|

시장보고서

상품코드

2062184

골판지 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)Corrugated Board - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

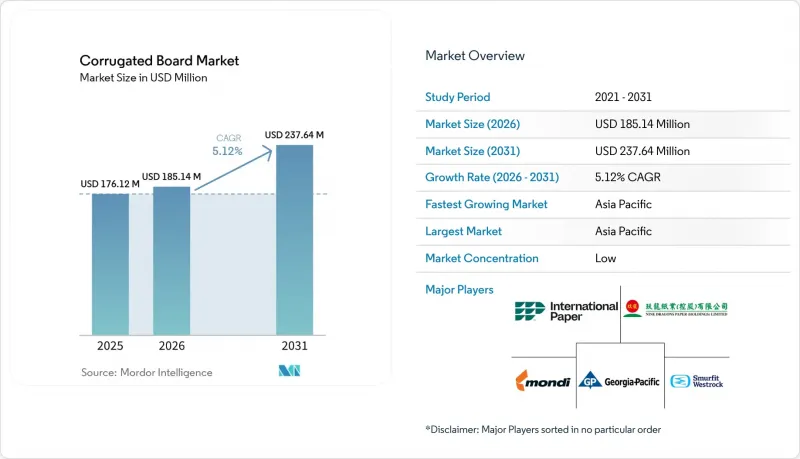

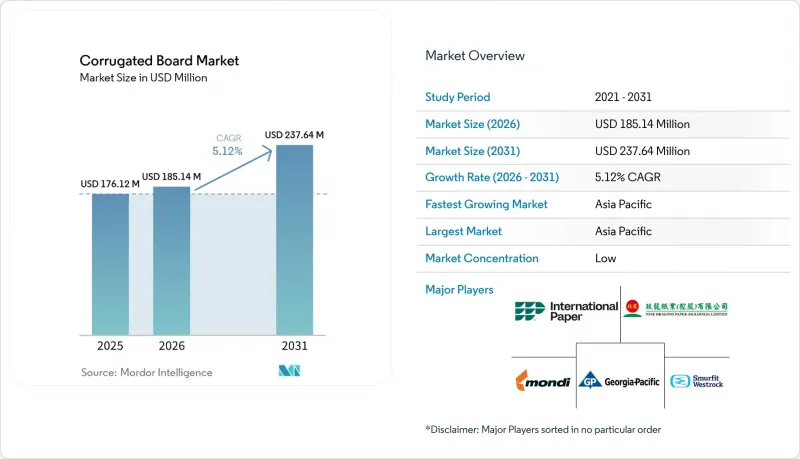

Mordor Intelligence에 의하면, 골판지 시장 규모는 2025년에 1억 7,612만 달러로 평가되었습니다. 2026년에 1억 8,514만 달러에서 2031년까지 2억 3,764만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR은 5.12%를 나타낼 전망입니다.

본 보고서는 골판지의 유형(단층, 2층, 3층), 재료의 유형(라이너보드, 중심, 재생 섬유, 버진 섬유), 최종 사용자 산업(식품 및 음료, 전자상거래·소매, 소비자용 전자기기 등), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 골판지 시장 동향 및 인사이트

전자상거래 출하량의 폭발적인 성장

Packsize사와 Panotec사의 통합형 최적 크기 조정 시스템은 SKU의 치수를 기준으로 5mm 이내의 정밀도로 컨테이너보드를 절단하고, 빈 공간을 최대 40%까지 줄임으로써 전 세계 택배 업체의 부피 중량 할증 요금을 절감합니다. 2025년 중국의 종이 포장재 수출량은 127만 4,503 컨테이너에 달하고, 인도의 27만 2,348 컨테이너를 크게 웃돌며 이 지역의 인프라가 얼마나 잘 갖춰져 있는지를 여실히 보여주었습니다. 캐논과 도미노의 QR 코드 지원 싱글 패스 디지털 인쇄기는 현재 B 플루트 및 E 플루트 골판지 상자를 분당 200미터의 속도로 맞춤 제작하여, 배송용 상자를 마케팅 자산으로 탈바꿈시키고 있습니다. 이러한 발전들이 맞물리면서, 골판지 시장은 대륙을 넘나드는 소포 처리량의 확대에 발맞추어 계속 성장하고 있습니다.

종이 재활용을 촉진하는 지속가능성 규제

EU의 ‘포장 및 포장 폐기물 규정(2025/40)’은 2030년까지 종이 회수율 85%를 의무화하고, 2030년까지 재활용이 불가능한 형태를 금지하고 있어, 이에 따라 재생 라이너보드 수요가 증가하고 있습니다. 캘리포니아주, 메인주, 오리건주 등 미국 각 주에서는 2024년부터 2026년에 시행될 확대 생산자 책임 제도를 통해 재활용 비용을 브랜드 소유자에게 전가하고, 조달을 회수율이 높은 원자재로 유도하고 있습니다. 2017년 이후 총 360만 톤의 재생 섬유 생산 능력이 추가됨에 따라, 컨테이너보드의 탄소 집약도는 이미 최대 20%까지 감소했습니다. 2026년 1월부터 시행되는 식품 접촉용 포장재에 대한 PFAS 금지 조치로 인해, 수성 코팅이 적용된 피자용 및 테이크아웃용 골판지 상자에 대한 수요가 더욱 증가하고 있습니다. ISO 14001 인증과 산림 공급망의 추적 가능성은 현재 거의 모든 다국적 기업의 조달 입찰 요건에 포함되어 있으며, 지속가능성은 경쟁상의 필수 요건으로 자리 잡아가고 있습니다.

유연성이 뛰어난 플라스틱 메일러와의 경쟁

2025년, 폴리에틸렌 소재의 메일백은 북미 경량 소포 시장의 8-12%를 차지했으며, 2kg 미만 중량대에서 단층 골판지 상자에 비해 30-40%의 비용 절감을 실현했습니다. 치수별 배송비 체계 덕분에 의류의 형태에 딱 맞는 유연한 파우치가 유리해져, 주택으로의 배송 시 0.50-1달러를 절약할 수 있게 되었습니다. 그러나 메인주, 오리건주, 콜로라도주에서는 현재 플라스틱 우편 봉투 1장당 0.02-0.05달러의 재활용 수수료가 부과되고 있어 경제성이 떨어지고 있는 만큼, 아마존은 가정 쓰레기로 재활용이 가능한 섬유가 혼합된 우편 봉투의 시범 도입을 추진하고 있습니다. EU의 일회용 플라스틱 지침 역시 이와 유사한 EPR(생산자 책임) 과세를 도입하고 있어, 각 브랜드 기업들은 자동 분류의 엄격한 요건을 충족하는 두께가 불과 1.5mm에 불과한 마이크로플루트 골판지로 전환해야 하는 상황에 직면해 있습니다. 메일러와 동일한 두께를 확보할 수 있는 골판지 가공업체들은 그렇지 않았다면 플라스틱에 빼앗겼을 수요를 되찾고 있습니다.

부문별 분석

2025년에는 싱글월이 매출의 49.11%를 차지했으나, 가전제품 운송업체들이 두 개의 골판지 상자를 하나의 보강 유닛으로 통합했음에도 불구하고 아마존의 ‘Frustration-Free 2.0’ 기준을 충족하기 위해, 더블월은 2031년까지 연평균 성장률(CAGR) 5.43%로 성장하고 있습니다. 3층 구조는 1,000 kPa를 초과하는 파열 강도가 필요한 화학약품 드럼이나 자동차 부품과 같은 틈새 시장에 국한되어 있습니다. 전자기기 분야에서는 AC 플루트를 대체하기 위해 설계된 BC 플루트가 채택되어, 충격으로 인한 손상을 최대 40%까지 줄이고 진열 시 외관을 개선하고 있습니다.

마이크로플루트의 E형 및 F형 프로파일은 고해상도 오프셋 인쇄와 견고한 마이크로 카톤의 제조를 가능하게 하여, 화장품 및 의약품 분야에 점차 확산되고 있습니다. 스마핏 웨스트록사는 2024년에 기존의 C-플루트 생산 능력 60만 톤을 폐쇄하는 동시에, 프리미엄 D2C(소비자 직접 판매) 채널을 위한 B-플루트 설비 업그레이드에 자금을 투입했습니다. 골판지 사용량을 줄이고 강도를 높임으로써 운송 부피를 절감하고, 지속가능성 목표에도 부합하기 때문에 골판지 시장에서 2층 구조에 대한 수요는 견조한 추세를 보이고 있습니다.

지역별 분석

아시아태평양은 2025년에 매출의 50.24%를 차지했으며, 중국의 거대한 수출 기반과 인도의 PLI(생산 연계형 인센티브) 주도의 전자기기 클러스터에 힘입어 2031년까지 연평균 성장률(CAGR) 5.88%를 기록하며 성장할 것으로 전망됩니다. 일본의 렌고는 2025년에 독일에 중량용 골판지 공장을 설립하며, 유럽의 자동차 제조업체 고객들에게 서비스를 제공하기 위한 해외 투자를 강화했습니다. 한국의 컨테이너 수출은 한국이 전자제품 포장 허브로서의 역할을 수행하고 있음을 뒷받침하고 있습니다.

북미에서는 라이너보드 가격 상승에 직면해 있지만, 아마존의 물류 센터 확충과 멕시코에서의 니어쇼어 생산의 혜택을 받고 있습니다. 인터내셔널 페이퍼가 99억 달러 규모로 DS 스미스를 인수함에 따라, 대서양을 아우르는 사업 규모 확대와 5억 1,400만 달러의 수익을 창출하게 됩니다. 총 400만 톤에 달하는 생산 능력의 가동 중단으로 인해 공급 부족 상황이 지속되면서, 엄격한 가격 책정이 강화되고 있습니다.

유럽에서는 PPWR(플라스틱 포장 재활용 의무) 및 CBAM(탄소 국경 조정 메커니즘)에 따른 과세 문제로 골머리를 앓고 있습니다. 몬디(Mondi)가 스테티(Steti)와 두이노(Duino)에 12억 유로를 투자한 것은 저탄소화 추세에 부합하는 조치인 반면, 슈마허(Schumacher)를 6억 3,400만 유로에 인수함으로써, 고급 컨버터 시장 진출을 가속화할 것입니다. 스토라 엔소(Stora Enso)의 오울루(Oulu)에 위치한 연간 75만 톤 규모의 판지 생산 라인과 같은 북유럽의 제지 공장들은 통합 펄프 사업을 통해 에너지 효율을 높이고 있습니다. 남미는 크라빈의 ‘푸마 II’를 통한 수출 흐름의 혜택을 누리고 있는 반면, 중동에서는 ‘비전 2030’ 인프라 계획에 발맞추어 산업용 골판지의 생산 능력을 확충하고 있습니다. 이러한 지역별 동향이 복합적으로 작용하여 골판지 시장 동향에 영향을 미치고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장률 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the corrugated board market size is projected to be USD 176.12 million in 2025, USD 185.14 million in 2026, and reach USD 237.64 million by 2031, growing at a CAGR of 5.12% from 2026 to 2031.

This report is Segmented by Board Type (Single-Wall, Double-Wall, and Triple-Wall), Material Type (Linerboard, Medium, Recycled Fiber, and Virgin Fiber), End-User Industry (Food and Beverage, E-Commerce and Retail, Consumer Electronics, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Corrugated Board Market Trends and Insights

Explosive Growth of E-Commerce Shipments

Integrated right-sizing systems from Packsize and Panotec cut board blanks within 5 millimeters of SKU dimensions, lowering void fill by up to 40% and reducing dimensional-weight surcharges levied by global couriers. China's export of 1,274,503 containers of paper packaging in 2025 dwarfed India's 272,348 tally, underscoring the region's infrastructure depth. QR-coded single-pass digital presses from Canon and Domino now personalize B-flute and E-flute cartons at 200 meters per minute, turning shipping boxes into marketing assets. These advances collectively keep the corrugated board market aligned with parcel-volume expansion across continents.

Sustainability Regulations Favouring Paper Recycling

The EU's Packaging and Packaging Waste Regulation 2025/40 mandates 85% collection for paper by 2030 and bans non-recyclable formats by 2030, escalating demand for recycled linerboard. U.S. states such as California, Maine, and Oregon shifted recycling costs to brand owners via extended producer responsibility schemes effective 2024-2026, steering procurement toward high-recovery substrate. Recycled-fiber capacity additions totaling 3.6 million tons since 2017 have already lowered containerboard carbon intensity by up to 20. PFAS bans in food-contact packaging, effective January 2026, further boost aqueous-coated corrugated pizza and take-out boxes. ISO 14001 certification and forest-chain traceability now appear in nearly every multinational procurement tender, embedding sustainability as a competitive necessity.

Competition from Flexible Plastic Mailers

Polyethylene mailers captured 8-12% of North American lightweight parcels in 2025, delivering 30-40% cost savings against single-wall corrugated in sub-2 kg bands. Dimensional shipping charges favor flexible pouches that hug apparel contours, saving USD 0.50-1.00 on residential deliveries. Yet Maine, Oregon, and Colorado now assess USD 0.02-0.05 recycling fees per plastic mailer, narrowing economics and prompting Amazon to test fiber-padded mailers eligible for curbside recycling. The EU Single-Use Plastics Directive layers similar EPR levies, nudging brands toward micro-flute cartons as thin as 1.5 millimeters that meet automated sortation rigors. Corrugated converters that match mailer thickness reclaim volumes otherwise lost to plastic.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Food and Beverage Distribution in Emerging Markets

- Shift Toward Lightweight, Cost-Efficient Packaging

- Carbon Border Taxes on Paper Exports

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Single-wall held 49.11% revenue in 2025, yet double-wall is growing at a 5.43% CAGR to 2031 as appliance shippers consolidate two cartons into one reinforced unit that still meets Amazon's Frustration-Free 2.0 metrics. Triple-wall remains niche for chemical drums and auto parts requiring burst strength above 1,000 kPa. Engineered BC-flute replaces AC-flute in electronics, trimming impact damage by up to 40% and enhancing shelf presentation.

Micro-flute E- and F-profiles are penetrating cosmetics and pharma because they permit high-definition litho and rigid micro-cartons. Smurfit Westrock shuttered 600,000 tons of legacy C-flute capacity in 2024 while funding B-flute upgrades that serve premium direct-to-consumer channels. Fewer, stronger cartons reduce freight cube and align with sustainability goals, giving double-wall formats durable tailwinds inside the corrugated board market.

Geography Analysis

Asia-Pacific commanded 50.24% of revenue in 2025 and is projected to grow at a 5.88% CAGR through 2031, lifted by China's vast export base and India's PLI-driven electronics clusters. Japan's Rengo opened a heavy-duty plant in Germany in 2025, underscoring outbound investments aimed at serving European auto clients. South Korea's container exports back its role as electronics-packaging hub.

North America faces linerboard price hikes yet benefits from Amazon's fulfillment build-out and nearshored Mexican manufacturing. International Paper's USD 9.9 billion DS Smith deal adds transatlantic scale and USD 514 million. Capacity closures totaling 4 million tons keep supply tight, reinforcing disciplined pricing.

Europe grapples with PPWR recyclability mandates and CBAM levies. Mondi's EUR 1.2 billion capex at Steti and Duino aligns with low-carbon trends, while its EUR 634 million acquisition of Schumacher accelerates access to premium converters. Nordic mills like Stora Enso's Oulu 750,000 tpa board line capitalize on integrated pulp energy efficiencies. South America benefits from Klabin's Puma II export flows, whereas the Middle-East builds industrial carton capacity for Vision 2030 infrastructure. These regional dynamics jointly influence the corrugated board market trajectory.

- Georgia-Pacific LLC

- International Paper

- Klabin S.A.

- Mondi

- Nine Dragons Worldwide (China) Investment Group Co., Ltd.

- NIPPON PAPER INDUSTRIES CO., LTD.

- Oji Holdings Corporation

- Ondupack

- Packaging Corporation of America

- Pratt Industries, Inc.

- Rengo Co., Ltd.

- Saica

- Smurfit Westrock

- Stora Enso

- Thai Containers Group Co., Ltd.

- Visy

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Explosive Growth of E-Commerce Shipments

- 4.2.2 Sustainability Regulations Favouring Paper Recycling

- 4.2.3 Expansion of Food and Beverage Distribution in Emerging Markets

- 4.2.4 Shift Toward Lightweight, Cost-Efficient Packaging

- 4.2.5 On-Demand Digital Printing Custom Packs

- 4.3 Market Restraints

- 4.3.1 Kraft Linerboard Price Volatility

- 4.3.2 Competition from Flexible Plastic Mailers

- 4.3.3 Carbon Border Taxes on Paper Exports

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Board Type

- 5.1.1 Single-wall

- 5.1.2 Double-wall

- 5.1.3 Triple-wall

- 5.2 By Material Type

- 5.2.1 Linerboard

- 5.2.2 Medium

- 5.2.3 Recycled Fiber

- 5.2.4 Virgin Fiber

- 5.3 By End-user Industry

- 5.3.1 Food and Beverage

- 5.3.2 E-commerce and Retail

- 5.3.3 Consumer Electronics

- 5.3.4 Personal Care and Household

- 5.3.5 Industrial and Heavy-Duty

- 5.3.6 Pharmaceuticals and Healthcare

- 5.3.7 Other (Furniture, Agriculture, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Georgia-Pacific LLC

- 6.4.2 International Paper

- 6.4.3 Klabin S.A.

- 6.4.4 Mondi

- 6.4.5 Nine Dragons Worldwide (China) Investment Group Co., Ltd.

- 6.4.6 NIPPON PAPER INDUSTRIES CO., LTD.

- 6.4.7 Oji Holdings Corporation

- 6.4.8 Ondupack

- 6.4.9 Packaging Corporation of America

- 6.4.10 Pratt Industries, Inc.

- 6.4.11 Rengo Co., Ltd.

- 6.4.12 Saica

- 6.4.13 Smurfit Westrock

- 6.4.14 Stora Enso

- 6.4.15 Thai Containers Group Co., Ltd.

- 6.4.16 Visy

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment