|

시장보고서

상품코드

2062173

다이 본더 장비 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Die Bonder Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

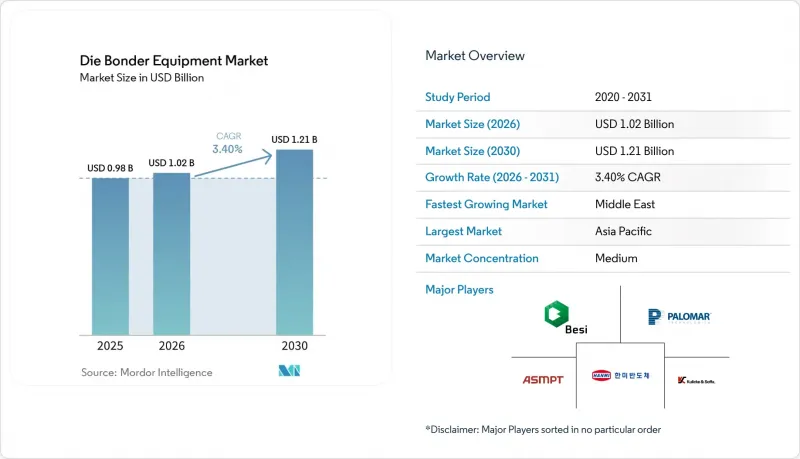

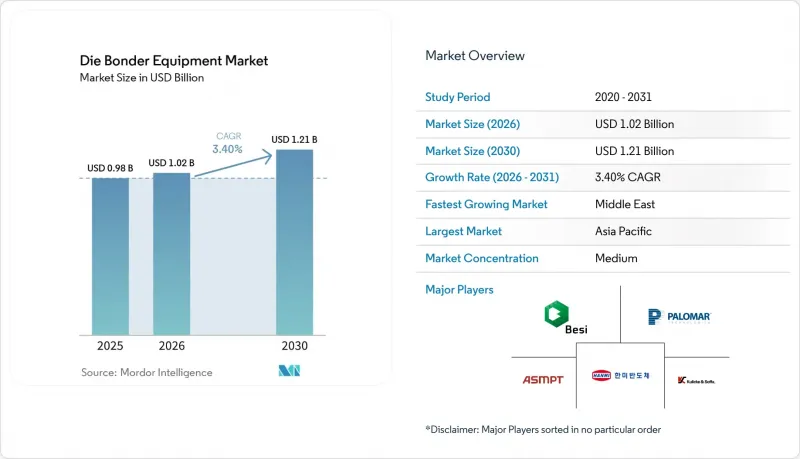

Mordor Intelligence에 의하면, 다이 본더 장비 시장 규모는 2025년 9억 8,000만 달러에서 2026년에는 10억 2,000만 달러로 확대되어 2031년까지 12억 1,000만 달러에 이를 것으로 예상되고 있어 2026년부터 2031년까지 CAGR 3.40%로 성장할 전망입니다.

본 보고서는 장비 유형(전자동 다이 본더 등), 본딩 기술(에폭시/접착제를 이용한 다이 어태치 등), 처리량 구분(6만 UPH 이상 등), 최종 이용 산업(집적 소자 제조업체 등), 소자 유형(로직 및 메모리 IC, 파워 및 RF 등), 그리고 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 다이 본더 장비 시장 동향 및 분석

이질적 통합과 치플렛의 붐

칩렛 분할을 통해 모놀리식 시스템 온 칩(SoC) 설계가, 미세 피치의 다이 간 링크로 연결된 더 작은 타일로 분할됩니다. 이로 인해 레티클 비용이 대폭 절감되고 수율이 향상되는 한편, 2µm 미만의 훨씬 더 엄격한 배치 정밀도가 요구됩니다. 치플렛 CPU의 초기 대량 출하를 통해 그 경제성이 입증됨에 따라, 수십 개의 와이어 대신 단일 본딩을 처리하는 열압축 플랫폼으로의 전환이 가속화되었습니다. 이를 통해 설비의 가동률이 향상되었으며, 더 많은 설비 투자가 정당화되었습니다. 유니버설 칩렛 인터커넥트 익스프레스(UCHI-Express)는 프로토콜 표준화를 추진하고 있으며, 이를 통해 2선급 디바이스 제조업체들도 첨단 패키징 기술을 활용할 수 있게 되어 다이 본더 장비 시장이 확대되고 있습니다. 공급업체들은 셋업 시간을 단축하고 초기 수율을 향상시키는 듀얼 갠트리 시스템, 간섭계 센서, 머신러닝 기반 정렬 엔진 등을 통해 이에 대응하고 있습니다. 고객에게 주는 이점은 프런트엔드의 미세화 속도가 둔화되더라도 경제적으로 무어의 법칙을 연장할 수 있는 믹스 앤 매치 설계 흐름을 구현할 수 있다는 점입니다.

선진적인 2.5D, 3D 및 하이브리드 본딩 기술 도입

하이브리드 본딩은 약 200°C에서 구리 패드와 유전체 층을 융합시켜 마이크로 범프를 제거하고, 연결 밀도를 10,000 링크/mm² 이상으로 높입니다. 이는 차세대 고대역폭 메모리 및 그래픽스 가속기에 있어 필수적인 요건입니다. 각 업체들은 구리 디싱을 5nm 미만으로, 오버레이 오차를 200nm 미만으로 억제하기 위해 웨이퍼 간 본더와 평탄화 공정의 공동 최적화를 추진하고 있습니다. 나노 트윈 구리의 도입으로 열 공정 범위가 확대되어, 유기 기판을 이용한 미세 피치의 3D 적층이 가능해지고 있습니다. 하이브리드 본딩 라인의 비용은 플립칩 라인보다 50-70% 높기 때문에 당초에는 수백만 달러 규모의 장비 세트를 대량 생산 프로그램을 통해 상각할 수 있는 최상위권 IDM이나 OSAT에 도입이 집중될 전망입니다. 2028년 이후 HBM 5세대의 양산이 본격화되면, 메모리 및 로직 공급망 전반에 걸쳐 소재 교체 열풍이 불어닥칠 것이며, 하이브리드 대응 다이 본더에 대한 수요가 가속화될 것입니다.

중견 OSAT 기업에게 있어 초고정밀 설비 투자의 부담

500nm 미만의 오버레이 정밀도를 갖춘 웨이퍼-투-웨이퍼 본더의 가격은 300만-500만 달러인 반면, 성숙 단계에 접어든 플립칩 장비는 100만-150만 달러로, 비용에 민감한 시장을 겨냥한 2차 공급업체들의 재무 상황을 압박하고 있습니다. 부수적인 계측 장비 및 클린룸 업그레이드에는 추가로 100만-200만 달러가 소요되며, 지역 은행의 대출 승인에 9개월이 걸릴 수 있어 확장 계획이 지연될 수 있습니다. 설비 구독 계약은 이러한 부담을 일부 상쇄해 주지만, 소규모 업체가 항상 충족시킬 수 있는 것은 아닌 생산량 보장이 수반됩니다. 그 결과, 최상위권과 중견 OSAT 간의 기술 격차가 확대되어 첨단 패키징 분야의 수익이 집중되는 한편, 업계 전반의 도입 속도가 제한될 것입니다.

부문별 분석

이 전동 시스템은 0.5초 미만의 사이클 타임을 실현하고, 비전, 힘 제어, 계측 기능을 통합하고 있어 대량 생산 라인의 로직 및 메모리 라인에서 주류로 자리 잡고 있습니다. 완전 자동화 플랫폼용 다이 본더 장비 시장 규모는 주요 IDM 및 OSAT 업체에서의 높은 보급률을 반영하고 있습니다. 반자동 장비는 혼합 툴링이 필요한 파워 및 고주파 패키지에 대응하는 반면, 수동 및 시제품용 스테이션은 연구 개발(R&D) 분야에서 여전히 중요한 역할을 수행하고 있습니다. 가장 빠르게 성장하고 있는 웨이퍼 간 본더는 픽 앤 플레이스 공정을 생략하고, 1mm²당 10,000개 이상의 연결 밀도를 구현함으로써 3D 칩렛 스택으로의 적용을 가능하게 하고 있습니다.

파운드리 업체들이 월 1,000장 이상의 웨이퍼를 처리할 수 있는 3D 집적 생산 라인을 확대함에 따라, 웨이퍼 레벨 장비에 대한 수요가 증가하고 있습니다. 각 공급업체들은 300mm 기판 전체에 걸친 오버레이 정밀도를 보장하기 위해 진공 핸들링, CMP 인터페이스, 인라인 검사 기능을 통합하여, 단순한 처리 속도가 아닌 공정 제어 측면에서 차별화를 꾀하고 있습니다. 실시간 광학 피드백을 통한 능동적인 정렬이 요구되는 포토닉스 분야에서는 여전히 수동 본더가 필수적입니다. 반자동 공구는 유연성과 비용의 균형을 고려하여 자동차 모듈 분야에서 틈새 시장을 개척하고 있습니다.

동 필러 어태치를 포함한 플립 칩은 그 성숙도와 유기 적층 기판과의 호환성 덕분에 가장 큰 시장 점유율을 차지하고 있습니다. 2028년 이후 하이브리드 본딩이 본격화되면, 플립 칩용 다이 본더 장비 시장 점유율은 점차 하락할 것으로 예측됩니다. 에폭시 접합은 비용과 열 설계상의 제약이 밀도보다 우선시되는 소비자용 및 산업용 디바이스에서 여전히 인기를 끌고 있는 반면, 공융 접합은 기밀성이 필수적인 항공우주 및 의료 분야에서 확고한 입지를 다지고 있습니다.

하이브리드 본딩의 전망은 2TB/s를 넘는 대역폭을 실현하기 위해 직접 구리-구리 연결로 전환하는 메모리 로드맵에 달려 있습니다. 각 업체들은 5nm 미만의 구리 디싱과 200nm 미만의 오버레이를 달성하기 위해 본더와 CMP 공정을 공동 개발하고 있습니다. 열압착 기술은 여전히 가교 기술로서의 위상을 유지하고 있으며, 이미 미세 피치 플립칩 및 고주파 모듈 분야에서 솔더 리플로우 공정을 대체하고 있습니다. 향후 비용 측면에서의 격차 해소와 고밀도화 수요에 힘입어 시장 점유율은 하이브리드 플랫폼으로 이동할 것이며, 다이 본더 장비 시장에서 직접 Cu-Cu 장비용 시장 규모가 확대될 것으로 보입니다.

지역별 분석

아시아태평양은 대만의 첨단 패키징 기술, 중국의 현지화 추진, 그리고 한국의 메모리 생산 기반을 바탕으로 전 세계 생산 능력의 절반 이상을 차지하고 있습니다. 미국의 정부 자금 투입으로 인해 2027년까지 가동을 시작할 것으로 예상되는 여러 후공정 파브(fab) 프로젝트가 추진되면서, 북미의 장비 출하 대수가 증가하고 있습니다. 유럽에서는 전기차 및 산업용 드라이브용 공급을 확보하기 위해 독일과 프랑스에서 화합물 반도체 패키징에 대한 투자가 진행되고 있습니다. 중동은 새로운 투자 지역으로 부상하고 있으며, 2028년 이후 첫 출하가 예정된 조립 공장에 정부 자금을 투입하고 있습니다.

아시아태평양의 장비 공급업체들은 지리적 근접성으로 인한 이점, 서비스 주기 단축, 그리고 현지 조달을 장려하는 정부의 인센티브를 누리고 있습니다. 북미 시장의 구매 경향은 하이브리드 본딩 및 웨이퍼 간 적층 공정에 대응하는 고정밀·고자동화 장비에 쏠려 있습니다. 유럽 시장은 파워 모듈용 은 소결 및 구리 클립 지원 플랫폼을 선호하고 있습니다. 중동의 주문은 생태계 구축을 가속화하기 위한 교육 프로그램이 포함된 턴키 라인을 중시하고 있습니다. 남미와 아프리카는 여전히 초기 단계에 머물러 있으며, 학술 기관이나 시제품 생산 설비의 도입에 국한되어 있습니다.

생산 능력 확대는 공급망 전반에 파급되고 있습니다. 대만의 확장만으로도 50대 이상의 웨이퍼 간 본더가 필요한 것으로 파악되며, 미국의 CHIPS법에 따른 수주 물량으로 인해 공급업체의 예약 일정은 수개월 앞까지 이미 꽉 차 있습니다. 중국의 신규 진출기업들은 성숙 단계에 접어든 플립칩용 장비의 가격보다 낮은 가격을 제시하고 있지만, 첨단 장비는 여전히 주로 기존 세계 브랜드에서 공급되고 있습니다. 반도체 공급의 지역화로 인해 공급업체들은 현지 지원 팀, 창고, 재생 센터를 확충해야 하는 상황에 직면해 있으며, 고정 비용은 증가하고 있지만 고객의 가동 중단 시간은 단축되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19According to Mordor Intelligence, the die bonder equipment market size is expected to increase from USD 0.98 billion in 2025 to USD 1.02 billion in 2026 and reach USD 1.21 billion by 2031, growing at a CAGR of 3.40% over 2026-2031.

This report is Segmented by Equipment Type (Fully-Automatic Die Bonders, and More), Bonding Technology (Epoxy/Adhesive Die Attach, and More), Throughput Category (Greater Than 60k UPH, and More), End-Use Industry (Integrated Device Manufacturers, and More), Device Type (Logic and Memory IC, Power and RF, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Die Bonder Equipment Market Trends and Insights

Heterogeneous-Integration and Chiplet Boom

Chiplet partitioning breaks monolithic system-on-chip designs into smaller tiles connected by fine-pitch die-to-die links, slashing reticle cost and improving yield while demanding placement accuracy tighter than 2 µm. Early high-volume shipments of chiplet CPUs validated the economics and triggered a shift from wire bonding toward thermocompression platforms that process one bond instead of dozens of wires, raising tool utilization and justifying higher capital outlays. Universal Chiplet Interconnect Express is standardizing protocols, making advanced packaging accessible to second-tier device makers and expanding the die bonder equipment market. Suppliers are responding with dual-gantry systems, interferometric sensors, and machine-learning alignment engines that cut setup time and improve first-pass yield. The payoff for customers is a mix-and-match design flow that extends Moore's Law economically even as front-end scaling slows.

Advanced 2.5D 3D And Hybrid Bonding Adoption

Hybrid bonding fuses copper pads and dielectric layers at around 200 °C, eliminating microbumps and lifting connection density above 10,000 links mm-2, a prerequisite for next-generation high-bandwidth memory and graphics accelerators. Tool vendors are co-optimizing wafer-to-wafer bonders with planarization steps to keep copper dishing below 5 nm and overlay error under 200 nm. Nanotwinned copper is widening the thermal process window, making organic substrates viable for fine-pitch 3D stacking. Because hybrid-bonding lines cost 50-70% more than flip-chip lines, adoption is initially concentrated at top-tier IDMs and OSATs that can amortize multi-million-dollar tool sets across high-volume programs. Once HBM generation 5 ramps after 2028, a material replacement wave will cascade through memory and logic supply chains, accelerating demand for hybrid-ready die bonders.

Ultra-High-Precision CapEx Burden For Mid-Tier OSATs

A wafer-to-wafer bonder with sub-500 nm overlay costs USD 3-5 million versus USD 1-1.5 million for a mature flip-chip tool, stretching balance sheets at second-tier providers that serve cost-sensitive markets. Ancillary metrology and cleanroom upgrades add another USD 1-2 million, and financing from regional banks can take nine months to approve, delaying expansion plans. Equipment-as-a-service contracts partly offset the burden but come with volume guarantees that smaller players cannot always meet. The result is a widening technology gap between top-tier and mid-tier OSATs, concentrating advanced-packaging revenue and limiting industry-wide adoption speed.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Uptake of Compound-Semiconductor Power Devices

- Data-Center Photonics and Co-Packaged Optics Demand

- Sub-Micron Alignment Yield-Loss Risk

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fully automatic systems dominate high-volume logic and memory lines because they deliver sub-0.5 s cycle times and integrate vision, force control, and metrology. The die bonder equipment market size for fully automatic platforms reflects deep penetration among large IDMs and OSATs. Semi-automatic machines serve power and radio-frequency packages that require mixed tooling, while manual and prototype stations stay relevant in R and D. Wafer-to-wafer bonders, growing fastest, eliminate pick-and-place steps and enable connection densities above 10,000 links mm-2, positioning them for 3D chiplet stacks.

Demand for wafer-level machines is rising as foundries scale 3D integration lines capable of more than 1,000 wafers a month. Suppliers bundle vacuum handling, CMP interfaces, and inline inspection to guarantee overlay across 300 mm substrates, differentiating on process control rather than raw speed. Manual bonders remain indispensable for photonics where active alignment with live optical feedback is required. Semi-automatic tools find a niche in automotive modules, balancing flexibility and cost.

Flip-chip, including copper-pillar attach, commands the largest slice thanks to its maturity and compatibility with organic laminates. The die bonder equipment market share for flip-chip is expected to erode slowly as hybrid bonding ramps after 2028. Epoxy attach stays popular in consumer and industrial devices where cost and thermal budget trump density, while eutectic attach secures aerospace and medical applications that mandate hermeticity.

Hybrid bonding's momentum hinges on memory roadmaps that move to direct copper-to-copper links for bandwidth beyond 2 TB s-1. Vendors co-develop bonders and CMP steps to hit <5 nm copper dishing and <200 nm overlay. Thermocompression remains the bridge technology, already displacing solder reflow in fine-pitch flip-chip and radio-frequency modules. Over time, cost parity and density demands will swing share toward hybrid platforms, expanding the die bonder equipment market size for direct Cu-Cu tools.

Geography Analysis

Asia-Pacific anchors more than half of global capacity, underpinned by Taiwan's advanced packaging, China's localization push, and South Korea's memory footprint. Government funding in the United States spurs multiple back-end fabs expected online by 2027, lifting North American equipment shipments. Europe invests in compound-semiconductor packaging in Germany and France to secure supply for electric vehicles and industrial drives. The Middle East emerges as a greenfield investor, channelling sovereign capital into assembly plants slated for first output after 2028.

Tool vendors in Asia-Pacific enjoy proximity advantages, shorter service cycles, and government incentives that subsidize local sourcing. North American purchases skew toward high-precision, high-automation tools compatible with hybrid bonding and wafer-to-wafer stacking. European demand favours silver-sinter and copper-clip compatible platforms for power modules. Middle East orders emphasize turnkey lines bundled with training to expedite ecosystem buildup. South America and Africa remain nascent, limited to academic and prototype installations.

Capacity moves ripple through supply chains: Taiwan's expansion alone requires more than 50 wafer-to-wafer bonders, and U.S. CHIPS Act awards reserve slots at suppliers' months ahead. Chinese entrants undercut pricing on mature flip-chip tools, but advanced equipment still flows mainly from incumbent global brands. Regionalization of semiconductor supply pushes tool vendors to expand local support teams, warehouses, and refurbish centers, raising fixed cost but shortening downtime for customers.

- ASMPT Ltd.

- Kulicke and Soffa Industries Inc.

- BE Semiconductor Industries N.V.

- Hanmi Semiconductor Co., Ltd.

- Palomar Technologies Inc.

- SHINKAWA Ltd.

- Panasonic Holdings Corp. (Factory Solutions)

- SUSS MicroTec SE

- Toray Engineering Co., Ltd.

- TOWA Corporation

- West-Bond Inc.

- MRSI Systems (Mycronic AB)

- Finetech GmbH & Co. KG

- Canon Machinery Inc.

- DIAS Automation (Shenzhen) Co., Ltd.

- F&K Delvotec Bondtechnik GmbH

- Tresky AG

- Hybond Inc.

- Integra Technologies LLC

- EV Group (EVG)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Heterogeneous-Integration and Chiplet Boom

- 4.2.2 Advanced 2.5D/3D and Hybrid Bonding Adoption

- 4.2.3 Rapid Uptake of Compound-Semiconductor Power Devices

- 4.2.4 Data-Center Photonics and Co-Packaged Optics Demand

- 4.2.5 Government On-Shoring Subsidies for Back-End Fabs

- 4.2.6 Industry 4.0 Push for Fully-Automatic High-UPH Bonders

- 4.3 Market Restraints

- 4.3.1 Ultra-High-Precision CapEx Burden for Mid-Tier OSATs

- 4.3.2 Sub-Micron Alignment Yield-Loss Risk

- 4.3.3 Precision Component Supply-Chain Bottlenecks

- 4.3.4 Fast Technology Obsolescence Risk in Bonding Tools

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Equipment Type

- 5.1.1 Fully-Automatic Die Bonders

- 5.1.2 Semi-Automatic Die Bonders

- 5.1.3 Manual / Prototype Bonders

- 5.1.4 Wafer-to-Wafer Bonders

- 5.2 By Bonding Technology

- 5.2.1 Epoxy / Adhesive Die Attach

- 5.2.2 Eutectic Die Attach

- 5.2.3 Flip-Chip (C4/Cu-Pillar)

- 5.2.4 Thermocompression and Thermosonic

- 5.2.5 Hybrid and Direct Cu-Cu Bonding

- 5.3 By Throughput Category (Units per Hour)

- 5.3.1 Greater Than 60 k UPH (High-Speed)

- 5.3.2 30-60 k UPH (Mid-Speed)

- 5.3.3 Below 30 k UPH (Low-Speed / High-Precision)

- 5.4 By End-Use Industry

- 5.4.1 Integrated Device Manufacturers (IDMs)

- 5.4.2 Outsourced Semiconductor Assembly and Test (OSATs)

- 5.4.3 Research and Prototyping Labs

- 5.5 By Device Type

- 5.5.1 Logic and Memory IC

- 5.5.2 Power and RF (SiC, GaN)

- 5.5.3 Photonics / Optical Transceivers

- 5.5.4 MEMS and Sensors

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 South Korea

- 5.6.4.4 India

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ASMPT Ltd.

- 6.4.2 Kulicke and Soffa Industries Inc.

- 6.4.3 BE Semiconductor Industries N.V.

- 6.4.4 Hanmi Semiconductor Co., Ltd.

- 6.4.5 Palomar Technologies Inc.

- 6.4.6 SHINKAWA Ltd.

- 6.4.7 Panasonic Holdings Corp. (Factory Solutions)

- 6.4.8 SUSS MicroTec SE

- 6.4.9 Toray Engineering Co., Ltd.

- 6.4.10 TOWA Corporation

- 6.4.11 West-Bond Inc.

- 6.4.12 MRSI Systems (Mycronic AB)

- 6.4.13 Finetech GmbH & Co. KG

- 6.4.14 Canon Machinery Inc.

- 6.4.15 DIAS Automation (Shenzhen) Co., Ltd.

- 6.4.16 F&K Delvotec Bondtechnik GmbH

- 6.4.17 Tresky AG

- 6.4.18 Hybond Inc.

- 6.4.19 Integra Technologies LLC

- 6.4.20 EV Group (EVG)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment