|

시장보고서

상품코드

2062254

PET 필름 피복 철강 코일 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)PET Film Coated Steel Coil - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

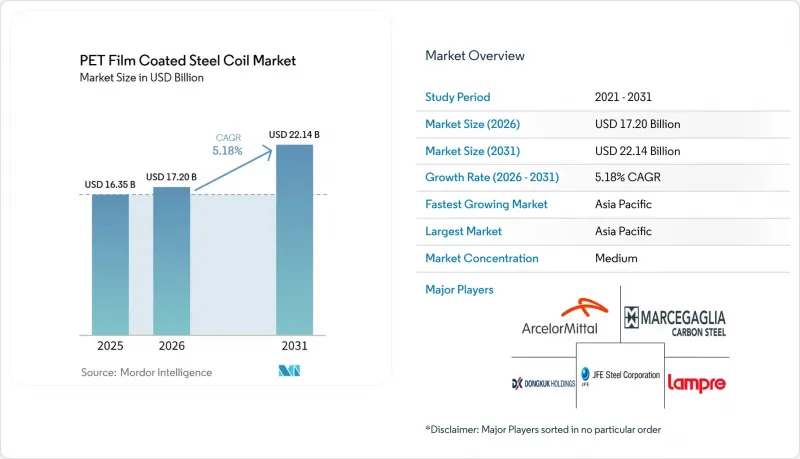

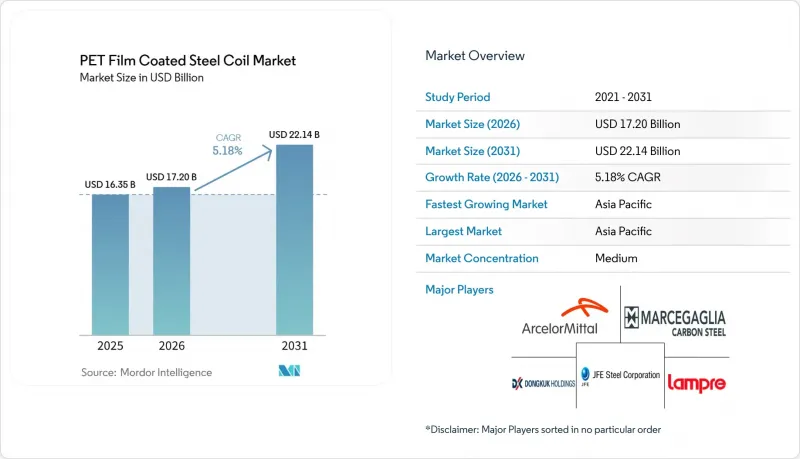

Mordor Intelligence에 의하면, PET 필름 피복 철강 코일 시장 규모는 2025년 163억 5,000만 달러로 평가되었고, 2026년에는 172억 달러로 추정되고, 2026-2031년 CAGR 5.18%로 성장을 지속할 전망이며, 2031년까지 221억 4,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 기판 유형별(냉연강판 등), 코팅 유형별(단면 PET 등), 용도별(벽 패널 및 지붕용 시트 등), 최종 사용자 산업별(건설 및 인프라 등), 그리고 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 PET 필름 코팅 강판 코일 시장 동향 및 분석

미관을 중시한 스틸 패널을 활용한 가전제품 생산 확대

아시아태평양의 백색 가전 제조업체들은 조립 후 도장 공정을 생략하고, 휘발성 유기 화합물(VOC) 배출을 줄이며, 균일한 광택을 구현하기 위해 PET 라미네이트를 지정하고 있습니다. 인도의 진달(Jindal)사는 2026년 2월에 가동을 시작할 코팅 라인을 통해 부가가치 생산 능력을 60% 증대시켜 연간 30만 톤으로 확대할 계획이며, 냉장고, 세탁기 본체 및 태양광 발전 설비를 주요 타겟으로 삼고 있습니다. 아르셀로미탈 닛폰 스틸 인디아는 가전 제조업체를 대상으로 한 두 가지 새로운 코팅 브랜드를 통해 부가가치 매출 비중을 75%로 높이는 것을 목표로 하고 있습니다. 전자상거래 유통의 확대에 따라, 찌그러짐이나 흠집에 강한 패널은 긴 물류 과정을 거치더라도 쇼룸과 같은 마감 상태를 유지하며, 이익의 원천을 하류의 라미네이팅 공정으로 전환시키고 있습니다.

지속가능성의 관점에서 볼 때, PVC보다 PET 코팅 강판이 더 선호됩니다.

규제 당국은 염소계 화학물질의 사용과 재활용성이 낮다는 점을 이유로 PVC 사용을 단계적으로 폐지하고 있습니다. 독일이 2024년 12월에 발표한 ‘국가 순환 경제 전략’에서는 폴리머별 재생 소재 함유율 할당제와 디지털 제품 여권이 도입되었으며, 단일 소재인 PET 설계가 장려되고 있습니다. 유럽연합(EU)의 포장 규제안에서는 2030년까지 재활용률 70%를 목표로 하고 있으며, 재료 회수를 방해하는 PVC 코팅보다 염소를 포함하지 않는 PET 라미네이트가 선호되는 추세입니다. 심사된 연구에 따르면, PET 코팅 강판은 차단 성능을 유지하면서 스프레이 도료에서 발생하는 VOC를 제거할 수 있는 것으로 나타났습니다.

다층 코팅 기판의 제한된 재활용 가능성

융합된 고분자와 금속의 계면은 기계적 분리를 어렵게 하여, 유럽의 재활용 목표 달성을 복잡하게 만들고 있습니다. ‘청정 생산’에 관한 조사에 따르면, 다층 필름은 이미 연포장 생산량의 17%를 차지하고 있지만, 현재 규모에서의 고도화된 회수 공정은 소각 처리에 비해 온실가스(GHG) 배출량을 21% 증가시킵니다. 화학적 탈중합 방식은 상업적으로 검증되지 않았기 때문에 제조업체들은 수용성 접착제나 층 분리 설계를 시험적으로 도입해야 하는 상황에 처해 있습니다.

부문별 분석

2025년에는 아연 도금 코일이 매출의 53.22%를 차지했으나, 해안 지역 인프라에 ISO 12944 C4-C5 내구성 기준이 채택됨에 따라, 갈바륨 강판 및 알잔크 강판은 예측 기간(2026년-2031년) 동안 연평균 성장률(CAGR) 5.81%로 성장할 것으로 전망됩니다. 염수 분무 시험에 따르면, 갈바륨 강판은 2,000시간이 경과한 후에도 연간 두께 감소량이 불과 0.03mm에 그치며, 실제 수명은 20년을 초과합니다. 따라서, 갈바륨 기판용 PET 필름 코팅 강판 코일 시장 규모는 톤당 150달러의 가격 프리미엄을 고려하더라도, 아연 도금 강판보다 빠르게 확대될 전망입니다. 각 제조업체는 접착을 저해할 가능성이 있어, 고알루미나 함량에 대응하기 위해 개량형 프라이머가 필요함에 따라 접착층을 재조정하고 있습니다.

새로운 코팅 라인에서 구현되는 첨단 AI 품질 관리는 갈바륨의 두께 균일성을 보장하고 수율을 향상시킵니다. 예지 보수를 통해 중국의 제철소에서는 이미 계획 외 가동 중단 시간이 50% 감소했으며, 이 프로젝트의 경제적 효과는 고품질 금속 코팅으로 이어지고 있습니다. 재생에너지 발전소 및 데이터센터 단지가 습한 연안 지역에 집중됨에 따라, 갈바륨 및 알잔크용 PET 필름 코팅 강판 코일 시장에 대한 수요는 2031년까지 계속 증가할 것으로 보입니다.

2025년에는 가전제품의 후면 패널 대부분이 표면 보호만 필요로 했기 때문에 단면 PET 필름 코팅이 매출의 63.35%를 차지했습니다. 그러나 항균·기능성 PET 필름을 사용한 PET 필름 코팅 강판 코일 시장 규모는 예측 기간(2026-2031년) 동안 연평균 성장률(CAGR) 5.97%로 확대될 전망입니다. 이는 병원, 구내식당, 클린룸에서 ISO 22196을 준수하는 솔루션이 지정되어 있기 때문입니다. 은 이온 코팅은 변색 없이 10년 동안 99% 이상의 세균 억제 효과를 유지합니다.

양면, 무광, UV 내성이 있는 제품은 양면이 보이는 장소나 햇빛에 심하게 노출되는 건축 실내 인테리어 및 엘리베이터 캐빈용으로 제공됩니다. 기능적 차별화를 통해 아시아 지역의 일반 상품 공급 과잉 속에서도 이익률을 유지하고 있습니다. 나노 입자, 지문 방지, 적외선 반사 등 각 제품군은 20-40%의 프리미엄 가격이 책정되어 있어, 공급업체가 수지 비용 급등을 상쇄하는 데 도움이 되고 있습니다. 첨가제의 공동 압출 기술을 통합한 시장 선도 기업은 스트립 도장 분야의 경쟁사들에 비해 PET 필름 코팅 강판 코일 시장 점유율을 확대할 태세를 갖추고 있습니다.

지역별 분석

아시아태평양은 2025년에 매출의 52.26%를 차지한 것으로 평가되었으며, 2031년까지 연평균 성장률(CAGR) 6.12%로 성장할 전망입니다. 인도에서는 새로 가동된 110억 루피(약 1억 3,200만 달러) 규모의 생산 라인을 통해 국내 코팅 강판 생산 능력이 확대되었으며, 가전제품 및 태양광 라크용으로 연간 30만 톤 생산을 목표로 하고 있습니다. 아르셀로미탈 닛폰 스틸은 인도 내 가전제품 수요가 연간 10% 성장하는 추세를 활용해, 매출의 75%를 부가가치가 높은 등급으로 전환하고 있습니다. 중국에서는 반덤핑 소송이 증가하고 있음에도 불구하고, 수지 공급 과잉이 수출을 뒷받침하고 있어 가동률은 75% 가까이 유지되고 있습니다. 아세안 지역의 양철판 생산 확대에 따라 PET 라미네이트가 해당 지역 공급망에 더욱 자리잡고 있습니다.

북미와 유럽에서는 판매량 증가세가 둔화되고 있지만, VOC 규제 및 재생재 함유율 할당 기준에 따라 톤당 이익률은 높은 수준을 유지하고 있습니다. 미국 환경보호청(EPA)은 철강 업계의 배출 규제(에어 룰) 준수 기한을 2027년 4월로 연기함에 따라, 국내 라미네이트 제조업체의 원자재 비용에 영향을 미치고 있습니다. 독일의 순환형 경제 프로그램에서는 2030년까지 디지털 제품 여권 도입이 의무화되어 있어, 추적 가능성이 있는 PET 코팅에 대한 수요를 촉진하고 있습니다. 2025년 4분기, 미국에서는 컨버터 수요가 부진했음에도 불구하고, 운임 급등으로 인해 BOPET(이축 연신 폴리에틸렌 테레프탈레이트) 가격이 상승했습니다.

남미와 중동 및 아프리카는 규모는 여전히 작지만, 인프라 메가 프로젝트나 석유화학 플랜트에 내식성 클래딩이 필요한, 기회가 풍부한 지역입니다. 이 지역들의 아시아산 필름 수입 의존도가 높다는 점은 가격 변동을 심화시키고 있지만, 현지에 슬리팅 센터를 설립함으로써 리드타임을 단축하고 PET 필름 코팅 강판 코일 시장의 침투율을 높일 수 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the pET film coated steel coil market size is expected to grow from USD 16.35 billion in 2025 to USD 17.20 billion in 2026 and is forecast to reach USD 22.14 billion by 2031 at 5.18% CAGR over 2026-2031.

This report is Segmented by Substrate Type (Cold-Rolled Steel, and More), Coating Type (Single-Side PET, and More), Application (Wall Panels and Roofing Sheets, and More), End-User Industry (Construction and Infrastructure, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global PET Film Coated Steel Coil Market Trends and Insights

Expansion of Appliance Manufacturing Using Aesthetic Steel Panels

White-goods producers in Asia-Pacific are specifying PET laminates to avoid post-assembly painting, cut volatile-organic-compound emissions, and deliver uniform gloss. Jindal India's February 2026 coating line lifts value-added capacity by 60% to 300,000 tons/year, targeting refrigerators, washer housings, and solar structures. ArcelorMittal Nippon Steel India aims to raise value-added revenue share to 75% with two new coated brands positioned for appliance OEMs. As e-commerce distribution grows, dent-resistant, scratch-proof panels maintain a showroom finish through long logistics chains, shifting margin pools toward downstream lamination.

Preference for PET-Coated Steel Over PVC on Sustainability Grounds

Regulators are phasing out PVC because of chlorine chemistry and poor recyclability. Germany's December 2024 National Circular Economy Strategy introduces polymer-specific recycled-content quotas and digital product passports, encouraging mono-material PET designs. The European Union's draft Packaging Regulation seeks 70% recycling by 2030, making chlorine-free PET laminates preferable to PVC coatings that hinder material recovery. Peer-reviewed work shows PET-coated steel eliminates spray-paint VOCs while maintaining barrier integrity.

Limited Recyclability of Multilayer Coated Substrates

Fused polymer-metal interfaces resist mechanical separation, complicating European recycling targets. Cleaner-Production reviews find multilayer films already 17% of flexible output, yet advanced recovery routes raise GHGs by 21% versus incineration at the current scale. Chemical depolymerization options are unproven commercially, pressuring manufacturers to trial water-soluble adhesives or split-layer designs.

Other drivers and restraints analyzed in the detailed report include:

- Improved Scratch Resistance and Color Retention Driving OEM Usage

- Adoption in Smart-Home Exterior Panels Requiring IR-Reflective Coatings

- Technical Challenges in Adhesion and Film Delamination

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Galvanized coil delivered 53.22% revenue in 2025, but galvalume/aluzinc steel is forecast to grow at a 5.81% CAGR during the forecast period (2026-2031) as coastal infrastructure adopts ISO 12944 C4-C5 durability. Salt-spray tests show galvalume loses only 0.03 mm/year after 2,000 hours, extending field life beyond 20 years. The PET film coated steel coil market size for galvalume substrates is therefore set to expand faster than for galvanized, even considering its USD 150/ton price premium. Producers are recalibrating adhesion layers to match the higher aluminum oxide content that can impair bonding and require modified primers.

Advanced AI quality-control on new coating lines supports uniform galvalume thickness control and raises yield. Predictive maintenance has already cut unplanned downtime 50% at Chinese mills, tipping project economics toward high-grade metallic coatings. As renewable-energy farms and data-center campuses cluster near humid coastal zones, PET film coated steel coil market demand for galvalume and aluzinc will keep climbing through 2031.

Single-side PET film coating retained 63.35% revenue in 2025 because most appliance back panels require only front-face protection. The PET film coated steel coil market size for antibacterial and functional PET films, however, is growing at a 5.97% CAGR for the forecast period (2026-2031) as hospitals, canteens, and cleanrooms specify ISO 22196-compliant solutions. Silver-ion coatings maintain more than 99% bacterial suppression for a decade without discoloration.

Double-side, matte, and UV-stable products serve architectural interiors and elevator cabins where both faces are visible or sunlight exposure is severe. Functional differentiation shields margins from Asian commodity overcapacity: nanoparticle, anti-fingerprint, and IR-reflective variants command 20-40% premiums, helping suppliers offset resin cost spikes. Market leaders that integrate co-extrusion of additives are positioned to widen their PET film coated steel coil market share over strip-paint rivals.

Geography Analysis

Asia-Pacific generated 52.26% revenue in 2025 and will grow at 6.12% CAGR through 2031. India's newly commissioned INR 11 billion (approximately USD 132 million) line lifts domestic coated-steel capacity, aiming at 300,000 tons/year for appliances and solar racks. ArcelorMittal Nippon Steel is shifting 75% of revenue to value-added grades, leveraging India's 10% annual appliance demand growth. China's resin surplus powers exports even as anti-dumping cases rise, sustaining utilization near 75%. ASEAN tinplate expansions further embed PET laminates into regional supply chains.

North America and Europe show slower volume growth yet command higher per-ton margins driven by VOC caps and recycled-content quotas. The U.S. EPA (Environmental Protection Agency) moved iron-and-steel air-rule compliance to April 2027, affecting substrate costs for domestic laminators. Germany's circular-economy program mandates digital product passports by 2030, boosting traceable PET coatings. Freight premiums lifted Q4 2025 BOPET (Biaxially Oriented Polyethylene Terephthalate) prices in the United States despite soft converter demand.

South America and the Middle East & Africa remain smaller, opportunity-rich regions where infrastructure megaprojects and petrochemical plants need corrosion-proof cladding. Their dependence on Asian film imports intensifies volatility, yet localized slitting centers could shorten lead times and lift PET film coated steel coil market penetration.

- ArcelorMittal

- Baosteel Co., Ltd.

- DONGKUKHOLDINGS CO., LTD.

- HYUNDAI STEEL

- JFE Steel Corporation

- Jiangyin Woda New Materials Co., Ltd.

- JSW Steel

- Lampre s.r.l.

- LIENCHY LAMINATED METAL CO., LTD.

- MARCEGAGLIA CARBON STEEL S.p.A.

- NIPPON STEEL CORPORATION

- NLMK

- POSCO

- Severstal

- Shandong Colour-Coated Steel

- Ternium

- ThyssenKrupp Steel Europe

- Yieh Phui Enterprise Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of appliance manufacturing using aesthetic steel panels

- 4.2.2 Preference for PET-coated steel over PVC on sustainability grounds

- 4.2.3 Improved scratch resistance and colour retention driving OEM usage

- 4.2.4 Adoption in smart-home exterior panels requiring IR-reflective coatings

- 4.2.5 Emergence of ultra-thin PET films enabling laser micro-perforation for ventilation

- 4.3 Market Restraints

- 4.3.1 Limited recyclability of multilayer coated substrates

- 4.3.2 Technical challenges in adhesion and film delamination

- 4.3.3 Scarce global PET-grade film supply outside of Asia

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Substrate Type

- 5.1.1 Cold-Rolled Steel (CR Steel)

- 5.1.2 Galvanized Steel

- 5.1.3 Galvalume/Aluzinc Steel

- 5.1.4 Other Substrate Types

- 5.2 By Coating Type

- 5.2.1 Single-side PET Film Coating

- 5.2.2 Double-side PET Film Coating

- 5.2.3 UV/Matte/Glossy PET Film Coatings

- 5.2.4 Antibacterial and Functional PET Films

- 5.3 By Application

- 5.3.1 Home Appliances

- 5.3.2 Wall Panels and Roofing Sheets

- 5.3.3 Doors and Partition Panels

- 5.3.4 Electrical Cabinets and Enclosures

- 5.3.5 Shipping Containers and Industrial Shelters

- 5.3.6 Other Applications (Elevators, Cladding, and Signage)

- 5.4 By End-user Industry

- 5.4.1 Construction and Infrastructure

- 5.4.2 Consumer Appliances

- 5.4.3 Industrial Equipment

- 5.4.4 Transportation and Automotive

- 5.4.5 Electrical and Electronics

- 5.4.6 Other End-user Industries (Retail, Furniture, and Interior Decor)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 NORDIC Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 ArcelorMittal

- 6.4.2 Baosteel Co., Ltd.

- 6.4.3 DONGKUKHOLDINGS CO., LTD.

- 6.4.4 HYUNDAI STEEL

- 6.4.5 JFE Steel Corporation

- 6.4.6 Jiangyin Woda New Materials Co., Ltd.

- 6.4.7 JSW Steel

- 6.4.8 Lampre s.r.l.

- 6.4.9 LIENCHY LAMINATED METAL CO., LTD.

- 6.4.10 MARCEGAGLIA CARBON STEEL S.p.A.

- 6.4.11 NIPPON STEEL CORPORATION

- 6.4.12 NLMK

- 6.4.13 POSCO

- 6.4.14 Severstal

- 6.4.15 Shandong Colour-Coated Steel

- 6.4.16 Ternium

- 6.4.17 ThyssenKrupp Steel Europe

- 6.4.18 Yieh Phui Enterprise Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment