|

시장보고서

상품코드

2062333

고반응성 폴리이소부틸렌 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Highly Reactive Polyisobutylene - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

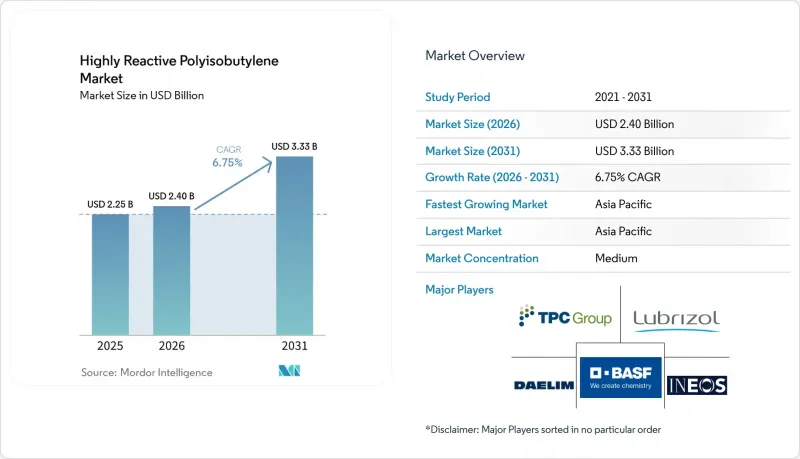

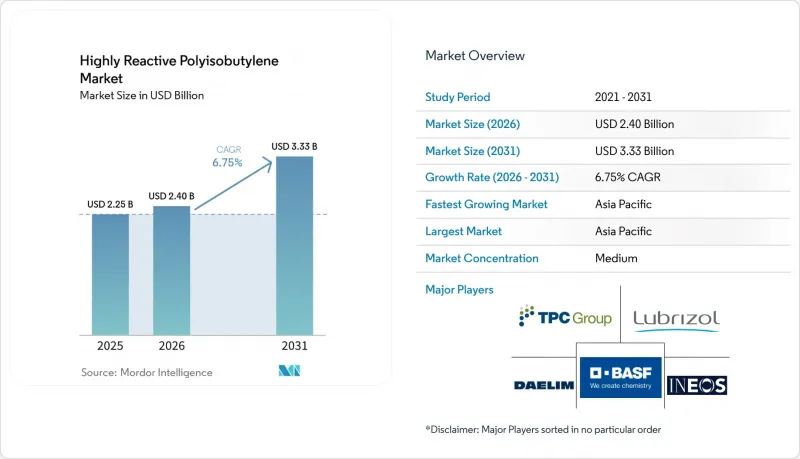

Mordor Intelligence에 의하면, 고반응성 폴리이소부틸렌 시장 규모는 2025년에 22억 5,000만 달러, 2026년에 24억 달러가 되어, 2031년까지 33억 3,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 6.75%로 성장할 전망입니다.

본 보고서는 분자량(1,000 g/mol 미만, 1,000-2,500 g/mol, 2,500 g/mol 초과), 용도(접착제, 윤활제·분산제 등), 최종 사용자 산업(자동차 및 운송 등), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 고반응성 폴리이소부틸렌 시장 동향 및 분석

연료 및 윤활유 첨가제에 대한 수요 증가

밀도 함수 이론과 엔진 시험을 결합한 2025년 동료 심사 논문에 따르면, 3.5-4.0%의 질소를 함유한 폴리이소부틸렌삭시니미드(PIBSI) 분산제는 금속계 세정제와 비교하여 저속 영역에서의 예연소를 98% 억제하고, 터보차저의 침전물을 90% 감소시켰습니다. Mack T-11 시험에서 분산제의 아민기가 그을음에 흡착되고 소수성 PIB 사슬이 응집을 방지했기 때문에 점도 상승을 20% 미만으로 억제할 수 있었습니다. 중국과 인도는 황산 회분 함량을 0.5%, 인 함량을 0.08%로 제한함으로써 이러한 추세를 뒷받침했으며, 그 결과 디알킬디티오포스페이트 아연의 사용을 사실상 배제했습니다.

전기차 조립 과정에서 접착제 및 실런트 소비량 급증

습기 유입을 막고 열폭주 가스를 봉쇄하기 위해, 전기차 배터리 팩에는 1유닛당 8-12m의 PIB계 부틸 코드와 200-400g의 핫멜트 실란트가 사용됩니다. 헨켈의 ‘LOCTITE RB EV 9740’ 코드 및 H.B. 풀러의 ‘EV SEAL 500’ 등급은 10?¹ cm³·cm/cm²·s·Pa 이하의 헬륨 투과성을 자랑하며, 150°C까지의 온도를 견딜 수 있고, 1,000시간의 사이클 시험에서 아크릴계 제품을 능가하는 성능을 보여주고 있습니다. 2030년까지 전 세계 전기차 생산 대수가 2,000만 대를 넘어설 것으로 예상되며, 이는 연간 최대 2만 톤의 PIB 수요 증가에 해당합니다.

변동이 심한 이소부틸렌 가격

2025년 4분기, 중국의 이소부틸렌 가격은 톤당 평균 1,038달러였던 반면, 미국에서는 톤당 1,187달러였습니다. 이는 정유시설의 가동률 차이에 기인한 것입니다. 엑슨모빌과 INEOS AG는 자사의 유동 접촉 분해(FCC) 공정을 활용하여 수익성을 유지한 반면, 시중에서 이소부틸렌을 구매하는 데 의존하는 비통합형 폴리이소부틸렌(PIB) 생산업체들은 수익성 악화로 인해 신규 플랜트 투자를 축소했습니다.

부문별 분석

중분자량 등급은 2025년 매출의 50.87%를 차지하며, 반응성 폴리이소부틸렌 시장에서 주요 성장 동력으로서의 입지를 확고히 했습니다. 감압 접착제나 폴리이소부틸렌 숙신산 무수물(PIBSA) 분산제로의 용도에 따라, 포장 및 윤활유 양 분야에서 안정적인 수요가 확보되고 있습니다. 고분자량 등급(2,500 g/mol 초과)은 연평균 성장률(CAGR) 6.63%를 기록했으며, 100°C에서 300,000 센티스톡스(cSt) 이상의 점도가 필요한 배터리용 바인더나 케이블용 플러딩 컴파운드 분야에서 채택이 확대되고 있습니다.

동남아시아의 케이블 제조업체들은 바셀린에서 PIB가 풍부하게 함유된 충전 페이스트로의 전환 과정에서 2kV/mm를 초과하는 절연 내력을 중요한 요소로 간주하고 있으며, 이에 따라 수요 전망이 안정적일 것으로 보입니다. 반면, 저분자량 PIB(1,000 g/mol 미만)는 정유시설의 알킬화 공정의 경제성으로 인해 성장세가 둔화되고 있습니다. 이는 옥탄 스프레드가 확대되면 이소부틸렌이 휘발유 혼합용으로 전용되어, 이 특수 폴리머공급이 제한되기 때문입니다.

지역별 분석

아시아태평양은 2025년 매출의 47.03%를 차지하며 연평균 성장률(CAGR) 7.32%로 성장하고 있습니다. 이러한 성장은 합성 윤활유 분야에서 중국의 자급자족을 위한 노력과, 한국의 대림(Daelim) 여수 공장의 비용 효율화에 힘입은 것입니다. 2031년까지 해당 지역의 고반응성 폴리이소부틸렌 시장 점유율은 50%를 넘어설 것으로 예측됩니다. 이러한 증가는 중국의 VI-B 배기가스 기준을 준수하기 위해 지역 블렌더들이 승용차용 오일 내 폴리이소부틸렌설포니미드(PIBSI)의 배합 비율을 높이고 있기 때문입니다.

북미는 통합된 밸류체인에 힘입어 전 세계 소비량의 상당 부분을 차지하고 있습니다. TPC 그룹, 엑슨모빌, INEOS 등의 기업들은 유동 접촉 분해(FCC) 공정에서 생산된 이소부틸렌을 자사의 폴리이소부틸렌(PIB), 폴리이소부틸렌 숙신산 무수물(PIBSA) 및 세제 생산 시설에 직접 공급하고 있습니다. 2024년, TPC 그룹은 지이소부틸렌의 생산 능력을 27% 확대하고, 키갈리 개정안에 부합하는 지구온난화지수(GWP)가 낮은 냉매용 윤활유 공급 체계를 구축했습니다.

유럽에서는 주요 업계 관계자들이 기여했습니다. BASF의 루트비히스하펜 및 안트베르펜 공장은 중분자량 등급에 중점을 두고 있으며, 이 제품들은 유로 7 시험용 차량을 위한 저황산회·저인·저황(low-SAPS) 엔진 오일 배합에 사용되고 있습니다. 휘발성 유기 화합물(VOC)에 대한 엄격한 규제로 인해 건설용 실런트 생산량은 감소했으나, 탄소 중립 건축물에서 통기성 막에 대한 수요가 특수 폴리이소부틸렌(PIB)의 소비를 지탱하고 있습니다. 남미 및 중동 및 아프리카는 합쳐서 5% 미만을 차지할 뿐이지만, 이소부틸렌 추출과 특수 폴리머 생산을 통합한 사우디아라비아의 110억 달러 규모 ‘아미랄’ 석유화학 단지가 2027년에 가동을 시작함에 따라 성장이 예상됩니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 A.타이틀과 목차

제2장 목차-고반응성 폴리이소부틸렌 시장

제3장 서론

제4장 조사 방법

제5장 주요 요약

제6장 시장 구도

제7장 시장 규모와 성장 예측

제8장 경쟁 구도

제9장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the highly reactive polyisobutylene market size is projected to be USD 2.25 billion in 2025, USD 2.40 billion in 2026, and reach USD 3.33 billion by 2031, growing at a CAGR of 6.75% from 2026 to 2031.

This report is Segmented by Molecular Weight (Less Than 1, 000 G/Mol, 1, 000-2, 500 G/Mol, Greater Than 2, 500 G/Mol), Application (Adhesives, Lubricant Dispersants, and More), End-User Industry (Automotive and Transportation and More), Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Highly Reactive Polyisobutylene Market Trends and Insights

Rising Demand for Fuel and Lubricant Additives

According to a 2025 peer-reviewed study that combined density-functional theory with engine testing, polyisobutenyl succinimide (PIBSI) dispersants, containing 3.5-4.0% nitrogen, achieved a 98% suppression of low-speed pre-ignition and a 90% reduction in turbocharger deposits compared to metallic detergents. In Mack T-11 trials, the amine centers of the dispersants anchored to soot, while the hydrophobic PIB tails prevented agglomeration, ensuring viscosity rise remained below 20%. China and India bolstered this trend by imposing caps on sulfated ash at 0.5% and phosphorus at 0.08%, effectively sidelining the use of zinc dialkyldithiophosphate.

Surge in Adhesive and Sealant Consumption in EV Assembly

To prevent moisture ingress and contain thermal-runaway gases, electric-vehicle battery packs utilize 8-12 m of PIB-based butyl cord and 200-400 g of hot-melt sealant per unit. Henkel's LOCTITE RB EV 9740 cord and H.B. Fuller's EV SEAL 500 grade boast helium permeability below 10-1° cm3*cm/cm2*s*Pa and can withstand temperatures up to 150°C, surpassing acrylic counterparts in 1,000-hour cycling tests. With global EV assembly projected to exceed 20 million units by 2030, this translates to an additional PIB demand of up to 20,000 t/y.

Volatile Isobutylene Prices

In Q4 2025, isobutylene prices averaged USD 1,038 per ton in China, compared to USD 1,187 per ton in the United States, driven by differences in refinery run rates. Exxon Mobil Corporation and INEOS AG utilized their captive Fluid Catalytic Cracking (FCC) streams to sustain profit margins, while non-integrated Polyisobutylene (PIB) producers, dependent on merchant isobutylene purchases, reduced new plant investments due to margin pressures.

Other drivers and restraints analyzed in the detailed report include:

- Accelerated Capacity Additions in Asia-Pacific

- Emerging Role of HR-PIB as Binder in Solid-State Batteries

- Stringent VOC and Carbon-Footprint Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Medium-molecular-weight grades accounted for 50.87% of the 2025 revenue, establishing them as key contributors in the reactive polyisobutylene market. Their application in pressure-sensitive adhesives and polyisobutylene succinic anhydride (PIBSA) dispersants ensures consistent demand from both packaging and lubricant sectors. High-molecular-weight grades (exceeding 2,500 g/mol) recorded a 6.63% compound annual growth rate (CAGR), gaining adoption in battery binders and cable flooding compounds that require viscosities above 300,000 centistokes (cSt) at 100 °C.

Southeast Asian cable manufacturers identify dielectric strength exceeding 20 kilovolts per millimeter (kV/mm) as a critical factor in transitioning from petroleum jelly to PIB-enriched flooding pastes, indicating a stable demand outlook. In contrast, low-molecular-weight PIB (below 1,000 g/mol) shows slower growth due to refinery alkylate economics, which diverts isobutylene into gasoline blending when octane spreads widen, limiting the availability of this specialty polymer.

Geography Analysis

Asia-Pacific, accounting for 47.03% of 2025's revenue, is growing at a 7.32% compound annual growth rate (CAGR). This growth is supported by China's efforts toward self-reliance in synthetic lubricants and the cost efficiencies achieved at Daelim's Yeosu site in South Korea. By 2031, the region's share in the highly reactive polyisobutylene market is expected to exceed 50%. This increase is driven by regional blenders raising polyisobutylene succinimide (PIBSI) inclusion rates in passenger-car oils to comply with China VI-B emission standards.

North America accounted for a significant portion of global consumption, supported by integrated value chains. Companies such as TPC Group, ExxonMobil, and INEOS direct fluid catalytic cracking (FCC)-sourced isobutylene into their proprietary polyisobutylene (PIB), polyisobutylene succinic anhydride (PIBSA), and detergent production facilities. In 2024, TPC Group expanded its diisobutylene capacity by 27%, positioning itself to supply low-global warming potential (GWP) refrigerant lubricants in compliance with the Kigali Amendment.

Europe contributed through key industry players. BASF's facilities in Ludwigshafen and Antwerp focus on medium-molecular-weight grades, which are used in low-sulfated ash, phosphorus, and sulfur (low-SAPS) engine-oil packages for Euro-7 test fleets. Although strict volatile organic compound (VOC) limits have reduced construction sealant volumes, demand for breathable membranes in net-zero buildings has supported specialty polyisobutylene (PIB) consumption. South America and the Middle East-Africa, together accounting for less than 5%, may see growth following the 2027 start-up of Saudi Arabia's USD 11 billion Amiral petrochemical complex, which integrates isobutylene extraction with specialty polymer production.

- BASF

- Braskem

- Chemex Chemicals

- Chevron Oronite Company LLC

- China Petroleum & Chemical Corporation

- Daelim Co., Ltd.

- ExxonMobil Chemical

- INEOS AG

- Infineum International Limited

- Janex S.A.

- Kothari Petrochemicals Limited

- KZJ New Materials Group Co., Ltd.

- Lubrizol

- LyondellBasell Industries Holdings B.V.

- RB Products, Inc.

- Shandong Orient Hongye Chemical Co., Ltd.

- TPC Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 A. Title and Table of Contents

2 Table of Contents - Highly Reactive Polyisobutylene Market

3 Introduction

- 3.1 Study Assumptions and Market Definition

- 3.2 Scope of the Study

4 Research Methodology

5 Executive Summary

6 Market Landscape

- 6.1 Market Overview

- 6.2 Market Drivers

- 6.2.1 Rising demand for fuel and lubricant additives

- 6.2.2 Surge in adhesive and sealant consumption in EV assembly

- 6.2.3 Accelerated capacity additions in Asia-Pacific

- 6.2.4 Regulatory push for low-SAPS and Euro-7-compliant engine oils

- 6.2.5 Emerging role of HR-PIB as binder in solid-state batteries

- 6.2.6 Commercialization of bio-based isobutylene feedstock

- 6.3 Market Restraints

- 6.3.1 Volatile isobutylene prices

- 6.3.2 Stringent VOC and carbon-footprint regulations

- 6.3.3 Growing preference for silicone-free sealants in construction

- 6.3.4 High CAPEX for ultra-low-temperature BF3 polymerization lines

- 6.4 Value Chain Analysis

- 6.5 Porter's Five Forces

- 6.5.1 Bargaining Power of Suppliers

- 6.5.2 Bargaining Power of Buyers

- 6.5.3 Threat of New Entrants

- 6.5.4 Threat of Substitutes

- 6.5.5 Competitive Rivalry

7 Market Size and Growth Forecasts (Value)

- 7.1 By Molecular Weight

- 7.1.1 Less than 1,000 g/mol (Low)

- 7.1.2 1,000-2,500 g/mol (Medium)

- 7.1.3 Greater than 2,500 g/mol (High)

- 7.2 By Application

- 7.2.1 Adhesives

- 7.2.2 Lubricant Dispersants

- 7.2.3 Fuel Detergents

- 7.2.4 Sealant Tapes

- 7.2.5 Cable Compounds and Others

- 7.3 By End-user Industry

- 7.3.1 Automotive and Transportation

- 7.3.2 Industrial Machinery

- 7.3.3 Oil and Gas/Refining

- 7.3.4 Construction and Infrastructure

- 7.3.5 Electrical and Electronics

- 7.4 By Geography

- 7.4.1 Asia-Pacific

- 7.4.1.1 China

- 7.4.1.2 Japan

- 7.4.1.3 India

- 7.4.1.4 South Korea

- 7.4.1.5 ASEAN Countries

- 7.4.1.6 Rest of Asia-Pacific

- 7.4.2 North America

- 7.4.2.1 United States

- 7.4.2.2 Canada

- 7.4.2.3 Mexico

- 7.4.3 Europe

- 7.4.3.1 Germany

- 7.4.3.2 United Kingdom

- 7.4.3.3 France

- 7.4.3.4 Italy

- 7.4.3.5 Spain

- 7.4.3.6 Russia

- 7.4.3.7 Rest of Europe

- 7.4.4 South America

- 7.4.4.1 Brazil

- 7.4.4.2 Argentina

- 7.4.4.3 Rest of South America

- 7.4.5 Middle East and Africa

- 7.4.5.1 Saudi Arabia

- 7.4.5.2 South Africa

- 7.4.5.3 Rest of Middle East and Africa

- 7.4.1 Asia-Pacific

8 Competitive Landscape

- 8.1 Market Concentration

- 8.2 Strategic Moves

- 8.3 Market Share(%)/Ranking Analysis

- 8.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, Recent Developments)

- 8.4.1 BASF

- 8.4.2 Braskem

- 8.4.3 Chemex Chemicals

- 8.4.4 Chevron Oronite Company LLC

- 8.4.5 China Petroleum & Chemical Corporation

- 8.4.6 Daelim Co., Ltd.

- 8.4.7 ExxonMobil Chemical

- 8.4.8 INEOS AG

- 8.4.9 Infineum International Limited

- 8.4.10 Janex S.A.

- 8.4.11 Kothari Petrochemicals Limited

- 8.4.12 KZJ New Materials Group Co., Ltd.

- 8.4.13 Lubrizol

- 8.4.14 LyondellBasell Industries Holdings B.V.

- 8.4.15 RB Products, Inc.

- 8.4.16 Shandong Orient Hongye Chemical Co., Ltd.

- 8.4.17 TPC Group

9 Market Opportunities and Future Outlook

- 9.1 White-space and Unmet-need Assessment