|

시장보고서

상품코드

2062143

미국의 소매 물류 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)United States Retail Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

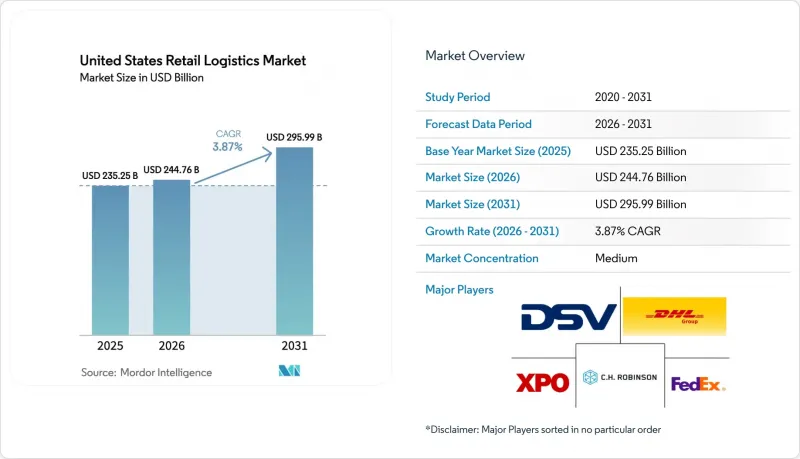

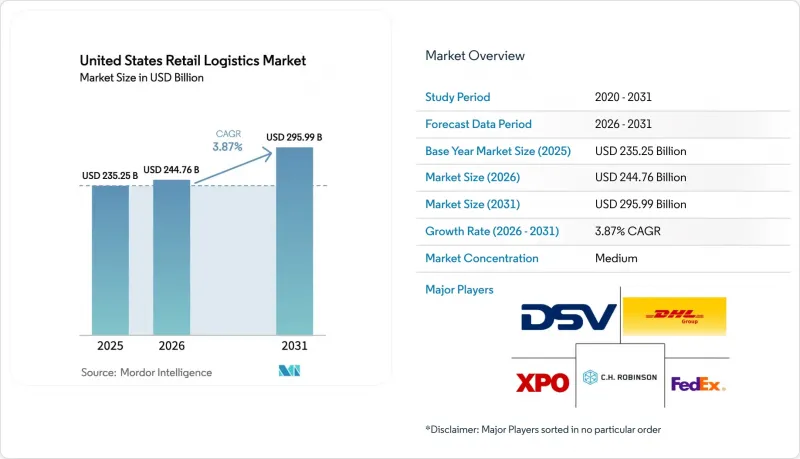

Mordor Intelligence에 의하면, 미국의 소매 물류 시장 규모는 2025년에 2,352억 5,000만 달러로 평가되었고 2026년 2,447억 6,000만 달러에서 2031년까지 2,959억 9,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 3.87%를 나타낼 전망입니다.

소매업체들은 매장을 물류 거점으로 전환하기 시작했으며, 복잡한 바이오의약품 파이프라인에 대응하기 위해 온도 관리 네트워크가 확대되고 있을 뿐만 아니라, 연방 정부의 그린 코리도(Green Corridor) 프로그램에 따라 장거리 운송 차량의 전기화 전환이 가속화되고 있습니다. 본 보고서는 서비스 유형(운송, 창고 및 물류, 기타), 온도 관리(상온, 냉장, 냉동, 비콜드체인), 제품 유형(식품 및 음료, 의류 및 신발, 가전제품, 헬스케어 및 의약품, 기타) 및 지역(북동부, 남동부, 남서부)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국 소매 물류 시장 동향과 인사이트

옴니채널 BOPIS(온라인 구매·매장 수령)의 확대

온라인 구매 및 매장 수령(BOPIS)은 디지털의 편의성과 오프라인 매장 네트워크를 결합함으로써 교외 소매 물류의 패러다임을 지속적으로 변화시키고 있습니다. 소매업체들은 전용 수령 구역, 커브사이드 레인, 신속한 주문 처리가 가능한 마이크로 풀필먼트용 백룸을 확보하기 위해 매장 레이아웃을 재설계하고 있습니다. 이 모델은 라스트 마일 배송 비용을 절감하는 동시에, 고객이 수령 시 추가 구매를 하는 경우가 많아 매장 방문객 수를 늘려줍니다. 대형 체인점들이 실시간 재고 현황 파악 및 원활한 앱 기반 주문 기능에 투자함에 따라 경쟁 압박이 심화되고 있으며, 고객들은 속도와 신뢰성에 대한 기대치를 높이고 있습니다. 그러나 현실은 중소 소매업체들이 이러한 기대에 부응하는 데 어려움을 겪는 경우가 많습니다. 교외 인구가 증가하고 전자상거래가 확산됨에 따라, BOPIS는 부가가치 서비스라기보다는 표준적인 주문 처리 옵션으로 자리 잡고 있습니다.

바이오의약품 주도의 초저온 수요

생물학적 제제, 세포 및 유전자 치료, mRNA 기반 치료법의 급속한 성장에 따라 특수한 초저온 보관 및 유통 인프라에 대한 수요가 증가하고 있습니다. 이러한 치료법은 종종 엄격한 온도 범위(경우에 따라 -70°C까지)를 요구하기 때문에 정교한 콜드체인 물류, 이중화된 전원 시스템, 그리고 엄격하게 모니터링되는 운송 네트워크가 필요합니다. 보스턴, 샌프란시스코, 리서치 트라이앵글 파크(RTP)와 같은 혁신 클러스터에서는 의료 서비스 제공업체 및 연구 기관을 위한 특수 온도 관리 창고와 라스트 마일 배송 솔루션에 대한 투자가 증가하고 있습니다. 또한, 민감한 바이오 의약품 취급의 복잡성은 물류 사업자들에게 실시간 추적, 예측 위험 관리, 규정 준수를 중시하는 업무 도입을 촉진하고 있으며, 이는 제약 공급망 전체의 고도화와 비용 구조의 변화를 가져오고 있습니다.

산업용 부동산의 낮은 공실률

인랜드 엠파이어, 댈러스-포트워스, 시카고, 뉴저지주 북부 등 주요 물류 허브에서 공실률이 낮은 수준을 유지하고 있어, 공급망 확장에 제약을 주고 있습니다. 사용 가능한 창고 공간이 사상 최저 수준에 머물러 있어, 임차인들은 임대료 상승, 입지 선택의 제한, 그리고 용량 확보까지 걸리는 리드타임의 장기화에 직면해 있습니다. 이러한 수급 불균형은 전자상거래 및 자동화에 적합한 현대적인 고천장 시설에서 특히 심각하며, 이러한 시설은 여전히 공급 부족 상태가 지속되고 있습니다. 그 결과, 임차인들은 최적의 입지라고 할 수 없는 곳이나 노후화된 건물을 선택할 수밖에 없게 되어, 물류 비효율화와 운영 비용 증가를 초래하고 있습니다. 단기적으로는 이러한 제약으로 인해 네트워크의 확장성이 제한되고 있으며, 특히 급성장 중인 소매업체나 제3자 물류(3PL) 업체의 경우 확장 계획에 차질이 발생하고 있습니다.

부문별 분석

운송 서비스는 2025년 미국 소매 물류 시장 점유율의 60.26%를 차지했습니다. 부가가치 서비스, 키팅, 역물류, 라벨링은 연평균 성장률(CAGR) 6.66%로 증가하고 있으며, 이는 소매업체들이 차별화된 주문 처리 방식으로 전환하고 있음을 반영합니다. 통합된 파트너십을 통해 운송, 창고 보관, 맞춤화가 하나의 패키지로 제공되어, 인계 횟수가 줄어들고 가시성이 향상되었습니다.

창고 운영사는 물류 허브 내에 간이 제조 스테이션, 반품 센터 및 패키지 단위의 맞춤화 기능을 통합하고 있습니다. 배송 정확성이나 반품 처리 속도 같은 고객 경험 지표가 고객 충성도로 직결되기 때문에 브랜드 기업들은 이러한 서비스에 대해 추가 비용을 지불하고 있습니다. 이러한 변화로 인해 창고는 비용 센터에서 밸류체인 내에서 가치를 창출하는 거점으로 변모하고 있습니다. 그 결과, 속도, 맞춤형 서비스, 데이터 가시성을 통합할 수 있는 운영 사업자는 B2B 시장과 D2C(소비자 직접 판매) 시장 모두에서 경쟁 우위를 확보하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19According to Mordor Intelligence, the united states retail logistics market size was valued at USD 235.25 billion in 2025 and is estimated to grow from USD 244.76 billion in 2026 to reach USD 295.99 billion by 2031, at a CAGR of 3.87% during the forecast period (2026-2031).

Retailers have begun converting stores into fulfillment nodes, temperature-controlled networks are expanding to serve complex biologics pipelines, and federal green-corridor programs are accelerating the shift toward electric line-haul fleets. This report is Segmented by Service Type (Transportation, Warehousing & Distribution, and More), by Temperature-Control (Ambient, Chilled, Frozen, Non Cold Chain), by Product Type (Food and Beverages, Apparel and Footwear, Electronic Appliances, Healthcare & Pharmaceuticals, and More), and by Region (Northeast, Southeast, Southwest). The Market Forecasts are Provided in Terms of Value (USD).

United States Retail Logistics Market Trends and Insights

Omnichannel BOPIS (Buy-Online-Pick-Up-In-Store) Expansion

Buy-online-pick-up-in-store (BOPIS) continues to reshape suburban retail logistics by blending digital convenience with physical store networks. Retailers are increasingly redesigning store footprints to accommodate dedicated pickup zones, curbside lanes, and micro-fulfillment backrooms that enable rapid order staging. This model reduces last-mile delivery costs while increasing store traffic, as customers frequently make incremental purchases during pickup visits. The competitive pressure is intensifying as large chains invest in real-time inventory visibility and seamless app-based ordering, raising customer expectations for speed and reliability capabilities that smaller retailers often struggle to match. As suburban populations grow and e-commerce penetration deepens, BOPIS is becoming a default fulfillment option rather than a value-added service.

Biologics-Led Ultra-Cold Demand

The rapid growth of biologic drugs, cell and gene therapies, and mRNA-based treatments is driving demand for specialized ultra-cold storage and distribution infrastructure. These therapies often require strict temperature ranges, sometimes as low as -70°C, creating a need for advanced cold chain logistics, redundant power systems, and highly monitored transportation networks. Innovation clusters such as Boston, San Francisco, and Research Triangle Park (RTP) are seeing increased investment in temperature-controlled warehousing and last-mile delivery solutions tailored to healthcare providers and research institutions. The complexity of handling sensitive biologics is also pushing logistics providers to adopt real-time tracking, predictive risk management, and compliance-focused operations, elevating the overall sophistication and cost structure of pharmaceutical supply chains.

Industrial Real Estate Vacancy Lows

Persistently low vacancy rates across major logistics hubs such as the Inland Empire, Dallas-Fort Worth, Chicago, and Northern New Jersey are constraining supply chain expansion. With available warehouse space at historic lows, tenants face rising lease rates, limited location choice, and longer lead times for securing capacity. This imbalance is particularly acute for modern, high-clearance facilities suited for e-commerce and automation, which remain in short supply. As a result, occupiers are forced into suboptimal locations or older assets, increasing transportation inefficiencies and operating costs. In the short term, these constraints limit network scalability and delay expansion plans, especially for fast-growing retailers and third-party logistics providers.

Other drivers and restraints analyzed in the detailed report include:

- Near-shoring & "Made in USA" Incentives

- Real-Time Freight Visibility Platforms

- Rising Cargo Theft & Insurance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation services generated 60.26% of the 2025 United States retail logistics market share. Value-added offerings, kitting, reverse logistics, and labeling are increasing at 6.66% CAGR, reflecting retailers' shift toward differentiated fulfillment. Integrated partnerships now bundle transportation, warehousing, and customization, reducing hand-offs and improving visibility.

Warehouse operators embed light-manufacturing stations, returns centers, and package-level personalization inside distribution hubs. Brands pay premiums for these capabilities because customer experience metrics such as delivery accuracy and returns turnaround directly drive loyalty. This shift is transforming warehouses from cost centers into value-generating nodes within the supply chain. As a result, operators who can integrate speed, customization, and data visibility are gaining a competitive edge in both B2B and direct-to-consumer markets.

List of Companies Covered in this Report:

- UPS

- FedEx

- DHL Group

- C.H. Robinson

- XPO Inc.

- GXO Logistics

- Ryder System

- J.B. Hunt

- Schneider National

- Lineage Logistics

- Americold

- Penske Logistics

- Kuehne+Nagel

- DSV

- GEODIS

- NFI Industries

- Xpress Global Systems (XGS)

- Kenco Logistics

- Marten Transport

- CMA CGM Group (CEVA Logistics)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Omnichannel "Buy-Online-Pick-Up" (BOPIS) Network Expansion

- 4.2.2 Biologics-Led Surge in Temperature-Controlled Pharma Shipments

- 4.2.3 Near-Shoring and Federal "Made In USA" Incentives Boosting Domestic Inventory Nodes

- 4.2.4 Widespread Roll-Out of Real-Time Freight-Visibility Platforms

- 4.2.5 Retail Subscription/Loyalty Programs Driving Scheduled Delivery Volumes

- 4.2.6 Federal Funding for Zero-Emission Truck Corridors (IIJA Grants)

- 4.3 Market Restraints

- 4.3.1 Record-Low Industrial Real-Estate Vacancy in Core Metros

- 4.3.2 Escalating Cargo-Theft and Insurance Premiums

- 4.3.3 Cyber-Security Vulnerabilities in Cloud Logistics Stacks

- 4.3.4 Persistent Chassis Shortages at Rail and Port Intermodal Hubs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Service Type

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Air

- 5.1.1.3 Rail

- 5.1.1.4 Sea

- 5.1.2 Warehousing and Distribution

- 5.1.3 Value-Added Services and Others (Kitting, Packaging, Labeling)

- 5.1.1 Transportation

- 5.2 By Temperature-Control Requirement

- 5.2.1 Cold Chian

- 5.2.1.1 Ambient (15-25 °C)

- 5.2.1.2 Chilled (2-8 °C)

- 5.2.1.3 Frozen (Less than 0 °C)

- 5.2.2 Non Cold Chain

- 5.2.1 Cold Chian

- 5.3 By Product Type

- 5.3.1 Food and Beverages

- 5.3.2 Apparel and Footwear

- 5.3.3 Electronic Appliances

- 5.3.4 Healthcare and Pharmaceuticals

- 5.3.5 Furniture and Home Furnishings

- 5.3.6 Others

- 5.4 By Region (United States)

- 5.4.1 Northeast

- 5.4.2 Midwest

- 5.4.3 Southeast

- 5.4.4 Southwest

- 5.4.5 West

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 UPS

- 6.4.2 FedEx

- 6.4.3 DHL Group

- 6.4.4 C.H. Robinson

- 6.4.5 XPO Inc.

- 6.4.6 GXO Logistics

- 6.4.7 Ryder System

- 6.4.8 J.B. Hunt

- 6.4.9 Schneider National

- 6.4.10 Lineage Logistics

- 6.4.11 Americold

- 6.4.12 Penske Logistics

- 6.4.13 Kuehne+Nagel

- 6.4.14 DSV

- 6.4.15 GEODIS

- 6.4.16 NFI Industries

- 6.4.17 Xpress Global Systems (XGS)

- 6.4.18 Kenco Logistics

- 6.4.19 Marten Transport

- 6.4.20 CMA CGM Group (CEVA Logistics)