3 million with 27% year-over-year growth, and Boomplay's 145-million-track catalog helping position West Africa as a content origination hub. This combination of regulation, local content depth, and rising entertainment investment means regional specialists still have room to hold meaningful ground even as global platforms expand.

- Spotify Technology S.A.

- Apple Inc. (Apple Music)

- Amazon.com Inc. (Amazon Music)

- Alphabet Inc. (YouTube Music)

- Tencent Music Entertainment Group

- Sirius XM Holdings Inc. (Pandora)

- SoundCloud Global Limited & Co. KG

- Deezer S.A.

- iHeartMedia Inc.

- KKBOX Inc.

- Anghami Plc

- JioSaavn LLC

- Gaana Media Private Ltd.

- Yandex N.V. (Yandex Music)

- NetEase Cloud Music Inc.

- Napster Group PLC

- TIDAL Music AS

- Qobuz SAS

- Boomplay Music Group

- Claro Musica (America Movil S.A.B. de C.V.)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Subscription Price Rationalization in Emerging Economies

- 4.2.2 Telco-OTT Bundling Pushes Paid Uptake

- 4.2.3 Rapid Smart Speaker Install Base Expansion

- 4.2.4 OEM-Level In-Car Streaming Integrations

- 4.2.5 AI Voice DJ and Generative Playlists Extend Daily Listening Time

- 4.2.6 Blockchain-Based Royalty Settlement Attracts Independent Catalogs

- 4.3 Market Restraints

- 4.3.1 Royalty-Rate Inflation Exceeding ARPU Growth

- 4.3.2 Content-License Windowing by Major Labels

- 4.3.3 Data-Privacy Regulations Limiting Ad-Targeting

- 4.3.4 Algorithmic Discovery Bias Marginalizing Long-Tail Creators

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 On-Demand Music Streaming

- 5.1.2 Live Internet Radio

- 5.1.3 Podcast Hosting and Distribution

- 5.1.4 Audiobook Streaming

- 5.1.5 Other Niche Audio (ASMR, Meditation)

- 5.2 By Monetization Model

- 5.2.1 Subscription-Based

- 5.2.2 Advertising-Supported

- 5.2.3 Hybrid Freemium

- 5.2.4 Pay-Per-Listen

- 5.3 By Platform/Device

- 5.3.1 Smartphones and Tablets

- 5.3.2 Desktop/Laptop

- 5.3.3 Smart Speakers and Home Hubs

- 5.3.4 Connected Cars

- 5.3.5 Wearables and Other IoT

- 5.4 By Content Type

- 5.4.1 Music

- 5.4.2 Podcasts

- 5.4.3 Audiobooks

- 5.4.4 Live Radio Streams

- 5.5 By End-User

- 5.5.1 Individual Consumers

- 5.5.2 Commercial Venues (Retail, Hospitality)

- 5.5.3 Automotive OEM Integrations

- 5.5.4 Media and Entertainment Enterprises

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Spotify Technology S.A.

- 6.4.2 Apple Inc. (Apple Music)

- 6.4.3 Amazon.com Inc. (Amazon Music)

- 6.4.4 Alphabet Inc. (YouTube Music)

- 6.4.5 Tencent Music Entertainment Group

- 6.4.6 Sirius XM Holdings Inc. (Pandora)

- 6.4.7 SoundCloud Global Limited & Co. KG

- 6.4.8 Deezer S.A.

- 6.4.9 iHeartMedia Inc.

- 6.4.10 KKBOX Inc.

- 6.4.11 Anghami Plc

- 6.4.12 JioSaavn LLC

- 6.4.13 Gaana Media Private Ltd.

- 6.4.14 Yandex N.V. (Yandex Music)

- 6.4.15 NetEase Cloud Music Inc.

- 6.4.16 Napster Group PLC

- 6.4.17 TIDAL Music AS

- 6.4.18 Qobuz SAS

- 6.4.19 Boomplay Music Group

- 6.4.20 Claro Musica (America Movil S.A.B. de C.V.)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment