|

시장보고서

상품코드

2062390

재활용 납 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Recycled Lead - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

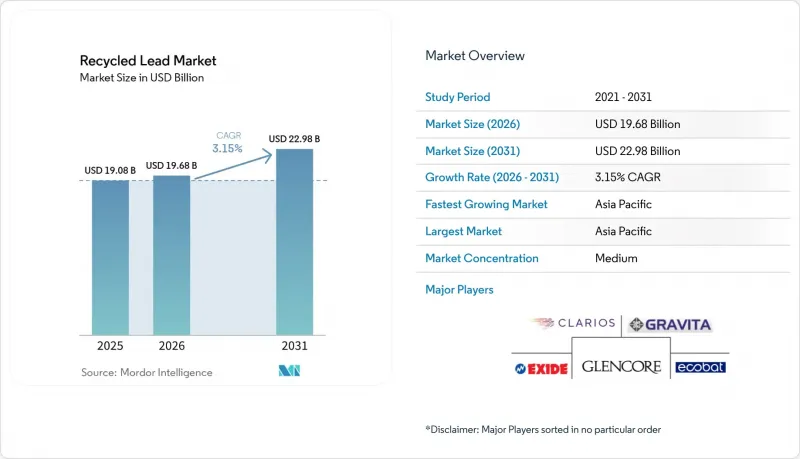

Mordor Intelligence에 의하면, 재활용 납 시장 규모는 2025년에 190억 8,000만 달러로 평가되었습니다. 2026년에 196억 8,000만 달러에 달하고, 2031년까지 229억 8,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년에 걸쳐 CAGR은 3.15%를 나타낼 전망입니다.

본 보고서는 원료의 유형(사용 후 납축전지, 납 스크랩 등), 재활용 방법(열법, 습법 등), 형태(재활용 납 잉곳, 재활용 납 합금 등), 최종 사용자 산업(자동차-SLI, 에너지 저장 시스템 등) 및 지역(아시아태평양, 북미 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 재활용 납 시장 동향 및 분석

지속 가능하고 순환형 경제 실천에 대한 수요 증가

순환형 경제와 관련된 규제로 인해 자동차 제조업체와 산업용 배터리 구매자들의 조달 전략이 변화하고 있습니다. 유럽연합(EU)은 2025년까지 회수율 75%, 2027년까지 납 회수율 90%를 달성하도록 제조업체에 의무화하고 있으며, 이에 따라 OEM(원청 브랜드 제조업체)은 인증된 재활용 업체와 장기 공급 계약을 체결하도록 장려받고 있습니다. 미국에서는 2차 제련소에 대한 NESHAP(국가대기오염방지법) 규제로 인해 규정 준수 비용은 증가하고 있지만, 도시 지역 시설 주변의 대기 질은 개선되고 있습니다. 대형 종합 기업들은 소규모 사업자가 도입하기 어려운 스크러버나 전기 집진 장치와 같은 첨단 기술을 도입하고 있으며, 이것이 재활용 납 시장의 재편을 촉진하고 있습니다. 배터리 제조업체들은 특히 2024년 인도네시아와 호주가 납광석 수출을 제한한 것을 계기로, 1차 광산에서공급 중단에 대비한 안전책으로서 재활용 납을 활용하고 있습니다. 그 결과, 재활용 납 시장은 보다 광범위한 배터리 밸류체인에서 전략적 중요성이 커지고 있습니다.

자동차 및 고정형 에너지 저장 시스템에서 납축전지의 이용 확대

2024년 전 세계 자동차 생산 대수는 8,500만 대를 넘어섰으며, 내연기관 차량 1대당 SLI 배터리 1개가 필요하기 때문에 재활용 납 시장의 기초적인 수요는 유지되고 있습니다. 전기자동차조차 안전 시스템을 위해 12볼트 보조 배터리 팩을 사용하고 있으므로, 재활용 납의 중요성은 앞으로도 계속될 것이 확실합니다. 인도 및 아프리카의 통신탑은 현재 60만 기를 넘어섰으며, 불안정한 전력망 상황에 대처하기 위해 VRLA 배터리에 의존하고 있어 고철 공급원이 확대되고 있습니다. 데이터센터 사업자들로부터 2025년에 예비 전원용 배터리 출하량이 15% 증가했다는 보고가 접수되면서, 고정형 에너지 저장 시장의 성장이 두드러지고 있습니다. 재활용 업체들은 VRLA 스크랩에서 얻어지는 고순도 산화납의 혜택을 누리고 있으며, 이는 5%-8%의 가격 프리미엄을 가져와 재활용 납 시장의 이익률을 끌어올리고 있습니다.

비공식 재활용 수거 장소에서 발생하는 환경 및 건강 위험

인도나 나이지리아 등 규제가 없는 재활용 시설에서 일하는 노동자들의 경우, 혈중 납 농도가 40µg/dL을 초과하는 사례가 빈번하게 확인되고 있으며, 이는 세계보건기구(WHO)의 지침인 5µg/dL을 크게 상회하는 수치입니다. 이러한 시설에서 배출되는 폐수는 관개 수로를 오염시켜 지역 사회의 우려를 불러일으키며, 때로는 공장 폐쇄로 이어지기도 합니다. 바젤 협약에서는 밀폐식 소각로 및 슬래그 안정화가 규정되어 있으나, 여전히 이행 미비 사항이 존재하고 있으며, 이로 인해 가격 경쟁이 심화되어 규제를 준수하는 사업자의 이익률이 하락하고 있습니다. 배터리 제조업체들은 평판 위험을 피하기 위해 공급망 감사를 강화하고 있습니다. 비공식 시설을 ISO 14001 규격에 부합하도록 하려면 1개 사업장당 50만-100만 달러의 비용이 소요되지만, 많은 사업자가 이러한 재정적 부담을 감당하지 못해, 그 결과 정식 납 재활용 시장으로 유입되는 고철량이 일시적으로 감소하고 있습니다.

부문별 분석

2025년에는 사용 후 납축전지(ULAB)가 재활용 납 시장의 73.89%를 차지하면서, 원료 확보에 있어 사용 후 SLI 및 VRLA 유닛이 수행하는 매우 중요한 역할이 부각되었습니다. 산업 폐기물 및 슬러지는 가장 빠르게 성장하고 있는 공급원이며, 전자기기 및 금속 성형 잔여물 처리에 관한 규제 강화에 힘입어 2031년까지의 연평균 성장률(CAGR)은 3.58%로 예측됩니다. 슬러지 및 공장 스크랩으로의 사업 확대는 처리 업체 입장에서 ULAB 유입 변동에 따른 수익 안정화에 기여하는 것으로, 대기업에서는 이미 이 전략을 채택하고 있습니다.

산업 폐기물은 황산염 중화나 탄산염 제거와 같은 처리가 필요하지만, 그 고순도 산화물 함량은 일관성을 중시하는 배터리 페이스트 제조업체에게 매력적입니다. 아쿠아 메탈즈(Aqua Metals)사의 ‘AquaRefining’ 시스템은 상온에서 가동되며, ULAB용으로 설계되어 있어 고로가 필요하지 않아 신규 플랜트의 설비 투자 비용을 약 30% 절감할 수 있습니다. 혼합 원료 전략을 채택한 가공업체들은 유연성을 확보함으로써 재활용 납 시장의 장기적인 안정을 뒷받침하고 있습니다.

2025년에는 연간 5만-10만 톤의 처리 능력을 갖춘 고로가 상당한 규모의 경제를 실현함에 따라, 열야금법을 통한 재활용 납 생산량이 전체의 63.02%를 차지했습니다. 습식 제련법은 에너지 소비량이 40-50% 감소하고 이산화황 배출이 사라진다는 장점 덕분에, 2031년까지 연평균 성장률(CAGR) 3.64%를 나타낼 것으로 예측됩니다.

2026년부터 시행되는 유럽연합(EU)의 탄소국경조정메커니즘(CBAM)에 따라 탄소 집약형 금속에 대한 수입 관세가 부과됨에 따라, 기업들은 용광로에 스크러버를 설치하는 개조 공사를 진행하거나 저온 반응 장치에 대한 투자를 확대하게 될 것입니다. ACE Green Recycling사의 모듈식 전기화학 장치는 가격이 100만 달러 미만이며, 아프리카나 인도 등 지역의 소규모 사업자를 위해 설계되었기 때문에 기술 보급을 가속화할 가능성이 있습니다. 기술의 양극화가 예상됩니다. 즉, 대규모 플랜트는 계속해서 화법(火法)을 통해 배출물을 정제하는 한편, 신규 진출기업들은 ESG 대출 기준에 부합하는 습식 제련법을 채택할 가능성이 높으며, 이로 인해 재활용 납 시장 내 경쟁의 다양성이 강화될 것입니다.

지역별 분석

아시아태평양은 2025년에 45.33%의 점유율로 재활용 납 시장을 주도했으며, 2031년까지 연평균 성장률(CAGR) 3.97%를 기록하며 성장할 것으로 전망됩니다. 중국은 2024년에 배출 규제를 강화하고, 비공식 제련소를 통합하도록 압박하며, 스크러버 및 실시간 감시 시스템 도입 자금을 확보할 수 있는 인가 사업자에게 우대 조치를 취하고 있습니다. 인도의 e-릭샤(전동 삼륜 택시) 생태계는 Gravita India와 같은 재활용 업체에 안정적인 VRLA 폐배터리를 공급하고 있는 반면, 아세안(ASEAN) 국가들에서는 새로운 습식 제련 설비에 대해 세제상의 우대 조치가 제공되고 있습니다. 일본과 한국은 2050년까지 탄소중립을 목표로 하고 있으며, 저탄소 반응로를 시험하는 시범 플랜트를 촉진하고, 재활용 납 시장 전반에 걸친 지역적 기술 보급을 지원하고 있습니다.

북미에서는 회수 효율이 이미 99%를 넘어섰기 때문에 그 이상의 양적 성장에는 한계가 있습니다. 2024년 미국 납·구리 규정의 개정에 따라 시설 개보수가 의무화되면서 고정 비용은 증가했으나, 지역의 대기 질은 개선되었습니다. 캐나다와 멕시코는 제련소의 가동률을 높이기 위해 국경을 넘는 고철 흐름을 통합하고 있으며, 미국의 여러 기업들은 데이터센터의 ESG 조달 규정을 충족하는 고정형 배터리용 프리미엄 산화납으로의 전환을 추진하고 있습니다. 이처럼 재활용 납 시장은 성숙한 회수 인프라와 진화하는 제품 구성에서 비롯된 기회 사이에서 균형을 이루고 있습니다.

유럽 수요는 제품 승인 절차에 재활용 함량 기준을 포함시킨 EU 배터리 규정에 의해 형성되고 있습니다. 독일, 프랑스, 이탈리아에는 ECOBAT이나 Campine과 같이 회수 및 제련을 동일한 거점에 집약하여, 집적에 따른 경제성을 확보하고 있는 수직 통합형 클러스터가 존재합니다. 러시아의 수출 규제로 인해 수요가 국내 및 북아프리카의 재활용 업체로 이동하면서 공급원이 다양해지고 있습니다.

남미와 중동 및 아프리카를 합친 시장 점유율은 2025년에도 낮은 수준에 머물 것으로 전망됩니다. 브라질의 4,000만 대에 달하는 차량 보유 대수는 ULAB(사용 후 납축전지)의 대규모 공급원이 되었지만, 주요 도시권 밖에서는 여전히 비공식 해체장이 존재했습니다. 아랍에미리트(UAE)와 사우디아라비아에서 진행 중인 데이터센터 확충은 VRLA(납산 축전지)의 수입을 촉진하고 있으며, 이러한 축전지들은 금세기 후반에는 폐기물로 처리될 예정입니다. 이로 인해 재활용 납 시장에 지역적 성장 요인이 더해지게 될 것입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the recycled lead market size is projected to be USD 19.08 billion in 2025, USD 19.68 billion in 2026, and reach USD 22.98 billion by 2031, growing at a CAGR of 3.15% from 2026 to 2031.

This report is Segmented by Source Type (Used Lead-Acid Batteries, Lead Scrap, and More), Recycling Method (Pyrometallurgical, Hydrometallurgical, and More), Form (Recycled Lead Ingots, Recycled Lead Alloys, and More), End-User Industry (Automotive - SLI, Energy Storage Systems, and More), and Geography (Asia-Pacific, North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Recycled Lead Market Trends and Insights

Growing Demand for Sustainable and Circular-Economy Practices

Circular-economy regulations are transforming procurement strategies among automakers and industrial battery buyers. The European Union mandates manufacturers to achieve 75% collection efficiency by 2025 and 90% lead recovery by 2027, encouraging original equipment manufacturers to establish long-term supply agreements with certified recyclers. In the United States, NESHAP limits for secondary smelters increase compliance costs but improve air quality near urban facilities. Large integrated firms are adopting advanced technologies like scrubbers and electrostatic precipitators, which smaller operators cannot afford, driving consolidation in the recycled lead market. Battery manufacturers view recycled lead as a safeguard against disruptions in primary-mine supply, particularly after Indonesia and Australia restricted lead-ore exports in 2024. As a result, the recycled lead market is gaining strategic importance within the broader battery value chain.

Rising Use of Lead-Acid Batteries in Automotive and Stationary Storage

Global vehicle production surpassed 85 million units in 2024, with each internal-combustion vehicle requiring an SLI battery, maintaining baseline demand for the recycled lead market. Even battery-electric vehicles use 12-volt auxiliary packs for safety systems, ensuring the continued relevance of recycled lead. Telecom towers in India and Africa now exceed 600,000 units and rely on VRLA batteries to address unreliable grid conditions, expanding the scrap stream. Data-center operators reported a 15% increase in reserve-power battery shipments in 2025, highlighting the growth of stationary storage. Recyclers benefit from VRLA scrap, which provides high-purity lead oxide with a 5%-8% price premium, boosting margins within the recycled lead market.

Environmental and Health Risks in Informal Recycling Clusters

Workers in unregulated recycling facilities in countries like India and Nigeria often record blood-lead levels exceeding 40 µg/dL, far above the World Health Organization guideline of 5 µg/dL. Effluent from these facilities contaminates irrigation channels, raising community concerns and occasionally leading to plant closures. While the Basel Convention prescribes enclosed furnaces and slag stabilization, enforcement gaps persist, enabling price undercutting that reduces margins for compliant operators. Battery manufacturers are increasingly auditing supply chains to avoid reputational risks. Upgrading informal facilities to ISO 14001 standards would cost USD 0.5-1 million per site, a financial burden many operators cannot bear, temporarily reducing scrap flows into the formal recycled lead market.

Other drivers and restraints analyzed in the detailed report include:

- Stringent EHS Regulations That Mandate Lead Recovery

- Cost Advantage of Secondary versus Primary Lead

- Lead-Price Volatility Squeezing Smelter Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Used lead-acid batteries (ULABs) contributed 73.89% of the recycled lead market share in 2025, highlighting the critical role of end-of-life SLI and VRLA units in ensuring feedstock availability. Industrial waste and sludge is the fastest-growing source type, with a CAGR of 3.58% projected through 2031, driven by stricter regulations on the disposal of electronics and metal-forming residues. Expanding into sludge and factory scrap helps processors stabilize revenues against fluctuations in ULAB inflows, a strategy already being utilized by larger firms.

Industrial waste requires processes like sulfate neutralization and carbonate removal, but its high-purity oxide content is appealing to battery paste manufacturers prioritizing consistency. Aqua Metals' AquaRefining system, which operates at room temperature, is designed for ULABs and eliminates the need for blast furnaces, reducing capital costs by approximately 30% for greenfield plants. Processors adopting blended feedstock strategies gain flexibility, supporting the long-term stability of the recycled lead market.

The pyrometallurgical method accounted for 63.02% of recycled lead output in 2025, as blast furnaces with capacities ranging from 50,000 to 100,000 tons per year achieve significant economies of scale. The hydrometallurgical method is expected to grow at a CAGR of 3.64% through 2031, benefiting from 40%-50% lower energy consumption and the elimination of sulfur-dioxide emissions.

The European Union's Carbon Border Adjustment Mechanism, effective from 2026, will impose import fees on carbon-intensive metals, encouraging companies to retrofit furnaces with scrubbers or invest in low-temperature reactors. ACE Green Recycling's modular electrochemical units, priced under USD 1 million, are designed for small operators in regions like Africa and India, potentially accelerating technology adoption. A bifurcation in technology is anticipated: high-volume plants will continue refining pyrometallurgical emissions, while new entrants are likely to adopt hydrometallurgical methods that align with ESG financing criteria, enhancing competitive diversity in the recycled lead market.

Geography Analysis

Asia-Pacific led the recycled lead market with 45.33% share in 2025 and is anticipated to grow at a 3.97% CAGR to 2031. China tightened emission controls in 2024, pushing informal smelters toward consolidation and favoring licensed operators capable of funding scrubbers and real-time monitoring. India's e-rickshaw ecosystem supplies predictable VRLA scrap to recyclers such as Gravita India, while ASEAN economies offer fiscal perks for new hydrometallurgical capacity. Japan and South Korea target carbon neutrality by 2050, stimulating pilot plants that test low-carbon reactors and supporting regional technology diffusion across the recycled lead market.

In North America, collection efficiency already exceeds 99%, capping incremental volume growth. The U.S. Lead and Copper Rule revisions in 2024 forced facility retrofits that raise fixed costs but improve community air quality. Canada and Mexico integrate cross-border scrap flows to buff smelter utilization, and several U.S. players are shifting into premium oxide for stationary storage that meets data-center ESG procurement rules. The recycled lead market thus balances mature collection infrastructure with evolving product-mix opportunities.

Europe's demand is shaped by the EU Battery Regulation that embeds recycled-content thresholds into product approval pathways. Germany, France, and Italy host vertically integrated clusters where ECOBAT and Campine co-locate collection and smelting, securing economies of density. Russia's export restrictions shift demand to domestic and North African recyclers, diversifying supply.

South America, and Middle-East and Africa combined for a lower share in 2025. Brazil's 40 million-vehicle fleet supplies significant ULAB volumes, yet informal yards persist outside major metros. Data-center expansion in the United Arab Emirates and Saudi Arabia stimulates VRLA imports that will transition into scrap later this decade, adding a regional growth vector to the recycled lead market.

- ACE Green Recycling, Inc.

- Aqua Metals, Inc.

- Battery Solutions Inc.

- Campine nv

- Clarios

- East Penn Manufacturing Company

- ECOBAT

- ENERSYS

- EXIDE INDUSTRIES LTD.

- Fenix Battery Recycling

- Glencore

- Gravita India Ltd.

- JAIN RESOURCE RECYCLING LTD.

- KC Recycling

- METALICO

- Pilot Industries Limited

- Pondy Oxides and Chemicals Limited

- Recylex SA

- Terrapure BR Ltd.

- The Doe Run Company

- Wirtz Manufacturing

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for sustainable and circular-economy practices

- 4.2.2 Rising use of lead-acid batteries in automotive and stationary storage

- 4.2.3 Stringent EHS regulations mandating lead recovery

- 4.2.4 Cost advantage of secondary vs. primary lead

- 4.2.5 Ramp-up of VRLA battery demand in emerging micro-mobility markets

- 4.3 Market Restraints

- 4.3.1 Environmental and health risks in informal recycling clusters

- 4.3.2 Lead-price volatility squeezing smelter margins

- 4.3.3 Shrinking scrap availability due to longer battery life

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Source Type

- 5.1.1 Used Lead-Acid Batteries (ULABs)

- 5.1.2 Lead Scrap (cables, roofing, alloys)

- 5.1.3 Industrial Waste and Sludge

- 5.1.4 Other Source Types

- 5.2 By Recycling Method

- 5.2.1 Pyrometallurgical

- 5.2.2 Hydrometallurgical

- 5.2.3 Electrochemical

- 5.2.4 Other Recycling Methods

- 5.3 By Form

- 5.3.1 Recycled Lead Ingots

- 5.3.2 Recycled Lead Alloys

- 5.3.3 Secondary Lead Oxide

- 5.3.4 Other Forms

- 5.4 By End-user Industry

- 5.4.1 Automotive - SLI (Starting, Lighting, and Ignition)

- 5.4.2 Energy Storage Systems

- 5.4.3 Telecom and Data Centers

- 5.4.4 Industrial Equipment

- 5.4.5 Construction and Infrastructure

- 5.4.6 Consumer Electronics

- 5.4.7 Defense and Marine

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 NORDIC Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 ACE Green Recycling, Inc.

- 6.4.2 Aqua Metals, Inc.

- 6.4.3 Battery Solutions Inc.

- 6.4.4 Campine nv

- 6.4.5 Clarios

- 6.4.6 East Penn Manufacturing Company

- 6.4.7 ECOBAT

- 6.4.8 ENERSYS

- 6.4.9 EXIDE INDUSTRIES LTD.

- 6.4.10 Fenix Battery Recycling

- 6.4.11 Glencore

- 6.4.12 Gravita India Ltd.

- 6.4.13 JAIN RESOURCE RECYCLING LTD.

- 6.4.14 KC Recycling

- 6.4.15 METALICO

- 6.4.16 Pilot Industries Limited

- 6.4.17 Pondy Oxides and Chemicals Limited

- 6.4.18 Recylex SA

- 6.4.19 Terrapure BR Ltd.

- 6.4.20 The Doe Run Company

- 6.4.21 Wirtz Manufacturing

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment