|

시장보고서

상품코드

2062285

단세포 단백질 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Single Cell Protein - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

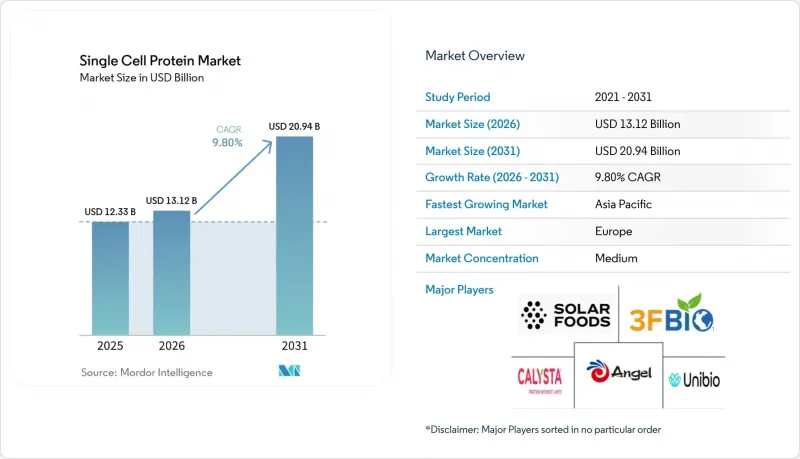

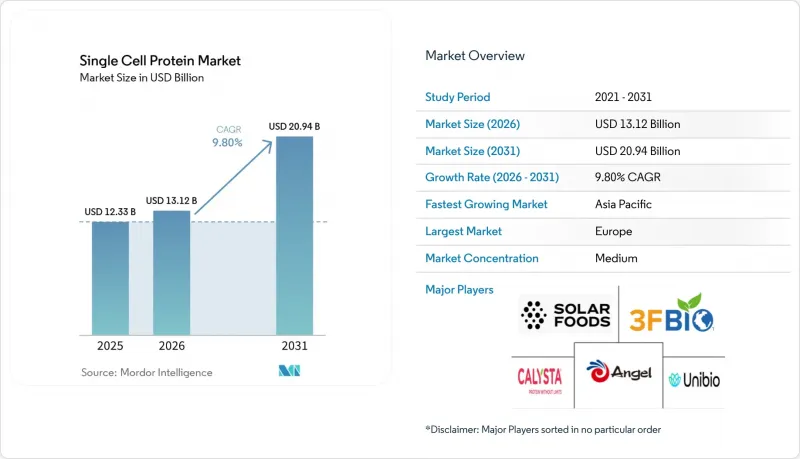

Mordor Intelligence에 의하면, 단세포 단백질 시장은 2025년에 123억 3,000만 달러 규모로 평가되었고, 2026년 131억 2,000만 달러로 추정되고, 2031년까지 209억 4,000만 달러로 성장할 전망이며, 2026-2031년 CAGR 9.80%를 나타낼 것으로 예측되고 있습니다.

본 보고서는 원료별(조류, 효모, 균류, 세균), 용도별(동물사료 및 반려동물사료, 식품 및 음료, 영양 보조 식품, 기타 용도) 및 지역별(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 단세포 단백질 시장 동향 및 인사이트

대체 단백질 원료에 대한 수요 증가

인구 증가와 식습관의 변화로 인해 전 세계적으로 단백질 부족 현상이 심화되고 있는 가운데, 단세포 단백질은 중국, 인도, 싱가포르의 국가 식량 안보 정책에 부합하며, 토지와 물을 효율적으로 활용하는 해결책을 제공합니다. 수입에 의존하는 경제권에서는 미생물 유래 단백질을 대두나 어분의 가격 변동에 대한 헤지 수단으로 간주하고 있는 반면, 앙젤 이스트(Angel East)나 칼리스타(Calista)와 같은 주요 생산자들은 대규모 생산을 통해 기존 사료용 단백질과 동등한 비용 경쟁력을 실현해 나가고 있습니다. 앤젤 이스트(Angel East)사의 효모 단백질 ‘AngeoPro’는 단백질 이용률 96%, 필수 아미노산 함유율 47%를 자랑하며, 프로틴 바, 시리얼, 대체육 제품에서 유청이나 대두의 대체재로 자리매김하고 있습니다. 싱가포르 식품청은 2024년에 여러 가지 마이코단백질 및 정밀 발효 원료를 승인함으로써, 2030년까지 영양 자급률 30%를 목표로 하는 시장에서 신속한 상용화를 가능하게 했습니다. 식량 안보에 대한 요구, 수입 대체 정책, 그리고 혼합 육류 제품을 수용하려는 소비자의 의지가 맞물리면서, 다국적 식품 기업과 지역 브랜드의 조달이 가속화되고 있습니다.

지속가능성과 환경 배려

생명주기 분석에 따르면, 미생물 유래 단백질은 쇠고기에 비해 온실가스 배출량을 최대 97%까지 줄일 수 있는 것으로 나타났으며, 과학에 기반한 목표 달성을 서두르는 기업들의 관심을 끌고 있습니다. EU의 ‘농장에서 식탁까지’ 전략은 저탄소 원료를 권장하고 있으며, 유럽식품안전청(EFSA)이 2025년에 Fermotein에 대해 제시한 긍정적인 견해는 주류 식품 공급망에서 탄소 음성 단백질로의 전환이 가속화되고 있음을 보여줍니다. 제철소와 정유시설에서는 란자테크(LanzaTech)사의 이산화탄소(CO2)를 이용해 단백질을 생산하는 모듈에 대한 실증 시험이 진행되고 있으며, 이를 통해 오염 물질을 수익원으로 전환하는 동시에 탄소 크레딧을 확보하고 있습니다. 호라이즌 계획의 자금 지원을 받은 SynoProtein 등의 이니셔티브는 산림 잔여물을 원료로 활용하고 있으며, 이를 통해 지속가능성에 대한 논의를 확대하고 단세포 단백질 시장을 강화하고 있습니다. 국제표준화기구(ISO)가 2021년에 발표한 ‘단백질 섬유’ 정의 개정(합성 단백질 포함) 등의 규제 체계는 미생물 유래 단백질을 공인된 원료 범주로 공식적으로 인정함으로써, 승인 절차상의 마찰을 줄이고, 기업의 지속가능성 노력을 조달 방침에 구체적으로 반영할 수 있도록 하고 있습니다.

기존 대두 및 어분 단백질과의 경쟁

대두박은 확립된 공급망, 농업 규모 및 상품 가격 메커니즘 덕분에 가축 및 수산 사료의 주요 단백질 공급원으로 자리매김하고 있습니다. 단세포 단백질이 가격에 민감한 사료 시장에서 기존 원료를 대체하기 위해서는 비용 면에서 동등한 경쟁력을 확보하거나, 뛰어난 기능적 성능(소화율, 아미노산 조성, 병원체 무함유 상태)을 입증해야 합니다. Calysta사의 FeedKind는 어분과 비교해 경쟁력 있는 위치를 차지하고 있지만, 틈새 용도를 넘어 규모를 확대하기 위해서는 수년에 걸친 공급 계약과 검증 시험이 필요하기 때문에 시장 침투가 지연되는 요인이 되고 있습니다. DSM-Firmenich가 실시한 무지개송어 실험에서는 단세포 단백질을 20% 배합했을 때 어분과 동등한 성능이 나타났으나, 장기적인 성능 데이터와 수출 시장 전반에 걸친 규제 기준이 명확하지 않아 사료 배합 업체들은 여전히 새로운 원료 도입에 신중한 태도를 보이고 있습니다. 2031년까지의 수산 사료 시장의 연평균 성장률(CAGR)과 단세포 단백질 시장 점유율은 전환 위험을 상쇄하고 공급망 통합에 공동 투자할 의사가 있는 주요 고객을 확보할 수 있느냐에 달려 있습니다.

부문별 분석

2025년, 효모 유래 단세포 단백질은 업계의 주요 발전에 힘입어 41.96%의 시장 점유율을 차지했습니다. 안숙(Angel Yeast)이 이창에 신설한 연간 생산량 1만 1,000톤 규모의 시설(2025년 11월부터 가동)이 이러한 성장에 크게 기여했습니다. 또한, 콴(Quorn)의 연간 약 2만 4,000톤에 달하는 마이코단백질 생산 능력과 라렘망(Lallemand)의 효모 추출물 및 영양 제품에 관한 광범위한 세계 포트폴리오가 이 부문의 입지를 한층 더 공고히 했습니다. 효모 단백질 생산은 수십 년에 걸친 산업용 발효 분야의 전문 지식, 견고하고 확립된 후공정 인프라, 그리고 효모 유래 원료에 대한 소비자들의 폭넓은 친숙도 등 여러 요인의 시너지 효과로 인해 혜택을 보고 있습니다.

세균 유래 단백질은 2026-2031년 연평균 성장률(CAGR) 10.71%를 나타낼 것으로 전망되며, 가장 빠르게 성장하는 원료 부문으로 부상하고 있습니다. 이러한 눈부신 성장은 주로 가스 발효 플랫폼의 발전에 힘입은 것으로, 이를 통해 이산화탄소(CO2), 메탄, 수소가 고단백 바이오매스로 효율적으로 전환됩니다. 이러한 혁신의 대표적인 사례로, 2024년 7월 우드사이드 에너지(Woodside Energy)를 주간사로 하여 시리즈 A 라운드에서 1,800만 달러의 자금을 조달한 NovoNutrients를 들 수 있습니다. 이 자금은 NovoNutrients의 이산화탄소를 단백질로 전환하는 기술의 확대를 목적으로 하고 있습니다. 이러한 동향은 단백질 시장에서 지속 가능하고 확장 가능한 대체재로서 박테리아 유래 단백질의 잠재력이 확대되고 있음을 여실히 보여주고 있습니다.

지역별 분석

2025년 기준으로 유럽은 32.86%의 시장 점유율을 차지했으며, 이는 해당 지역의 선진적인 규제 체계와 확립된 산업 인프라를 반영한 것입니다. 네덜란드 등 여러 국가들은 수입 의존도를 낮추고 국내 미생물 단백질 생산을 강화하기 위한 국가 단백질 전략을 추진하고 있습니다. 이 지역은 대체 단백질에 대한 소비자의 높은 수용도와, 단세포 단백질 도입을 지원하는 지속가능성을 중시하는 정책의 혜택을 받고 있습니다. 주요 발전 사항으로는 신규 단백질 원료에 대한 EU의 승인 및 발효 능력에 대한 대규모 투자가 있습니다. 예를 들어, 핀란드의 Solar Foods사가 운영하는 ‘Factory01’에서는 연간 160톤의 솔레인(Solein)을 생산하고 있습니다. 그러나 복잡한 규제 절차와 성숙한 시장 특유의 제약으로 인해 유럽의 성장률은 아시아태평양 지역에 뒤처지고 있습니다.

아시아태평양은 가장 성장세가 두드러진 지역으로, 2031년까지의 연평균 성장률(CAGR)은 11.91%로 전망됩니다. 이러한 성장은 중국의 바이오 제조 인프라 발전과 단백질 발효에 대한 정부의 지원에 힘입어 이루어지고 있습니다. 또한, 최근 인도에서 사료 생산 및 소비가 확대되면서 시장 수요도 증가하고 있습니다. 싱가포르는 대체 단백질에 대한 규제 승인 과정에서 주도적인 역할을 수행함으로써 지역 혁신 허브로서의 입지를 확고히 하고 있으며, 이를 통해 여러 기업이 제조 허가 및 신규 식품 승인을 획득할 수 있게 되었습니다. 일본과 한국은 정부 프로그램과 기업의 투자를 통해 정밀 발효 역량을 강화하고 있는 반면, 호주는 대체 단백질의 상용화를 위한 종합적인 전략을 시행하고 있습니다.

북미는 유리한 규제 환경과 막대한 벤처 캐피털 투자의 혜택을 누리고 있습니다. 이 기업은 NovoNutrients의 1,800만 달러 규모 시리즈 A 투자 유치와 같은 대규모 자금 조달 외에도, 미생물 유래 단백질에 대한 여러 건의 ‘일반적으로 안전하다고 인정되는(GRAS)’ 승인을 획득했습니다. 이 지역의 역동적인 혁신 생태계는 생명공학 스타트업과 기존 식품 기업 간의 파트너십을 통해 신속한 상용화를 촉진하고 있습니다. 한편, 남미와 중동 및 아프리카는 단백질 수요 증가와 투자 관심 고조를 배경으로 유망한 시장으로 부상하고 있습니다. 예를 들어, Unibio사는 생산 능력 확대를 위해 사우디 산업 투자 그룹으로부터 7,000만 달러의 자금을 조달하는 데 성공했습니다. 이러한 지역에서는 규제 체계가 어떻게 마련되느냐에 따라, 동물사료 및 향후 인간용 영양 시장에서의 단일 세포 단백질 도입에 큰 기회가 있을 것으로 기대됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the single-cell protein market was valued at 12.33 billion in 2025, and is expected to grow from USD 13.12 billion in 2026 to USD 20.94 billion by 2031, registering a CAGR of 9.80% over 2026-2031.

This report is Segmented by Source (Algae, Yeast, Fungi, Bacteria), Application (Animal Feed and Pet Food, Food and Beverages, Dietary Supplements, Other Applications), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Single Cell Protein Market Trends and Insights

Rising demand for alternative protein sources

Population growth and shifting dietary preferences are widening the global protein gap, and single-cell protein offers a land- and water-efficient solution that fits national food-security agendas in China, India, and Singapore. Import-reliant economies view microbial protein as a hedge against soybean and fishmeal volatility, while leading producers such as Angel Yeast and Calysta are reaching cost parity with traditional feed proteins at scale. Angel Yeast's AngeoPro yeast protein, with 96% protein utilization and 47% essential amino acid content, is positioned to substitute whey and soy in protein bars, cereals, and alternative meats. Singapore's Food Agency approved multiple mycoprotein and precision-fermented ingredients in 2024, enabling rapid commercialization in a market targeting 30% nutritional self-sufficiency by 2030. The convergence of food-security mandates, import-substitution policies, and consumer willingness to adopt blended meat products is accelerating procurement by multinational food companies and regional brands.

Sustainability and environmental concerns

Life-cycle studies indicate that microbial protein can cut greenhouse-gas emissions by up to 97% relative to beef, attracting companies racing to meet science-based targets. EU farm-to-fork strategies favor low-emission ingredients, and the European Food Safety Authority's 2025 positive opinion for Fermotein illustrates momentum toward carbon-negative proteins in the mainstream food supply. Steel mills and refineries are piloting LanzaTech's CO2-to-protein modules, turning pollution into revenue while earning carbon credits. Horizon-funded initiatives such as SynoProtein are validating forest-residue feedstocks, broadening the sustainability narrative, and strengthening the single-cell protein market. Regulatory frameworks such as the International Standard Organization's 2021 revision of "protein fibre" definitions to include synthetically produced proteins are formalizing microbial protein as a recognized ingredient category, reducing approval friction and enabling corporate sustainability commitments to translate into procurement mandates.

Competition from established soy/fishmeal proteins

Soybean meal remains the dominant protein source in livestock and aquafeed due to established supply chains, agronomic scale, and commodity pricing mechanisms. Single-cell protein must achieve cost parity or demonstrate superior functional performance (digestibility, amino acid profile, pathogen-free status) to displace incumbent ingredients in price-sensitive feed markets. Calysta's FeedKind positions itself competitively with fishmeal, but scaling beyond niche applications requires multi-year supply agreements and validation trials that delay market penetration. DSM-Firmenich's rainbow trout trials demonstrated that 20% single-cell protein inclusion performs comparably to fishmeal, yet feed formulators remain conservative in adopting novel ingredients without long-term performance data and regulatory clarity across export markets. The aquafeed market's CAGR through 2031, and single-cell protein's share will depend on securing anchor customers willing to absorb transition risk and co-invest in supply-chain integration.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of aqua-/animal feed and pet-food industry

- Advancements in precision-fermentation technology

- Regulatory and consumer-acceptance hurdles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, yeast-based single-cell protein commanded a 41.96% market share, driven by several key developments in the industry. Angel Yeast's newly commissioned 11,000-tonne-per-year facility in Yichang (operational from November 2025) significantly contributed to this growth. Additionally, Quorn's mycoprotein production capacity, which is approximately 24,000 tonnes annually, and Lallemand's extensive global portfolio of yeast extracts and nutritional products further strengthened the segment's position. Yeast protein production benefits from a combination of factors, including decades of industrial fermentation expertise, a robust and well-established downstream processing infrastructure, and widespread consumer familiarity with yeast-derived ingredients.

Bacterial protein is rapidly emerging as the fastest-growing source segment, with a projected compound annual growth rate (CAGR) of 10.71% from 2026 to 2031. This remarkable growth is primarily driven by advancements in gas-fermentation platforms, which efficiently convert carbon dioxide (CO2), methane, and hydrogen into high-protein biomass. A notable example of this innovation is NovoNutrients, which raised USD 18 million in Series A funding in July 2024, with Woodside Energy leading the investment. This funding aims to scale NovoNutrients' CO2-to-protein technology. These developments highlight the growing potential of bacterial proteins as a sustainable and scalable alternative in the protein market.

Geography Analysis

In 2025, Europe holds a 32.86% market share, reflecting its advanced regulatory frameworks and well-established industrial infrastructure. Countries such as the Netherlands are leading efforts with national protein strategies aimed at reducing import reliance and enhancing domestic microbial protein production. The region benefits from strong consumer acceptance of alternative proteins and sustainability-driven policies that support single-cell protein adoption. Key developments include EU approvals for novel protein sources and significant investments in fermentation capacity, such as Solar Foods' Factory01 in Finland, which produces 160 tons of Solein annually. However, Europe's growth rate lags behind that of the Asia-Pacific due to complex regulatory processes and the constraints of a mature market.

Asia-Pacific is the fastest-growing region, with an 11.91% CAGR projected through 2031. This growth is driven by China's advancements in biomanufacturing infrastructure and government support for protein fermentation. India's animal feed growth and consumption over recent years have also boosted market demand. Singapore has established itself as a regional innovation hub through its leadership in alternative protein regulatory approvals, enabling multiple companies to secure manufacturing licenses and novel food authorizations. Japan and South Korea are enhancing their precision fermentation capabilities through government programs and corporate investments, while Australia is implementing comprehensive strategies to commercialize alternative proteins.

North America benefits from a favorable regulatory environment and substantial venture capital investments. Companies have secured significant funding, such as NovoNutrients' USD 18 million Series A round, alongside multiple Generally Recognized as Safe (GRAS) approvals for microbial proteins. The region's dynamic innovation ecosystem fosters rapid commercialization through partnerships between biotech startups and established food companies. Meanwhile, South America and the Middle East and Africa are emerging as promising markets, driven by increasing protein demand and growing investment interest. For instance, Unibio secured USD 70 million from the Saudi Industrial Investment Group to expand its production capacity. These regions offer significant opportunities for Single Cell Protein adoption in animal feed and potential human nutrition markets, contingent on the development of their regulatory frameworks.

- Calysta

- Solar Foods

- 3FBIO Ltd.

- Unibio A/S

- Quorn Foods (Marlow Foods)

- KnipBio

- Corbion NV

- Alltech

- AngelYeast

- Cargill Inc.

- DSM-Firmenich AG

- Cyanotech Corporation

- NovoNutrients

- Deep Branch Biotech

- Kiverdi

- Mycorena

- String Bio

- Lallemand Inc.

- EniferBio (Enifer)

- The Protein Brewery

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for alternative protein sources

- 4.2.2 Sustainability and environmental concerns

- 4.2.3 Expansion of aqua-/animal feed and pet-food industry

- 4.2.4 Advancements in precision-fermentation technology

- 4.2.5 Carbon-capture based single cell protein production economics

- 4.2.6 Custom amino-acid profile products for sports nutrition

- 4.3 Market Restraints

- 4.3.1 Competition from established soy/fishmeal proteins

- 4.3.2 High CAPEX and operating costs of large-scale bioreactors

- 4.3.3 Regulatory and consumer-acceptance hurdles

- 4.3.4 Feed-gas and molasses price volatility

- 4.4 Raw Material Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Supply Chain Analysis

- 4.8 Porter's Five Forces

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 Source

- 5.1.1 Algae

- 5.1.2 Yeast

- 5.1.3 Fungi

- 5.1.4 Bacteria

- 5.2 Application

- 5.2.1 Animal Feed and Pet Food

- 5.2.2 Food and Beverages

- 5.2.3 Dietary Supplements

- 5.2.4 Other Applications

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 Italy

- 5.3.2.4 France

- 5.3.2.5 Spain

- 5.3.2.6 Netherlands

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 South Africa

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Positioning Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Calysta

- 6.4.2 Solar Foods

- 6.4.3 3FBIO Ltd.

- 6.4.4 Unibio A/S

- 6.4.5 Quorn Foods (Marlow Foods)

- 6.4.6 KnipBio

- 6.4.7 Corbion NV

- 6.4.8 Alltech

- 6.4.9 AngelYeast

- 6.4.10 Cargill Inc.

- 6.4.11 DSM-Firmenich AG

- 6.4.12 Cyanotech Corporation

- 6.4.13 NovoNutrients

- 6.4.14 Deep Branch Biotech

- 6.4.15 Kiverdi

- 6.4.16 Mycorena

- 6.4.17 String Bio

- 6.4.18 Lallemand Inc.

- 6.4.19 EniferBio (Enifer)

- 6.4.20 The Protein Brewery