|

시장보고서

상품코드

2062350

금속 코일 라미네이트 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Metal Coil Lamination - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

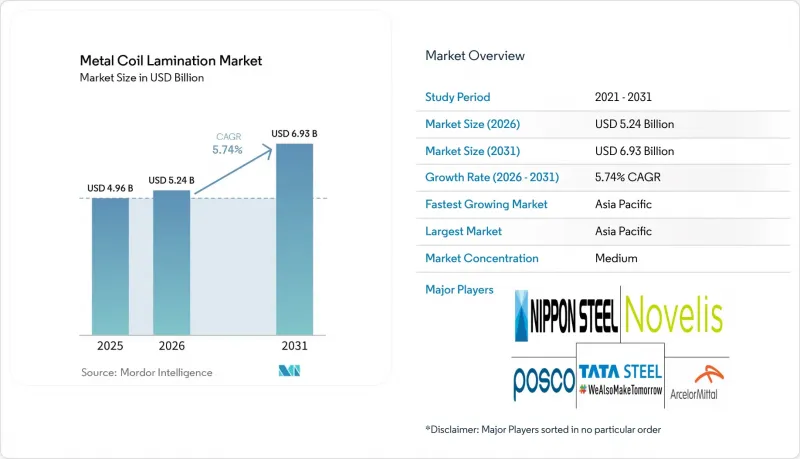

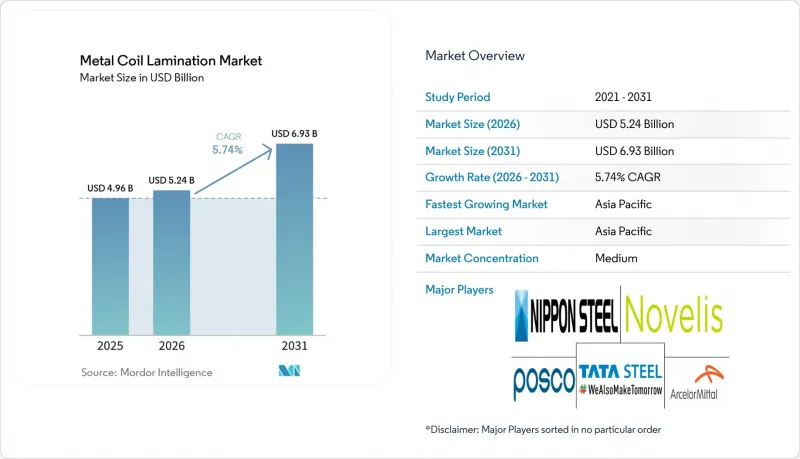

금속 코일 라미네이트 시장 규모는 2025년 49억 6,000만 달러로 평가되었습니다. 2026년 52억 4,000만 달러로 확대되어 2031년까지 69억 3,000만 달러에 이를 것으로 예상되며 2026년부터 2031년에 걸쳐 CAGR은 5.74%를 나타낼 전망입니다.

본 보고서는 적층 방식(열적층 등), 기판 금속(강, 알루미늄 등), 적층 재료(폴리에틸렌 테레프탈레이트(PET) 필름 등), 용도(건축용 패널 및 외장재 등), 최종 사용자 산업(건축 및 건설 등), 지역(아시아태평양 등)에 따라 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 금속 코일 라미네이트 시장 동향 및 인사이트

건설 및 가전 분야에서 프리코팅 금속 수요 증가

공장에서 코팅 공정을 거치면 현장에서 도장을 할 필요가 없어져, 근로자의 용제 노출을 줄이고 공사 기간을 단축할 수 있습니다. AM/NS India는 스프레이 부스가 널리 보급되지 않은 지방 도시의 지붕 자재 시장을 겨냥하여, 2026년까지 컬러 코팅 강판의 생산 능력을 연간 100만 톤으로 확대했습니다. 가전 제조업체들은 일관된 색상 품질 덕분에 라미네이트 코일을 선호하여 사용하고 있습니다. 베트남공급업체인 Systeel Vina는 아세안 협정에 따라 지역 내 LG 및 삼성 공장에 VCM과 PCM을 관세 없이 공급하고 있습니다. 인건비 상승이 자동화 비용 상승을 상회하는 지역에서는 공장에서의 라미네이팅 가공이 경제적으로 더 현실적인 선택지가 됩니다. 새로운 가전제품용 등급 라인에서는 기존의 도장 방식으로는 구현할 수 없는 지문 방지 기능이나 심압 성형성 등의 기능이 제공되고 있습니다. 이러한 요인들이 복합적으로 작용하여 금속 코일 라미네이트 시장 수요를 견인하고, 이익률을 높이고 있습니다.

자동차 경량화 및 실내 인테리어에서의 적용 확대

각 자동차 제조업체들은 새로운 도장 설비에 투자하지 않고도 CO2 배출 목표를 달성하기 위해 프리라미네이트 알루미늄의 사용을 확대되고 있습니다. AMAG는 알루미늄 차체 시트를 공급하고 있으며, 한편 Alutrim의 장식 필름은 클래스 A 수준의 표면 품질을 유지하면서 내장재의 무게를 최대 12%까지 줄여줍니다. 머티리얼 사이언스 코퍼레이션의 ‘스마트 스틸’은 폴리머 필름과 고장력 강재를 결합함으로써, 충돌 안전 기준을 충족하면서도 판 두께를 얇게 만들 수 있게 해줍니다. 캘리포니아주의 ‘어드밴스드 클린 카 II(Advanced Clean Cars II)’와 같은 규제가 도입을 더욱 촉진하고 있으며, 1차 공급업체 측에서는 도장로를 폐지함으로써 조립 공정에서의 에너지 소비를 15-20% 절감할 수 있었다고 보고하고 있습니다.

금속 및 폴리머 원자재 가격 변동

철강, 알루미늄, 수지의 원가는 여전히 에너지 시장의 변동 영향을 받기 쉬운 상황입니다. 예를 들어, 2025년에는 폴리에틸렌 테레프탈레이트(PET) 수지 가격이 급등하여, 계약에 가격 전가 조항을 포함하지 않은 가공업체들에게 타격을 주었습니다. 1톤당 약 15MWh를 소비하는 알루미늄 제련소는 전력 가격 급등의 영향을 특히 많이 받으며, 이로 인해 코일 가격에 영향을 미치고 있습니다. 또한, 특수 합금용 중요 광물공급 차질은 리드타임 관련 위험을 높이며, 업계의 재고 및 현금 흐름 관리를 복잡하게 만들고 있습니다.

부문별 분석

2025년, 금속 코일 라미네이트 시장에서 열 라미네이트가 40.91%의 점유율을 차지하며 계속해서 1위를 유지했습니다. 그러나 UV 라미네이트는 순간 경화 능력과 에너지 비용의 대폭적인 절감 덕분에 2031년까지 연평균 성장률(CAGR) 6.35%로 가장 높은 성장률을 보일 것으로 예측됩니다. 특히 EU의 CBAM(국경조정조치)으로 인해 천연가스식 건조기의 비용이 증가하고 있는 지역에서 UV 라미네이션 도입이 가속화되고 있습니다. 정전기식, 냉간식 및 접착제식은 여전히 틈새 시장에 머물러 있으며, 특수한 접착이 필요한 전자기기, 간판, 다층 차폐재에 대한 수요를 충족시키고 있습니다. OEM 각사는 에너지 절감 효과와 탄소 배출 제재 회피를 고려할 때, UV로 업그레이드할 경우 투자 회수 기간이 3년에서 5년 정도라고 보고하고 있습니다. IST METZ사와 Koenig &Bauer사가 장비 공급 시장을 독점하고 있으며, 램프 교체 일정에 연동된 서비스 수익의 혜택을 누리고 있습니다. 장기적으로는 UV 기술의 높은 처리량으로 인해 열식 오븐 시장 점유율이 잠식될 것으로 예상되지만, 에너지 보조금이 지급되는 지역에서는 기존 시스템이 계속 유지될 가능성이 있습니다.

아크릴이나 불소 수지 필름을 UV로 경화시키는 컨버터는 기판의 뒤틀림을 방지할 수 있습니다. 이는 두께 0.5mm인 자동차용 차체 시트에 있어 매우 중요한 요건입니다. 일시적인 보호 필름의 경우, 냉간 라미네이션이 여전히 유용하지만, 그 라인 속도는 접착제의 휘발 시간에 의해 제한됩니다. 접착제 라미네이션은 폴리이미드, 아라미드, PET가 사용되는 고전압 변압기 등 다층 배리어가 필요한 용도에서 활발히 이루어지고 있습니다. 규제로 인한 에너지 추가 비용 증가에 따라, 금속 코일 라미네이트 시장의 신규 설비 투자에서 UV 기술이 유력한 대안으로 떠오르고 있습니다.

2025년 기준으로, 금속 코일 라미네이트 시장 점유율의 63.78%를 강철 코일이 차지했으며, 이는 주로 비용 효율성과 자기적 특성 덕분입니다. 그러나 차량 경량화와 2027년 자동차 배기가스 규제에 대응해야 할 필요성이 제기됨에 따라, 알루미늄 코일 시장은 2031년까지 연평균 성장률(CAGR) 6.89%를 기록하며 성장할 것으로 예측됩니다. 노벨리스는 연간 생산 능력 60만 톤을 갖추고, 사전 라미네이트 처리된 자동차 차체용 시트를 공급하는 베이 미넷 압연 공장에 41억 달러를 투자하고 있습니다. 구리는 전기 절연재용의 고급이자 틈새 시장용 기판으로, 그 유전 특성 덕분에 높은 이익률을 가져다주고 있습니다. 아연 및 니켈 합금은 갈바닉 내성이 높은 비용을 정당화할 수 있는 화학 처리 용도로 사용됩니다.

포스코와 같은 통합 제철사는 2025년에 700만 톤 이상의 도금강판을 판매했습니다. 그러나 구매자들이 내재된 탄소를 포함한 총 소유 비용을 점점 더 중요하게 여기게 됨에 따라, 그 우위는 과제로 대두되고 있습니다. 알루미늄은 가격이 비싸지만, 재활용성과 경량화라는 장점 덕분에 구매자들의 선호도가 변화하고 있습니다. 금속 코일 적층 시장은 강철의 비용 경쟁력과 알루미늄의 규제 대응 및 경량화 이점 간경쟁 구도로 진화하고 있습니다.

지역별 분석

2025년, 아시아태평양은 금속 코일 라미네이트 시장 점유율의 42.83%를 차지했으며, 2031년까지 연평균 성장률(CAGR) 7.18%를 나타낼 것으로 예측됩니다. 30년 PVDF 보증을 제공하는 산시 지안룽(Shanxi Jianlong)의 14억 달러 규모 자오저우(Jiaozuo) 생산라인 등 투자들이 중국 2선 도시의 주택 붐을 뒷받침하고 있습니다. 일본과 한국의 제조업체들은 이산화탄소 감축에 주력하고 있으며, 신일철주금의 ‘Viewcoat’는 톤당 배출량을 30% 감축하고 있습니다. 연간 생산 능력 100만 톤 규모의 인도 AM/NS 공장은 현장에 스프레이 부스가 없는 지붕재 용도를 주요 대상으로 하고 있습니다.

북미는 소규모 기반에서 성장하고 있으며, 노벨리스(Novelis)사의 베이 미넷 알루미늄 코일 공장과 자동차 부품의 현지 조달을 촉진하는 USMCA(미국·멕시코·캐나다 협정) 규정이 이를 주도하고 있습니다. EPA(미국 환경보호청)의 PFAS 규제로 인해 수처리 분야에 대한 투자가 확대되면서 신규 진입 장벽이 높아지고 있습니다. 멕시코는 가전제품 수출 거점으로 부상하고 있는 반면, 캐나다에서는 친환경 건축 노력의 일환으로 저VOC(휘발성 유기화합물) 도장 강판의 사용이 장려되고 있습니다.

유럽은 성숙한 시장이지만, 지속가능성에 대한 노력이 활발히 진행되고 있습니다. CBAM(탄소 국경 조정 메커니즘)은 수입품에 탄소 비용을 부과하기 때문에 구매자들은 국내산 UV 경화형 코일을 선택하도록 권장받고 있습니다. SSAB의 ‘GreenCoat’는 바이오 수지 시스템을 채택하여 지지를 넓혀가고 있습니다. 남유럽에서는 비용 효율이 높은 아연 도금 강판이 선호되는 반면, 독일이나 북유럽 국가들에서는 생애주기 평가(LCA)를 통해 그 우수성이 입증된 고품질 라미네이트 소재가 선호되고 있습니다.

중동 및 아프리카 및 남미는 시장 점유율은 작지만, 선택적인 성장세를 보이고 있습니다. 사우디아라비아의 ‘비전 2030’ 프로젝트에서는 해안 리조트용으로 내식성 클래딩이 요구되고 있습니다. 브라질의 건설 호황이 코팅 지붕 자재 수요를 뒷받침하고 있으며, 아르헨티나에서는 수출용 차량에 적층 알루미늄이 사용되고 있습니다. 이러한 지역들은 인프라 및 자원 투자가 금속 코일 라미네이트 시장의 점진적인 성장을 어떻게 뒷받침하고 있는지를 여실히 보여주고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the metal coil lamination market size is expected to increase from USD 4.96 billion in 2025 to USD 5.24 billion in 2026 and reach USD 6.93 billion by 2031, growing at a CAGR of 5.74% over 2026-2031.

This report is Segmented by Lamination Type (Thermal Lamination, and More), Substrate Metal (Steel, Aluminum, and More), Laminate Material (Polyethylene Terephthalate (PET) Films, and More), Application (Architectural Panels and Cladding, and More), End-User Industry (Building and Construction, and More), and Geography (Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Metal Coil Lamination Market Trends and Insights

Growing Demand for Pre-Coated Metal in Construction and Appliances

Factory coating eliminates the need for on-site painting, reducing labor exposure to solvents and shortening construction schedules. AM/NS India expanded its color-coated steel capacity to 1 million tons per year in 2026, targeting roofing applications in second-tier cities where spray booths are less common. Appliance manufacturers prefer laminated coils for their consistent color quality; Vietnamese supplier Systeel Vina provides VCM and PCM to regional LG and Samsung plants tariff-free under ASEAN agreements. In regions where labor costs rise faster than automation expenses, factory lamination becomes more economically viable. New appliance-grade lines now offer features such as fingerprint resistance and deep-draw formability, which traditional paint cannot achieve. These factors collectively drive unit demand and improve margins in the metal coil lamination market.

Increasing Adoption in Automotive Lightweighting and Interiors

Automakers are increasingly adopting pre-laminated aluminum to meet CO2 targets without investing in new paint facilities. AMAG supplies aluminum body sheets, while Alutrim's decorative films reduce interior weight by up to 12% while maintaining Class-A surface quality. Material Sciences Corporation's Smart Steel combines polymer film with high-strength steel, enabling thinner gauges to meet crash standards. Regulations such as California's Advanced Clean Cars II further drive adoption, and Tier 1 suppliers report 15%-20% energy savings in assembly processes when paint ovens are eliminated.

Volatility in Metal and Polymer Feedstock Prices

Steel, aluminum, and resin costs remain vulnerable to energy market fluctuations. For instance, polyethylene terephthalate resin prices surged in 2025, impacting converters without price-pass clauses in their contracts. Aluminum smelters, which consume approximately 15 MWh per ton, are particularly affected by power price spikes, which influence coil pricing. Additionally, supply disruptions of critical minerals for specialty alloys increase lead-time risks, complicating inventory and cash flow management in the industry.

Other drivers and restraints analyzed in the detailed report include:

- Enhanced Corrosion Resistance and Aesthetic Appeal

- Shift Toward High-Performance and Decorative Laminates

- Environmental Scrutiny Over VOC and PFAS Emissions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, thermal lamination continued to lead with 40.91% of the metal coil lamination market share. However, UV lamination is anticipated to grow at the fastest rate, with a 6.35% CAGR through 2031, due to its instant curing capabilities and significant energy cost reductions. The adoption of UV lamination is accelerating, particularly in regions where the EU CBAM increases the cost of natural gas ovens. Electrostatic, cold, and adhesive methods remain niche, catering to electronics, signage, and multilayer shields requiring specialized bonding. OEMs report a three- to five-year payback period for UV upgrades, factoring in energy savings and avoided carbon penalties. IST METZ and Koenig & Bauer dominate the equipment supply market, benefiting from service revenues tied to lamp replacement schedules. Over time, UV technology's higher throughput is expected to erode the market share of thermal ovens, although legacy systems may persist in regions with energy subsidies.

Converters using UV to bake acrylic or fluoropolymer films avoid substrate warpage, a critical requirement for 0.5 mm automotive body sheets. Cold lamination remains relevant for temporary protection films, though its line speeds are limited by adhesive flash-off time. Adhesive lamination thrives in applications requiring multilayer barriers, such as high-voltage transformers, where polyimide, aramid, and PET are used. As regulatory energy surcharges increase, UV technology is emerging as the preferred choice for new capacity in the metal coil lamination market.

Steel coils held 63.78% of the metal coil lamination market share in 2025, primarily due to their cost-effectiveness and magnetic properties. However, aluminum coils are expected to grow at a CAGR of 6.89% through 2031, driven by the need to reduce vehicle weight and comply with 2027 fleet CO2 limits. Novelis has committed USD 4.1 billion to its Bay Minette rolling mill, which has a capacity of 600,000 tons per year and offers pre-laminated autobody sheets. Copper remains a premium but niche substrate for electrical insulation, offering higher margins due to its dielectric properties. Zinc and nickel alloys are used in chemical processing applications where galvanic resistance justifies their higher costs.

Integrated steel producers like POSCO sold over 7 million tons of coated steel in 2025. However, their dominance is challenged as buyers increasingly consider the total cost of ownership, including embedded carbon. Aluminum's recyclability and weight reduction benefits are shifting buyer preferences, despite its higher price. The metal coil lamination market is evolving into a competition between steel's cost advantage and aluminum's regulatory and lightweighting benefits.

Geography Analysis

Asia-Pacific accounted for 42.83% of the metal coil lamination market share in 2025 and is expected to grow at a CAGR of 7.18% through 2031. Investments such as Shanxi Jianlong's USD 1.4 billion Jiaozuo line, which offers 30-year PVDF warranties, are supporting housing booms in tier-2 Chinese cities. Japanese and Korean producers are focusing on CO2 reductions, with Nippon Steel's Viewcoat achieving 30% lower emissions per ton. India's AM/NS plant, with a capacity of 1 million tons per year, targets roofing applications where on-site spray booths are unavailable.

North America is growing from a smaller base, led by Novelis's Bay Minette aluminum coil mill and USMCA regulations that localize automotive sourcing. EPA PFAS limits are driving investments in water treatment, raising entry barriers for new players. Mexico is emerging as a hub for appliance exports, while Canada's green-building initiatives encourage the use of low-VOC coated steel.

Europe, while mature, is advancing sustainability initiatives. CBAM imposes carbon costs on imports, encouraging buyers to choose domestic UV-cured coils. SSAB's GreenCoat is gaining traction with bio-based resin systems. Southern Europe favors cost-effective galvanized sheets, while Germany and Nordic countries prefer premium laminates with documented life cycle assessments.

The Middle-East and Africa, along with South America, contribute smaller shares but show selective growth. Saudi Arabia's Vision 2030 projects require corrosion-resistant cladding for coastal resorts. Brazil's construction cycle supports demand for coated roofing, while Argentina uses laminated aluminum in export vehicles. These regions highlight how infrastructure and resource investments sustain incremental growth in the metal coil lamination market.

- American Nickeloid Company

- ArcelorMittal

- Globus s.r.l.

- Hindalco Industries Ltd. (Novelis)

- Jindal Poly Films Limited.

- Laminators Incorporated

- LIENCHY Laminated Metal Co.

- Material Sciences Corp.

- Metacolour A/S

- Mitsubishi Chemical Group Corp.

- NIPPON STEEL CORPORATION

- POSCO

- Tata Steel

- Thyssenkrupp Steel

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for pre-coated metal in construction and appliances

- 4.2.2 Increasing adoption in automotive lightweighting and interiors

- 4.2.3 Enhanced corrosion resistance and aesthetic appeal

- 4.2.4 Shift toward high-performance and decorative laminates

- 4.2.5 Energy-efficient building materials adoption

- 4.2.6 Integration of antimicrobial and smart-surface laminates

- 4.3 Market Restraints

- 4.3.1 Volatility in metal and polymer feedstock prices

- 4.3.2 Environmental scrutiny over VOC and PFAS emissions

- 4.3.3 Competition from powder-coated/painted metal

- 4.3.4 Complex recycling of multi-layer laminate scrap

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Lamination Type

- 5.1.1 Thermal Lamination

- 5.1.2 Adhesive Lamination

- 5.1.3 Cold Lamination

- 5.1.4 UV Lamination

- 5.1.5 Electrostatic Lamination

- 5.2 By Substrate Metal

- 5.2.1 Steel Coils

- 5.2.2 Aluminum Coils

- 5.2.3 Copper Coils

- 5.2.4 Other Substrate Metals (Zinc, Nickel Alloys)

- 5.3 By Laminate Material

- 5.3.1 Polyethylene Terephthalate (PET) Films

- 5.3.2 Polyvinyl Chloride (PVC) Films

- 5.3.3 Biaxially Oriented Polypropylene (BOPP Films)

- 5.3.4 Paper-Based Laminates

- 5.3.5 Other Laminate Materials (Acrylics, Fluoropolymers)

- 5.4 By Application

- 5.4.1 Architectural Panels and Cladding

- 5.4.2 Household Appliances

- 5.4.3 Furniture and Interior Decor

- 5.4.4 Electrical Cabinets and Equipment

- 5.4.5 Automotive Panels and Trim

- 5.4.6 Industrial Storage and Racks

- 5.4.7 Other Applications (Signage, Consumer)

- 5.5 By End-user Industry

- 5.5.1 Building and Construction

- 5.5.2 Consumer Appliances

- 5.5.3 Automotive and Transportation

- 5.5.4 Electrical and Electronics

- 5.5.5 Furniture and Interior Design

- 5.5.6 Industrial and Manufacturing

- 5.5.7 Other End-user Industries

- 5.6 By Geography

- 5.6.1 Asia-Pacific

- 5.6.1.1 China

- 5.6.1.2 India

- 5.6.1.3 Japan

- 5.6.1.4 South Korea

- 5.6.1.5 ASEAN Countries

- 5.6.1.6 Rest of Asia-Pacific

- 5.6.2 North America

- 5.6.2.1 United States

- 5.6.2.2 Canada

- 5.6.2.3 Mexico

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 NORDIC Countries

- 5.6.3.8 Rest of Europe

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle-East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 South Africa

- 5.6.5.3 Rest of Middle-East and Africa

- 5.6.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 American Nickeloid Company

- 6.4.2 ArcelorMittal

- 6.4.3 Globus s.r.l.

- 6.4.4 Hindalco Industries Ltd. (Novelis)

- 6.4.5 Jindal Poly Films Limited.

- 6.4.6 Laminators Incorporated

- 6.4.7 LIENCHY Laminated Metal Co.

- 6.4.8 Material Sciences Corp.

- 6.4.9 Metacolour A/S

- 6.4.10 Mitsubishi Chemical Group Corp.

- 6.4.11 NIPPON STEEL CORPORATION

- 6.4.12 POSCO

- 6.4.13 Tata Steel

- 6.4.14 Thyssenkrupp Steel

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment